Long Term Wealth Building in India: A Practical Blueprint

Shlok Sobti

Long Term Wealth Building in India: A Practical Blueprint

Most people in India want financial security but struggle to build lasting wealth. You earn a decent salary, pay your bills, and save what you can. Yet month after month, your savings barely grow and inflation quietly erodes what little you set aside. The stock market feels risky. Mutual funds confuse you. And expert advice often comes loaded with hidden fees that eat into your returns before you even realize it.

Building wealth over time doesn't require a six figure salary or advanced financial knowledge. It needs a clear plan, disciplined habits, and smart choices that compound over the years. You can grow your money systematically while protecting it from unnecessary risks and costs that others ignore.

This guide breaks down the practical steps to build wealth in India. You'll learn how to set meaningful financial goals, create a solid foundation, invest for long term growth, and keep your wealth protected. Each step is designed for working professionals who want real results without the jargon or complexity that makes financial planning feel overwhelming.

Why long term wealth building matters in India

Your salary might increase by 8% each year, but inflation in India often runs at 6% or higher. This gap means your purchasing power barely grows, and sometimes it shrinks. You need your money to work harder than the cost of living rises, or you'll never escape the cycle of earning, spending, and watching your savings stagnate. The difference between someone who builds wealth and someone who doesn't comes down to making your money multiply through strategic choices over decades, not just saving harder.

The real cost of waiting

Starting early changes everything because compound returns need time to work their magic. A 30 year old who invests ₹10,000 monthly until retirement will accumulate significantly more wealth than a 40 year old who invests ₹20,000 monthly for the same duration. Your younger years give you the single most valuable asset in long term wealth building: time to recover from market dips and capture growth across multiple economic cycles.

Time in the market beats timing the market, and every year you delay costs you exponentially more than the amount you could have invested.

Indians face unique challenges like rising healthcare costs, longer life expectancies, and limited social security. Traditional pension systems don't exist for most private sector employees. You alone are responsible for funding your retirement, your children's education, and your family's medical emergencies. Building wealth systematically protects you from these certainties while giving you the freedom to make life choices based on what you want, not what you can barely afford.

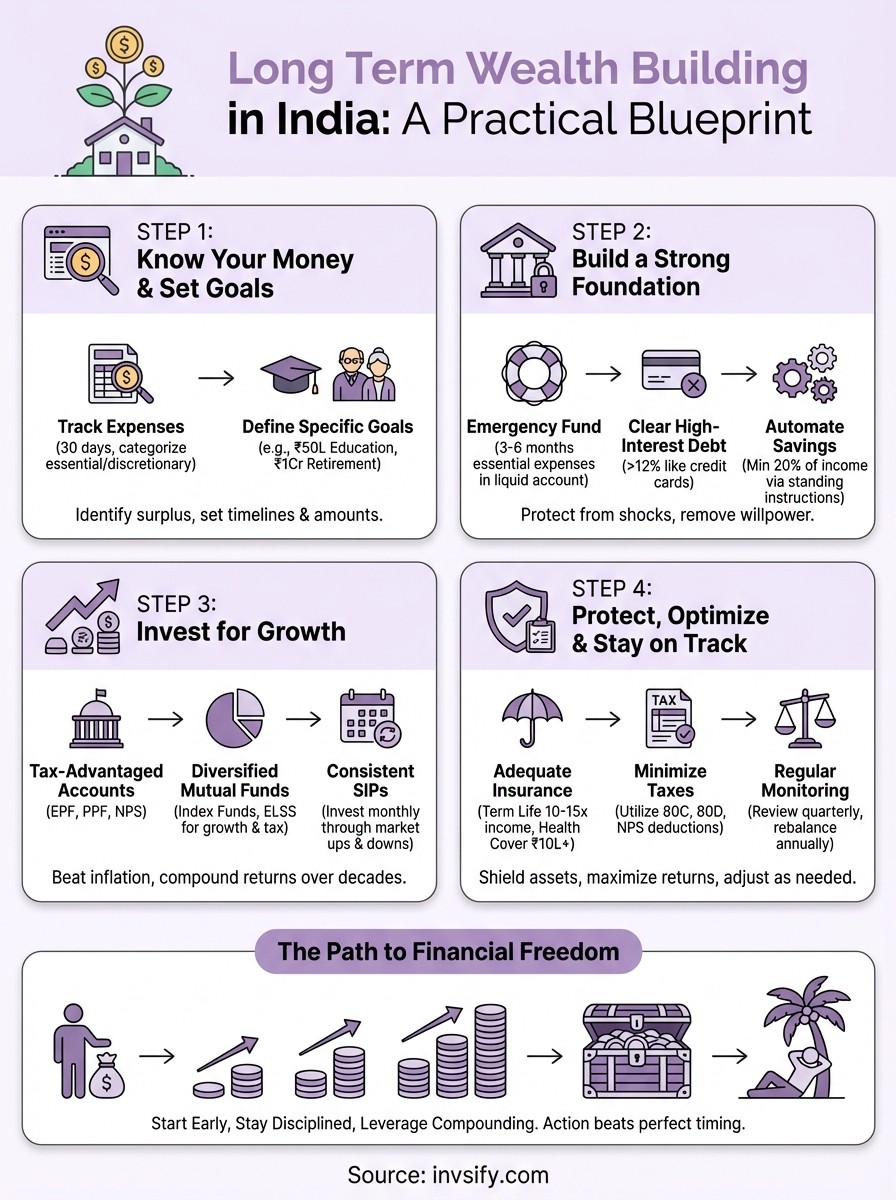

Step 1. Know your money and set clear goals

You cannot build wealth without knowing exactly where your money goes each month. Track your income against your expenses for at least 30 days using a simple spreadsheet or notebook. Write down every transaction, from your morning chai to your rent payment, and categorize each expense as either essential (groceries, utilities, insurance) or discretionary (dining out, entertainment, subscriptions). This exercise reveals spending patterns you've ignored and shows you exactly how much surplus you can direct toward long term wealth building.

Track every rupee that comes and goes

Download your bank statements for the past three months and highlight all recurring expenses. Calculate your monthly average for each category, then identify the top three areas where you spend unnecessarily. Most people discover they waste ₹5,000 to ₹15,000 monthly on forgotten subscriptions, impulse purchases, or convenience spending that adds no real value to their lives.

Create a simple monthly budget by listing your fixed expenses first (rent, EMIs, insurance), then allocating specific amounts to variable categories like food, transport, and personal spending. Leave 10% to 15% as buffer for unexpected costs, but treat your savings and investments as non-negotiable fixed expenses that you pay yourself first, not as whatever remains at month end.

Define what wealth means for you

Set specific financial targets with exact numbers and deadlines rather than vague wishes like "save more money." Write down concrete goals such as ₹50 lakhs for your child's education in 15 years, ₹1 crore retirement corpus by age 60, or ₹20 lakhs emergency fund within 3 years. Each goal needs its own timeline and investment strategy because money needed in 5 years demands different treatment than money you won't touch for 30 years.

Your goals determine every investment choice you make, so clarity here prevents costly mistakes later.

Step 2. Build a strong financial foundation

Strong long term wealth building requires three pillars before you invest a single rupee in the stock market: an emergency fund, freedom from expensive debt, and automated savings. These fundamentals protect you from derailing your wealth plan when unexpected expenses hit or when markets crash exactly when you need money. You build wealth faster when you remove financial stress and create systems that work without constant attention.

Start with an emergency fund you can actually access

Set aside 3 to 6 months of your essential expenses in a separate savings account that you can access within 24 hours. Calculate this by adding up only your must-pay bills like rent, groceries, utilities, insurance premiums, and loan EMIs, then multiply by the number of months based on your job stability. A salaried employee with stable income needs 3 months, while freelancers or business owners should target 6 months because income fluctuates unpredictably.

Keep this emergency money in a high-yield savings account or liquid fund, never in fixed deposits that penalize early withdrawal or equity investments that might lose value when you need them most. Your emergency fund serves one purpose: protecting your long term investments from forced liquidation during medical emergencies, job loss, or urgent family needs. Check your bank's interest rates and switch to accounts offering 6% to 7% annual returns to keep pace with inflation while maintaining instant access.

Eliminate high-interest debt before investing

Pay off all credit card debt and personal loans charging more than 12% interest before you start investing for wealth creation. No investment consistently beats the 36% to 42% annual interest that credit cards charge on outstanding balances, so every rupee you keep in credit card debt costs you more than any market gain you might capture. List all your debts with their interest rates, minimum payments, and outstanding balances in a simple table.

Debt Type | Interest Rate | Outstanding Amount | Monthly Payment |

|---|---|---|---|

Credit Card | 36% | ₹45,000 | ₹5,000 |

Personal Loan | 14% | ₹2,50,000 | ₹8,500 |

Car Loan | 9% | ₹3,00,000 | ₹7,200 |

Target the highest interest debt first while paying minimums on everything else, a strategy that saves you thousands in interest charges over months. Once you clear expensive debt, redirect those same monthly payments directly into your investment accounts rather than treating that money as newly available spending cash.

Automate your savings to remove willpower from the equation

Set up automatic transfers on your salary date that move at least 20% of your income into separate accounts for different goals before you can spend it. Log into your bank's net banking portal and create standing instructions that transfer fixed amounts to your emergency fund, investment accounts, and goal-specific savings without requiring any action from you each month.

Automation removes the daily decision to save or spend, making wealth building effortless and consistent regardless of your mood or circumstances.

Treat these automatic transfers as mandatory expenses you cannot skip, just like your rent or electricity bill. Your remaining balance becomes your true spending money, forcing you to live within realistic means while your wealth grows automatically in the background. Increase your automatic savings by 1% every time you receive a salary hike to scale your wealth building without feeling the pinch in your daily lifestyle.

Step 3. Invest for growth the right way

Your emergency fund and debt repayment create the safety net, but long term wealth building happens through strategic investing that beats inflation by wide margins. Keeping money in savings accounts earning 6% to 7% means you barely keep pace with rising costs, while equity investments historically deliver 12% to 15% annual returns over decades in India. The gap between these returns compounds into millions of rupees over your working life, transforming modest monthly investments into substantial wealth that funds your retirement, your children's education, and your financial independence.

Start with tax-advantaged retirement accounts

Maximize your contributions to the Employee Provident Fund (EPF) first because it offers guaranteed returns around 8.5% annually, complete tax exemption on maturity, and a forced discipline that keeps retirement money locked until you actually need it. Your employer matches your EPF contribution up to certain limits, giving you immediate 100% returns on that portion before any investment gains. Calculate your monthly EPF deduction from your salary slip and consider making Voluntary Provident Fund (VPF) contributions if you want additional guaranteed returns with tax benefits.

Open a Public Provident Fund (PPF) account at any bank or post office and deposit up to ₹1.5 lakhs annually to claim tax deductions under Section 80C while your money grows tax-free for 15 years. PPF currently offers around 7.1% interest compounded annually, with complete safety backed by the government and no market risk whatsoever. This account works perfectly for conservative long term goals like retirement or your child's higher education because you cannot withdraw the entire amount before 15 years, protecting you from impulsive spending.

Consider the National Pension System (NPS) for additional retirement savings because it provides extra tax deductions of ₹50,000 under Section 80CCD(1B) beyond the standard ₹1.5 lakh limit. NPS invests your money across equity, corporate bonds, and government securities based on your age and risk appetite, automatically shifting to safer assets as you approach retirement. You control your asset allocation and can invest as little as ₹500 monthly, making it accessible for systematic wealth building through your working years.

Build a diversified portfolio through mutual funds

Equity mutual funds deliver the real growth that builds wealth because they invest in shares of Indian companies that expand and generate profits over time. Start with diversified equity funds that spread your money across 50 to 100 companies in different sectors, reducing the risk that one company's failure destroys your savings. These funds historically return 12% to 15% annually over 10 year periods, though they fluctuate significantly in shorter timeframes and require patience through market downturns.

Index funds tracking the Nifty 50 or Sensex offer the simplest entry into equity investing because they buy all stocks in these major market indices automatically, charging minimal fees of 0.1% to 0.3% annually compared to 1.5% to 2% for actively managed funds. You get instant diversification across India's largest companies without needing to pick individual stocks or trust fund managers to beat the market, which most fail to do consistently over long periods. Set up Systematic Investment Plans (SIPs) that invest fixed amounts monthly regardless of market levels, averaging your purchase price and removing emotion from investment timing.

Allocate 10% to 20% of your equity portfolio to Equity Linked Savings Schemes (ELSS) that offer tax deductions under Section 80C while investing in diversified stocks. ELSS funds lock your money for just three years, the shortest lock-in period among all tax-saving instruments, and they historically deliver better returns than traditional options like tax-saving fixed deposits. Choose ELSS funds with strong 5 year and 10 year track records rather than chasing last year's top performers, because consistent performance matters more than one year of exceptional returns.

Diversification across asset classes and investment types protects your wealth from any single economic event destroying your financial future.

Add debt mutual funds or corporate bond funds for stability, targeting 20% to 30% of your portfolio in these less volatile investments that generate steady income through interest payments. Rebalance your portfolio annually by selling some of your best performers and buying more of underperforming assets to maintain your target allocation, a disciplined approach that forces you to buy low and sell high without emotional decisions.

Invest consistently through market ups and downs

Market crashes feel terrifying when your portfolio drops 20% or 30% in weeks, but continuing your SIPs during downturns buys you more units at cheaper prices that multiply your wealth when markets inevitably recover. Review every major market crash in Indian history and you'll find that investors who stayed invested for 5 years or longer always recovered their losses and generated positive returns. Your monthly investments during the 2008 financial crisis or the 2020 pandemic crash would have grown substantially by 2023, rewarding patience over panic.

Never try to time the market by stopping investments when prices seem high or waiting for the perfect entry point that never arrives. Studies show that investors who miss just the 10 best days in the stock market over a decade earn significantly lower returns than those who stay fully invested throughout, and those best days often happen immediately after the worst days when fear tempts you to sell. Your consistent monthly investments through all market conditions capture both the highs and the lows, averaging out to solid long term returns without the stress of predicting unpredictable market movements.

Avoid frequent buying and selling because short term capital gains on equity held less than one year face 15% tax, while gains on investments held longer than one year enjoy either complete tax exemption up to ₹1 lakh annually or 10% tax beyond that limit. Transaction costs, exit loads on mutual funds sold before one year, and the time spent monitoring daily market movements all erode your returns without adding real value. Focus on accumulating quality investments over decades rather than trading for quick profits that rarely materialize consistently.

Step 4. Protect, optimize, and stay on track

Building wealth means nothing if one medical emergency or tax mistake wipes out years of savings. You need protective measures that shield your assets while continuously improving your returns through smart optimization. Regular monitoring and adjustments keep your long term wealth building plan aligned with your changing life circumstances, market conditions, and financial goals rather than letting your portfolio drift into risky territory or stagnate in outdated allocations.

Secure adequate insurance coverage

Buy term life insurance worth 10 to 15 times your annual income to protect your family's financial future if something happens to you, choosing pure term plans that cost ₹500 to ₹1,500 monthly instead of expensive investment-linked policies that deliver poor returns. Calculate your coverage by adding your outstanding debts, your family's living expenses for 20 years, and major future goals like children's education. Purchase this insurance before age 35 when premiums stay lowest and health complications haven't appeared.

Add health insurance covering ₹10 lakhs minimum per family through a combination of your employer's group policy and a top-up or super top-up plan that fills coverage gaps. Medical inflation runs at 12% to 15% annually in India, meaning a ₹5 lakh hospitalization today costs ₹10 lakhs in just five years. Review your policies annually and increase coverage as your income grows and medical costs rise.

Minimize taxes through strategic planning

Review your Section 80C deductions, 80D health insurance deductions, and NPS contributions each April to maximize tax savings before the financial year ends. Create a simple checklist tracking which tax-saving investments you've completed and how much room remains under each section, ensuring you claim every available deduction without last-minute rushed decisions.

Strategic tax planning adds 2% to 3% to your annual returns without taking additional investment risk, compounding into substantial wealth over decades.

Rebalance your portfolio every 12 months by comparing your current asset allocation against your target percentages, then selling overperforming assets and buying underperforming ones to maintain your risk level. Set a calendar reminder each January to review your entire investment portfolio, checking that your equity allocation hasn't grown too large during bull markets or shrunk too small during corrections. Adjust your investment amounts as your salary increases, redirecting at least half of every raise into additional monthly SIPs rather than lifestyle inflation.

Bringing your wealth plan to life

Long term wealth building succeeds when you move from reading to doing. Start this month by tracking every rupee for 30 days, then set up automatic transfers that send at least 20% of your salary to separate accounts for emergency funds and investments. You don't need perfect knowledge or ideal market conditions to begin, you just need to take the first small step that compounds into financial freedom over decades.

Review your progress quarterly rather than checking your portfolio daily, adjusting your investment amounts as your income grows and rebalancing when your asset allocation drifts more than 5% from your targets. The difference between people who build substantial wealth and those who struggle financially comes down to consistent action over years, not complex strategies or perfect timing.

Professional guidance accelerates your wealth building by eliminating costly mistakes and optimizing your returns without hidden fees eating into your gains. Start your AI-powered wealth journey with Invsify to get personalized investment recommendations, track your entire portfolio in one place, and access conflict-free financial advice that puts your interests first. Your financial future depends on decisions you make today, so take action now rather than wishing you had started years ago.