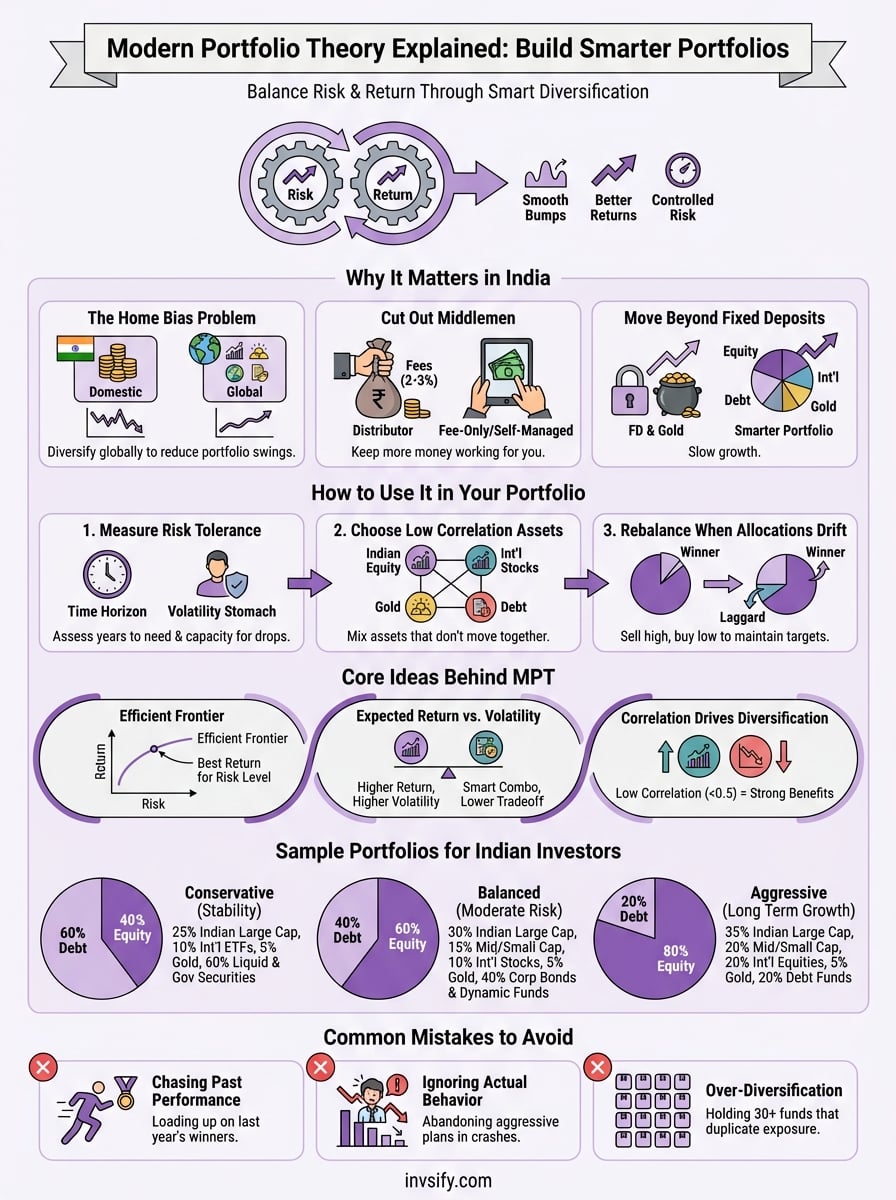

Modern Portfolio Theory Explained: Build Smarter Portfolios

Shlok Sobti

Modern Portfolio Theory Explained: Build Smarter Portfolios

Modern Portfolio Theory is a framework that helps you build investment portfolios by balancing risk and return. Instead of picking random stocks or mutual funds, it shows you how to combine different assets so you get better returns without taking unnecessary risks. The core idea is simple: some investments move up when others move down, and when you mix them smartly, you smooth out the bumps in your portfolio's performance.

This article breaks down how Modern Portfolio Theory works and how you can apply it to your own investments. You'll learn why it matters for Indian salaried investors, the core concepts that drive it, and practical ways to build portfolios that match your risk tolerance. We'll also look at sample portfolios you can adapt, cover the theory's limitations, and point out common mistakes to avoid. By the end, you'll know how to use this proven framework to make better investment decisions with your hard earned money.

Why modern portfolio theory matters in India

Most Indian investors keep too much money in fixed deposits and gold, missing out on better returns because they fear stock market volatility. When you understand modern portfolio theory explained in the Indian context, you realize you don't have to choose between safety and growth. You can build portfolios that give you better returns than traditional savings while keeping risk under control through smart diversification.

The home bias problem affects your returns

Indian salaried professionals typically invest 90% of their equity allocation in domestic stocks, ignoring international markets that could reduce portfolio swings. Your portfolio suffers when Indian markets go through rough patches because you have no cushion from assets that move differently. Modern Portfolio Theory shows you how to mix asset classes and geographies so a downturn in one area doesn't wreck your entire savings.

"Diversification is the only free lunch in investing, but most Indian portfolios miss this opportunity by concentrating too heavily in domestic assets."

You save more when you cut out middlemen

Traditional distributors charge hidden commissions that can eat 2-3% of your returns annually, compounding into lakhs lost over decades. By applying Modern Portfolio Theory yourself or through a fee-only advisor, you keep more of your money working for you instead of paying unnecessary fees that drag down your wealth accumulation.

How to use modern portfolio theory in your portfolio

You don't need complex software or an economics degree to apply this framework to your investments. Modern portfolio theory explained in practical terms means you assess your risk capacity, pick assets that move differently, and maintain your target allocation through regular rebalancing. Start by understanding your own situation before you touch any investment product.

Step one: measure your risk tolerance accurately

Your risk tolerance depends on how many years until you need the money and how much portfolio volatility you can stomach without making panic decisions. If you plan to retire in 30 years, you can handle more equity exposure than someone who needs funds in 5 years. Run scenarios where your portfolio drops 20% or 30% and ask yourself honestly if you would sell everything or stay invested. This self-awareness prevents you from choosing aggressive allocations that you'll abandon during market corrections.

Step two: choose assets with low correlation

Pick investments that don't move in lockstep with each other so losses in one area get offset by stability or gains elsewhere. Indian equities, international stocks, gold, and debt instruments typically show different behaviors across market cycles. When Indian markets fall, gold often holds steady or rises. International equities give you exposure to sectors and economies that don't mirror India's performance. You can access these through mutual funds and ETFs without needing separate brokerage accounts for foreign stocks.

"Assets with correlation below 0.7 provide meaningful diversification benefits, while perfectly correlated assets just amplify your existing risks."

Step three: rebalance when allocations drift

Market movements shift your portfolio away from your original plan, so you need to sell winners and buy laggards periodically to maintain your target allocation. Check your portfolio every six months and rebalance if any asset class drifts more than 5% from its target weight. This disciplined approach forces you to sell high and buy low automatically, removing emotion from your investment decisions.

Core ideas behind modern portfolio theory

The framework rests on three mathematical principles that determine how your portfolio performs over time. When you grasp these concepts, you understand why randomly picking investments rarely produces optimal results and why systematic portfolio construction beats gut feelings. Each principle builds on the others to create a complete system for managing investment risk and return.

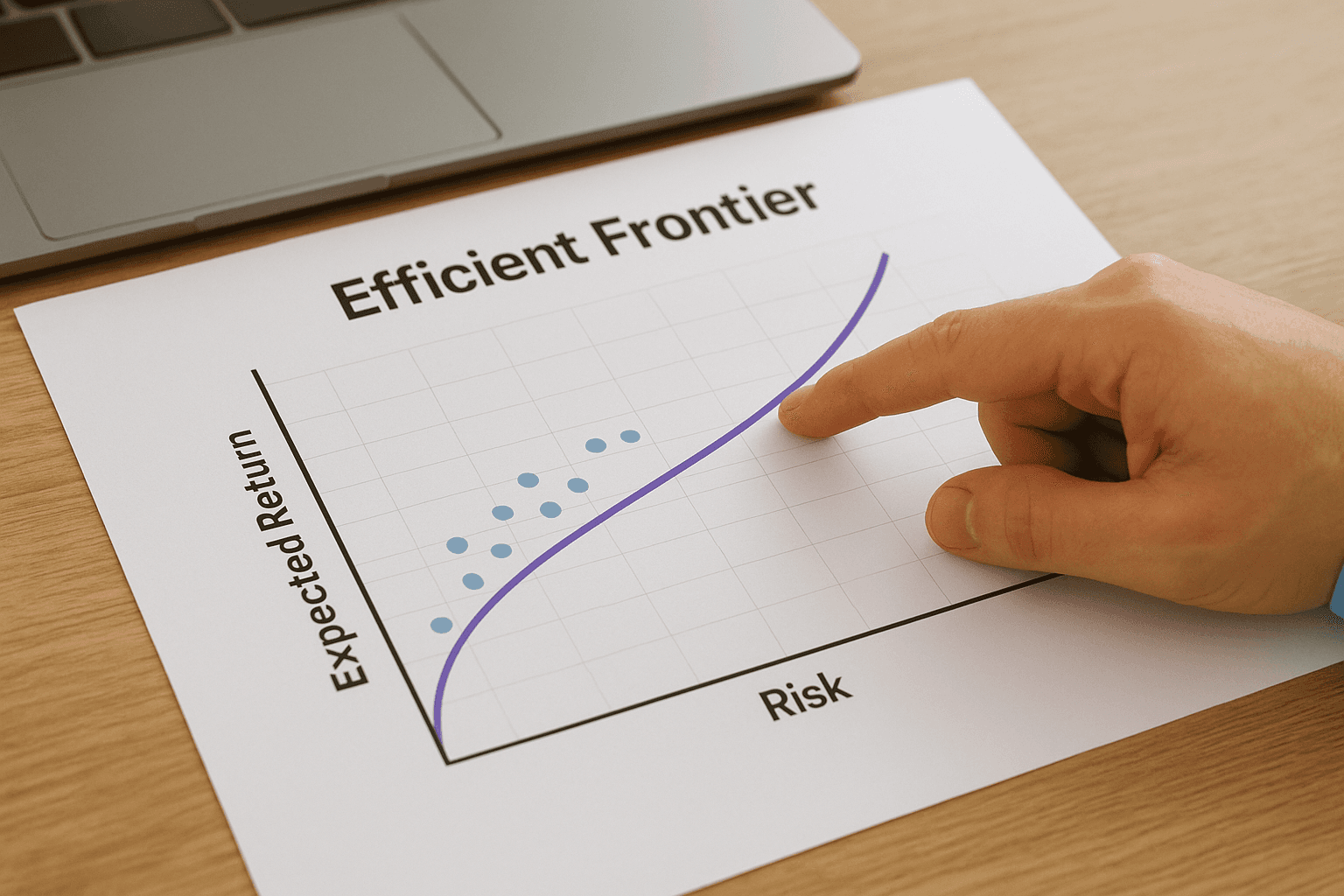

The efficient frontier shows your best options

You can plot every possible portfolio combination on a graph that maps expected return against risk, and the efficient frontier represents the curve of portfolios that give you the highest return for each risk level. Any portfolio below this curve wastes your money because you could get better returns without taking additional risk. Your goal is to pick a point on this frontier that matches your personal risk tolerance, whether that means accepting higher volatility for growth potential or choosing stability with modest returns.

Expected return versus actual volatility

Modern portfolio theory explained through numbers reveals that higher returns always come with higher volatility in individual assets, but smart combinations reduce this tradeoff. You measure volatility using standard deviation, which shows how much your portfolio value swings around its average return. A portfolio with 10% expected return and 15% standard deviation outperforms one with 10% return and 20% standard deviation because you get the same gains with less nerve-wracking movement in your account balance.

"Volatility measures the price you pay for returns, and diversification helps you negotiate a better deal."

Correlation drives diversification benefits

The correlation coefficient between two assets ranges from negative one to positive one, telling you whether they move together or opposite each other. Assets with correlations below 0.5 provide strong diversification because losses in one investment don't predict losses in the other. Indian equities and U.S. treasury bonds show low correlation, so combining them smooths your portfolio performance better than holding only Indian stocks and Indian bonds that tend to move similarly during domestic economic events.

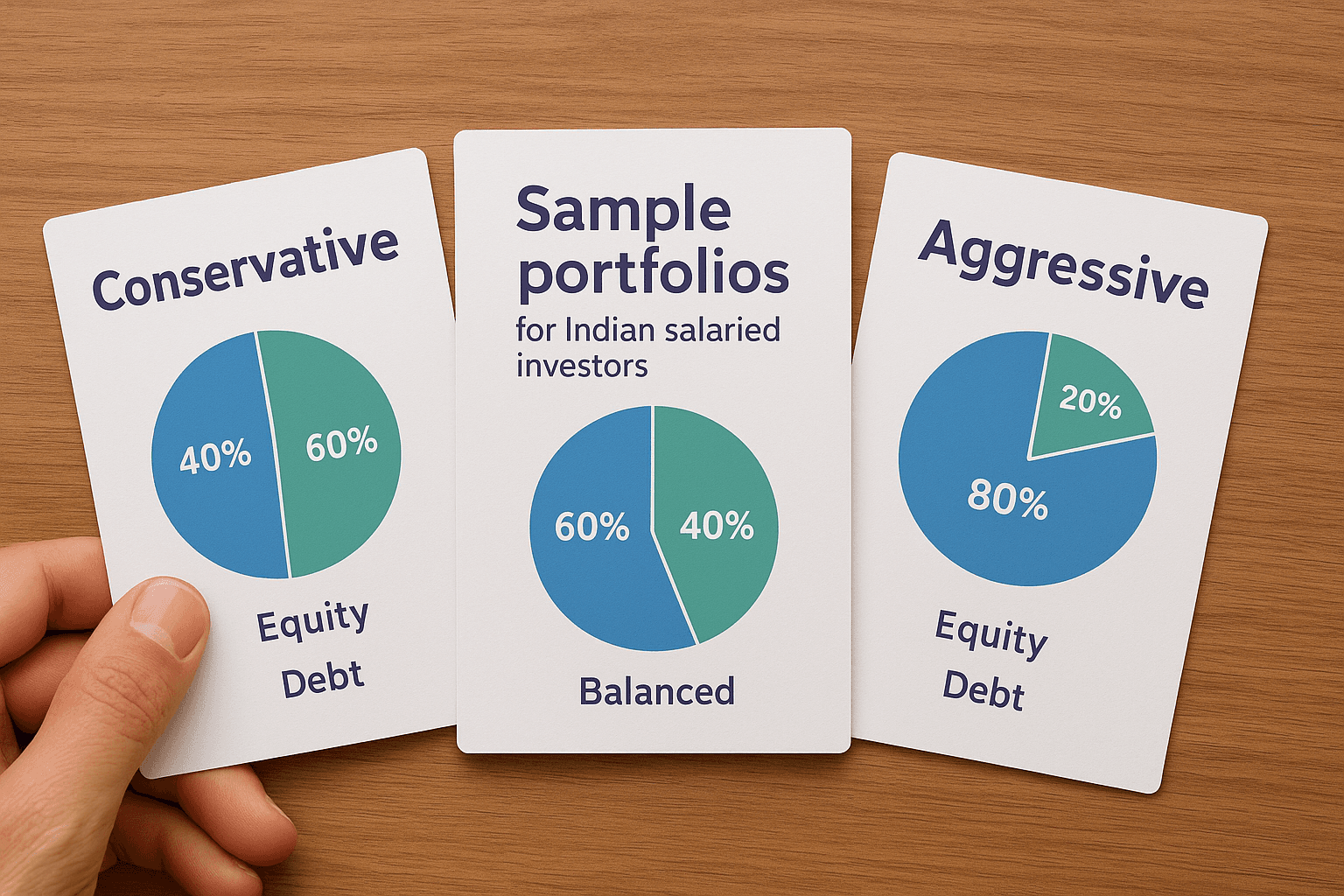

Sample portfolios for Indian salaried investors

You can apply modern portfolio theory explained above by starting with three portfolio templates that match different risk profiles and investment timelines. These allocations use asset classes available to Indian investors through mutual funds and ETFs, making implementation straightforward without requiring foreign brokerage accounts. Each portfolio adjusts the equity to debt ratio based on how much volatility you can handle while staying invested through market downturns.

Conservative portfolio for stability seekers

Your conservative portfolio should hold 40% equity and 60% debt instruments when you need money within 5 to 7 years or can't stomach significant portfolio swings. Split the equity portion into 25% Indian large cap funds, 10% international equity ETFs, and 5% gold to capture different market behaviors. The debt allocation goes into liquid funds, short duration funds, and government securities that protect your principal while generating steady returns above inflation.

Balanced portfolio for moderate risk takers

This middle ground allocation puts 60% in equities and 40% in debt, suitable when your investment horizon spans 10 to 15 years and you accept temporary losses for higher long term gains. Divide equities into 30% Indian large cap, 15% mid and small cap, 10% international stocks, and 5% gold to balance growth potential with diversification. Your debt holdings in corporate bonds and dynamic bond funds add stability without dragging returns too much.

"Most Indian salaried professionals benefit from balanced portfolios because they offer growth without requiring iron nerves during market corrections."

Aggressive portfolio for long term wealth builders

An aggressive stance allocates 80% to equities and 20% to debt when you won't need the money for 20 years or more and can watch your portfolio drop 30% without selling. Structure your equity exposure as 35% Indian large cap, 20% mid and small cap, 20% international equities, and 5% gold, capturing maximum growth across markets. Keep the remaining 20% in debt funds for emergency liquidity and opportunistic rebalancing when equity markets crash.

Assumptions limits and common mistakes

Modern portfolio theory explained in textbooks makes several assumptions that don't perfectly match real world investing, which affects how you should apply the framework. The theory assumes markets are efficient, investors act rationally, and past correlations predict future relationships between assets. Your actual results will differ because markets show inefficiencies, behavioral biases affect decisions, and correlations shift dramatically during crises when diversification benefits disappear.

The theory assumes perfect market conditions

The mathematical models behind modern portfolio theory require frictionless markets without taxes or transaction costs, but you pay securities transaction tax, capital gains tax, and fund expense ratios that eat into returns. Indian investors face additional challenges like currency risk on international holdings and regulatory restrictions on asset allocations that limit your ability to implement theoretically optimal portfolios. These real world constraints mean you need to adjust allocations based on tax efficiency and practical accessibility rather than purely mathematical optimization.

"Perfect theory meets imperfect markets, so your job is adapting the framework to work within real constraints rather than abandoning it entirely."

Common mistakes that hurt your returns

You make the biggest error when you chase past performance by loading up on last year's winners, forgetting that mean reversion brings high flyers back down. Another mistake involves ignoring your actual behavior during market crashes and choosing aggressive allocations that you'll abandon when your portfolio drops 25%. Investors also fail by never rebalancing, letting winning positions grow too large and eliminating diversification benefits you built into your original plan. The final common trap is over diversifying into 30 or 40 funds that just duplicate the same exposures and add complexity without reducing risk.

Bringing it all together

Modern portfolio theory explained through this article gives you a practical framework to build investment portfolios that balance risk and return. You now understand why diversification across asset classes beats concentrating in fixed deposits or single market investments, how to choose allocations that match your risk tolerance, and which common mistakes destroy portfolio performance over time.

Your next step involves applying these principles to your own savings by selecting an appropriate asset allocation, picking low-cost mutual funds or ETFs that give you exposure to different markets, and setting up a rebalancing schedule you'll actually follow. The theory works best when you commit to staying invested through market cycles rather than jumping in and out based on news headlines.

Ready to build a smarter portfolio with AI-powered guidance and transparent advice? Start your wealth journey with Invsify today and get personalized recommendations based on your financial goals.