Nippon India Retirement Fund: NAV, Returns, Lock-In, Plans

Shlok Sobti

Nippon India Retirement Fund: NAV, Returns, Lock-In, Plans

Planning for retirement requires choosing the right investment vehicle that matches your financial goals and risk appetite. The Nippon India Retirement Fund stands out as a solution-oriented mutual fund designed specifically for long-term wealth accumulation toward your post-work years.

Whether you're evaluating NAV trends, comparing the wealth creation scheme versus the income generation plan, or trying to understand the lock-in implications, getting clear and unbiased information matters. At Invsify, we help salaried Indians make conflict-free investment decisions through AI-powered insights, and that starts with understanding your options thoroughly before committing your hard-earned money.

This guide breaks down everything you need to know about the Nippon India Retirement Fund: current NAV, historical returns, lock-in periods, and the key differences between its two scheme options. By the end, you'll have the clarity to evaluate whether this fund aligns with your retirement planning strategy.

What the Nippon India Retirement Fund is

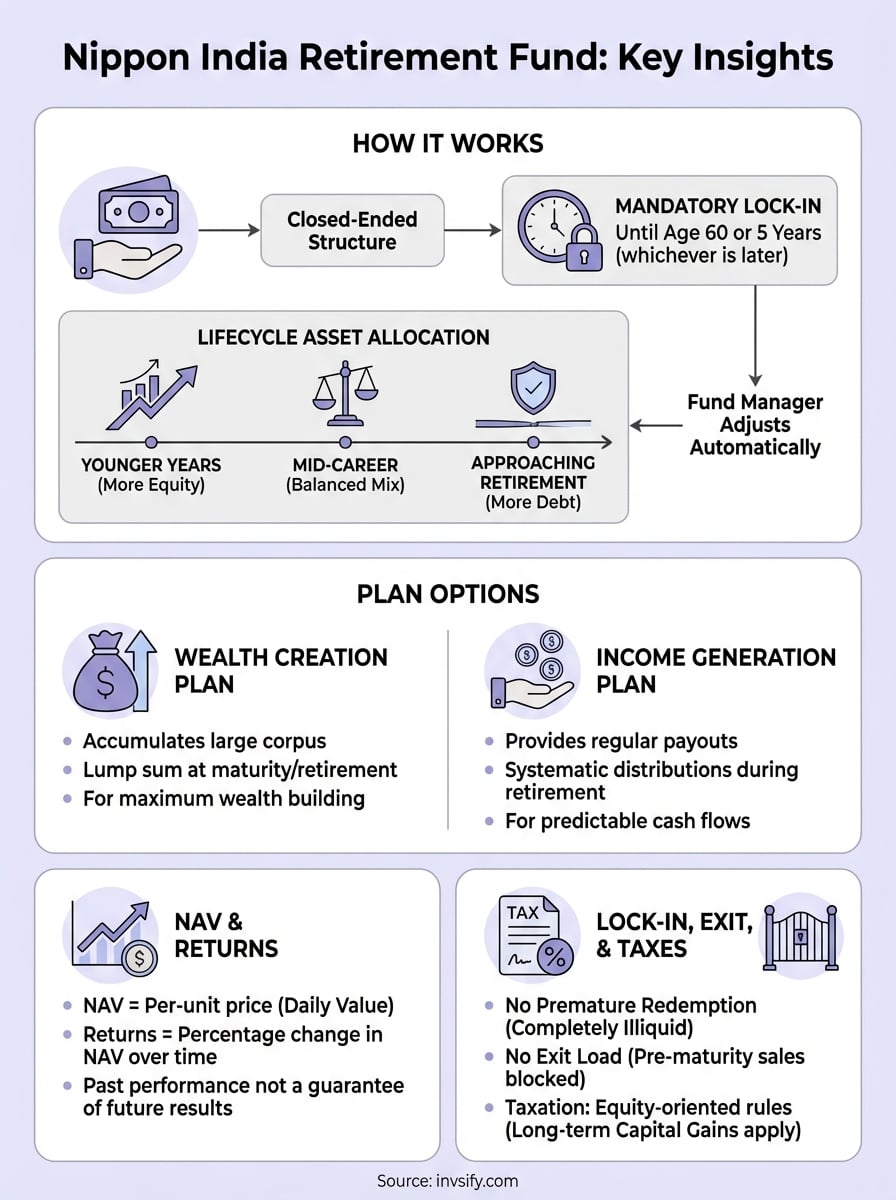

The Nippon India Retirement Fund is a solution-oriented mutual fund scheme launched by Nippon Life India Asset Management Limited (formerly Reliance Mutual Fund). This fund operates under a closed-ended structure, meaning you cannot redeem your investment until maturity or retirement, whichever comes first. The fund's sole purpose centers on helping Indian investors build a retirement corpus through systematic exposure to equity and debt instruments.

How the fund structure works

You invest in this fund with a mandatory lock-in period that extends until you turn 60 years old or for a minimum of five years from the date of investment, whichever is later. The fund house follows a lifecycle-based asset allocation strategy, which means it automatically adjusts the equity-to-debt ratio as you age. When you're younger, the portfolio tilts heavily toward equities for growth potential. As you approach retirement, the fund manager shifts more assets into debt securities to preserve capital and reduce volatility.

The lifecycle approach removes the need for you to manually rebalance your portfolio as retirement nears.

Who manages your money

Nippon Life India Asset Management manages your contributions through professional fund managers who make daily investment decisions based on market conditions and the fund's mandate. The fund deploys your money across diversified equity stocks, government securities, corporate bonds, and money market instruments. Your returns depend on the performance of these underlying assets, not on guaranteed interest rates. The Asset Management Company charges an expense ratio that covers fund management, administration, and regulatory compliance costs.

Wealth creation vs income generation plans

The Nippon India Retirement Fund offers two distinct plans that serve different financial objectives during your retirement journey. You choose between the Wealth Creation Plan and the Income Generation Plan based on when you need the money and how you want it deployed. Both plans follow the same lifecycle asset allocation philosophy but differ fundamentally in their payout structures and investment horizons.

The wealth creation scheme

This plan focuses entirely on accumulating a large retirement corpus over the long term. Your investment grows through compounding returns, and you receive the entire accumulated value as a lump sum when the fund matures or when you turn 60, whichever comes later. The fund manager invests aggressively in equities during your younger years, gradually shifting toward debt instruments as retirement approaches. You benefit from this plan if you want to build maximum wealth and handle your retirement income planning separately through other instruments or systematic withdrawals.

The wealth creation option works best when you have other income sources lined up for retirement.

The income generation option

This plan targets investors who need regular income after retirement rather than a single lump sum. Your money stays invested in the same lifecycle portfolio, but the fund provides systematic payouts during your retirement years instead of returning everything at once. You receive periodic distributions that help cover living expenses without liquidating your entire corpus immediately. This structure suits you if you lack guaranteed pension income and need predictable cash flows post-retirement.

NAV and returns: what they mean for you

The Net Asset Value (NAV) represents the per-unit price you pay when investing in the Nippon India Retirement Fund and the value you receive when redeeming your units. The fund house calculates NAV daily by dividing the total market value of all securities in the portfolio by the number of outstanding units. Your investment's current worth equals the number of units you hold multiplied by the latest NAV. This figure changes every business day based on how the underlying equity stocks and debt instruments perform in the market.

Understanding NAV movements

You should view NAV as a measurement tool rather than a performance indicator by itself. A higher NAV does not automatically signal a better investment, just as a lower NAV does not mean the fund lacks quality. What matters more is the percentage change in NAV over time, which reflects your actual gains or losses. The fund's NAV fluctuates based on equity market volatility, interest rate changes, and the fund manager's investment decisions across lifecycle phases.

Your actual returns depend on how much the NAV grows between your purchase and redemption dates, not the absolute NAV number.

What historical returns tell you

Past performance shows how the fund navigated different market cycles but never guarantees future results. You can examine trailing returns over one year, three years, five years, and since inception to understand consistency patterns.

Lock-in, exit load, and taxes in India

The Nippon India Retirement Fund locks your investment until you turn 60 years old or complete five years from purchase, whichever comes later. This mandatory restriction exists because SEBI classifies retirement funds as solution-oriented schemes requiring lock-in periods. You cannot withdraw money during emergencies or financial hardships unless specific exemptions apply, such as critical illness or death of the unit holder. Understanding these constraints matters before you commit funds that become inaccessible for years.

Understanding the lock-in period

Your money becomes completely illiquid the moment you invest in either the wealth creation or income generation plan. The fund house blocks all premature redemptions through regulatory requirements, and no exit load applies because you physically cannot sell units before maturity. This structure protects your retirement corpus from impulsive withdrawals but eliminates flexibility if you face urgent financial needs or find better investment opportunities elsewhere.

The lock-in ensures discipline but removes all access to your capital during the entire holding period.

How taxes apply

The tax department treats this as an equity-oriented fund when equity allocation exceeds 65 percent at redemption. You pay long-term capital gains tax at 12.5 percent on profits above ₹1.25 lakh per financial year after holding units beyond one year. Short-term gains attract a 20 percent tax rate, though the mandatory lock-in typically ensures all your redemptions fall under long-term classification.

How to check if it fits your retirement plan

You need to evaluate the Nippon India Retirement Fund against your specific retirement goals, existing investments, and liquidity requirements before committing. Start by calculating your expected retirement corpus using online calculators that factor in inflation, current age, retirement age, and monthly expenses. Compare this target amount with what the fund historically delivered across similar investment periods. Your decision depends on whether the fund's structure matches your financial situation and risk profile.

Assess your liquidity needs

Examine your emergency fund status and other liquid assets before locking money into this fund. You should maintain at least six months of expenses in accessible accounts because the mandatory lock-in period removes all flexibility. If you anticipate needing funds for education, medical emergencies, or home purchases before retirement, allocate those amounts elsewhere first. This fund works only when you have surplus capital that you absolutely will not touch until age 60.

Lock-in penalties do not exist because early withdrawals simply remain blocked by regulation.

Compare with alternative retirement vehicles

Consider how this fund compares against National Pension System (NPS), Public Provident Fund (PPF), and diversified equity mutual funds with voluntary systematic withdrawals. NPS offers tax benefits under Section 80CCD but also restricts access until retirement. PPF provides guaranteed returns with complete safety but limits annual contributions to ₹1.5 lakh.

Next steps

You now understand the Nippon India Retirement Fund structure, lock-in requirements, NAV mechanics, and how both plans serve different retirement objectives. Your next action depends on whether this fund aligns with your liquidity needs, risk tolerance, and retirement timeline. The mandatory lock-in until age 60 creates significant commitment, so thorough evaluation matters before investing.

Start by reviewing your complete financial picture, including emergency funds, existing retirement investments, and expected retirement corpus. Compare the fund's historical performance against your required growth rate, then evaluate whether the lifecycle asset allocation strategy matches your age and retirement date. Consider consulting tax implications based on your income bracket and how this fund fits alongside other retirement instruments like NPS or PPF.

Making informed investment decisions requires unbiased guidance and comprehensive portfolio analysis across all your holdings. Get conflict-free retirement planning advice from Invsify's AI-powered platform, where you can track investments, receive personalized insights, and build a retirement strategy without hidden fees or commissions that eat into your returns.