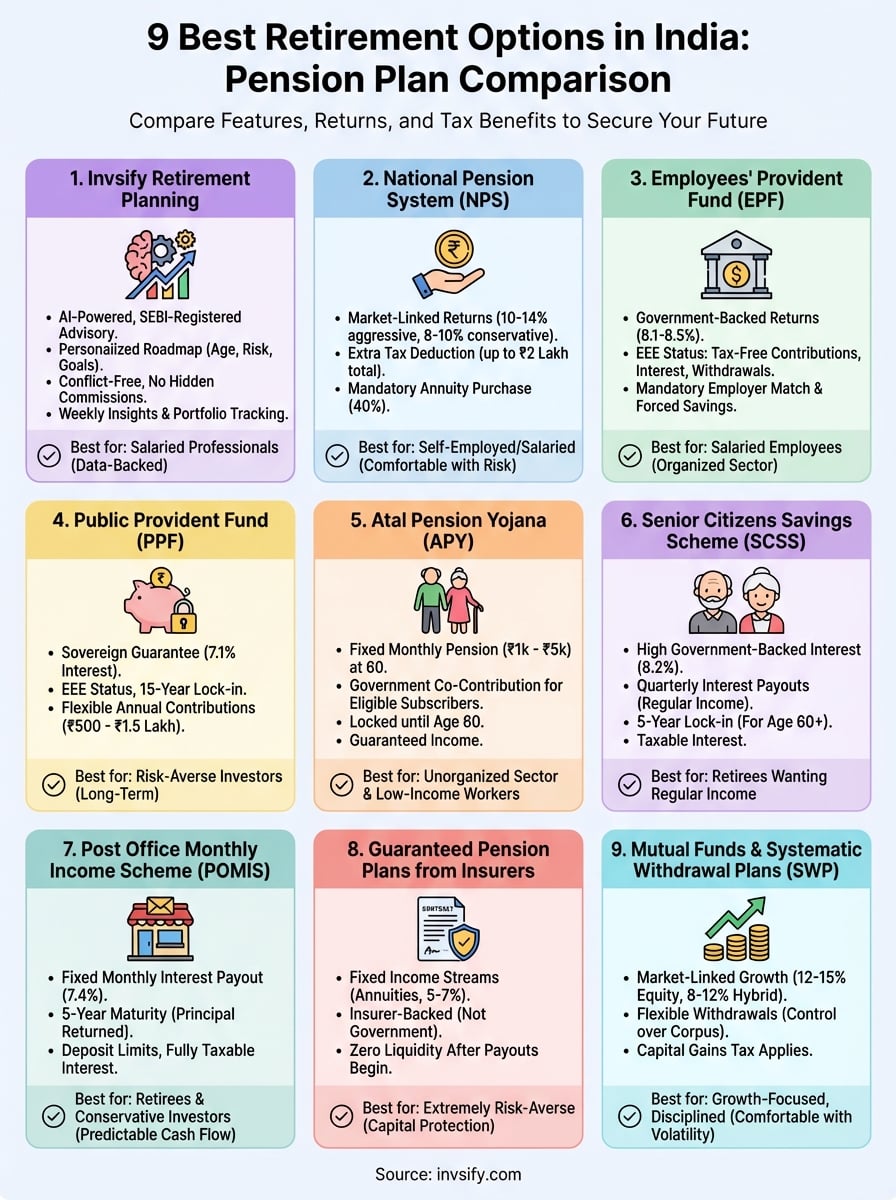

Pension Plan Comparison India: 9 Best Retirement Options

Shlok Sobti

Pension Plan Comparison India: 9 Best Retirement Options

Retirement might feel like a distant milestone, but the decisions you make today directly shape the financial freedom you'll have decades from now. With so many options available, government schemes like NPS and PPF, private insurance plans, and hybrid products, a proper pension plan comparison India can save you from costly mistakes and missed opportunities.

The challenge? Each plan comes with different lock-in periods, tax treatments, and return potential. Some prioritize guaranteed payouts while others offer market-linked growth. Choosing the wrong one could mean leaving lakhs on the table or facing unexpected tax burdens when you need your money most.

This guide breaks down 9 of the best retirement options available to Indian investors in 2026. You'll find clear comparisons of features, returns, and tax benefits so you can match each plan to your specific goals and risk appetite. At Invsify, our AI-powered advisory helps salaried professionals cut through the noise and build retirement portfolios that actually make sense, free from hidden commissions and conflicted advice. Let's get into the options worth considering.

1. Invsify retirement planning and portfolio guidance

Most retirement planning tools throw generic suggestions at you without understanding your actual salary structure, existing investments, or life goals. Invsify takes a different approach by combining AI-powered analytics with SEBI-registered advisory to build retirement plans that align with your real financial situation. You get a personalized roadmap that factors in your age, risk tolerance, current portfolio, and target retirement corpus, all without the hidden commissions that plague traditional distributors.

What it is and how it works

Invsify operates as your digital financial advisor that uses artificial intelligence to analyze your complete financial picture and recommend specific retirement strategies. After you complete a quick KYC process and risk profiling, the platform calculates your Wealth Wellness Score and suggests a customized mix of instruments like NPS, PPF, mutual funds, or other options based on your timeline and goals. The conversational RM AI stays available 24/7 in multiple languages, so you can ask questions about any aspect of your retirement plan whenever you need clarity.

How it helps you compare options and set a retirement plan

The platform shows you side-by-side comparisons of different pension schemes with their actual returns, lock-in periods, and tax implications specific to your income bracket. You'll see exactly how much a combination of NPS contributions plus mutual fund SIPs could grow versus putting everything into a PPF or insurance plan. The hidden fee calculator reveals how much traditional distributor commissions would cost you over 20 or 30 years, making it easier to understand why conflict-free advice matters for long-term wealth building.

"The difference between a 0.5% expense ratio and a 2% commission adds up to lakhs when compounded over decades."

Expected outcomes and what to track

You'll receive weekly personalized insights that track your progress toward your retirement corpus target and alert you when your asset allocation drifts from the recommended mix. The advanced portfolio tracking feature consolidates all your investments in one dashboard, showing real-time values and projected retirement income based on current contribution rates. Your Wealth Wellness Score updates automatically as you make changes, giving you a clear metric to measure improvement over time.

Tax planning support and documentation readiness

Invsify's system identifies tax-saving opportunities within your retirement investments, like maximizing Section 80C deductions through PPF or claiming additional deductions under Section 80CCD(1B) for NPS contributions. When tax season arrives, you'll have all your investment statements and tax documents organized in one place instead of hunting through email attachments or physical files from multiple providers.

Costs and fees to expect

The advisory service operates on a transparent fee structure with no hidden commissions or trailing charges. You pay directly for advice rather than through embedded product costs, which typically saves you 1.5% to 2% annually compared to traditional distributor models. The platform clearly displays all fees upfront before you commit to any plan.

Who it fits best

Invsify works best for salaried professionals who want data-backed retirement planning but don't have time to research every scheme themselves. If you're currently managing investments through Reddit threads or unverified online sources, or if you're paying high commissions to traditional advisors, this AI-powered approach gives you institutional-grade guidance at a fraction of the cost. The multilingual support makes it accessible even if you prefer financial discussions in Hindi or other regional languages.

When to avoid or use with caution

If you prefer face-to-face meetings for all financial decisions or need extremely complex estate planning involving multiple trusts and international assets, you might want additional specialized advisory beyond what the platform offers. The 30-second callback feature helps with urgent queries, but some people still value in-person relationship management for major financial moves.

2. National Pension System

The National Pension System stands out in any pension plan comparison India offers because it combines market-linked returns with government regulation through the Pension Fund Regulatory and Development Authority (PFRDA). You contribute to a mix of equity, corporate bonds, and government securities based on your risk appetite, and the corpus grows tax-deferred until retirement. Unlike traditional pension plans, NPS gives you control over asset allocation and fund manager selection.

What it is and how it works

You open two accounts: Tier 1 (locked until 60) and Tier 2 (voluntary savings with no restrictions). Your contributions get invested across equity (up to 75%), corporate debt, government bonds, and alternative assets based on the active choice or auto choice lifecycle fund you select. Seven pension fund managers compete for your money, and you can switch between them if performance disappoints.

Expected returns and risk profile

Historical returns hover around 10% to 14% annually for aggressive portfolios with higher equity allocation, while conservative options deliver 8% to 10%. Your actual returns depend entirely on market performance since NPS offers no guaranteed returns. Equity exposure makes this riskier than PPF or EPF but potentially more rewarding over decades.

Tax benefits and tax on exit

You claim deductions up to Rs 1.5 lakh under Section 80C plus an additional Rs 50,000 under Section 80CCD(1B) exclusively for NPS. At withdrawal, 60% comes out tax-free while the remaining 40% used for annuity purchase gets taxed as income when you receive pension payouts.

"The extra Rs 50,000 deduction makes NPS the only retirement product that lets you claim Rs 2 lakh in total tax benefits annually."

Liquidity and withdrawal rules

Partial withdrawals become available after three years for specific needs like children's education or medical emergencies, capped at 25% of your contributions. After 60, you withdraw up to 60% as a lump sum while the remaining 40% must purchase an annuity.

Costs and charges

Fund management fees range from 0.09% to 0.25% depending on the asset class, making NPS one of the lowest-cost investment products available in India. You also pay nominal charges for account maintenance.

Who it fits best

NPS works best for self-employed professionals and salaried individuals who want market-linked growth with disciplined retirement savings. If you're comfortable with equity volatility and want the extra tax deduction beyond Section 80C, this option deserves serious consideration.

Key trade-offs to know before you commit

The mandatory annuity requirement locks 40% of your money into relatively low-return products at retirement. Annuity rates in India typically deliver only 5% to 7% returns, which may not keep pace with inflation during your retirement years.

3. Employees' Provident Fund

The Employees' Provident Fund operates as a mandatory retirement savings scheme for salaried employees in organizations with 20 or more workers. Both you and your employer contribute 12% of your basic salary plus dearness allowance each month, with the money managed by the Employees' Provident Fund Organisation (EPFO). This creates a forced savings habit that builds your retirement corpus automatically through payroll deductions.

What it is and how it works

Your employer deducts 12% of your basic salary each month and matches it with an equal contribution, though 8.33% of the employer's share goes to the Employee Pension Scheme while the rest enters your EPF account. Interest gets credited annually based on rates declared by the EPFO, which have ranged from 8.1% to 8.5% in recent years.

Expected returns and risk profile

EPF delivers government-backed returns with zero market risk, typically offering rates slightly above PPF. The government sets interest rates each financial year, and you earn compound interest on your accumulated balance.

Tax benefits and tax on withdrawal

Contributions qualify for Section 80C deductions up to Rs 1.5 lakh annually. Withdrawals stay completely tax-free if you keep the account active for at least five continuous years, making EPF one of the few EEE (exempt-exempt-exempt) investment options available.

"EPF remains the only retirement product where contributions, interest, and withdrawals all stay tax-free under specific conditions."

Liquidity and withdrawal rules

You can withdraw for specific purposes like home purchase, medical emergencies, or education after completing seven years of service. Full withdrawal becomes available at retirement (58 years) or if you remain unemployed for two months.

Costs and charges

EPF comes with zero charges or fees since the government manages the scheme. You don't pay fund management costs.

Who it fits best

This works perfectly for salaried employees in organized sectors who want guaranteed returns without managing investments themselves. The automatic deduction removes the discipline problem many face with voluntary retirement savings.

Key trade-offs to know before you commit

Returns lag behind market-linked options over long periods, and you sacrifice potential equity growth for guaranteed safety. The mandatory nature also reduces your take-home salary during working years.

4. Public Provident Fund

The Public Provident Fund remains one of the safest retirement options in any pension plan comparison India features, backed by sovereign guarantee from the Government of India. You invest as little as Rs 500 or up to Rs 1.5 lakh annually into this 15-year scheme, earning fixed interest rates declared quarterly by the Ministry of Finance. PPF accounts suit conservative investors who prioritize capital protection over market-linked growth.

What it is and how it works

You open a PPF account at any nationalized bank or post office and contribute any amount between Rs 500 and Rs 1.5 lakh per financial year. Interest compounds annually and gets credited to your account on March 31 each year. After 15 years, you can extend the account in blocks of five years with or without additional contributions.

Expected returns and risk profile

Current PPF rates stand at 7.1% annually with zero risk since the government guarantees both principal and interest. Returns remain predictable though rates may fluctuate quarterly based on government bond yields.

Tax benefits and tax on maturity

You claim Section 80C deductions on contributions up to Rs 1.5 lakh while all interest and maturity proceeds come out completely tax-free. This EEE status makes PPF extremely tax-efficient for long-term wealth building.

"PPF's triple tax exemption delivers better post-tax returns than taxable fixed deposits offering higher nominal rates."

Liquidity and withdrawal rules

Partial withdrawals become available from year 7 onwards, limited to 50% of the balance. Loans against your PPF balance work from years 3 to 6.

Costs and charges

PPF carries zero fees or charges. You keep every rupee of interest earned.

Who it fits best

This works best for risk-averse investors wanting guaranteed returns with complete tax benefits. Salaried professionals seeking stable retirement corpus growth without market volatility find PPF ideal.

Key trade-offs to know before you commit

The 15-year lock-in restricts access to your money during emergencies. Returns lag behind equity-oriented options over long horizons, potentially costing you higher retirement income.

5. Atal Pension Yojana

The Atal Pension Yojana targets unorganized sector workers who lack employer-sponsored retirement benefits, offering fixed monthly pensions between Rs 1,000 and Rs 5,000 starting at age 60. You contribute small monthly amounts based on your entry age and desired pension, with the government co-contributing for eligible subscribers. This scheme works best for those wanting guaranteed pension income without market risk.

What it is and how it works

You join APY between ages 18 and 40 and contribute monthly until you turn 60, with contribution amounts increasing the later you start. The Pension Fund Regulatory and Development Authority manages your money, and you receive a fixed pension amount you selected at enrollment for life.

Pension payout structure and key limits

APY offers five pension slabs of Rs 1,000, Rs 2,000, Rs 3,000, Rs 4,000, or Rs 5,000 monthly. After your death, your spouse receives the same pension amount, and the corpus goes to your nominee after both pass away.

Tax benefits and tax on payouts

Contributions qualify for Section 80CCD deductions up to Rs 1.5 lakh under the overall Section 80C limit. Pension payouts get treated as regular income and taxed per your applicable slab rate.

Liquidity and exit rules

You stay locked in until age 60 with limited exit options. Premature exit due to death or terminal illness returns the corpus to nominees.

Costs and charges

The government bears administrative costs for eligible subscribers earning below the taxable threshold. You pay minimal account maintenance fees.

Who it fits best

This scheme suits informal sector workers, daily wage earners, and small business owners wanting guaranteed pension floors. When doing any pension plan comparison India offers, APY stands out for predictable low-income retirement support.

"APY provides retirement security to millions of Indians working outside the formal employment system."

Key trade-offs to know before you commit

Fixed pension amounts don't adjust for inflation, reducing purchasing power over decades. The corpus remains small compared to market-linked alternatives, limiting wealth creation potential.

6. Senior Citizens Savings Scheme

The Senior Citizens Savings Scheme offers one of the highest government-backed interest rates available to retirees aged 60 and above, making it a popular choice in any pension plan comparison India retirees conduct. You invest between Rs 1,000 and Rs 30 lakh in this five-year scheme through post offices or authorized banks, receiving quarterly interest payouts that provide regular income during retirement. This scheme prioritizes capital safety and predictable cash flow over growth potential.

What it is and how it works

You open an SCSS account at any post office or designated bank branch after turning 60 (or 55 if you've taken voluntary retirement). The money stays locked for five years, with an option to extend for another three years after maturity. Interest gets credited to your savings account every quarter.

Expected returns and payout structure

Current SCSS rates stand at 8.2% annually, paid quarterly. A Rs 15 lakh deposit generates approximately Rs 30,750 every quarter before tax.

Tax benefits and TDS basics

Deposits qualify for Section 80C deductions up to Rs 1.5 lakh. Banks deduct TDS if quarterly interest exceeds Rs 12,500, though you can submit Form 15H to avoid deduction if your total income stays below taxable limits.

Liquidity and premature closure rules

Premature withdrawal carries penalties: 1.5% of deposit if closed after one year but before two years, and 1% of deposit after two years. Emergency access remains limited.

Costs and charges

SCSS has zero account opening or maintenance fees. You keep all interest earned minus applicable TDS.

Who it fits best

This works perfectly for retirees wanting regular income without market risk. The higher rates compared to fixed deposits make it attractive for conservative senior investors.

Key trade-offs to know before you commit

The five-year lock-in restricts flexibility, and rates may drop at renewal. Interest income gets taxed at your slab rate, reducing post-tax returns for higher-income retirees.

"SCSS delivers the highest government-guaranteed returns available exclusively to senior citizens."

7. Post Office Monthly Income Scheme

The Post Office Monthly Income Scheme delivers regular monthly income through a safe government-backed instrument, making it popular among retirees and conservative investors seeking predictable cash flow. You invest between Rs 1,500 and Rs 9 lakh (or Rs 15 lakh for joint accounts) in this five-year scheme, receiving fixed monthly interest payments directly to your savings account. POMIS works differently from typical pension plans since it returns your principal at maturity rather than converting it to an annuity.

What it is and how it works

You open a POMIS account at any post office branch with a minimum deposit of Rs 1,500. The scheme pays fixed monthly interest starting from the month following your deposit, with interest credited directly to your linked savings account. At maturity after five years, you receive your entire principal back in one lump sum.

Expected returns and payout structure

Current POMIS rates stand at 7.4% annually, paid monthly. A Rs 9 lakh deposit generates Rs 5,550 every month before tax, providing consistent retirement income.

Tax treatment of interest income

Monthly interest counts as income from other sources and gets taxed at your applicable slab rate. Post offices deduct TDS if annual interest exceeds Rs 40,000 (Rs 50,000 for senior citizens), though you can submit Form 15G/15H to prevent deduction if your total income stays below taxable limits.

Liquidity and premature closure rules

Premature closure carries penalties: you lose 2% of principal if withdrawn within one year, 1% between one and three years, and no penalty after three years. Emergency liquidity remains limited compared to bank deposits.

Costs and charges

POMIS has zero account opening fees or maintenance charges. You receive full interest payments minus applicable TDS.

Who it fits best

This scheme suits retirees needing monthly income and conservative investors wanting government-guaranteed returns. Anyone conducting a pension plan comparison India offers should consider POMIS for its predictable cash flow and capital safety.

"POMIS transforms a lump sum into steady monthly income without touching your principal until maturity."

Key trade-offs to know before you commit

The Rs 9 lakh deposit limit restricts how much monthly income you can generate from this single scheme. Interest income faces full taxation, reducing post-tax returns for higher-income investors.

8. Guaranteed pension plans from insurers

Guaranteed pension plans from life insurance companies promise fixed income streams after retirement through immediate or deferred annuities, backed by the insurer's financial strength rather than government guarantees. You pay either a lump sum or regular premiums during your working years, and the insurer commits to specific monthly or annual payouts starting at a predetermined age. These products appeal to retirees wanting predictable income without market volatility, though returns typically lag behind equity-oriented alternatives.

What it is and how it works

You purchase an annuity from a life insurance company by paying either a single premium (immediate annuity) or regular premiums over years (deferred annuity). The insurer invests your money in debt instruments and pays you a fixed income stream based on prevailing annuity rates, your age, and chosen payout option. Some plans offer life cover during accumulation phase before converting to pension payouts.

Payout options and how annuities work

Insurers offer multiple payout structures: life annuity (income until death), life with return of purchase price (corpus goes to nominee after death), joint life (continues for surviving spouse), and annuity certain (guaranteed payout period regardless of survival). Current annuity rates typically deliver 5% to 7% returns depending on your age and chosen option.

Tax treatment of premiums and payouts

Premiums qualify for Section 80CCC deductions up to Rs 1.5 lakh within the overall Section 80C limit. Pension income gets taxed as salary income at your applicable slab rate, though one-third of commuted amount stays tax-free.

Liquidity, surrender, and commutation rules

Most annuity plans offer zero liquidity once pension payouts begin. Some deferred plans allow surrender during accumulation phase with penalties ranging from 2% to 6% depending on policy year. You can commute up to one-third of purchase price as a lump sum at pension start.

Costs, charges, and what impacts your payout rate

Insurance plans carry mortality charges, fund management fees, and administrative costs that reduce your effective returns. Higher charges directly lower the annuity rate you receive. Your age, gender, and chosen payout option significantly impact rates, with older entrants getting better rates.

"Insurance annuity rates in India remain among the lowest globally, often failing to beat inflation over long retirement periods."

Who it fits best

These products suit extremely risk-averse retirees who prioritize guaranteed income over growth potential. If your entire pension plan comparison India research prioritizes capital protection above all else, insurer annuities provide that certainty.

Key trade-offs to know before you commit

Low annuity rates mean your money grows slowly, often underperforming inflation. The complete loss of liquidity and high costs make these products expensive compared to self-managed withdrawal strategies using mutual funds or other instruments.

9. Mutual funds and systematic withdrawal plans for retirement

Mutual funds with systematic withdrawal plans offer the most flexible retirement income strategy among all options in a pension plan comparison India provides, letting you build a diversified portfolio during accumulation and create customized withdrawal streams in retirement. You invest in equity, debt, or hybrid funds based on your risk appetite, then set up automatic monthly withdrawals once you retire. This approach gives you complete control over corpus size, withdrawal amounts, and asset allocation throughout retirement.

What it is and how it works

You invest in diversified mutual fund schemes through SIPs during your working years, building wealth through market-linked returns. At retirement, you set up a systematic withdrawal plan that automatically redeems units and transfers a fixed amount to your bank account monthly or quarterly. Your remaining corpus stays invested and continues growing.

Expected returns and risk profile

Equity funds historically deliver 12% to 15% annually over long periods, while hybrid funds offer 8% to 12%. Returns fluctuate with markets, creating short-term volatility but potentially higher retirement income compared to fixed-return products.

Tax treatment of gains and withdrawals

Each withdrawal triggers capital gains tax based on holding period. Equity fund gains beyond Rs 1.25 lakh annually face 12.5% LTCG tax, while debt fund gains get taxed at your slab rate.

Liquidity and how to build a withdrawal plan

You access your money anytime without penalties. Structure withdrawals to last through retirement by limiting annual drawdowns to 4% to 5% of your corpus initially.

Costs and charges

Mutual funds charge expense ratios between 0.5% and 2.5% annually. Direct plans cut costs by roughly 1% compared to regular plans.

Who it fits best

This works for retirees comfortable with market volatility who want growth potential and complete flexibility. You need discipline to avoid excessive withdrawals during market downturns.

"SWPs let you control both your retirement income and investment strategy instead of locking into fixed annuity rates."

Key trade-offs to know before you commit

Market crashes can deplete your corpus faster if you withdraw during downturns. You bear full sequence of returns risk without guaranteed income floors.

Next steps to pick your plan

Starting with your current financial situation and retirement timeline gives you the clearest path forward in any pension plan comparison India offers. Calculate your expected monthly expenses after retirement, then work backwards to determine the corpus size you need and which combination of schemes delivers that target with acceptable risk. Your age, tax bracket, and existing investments all influence whether you should prioritize NPS for tax benefits, PPF for safety, or mutual funds for growth potential.

Most investors benefit from a diversified retirement strategy that combines multiple instruments rather than betting everything on a single option. The right mix changes as you age, shifting from growth-focused equity funds in your 30s to more stable options like debt funds and annuities as you approach retirement. Sign up with Invsify to get AI-powered recommendations tailored to your specific situation, complete with real-time tracking and conflict-free guidance that shows you exactly how much you'll save by avoiding traditional distributor commissions.