Personal Financial Planning Guide: Step-by-Step for India

Shlok Sobti

Personal Financial Planning Guide: Step-by-Step for India

Your salary hits your account every month. Rent gets paid. Bills get cleared. You buy groceries and maybe order food a few times. By month end, you wonder where it all went. You want to save more, invest better, and stop feeling anxious about money. But creating a financial plan feels overwhelming when you do not know where to start.

The good news is that personal financial planning is not rocket science. You do not need an MBA or a fat bank balance to begin. What you need is a simple system to understand where you stand today, decide where you want to go, and map out the steps to get there. This approach works whether you earn ₹30,000 or ₹3 lakhs per month.

This guide walks you through five practical steps to build your own financial plan. You will learn how to assess your current money situation, set goals that matter, create a budget that actually works, protect yourself from emergencies, and invest for your future. Each step is designed for Indian realities, from EPF contributions to Section 80C benefits. By the end, you will have a clear roadmap to take control of your finances.

Why personal financial planning matters in India

Your income faces unique pressures in India that make planning non-negotiable. Inflation sits between 5-7% annually, which means your money loses value every year if it just sits in a savings account. Medical costs rise faster than salaries. Education expenses double every few years. Property prices keep climbing in most cities. Without a plan, your purchasing power shrinks even when your salary grows.

The real cost of delay

Most Indians start thinking about money seriously only in their 30s or 40s. By then, you have lost 10-15 years of potential compound growth on your investments. A ₹5,000 monthly SIP started at 25 grows to roughly ₹1.5 crores by 55 (assuming 12% returns). Start the same SIP at 35, and you get only ₹60 lakhs. That 10-year delay costs you ₹90 lakhs. Time is your biggest asset when building wealth, and this personal financial planning guide helps you use it wisely.

Starting early gives you the luxury of taking calculated risks and recovering from mistakes.

What planning actually does for you

Planning removes the guesswork from money decisions. You know exactly how much to save for your child's college, when you can afford that car upgrade, and whether you are on track for retirement. It helps you optimize tax deductions under Section 80C and 80D without scrambling every March. Your emergency fund protects you when job losses or medical issues strike, which they do more often than people expect. Planning also stops you from making emotional investment choices during market ups and downs. You follow your system instead of reacting to news headlines or neighbor's stock tips.

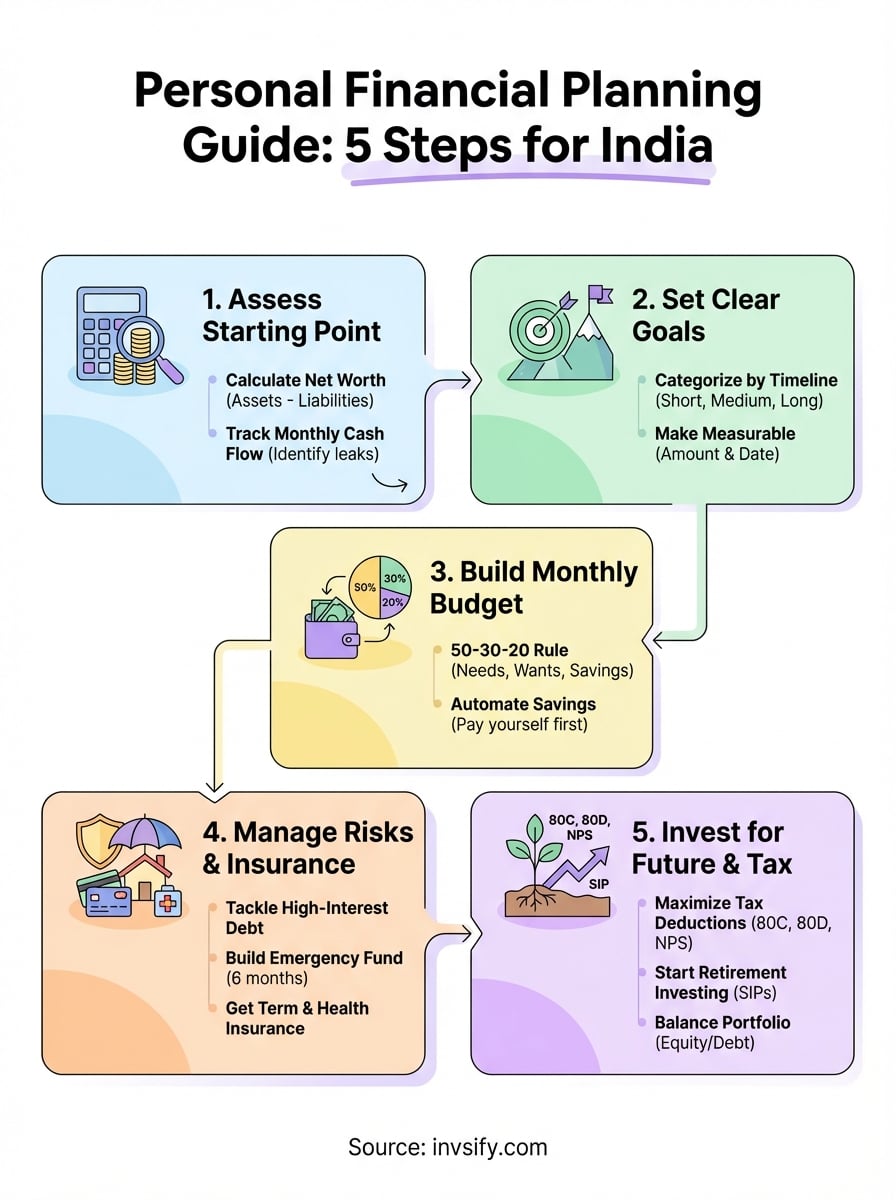

Step 1. Assess your starting point

You cannot plan a journey without knowing where you stand today. Your financial starting point has two parts: your net worth (what you own minus what you owe) and your monthly cash flow (what comes in versus what goes out). This first step in any personal financial planning guide takes just 2-3 hours but gives you total clarity on your money situation. Most people skip this step and jump straight to investing, which is like trying to run before learning to walk.

Calculate your net worth

Your net worth shows your financial health in one number. List everything you own (bank balance, EPF, mutual funds, property value, gold) and subtract everything you owe (home loan, car loan, credit card dues, personal loans). A simple table helps you organize this:

Assets | Value (₹) | Liabilities | Amount (₹) |

|---|---|---|---|

Savings account | 80,000 | Credit card debt | 15,000 |

EPF balance | 2,50,000 | Car loan | 1,80,000 |

Mutual funds | 1,20,000 | Personal loan | 0 |

Total Assets | 4,50,000 | Total Liabilities | 1,95,000 |

Your net worth equals ₹4,50,000 minus ₹1,95,000, which gives you ₹2,55,000. This number might be negative when you start your career, which is normal. The goal is to track it every six months and watch it grow.

Track your monthly cash flow

Download your last three months of bank statements and categorize every expense. Your salary might be ₹60,000, but you need to see where it actually goes. Create buckets: rent (₹18,000), groceries (₹8,000), utilities (₹3,000), eating out (₹5,000), EMIs (₹12,000), subscriptions (₹2,000), and others. Many Indians discover they spend ₹4,000-6,000 monthly on food delivery without realizing it. This awareness alone helps you find money to save and invest.

Tracking expenses for three months reveals patterns that a single month's data misses.

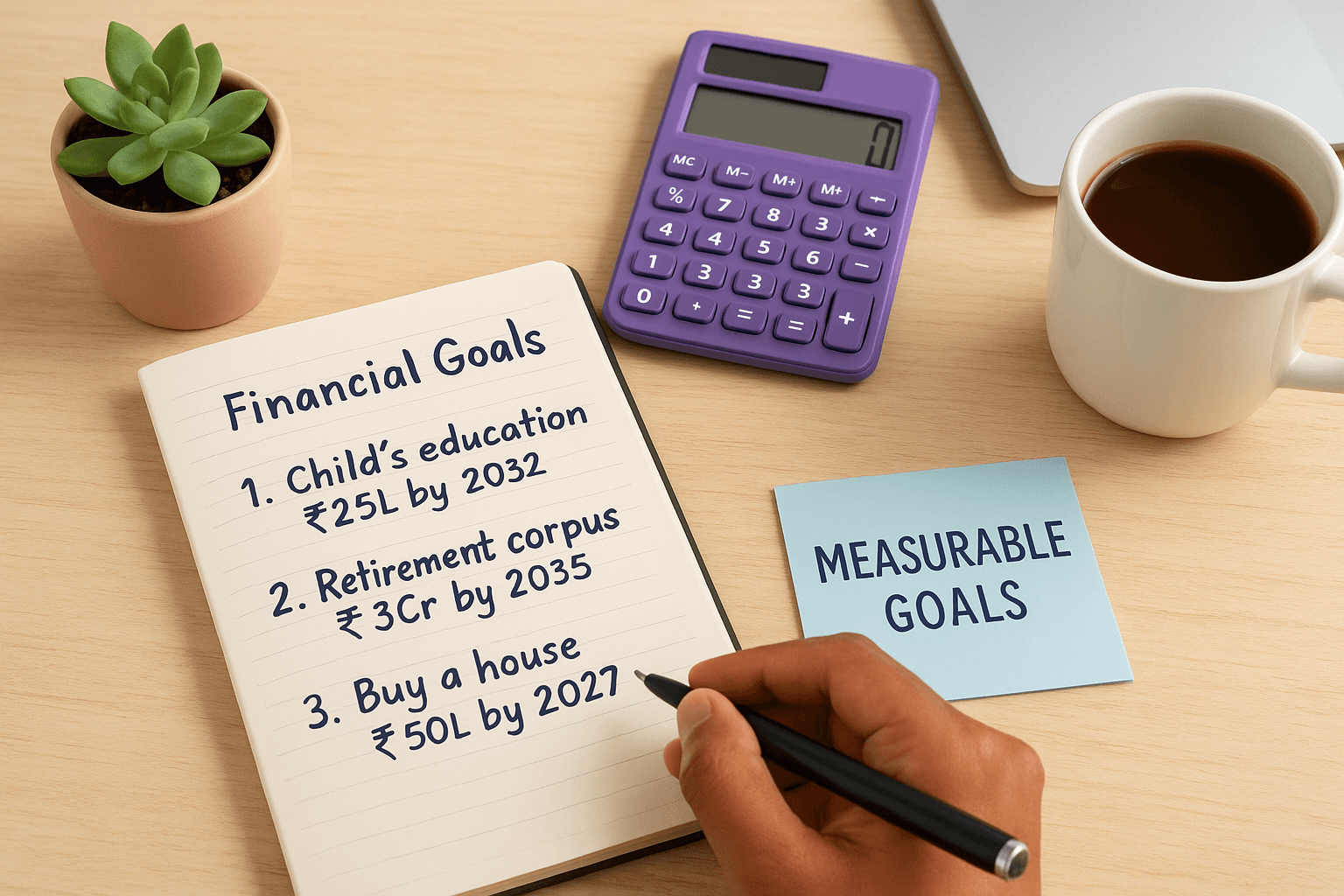

Step 2. Set clear financial goals

Goals give your money a purpose beyond just accumulating numbers in a bank account. You need to know what you are saving for and when you need that money. Vague wishes like "I want to be rich" or "I should save more" never work because you cannot measure progress or know when you have achieved them. This step in your personal financial planning guide transforms fuzzy intentions into concrete targets that drive your daily money decisions.

Sort goals by timeline

Your goals fall into three buckets based on when you need the money. Short-term goals (1-3 years) include building an emergency fund, buying a laptop, or taking a vacation. Medium-term goals (3-7 years) cover things like a car purchase, wedding expenses, or a home down payment. Long-term goals (7+ years) focus on your child's education, retirement corpus, or buying property outright. Each timeline demands different savings and investment strategies, which is why categorizing matters.

Timeline | Goal Examples | Suitable Instruments |

|---|---|---|

Short-term (1-3 years) | Emergency fund, vacation | Savings account, liquid funds, FDs |

Medium-term (3-7 years) | Car, wedding, house down payment | Debt mutual funds, balanced funds |

Long-term (7+ years) | Retirement, child's education | Equity mutual funds, PPF, NPS |

Make goals measurable

Every goal needs a specific number and date attached to it. Instead of "save for retirement," write "accumulate ₹3 crores by age 55" or instead of "pay for child's education," specify "save ₹25 lakhs by 2032 for engineering college." These numbers tell you exactly how much to invest monthly. A goal template helps you structure this:

Goal: Child's engineering education

Amount needed: ₹25 lakhs

Target year: 2032 (8 years away)

Expected return: 12% per year

Monthly SIP required: ₹15,500

Measurable goals convert wishful thinking into an actionable savings plan with clear monthly commitments.

You can use online SIP calculators to figure out monthly amounts for each goal. Write down your top 3-5 goals with their numbers and dates. This clarity stops you from starting random investments that do not align with your actual needs.

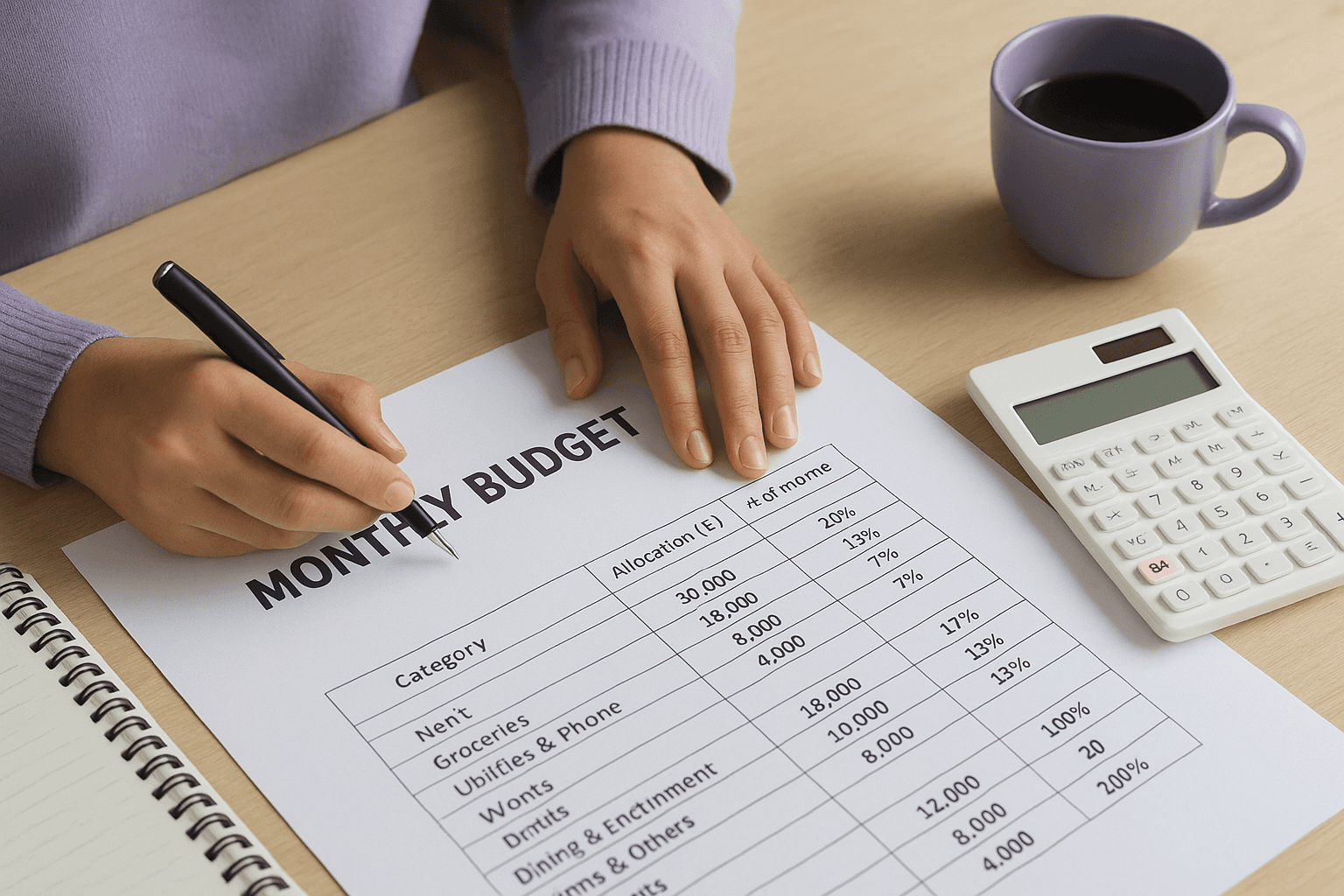

Step 3. Build your monthly budget and cash flow

A budget is not about restricting your spending or living like a monk. It gives you permission to spend guilt-free on things that matter while cutting waste from things that do not. Your budget connects your income to your goals by allocating every rupee a job. This step in your personal financial planning guide turns your financial goals from wishes into monthly action items. You decide in advance where your money goes instead of wondering where it went.

Choose a budgeting method that fits your style

The 50-30-20 rule works well for most Indian salaries and keeps budgeting simple. You split your after-tax income into three buckets: 50% for needs (rent, groceries, utilities, EMIs, insurance), 30% for wants (eating out, shopping, entertainment, hobbies), and 20% for savings and investments (SIPs, EPF, emergency fund). This framework gives you structure without making you track every single transaction.

A basic monthly budget template looks like this:

Category | Allocation (₹) | % of Income |

|---|---|---|

Needs | 30,000 | 50% |

Rent | 18,000 | 30% |

Groceries | 8,000 | 13% |

Utilities & Phone | 4,000 | 7% |

Wants | 18,000 | 30% |

Dining & Entertainment | 10,000 | 17% |

Shopping & Others | 8,000 | 13% |

Savings | 12,000 | 20% |

SIPs | 8,000 | 13% |

Emergency Fund | 4,000 | 7% |

Total Income | 60,000 | 100% |

Your percentages might differ based on your city and life stage. Someone living with parents can push savings to 40-50%. High-rent cities like Mumbai or Bangalore might force needs up to 60%.

Track and adjust weekly

Budgets fail when you set them once and forget them. Check your spending every Sunday against your plan. Most banking apps show category-wise breakdowns that take 10 minutes to review. You will spot problems early before they spiral. Did you overspend on wants this week? Pull back the next week to stay on track for the month.

A budget only works when you review it regularly and make real-time adjustments to your spending behavior.

Automate your savings by setting up automatic transfers on salary day. Move your SIP amount and emergency fund contribution to separate accounts before you can spend them. Pay yourself first, then budget the remainder. Your wants category has the most flexibility, so adjust it when unexpected expenses pop up. The key is protecting your 20% savings rate no matter what. That non-negotiable commitment separates people who build wealth from those who stay stuck.

Step 4. Manage debt, emergencies and insurance

Your financial plan falls apart fast if you ignore protection basics. Debt drains your wealth through interest payments. Emergencies without savings push you deeper into loans. Medical crises or income loss without insurance wipe out years of savings in months. This step in your personal financial planning guide focuses on building shields that protect everything you have worked to create. You need defense before offense.

Tackle high-interest debt first

Credit card balances and personal loans eat your money through 15-36% annual interest rates that compound monthly. Your first priority is eliminating these toxic debts before serious investing begins. Use the avalanche method by listing all debts with their interest rates, then throwing every extra rupee at the highest-rate debt while paying minimums on others.

Here is what this looks like in practice:

Debt Type | Balance (₹) | Interest Rate | Action |

|---|---|---|---|

Credit card | 50,000 | 36% | Attack with ₹8,000/month |

Personal loan | 1,20,000 | 18% | Pay minimum ₹5,000/month |

Car loan | 2,80,000 | 9% | Pay minimum ₹10,000/month |

Once you clear the credit card, redirect that ₹8,000 to the personal loan. This snowball effect kills debt faster than spreading payments evenly. Avoid taking new loans while clearing old ones, no matter how attractive the offer sounds.

Build your emergency fund layer by layer

Your emergency fund catches you when income stops or unexpected bills arrive. Start with a ₹50,000 starter fund even if you have debt, then push to 6 months of essential expenses once high-interest debt is gone. Essential expenses include only rent, groceries, utilities, EMIs, and insurance, not your wants bucket.

Park this money in a savings account or liquid mutual fund where you can access it within 24 hours. Your EPF balance does not count as emergency money because withdrawals take weeks and come with penalties. Building ₹3 lakhs (6 months of ₹50,000 expenses) takes time, so set up a monthly auto-transfer of whatever you can afford.

An emergency fund protects your investments by preventing forced withdrawals during market downturns when you need cash.

Cover your income and health risks

Insurance transfers risks you cannot afford to bear yourself. Term life insurance should cover 10-15 times your annual income if anyone depends on your salary. A ₹6 lakh salary needs ₹60-90 lakh coverage, which costs ₹8,000-12,000 yearly for a healthy 30-year-old. Buy term plans online directly from insurers to avoid agent commissions that inflate premiums.

Health insurance needs ₹5-10 lakh coverage minimum per person, more in expensive cities like Mumbai or Bangalore. Your employer's group cover is not enough because it ends when you change jobs, often when you need it most. Get a personal floater policy for your family that stays with you regardless of employment. These two insurance types form your financial safety net, letting you invest aggressively without worry.

Step 5. Invest smartly for taxes and retirement

Investing bridges the gap between saving money and building real wealth. Your savings account gives 3-4% returns while inflation runs at 6-7%, which means you lose purchasing power every year. Strategic investing in equity and debt instruments helps you beat inflation, grow your corpus for long-term goals, and claim legitimate tax deductions that put thousands back in your pocket. This step in your personal financial planning guide transforms you from a saver into a wealth builder who uses the tax code to your advantage.

Maximize tax deductions within Section 80C and beyond

Section 80C lets you deduct ₹1.5 lakhs annually from taxable income through specific investments like EPF contributions, PPF deposits, ELSS mutual funds, life insurance premiums, and home loan principal repayments. Someone in the 30% tax bracket saves ₹46,800 yearly by maxing out 80C, which is free money you should never leave on the table. Section 80D adds another ₹25,000 deduction for health insurance premiums (₹50,000 if covering parents above 60).

Your tax-saving strategy should look something like this:

Instrument | Annual Investment (₹) | Lock-in | Expected Return |

|---|---|---|---|

EPF (automatic) | 60,000 | Till retirement | 8.15% |

ELSS mutual fund | 50,000 | 3 years | 10-12% |

PPF | 40,000 | 15 years | 7.1% |

Health insurance | 25,000 | 1 year | Protection value |

Total 80C + 80D | 1,75,000 | Varies | Tax saving ₹52,500 |

ELSS funds work best for young investors because they offer equity exposure with the shortest 3-year lock-in among 80C options. PPF suits conservative investors who want guaranteed returns. Spread your ₹1.5 lakh across multiple instruments instead of putting everything in one place to balance growth and safety.

Start your retirement investing today

Your EPF contributions form the base of retirement savings, but they will not be enough. A comfortable retirement needs 25-30 times your annual expenses as corpus. If you spend ₹6 lakhs yearly today, you need ₹1.5-1.8 crores at retirement (accounting for inflation). Starting a ₹10,000 monthly SIP in equity mutual funds at age 25 can build ₹3 crores by 55, assuming 12% returns. Wait till 35, and the same SIP gives you only ₹1.2 crores.

National Pension System (NPS) adds tax efficiency with an extra ₹50,000 deduction under Section 80CCD(1B) beyond your 80C limit. This brings total tax-saving potential to ₹2 lakhs yearly. NPS works well as a retirement-focused product because withdrawals are restricted till 60, forcing long-term discipline that equity mutual funds do not impose.

Starting retirement investing in your 20s gives you 30-35 years of compounding, which does the heavy lifting while you contribute relatively small monthly amounts.

Balance your portfolio by age and goals

Asset allocation determines 80-90% of your returns, not stock picking or timing the market. Your equity exposure should roughly equal 100 minus your age. A 30-year-old can handle 70% equity and 30% debt, while a 50-year-old should shift to 50% equity and 50% debt. Equity mutual funds through SIPs work for goals beyond 7 years, while debt funds or FDs suit goals under 5 years.

Review your portfolio every six months and rebalance when allocations drift by more than 5%. Avoid chasing hot sectors or tips from colleagues because they usually buy at peaks and panic-sell at bottoms. Stick to diversified index funds or large-cap funds that give you broad market exposure without requiring constant monitoring or stock market expertise.

Keeping your plan on track

Your personal financial planning guide does not end once you create it. Plans become outdated fast as salaries change, expenses shift, goals get achieved, and new priorities emerge. Markets move up and down, inflation rates fluctuate, and your life circumstances evolve through marriage, children, job switches, or relocations. Review and adjust your plan every six months to keep it aligned with your current reality instead of letting it gather digital dust in a forgotten spreadsheet.

Schedule regular financial check-ins

Block two hours every January and July for a complete financial review. Pull up your net worth statement, budget tracker, investment portfolio, and goal list. Calculate your current net worth and compare it to six months ago. Check if your savings rate held at 20% or slipped. Review each goal's progress by looking at actual corpus built versus the target amount needed. This disciplined review catches problems early before they derail your entire plan.

Regular reviews transform your financial plan from a one-time document into a living system that adapts to your changing life.

A simple review checklist keeps you focused:

Review Item | Action |

|---|---|

Net worth | Calculate and compare to last review |

Budget | Check spending vs. plan for past 6 months |

Emergency fund | Verify it still covers 6 months expenses |

Debt | Track reduction progress and interest paid |

Investments | Rebalance if allocation drifts beyond 5% |

Goals | Update timelines and required monthly amounts |

Adjust for major life changes

Marriage, childbirth, job changes, or property purchases demand immediate plan updates, not waiting for your scheduled review. Your budget needs restructuring when rent doubles after relocation or expenses jump with a new baby. Increase insurance coverage when dependents arrive or income grows significantly. Adjust your SIP amounts upward after salary hikes instead of inflating lifestyle expenses. Life changes happen whether you plan for them or not, so build flexibility into your financial system that accommodates reality instead of fighting it.

Conclusion

You now have a complete personal financial planning guide that covers assessment, goal-setting, budgeting, protection, and investing. These five steps work whether you earn ₹30,000 or ₹3 lakhs monthly because the principles stay the same. Start with step one today instead of waiting for the perfect moment that never arrives. Invsify's AI-powered advisory can help you build and track your personalized plan with real-time insights and tax optimization strategies built specifically for Indian investors. Your financial future depends on actions you take now, not intentions you keep postponing.