Personal Investment Goals: Set, Plan, and Achieve in India

Shlok Sobti

Personal Investment Goals: Set, Plan, and Achieve in India

You know you should invest, but every time you open your investment app, you freeze. Should you put money in mutual funds for retirement? Save for your child's education? Build an emergency corpus? Without clear targets, your money sits idle or gets scattered across random investments that may not serve any real purpose.

Personal investment goals give your money direction. They transform vague wishes into specific targets with deadlines and amounts. When you know exactly what you're saving for, you can choose the right investment products, calculate how much to invest monthly, and measure your progress along the way.

This guide walks you through setting investment goals that match your life in India. You'll learn how to assess where you stand financially, turn your priorities into actionable targets, match each goal to suitable investment options, and track your progress. By the end, you'll have a clear roadmap that connects your current income to your future aspirations, whether that's buying a home in three years or retiring comfortably in 25.

Why personal investment goals matter in India

India's financial landscape puts unique pressure on your money. Inflation consistently runs at 5-6% annually, eating away at savings that sit in regular bank accounts earning 3-4%. Your salary might increase every year, but without specific targets, lifestyle expenses expand to match your income. You end up with the same financial stress despite earning more, and retirement feels as distant as it did five years ago.

Goals create clarity in a crowded financial market

Setting personal investment goals cuts through the noise of endless investment products. Instead of jumping between trending mutual funds or the latest tax-saving scheme your colleague mentioned, you filter every financial decision through a simple question: does this help me reach my specific goal? This focus prevents you from spreading your money too thin across investments that don't align with your timeline or risk tolerance.

Goals turn abstract worries into concrete plans

Most Indians juggle multiple financial priorities at once. You might need to save for your child's education, build a retirement corpus, plan for a home down payment, and support aging parents. Without clear goals, these competing demands create paralysis. You know you should invest more, but you don't know where to allocate each rupee.

When you assign specific amounts and deadlines to each priority, you transform overwhelming financial stress into a manageable monthly action plan.

Defined goals also protect you from emotional investing decisions. Markets will drop, panic will set in, and your instinct will tell you to sell everything. But when you're investing toward a goal 15 years away, a temporary market dip becomes irrelevant. Your goal's timeline keeps you invested through volatility, which historically delivers better returns than trying to time the market.

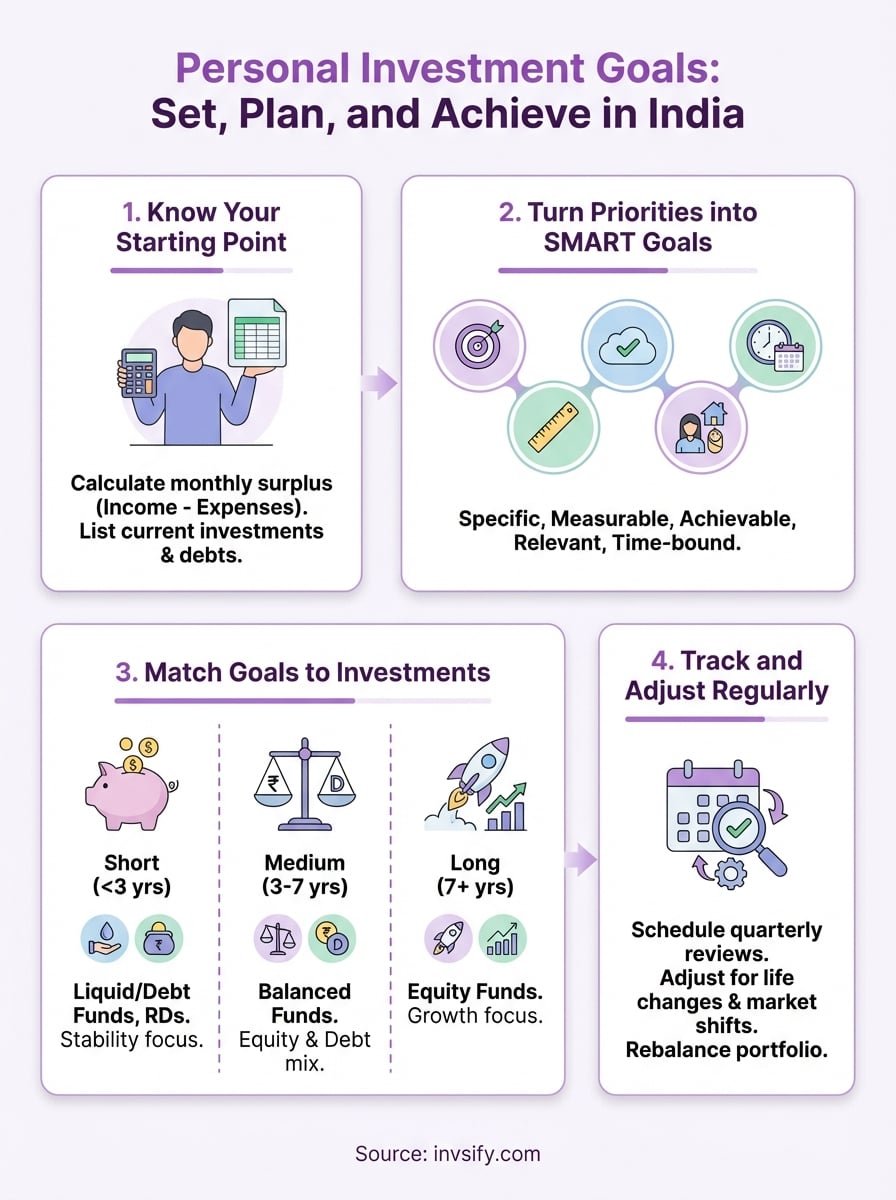

Step 1. Know your financial starting point

You cannot set realistic personal investment goals without knowing how much money flows in and out each month. Most people overestimate their investable income because they ignore irregular expenses like annual insurance premiums, festival shopping, or medical emergencies. Your actual monthly surplus (the amount available to invest) typically runs 20-30% lower than what you initially calculate.

Start by tracking every rupee for at least two months. Don't rely on memory or rough estimates. Use your bank statements, credit card bills, and UPI transaction history to capture your real spending patterns. This exercise reveals the gap between what you think you spend and what you actually spend, and that gap determines whether your investment targets are achievable or wishful thinking.

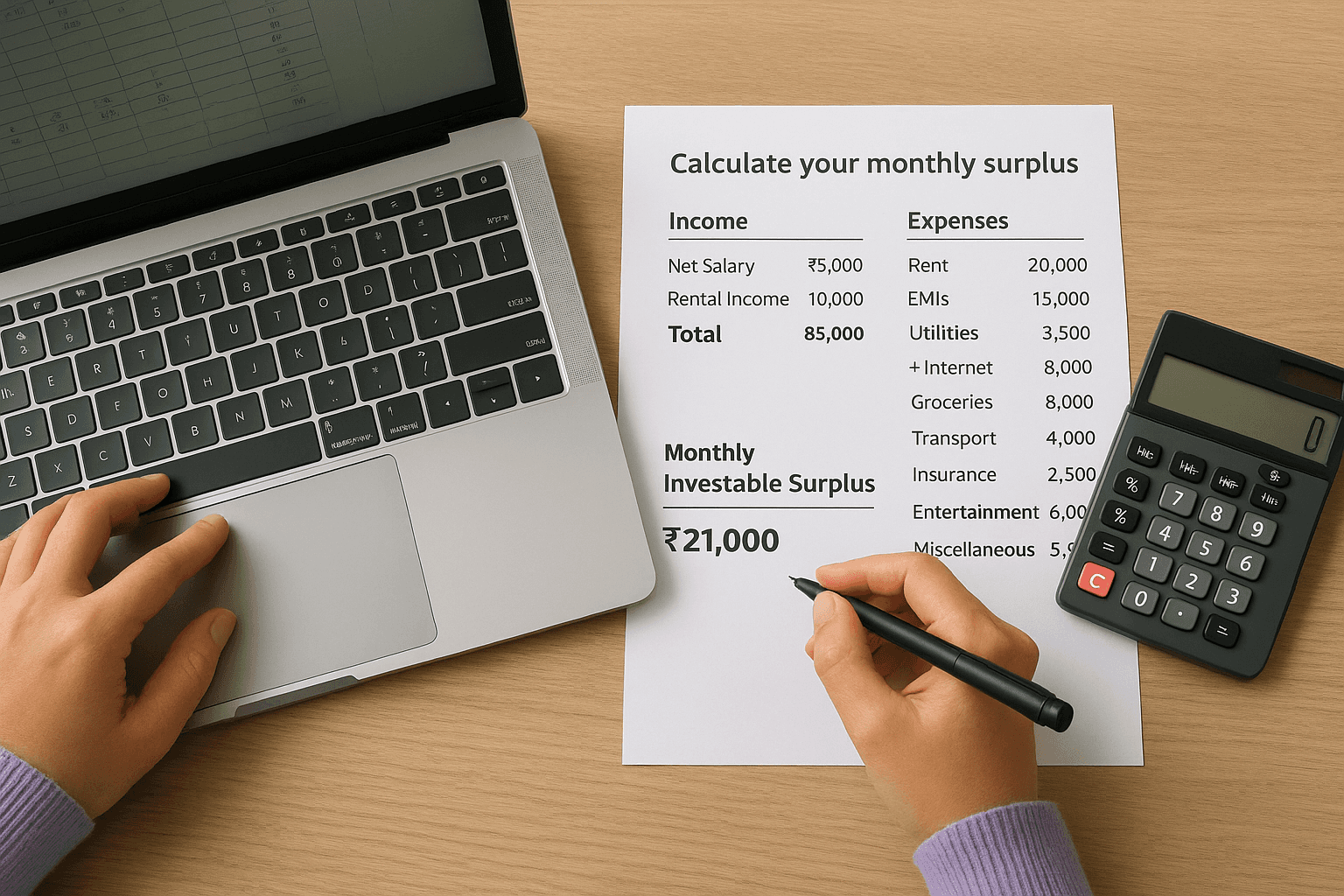

Calculate your monthly surplus

Open a spreadsheet and create two columns: income and expenses. List your post-tax monthly salary in the income column, including any predictable bonuses or rental income you receive consistently. In the expenses column, break down your spending into fixed costs (rent, EMIs, insurance) and variable costs (groceries, transport, entertainment, dining out).

Your investable surplus tells you the maximum amount you can commit to goals each month without disrupting your lifestyle or building debt.

List your current investments and debts

Create an inventory of everything you own and owe. Write down each investment with its current value, expected return, and maturity date. Include provident fund balances, mutual funds, stocks, fixed deposits, real estate, and gold. Then list all debts with outstanding amounts, interest rates, and monthly EMIs. High-interest debt above 12% (credit cards, personal loans) should be cleared before you commit serious money to new investments, because no investment consistently beats 18-24% credit card interest.

Step 2. Turn priorities into SMART goals

You've identified your monthly surplus and listed your current assets. Now transform your vague financial wishes into concrete targets. A properly structured goal includes a specific amount, a clear deadline, and a realistic plan to get there. Without these three elements, "I want to save for retirement" remains an intention that never translates into consistent action.

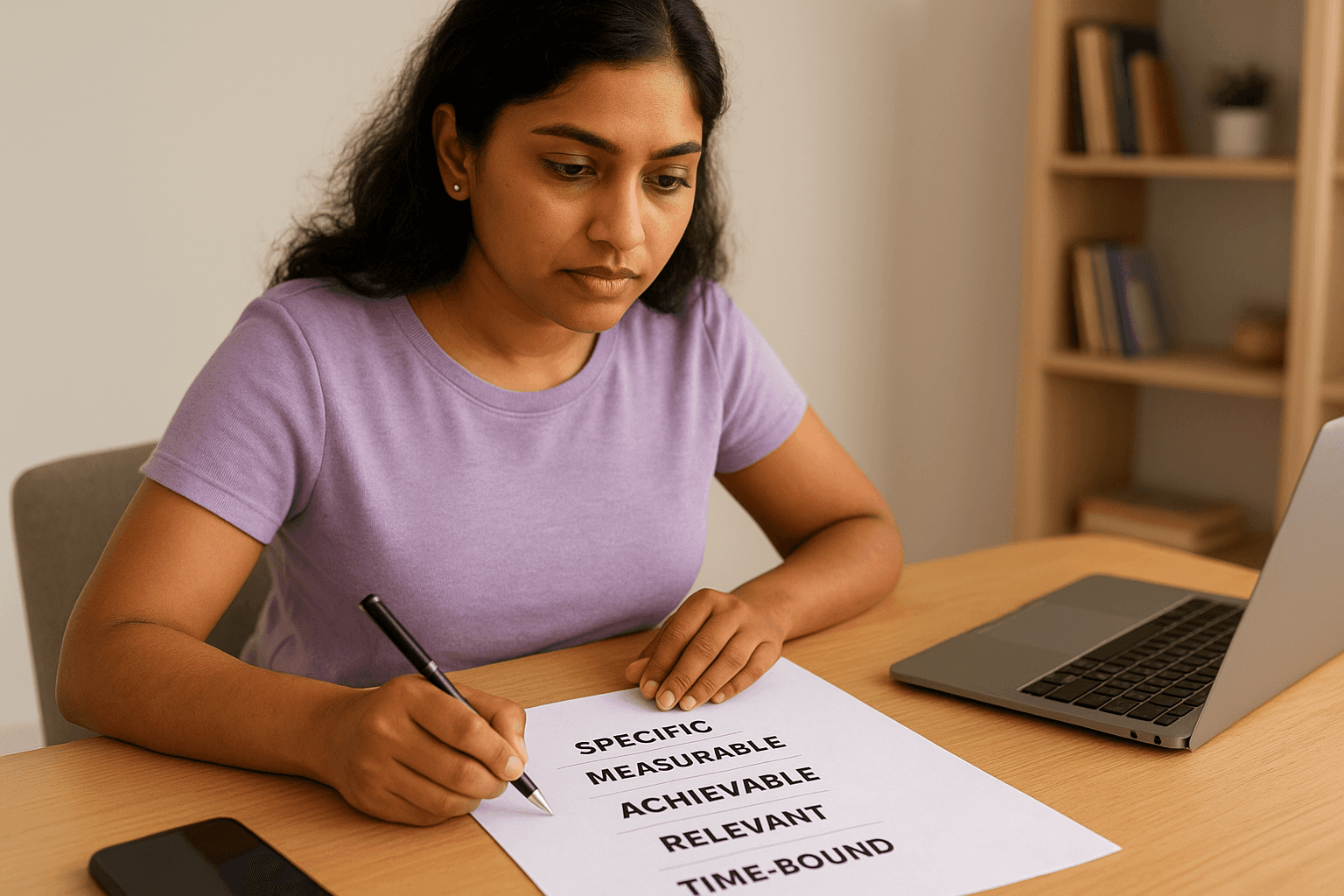

Define what SMART means for Indian investors

SMART goals give you five checkpoints to verify whether your target makes sense. Specific means you name the exact purpose and amount (not "save money" but "accumulate ₹15 lakh for home down payment"). Measurable means you can track progress in rupees and percentage terms each month. Achievable tests whether your goal fits within your monthly surplus without forcing you into debt or extreme lifestyle cuts.

Relevant asks whether this goal actually matters to your life right now. If you're 28 and single, saving for your child's college fund isn't relevant yet, but building a marriage corpus or career development fund might be. Time-bound assigns a specific deadline, which determines which investment products make sense for that goal. A three-year goal and a 15-year goal require completely different investment approaches.

Create your SMART goal template

Write each goal following this structure, filling in every blank with specific numbers and dates. This template forces clarity and exposes unrealistic targets before you commit money to them.

Here's a concrete example of personal investment goals structured correctly:

When your goal fits this template with realistic numbers, you've created an actionable target instead of a wish.

List all your goals using this format. Rank them by priority, then allocate your monthly surplus starting from the highest priority goal and working down. If your surplus runs out before covering all goals, you face a choice: increase income, reduce expenses, extend timelines, or drop lower-priority goals entirely.

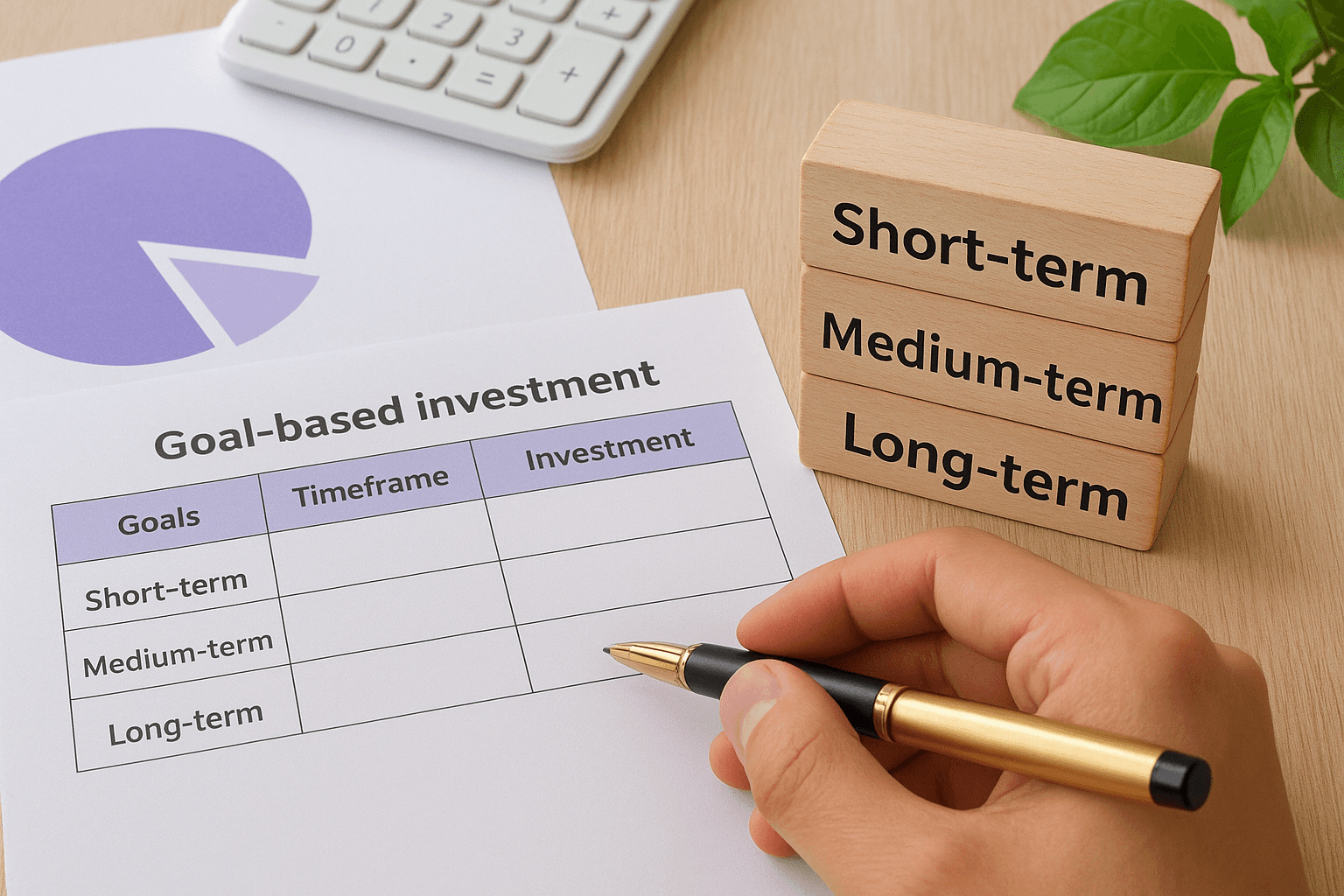

Step 3. Match each goal to the right investments

Your personal investment goals now have specific amounts and deadlines, but they're still abstract numbers until you connect them to actual investment products. Each goal lives in a different time zone, and time determines everything about which investments make sense. A goal due in two years cannot tolerate the volatility of equity funds, while a 20-year retirement goal wastes potential growth if you keep it in fixed deposits earning 6%. Match your timeline to the right product, and you maximize returns while controlling risk.

Short-term goals (under 3 years)

Goals with deadlines under three years need stability more than growth. You cannot afford to see your corpus drop by 20% six months before you need the money, which rules out equity exposure. Your wedding in 18 months or your car down payment in two years belongs in instruments that guarantee capital protection and provide liquidity when you need it.

Park these funds in liquid mutual funds, short-duration debt funds, or recurring deposits. Liquid funds give you 6-7% returns with same-day redemption. Short-duration debt funds offer slightly higher returns (7-8%) with minimal interest rate risk. Recurring deposits in banks lock in 6.5-7% returns with zero volatility. Fixed deposits work if you're certain about the timeline, but they penalize early withdrawal, so avoid them if your goal date might shift by a few months.

Medium-term goals (3-7 years)

Medium-term goals give you breathing room to add some equity exposure while maintaining a debt cushion. Your child's school admission in five years or your home down payment in six years can tolerate short-term market drops because you have time to recover. But you still need to protect a significant portion in stable instruments as the deadline approaches.

Start with 60-70% equity and 30-40% debt, then shift gradually toward debt as you approach the goal date. Use balanced advantage funds or hybrid funds that automatically adjust this mix, or manually rebalance every year. Equity exposure targets 10-12% annual returns, while the debt portion provides 7-8%, giving you a blended return of 9-10% with controlled volatility.

Start shifting from equity to debt two years before your goal date to protect accumulated gains from sudden market corrections.

Long-term goals (7+ years)

Goals beyond seven years give you the single biggest advantage in investing: time to ride out market cycles. Your retirement in 25 years or your child's college fund in 12 years should sit primarily in equity, where historical data shows 12-15% annual returns over extended periods. Equity volatility becomes irrelevant when you're not touching the money for a decade or more.

Allocate 80-90% to equity mutual funds (index funds or actively managed large-cap funds) and 10-20% to debt for rebalancing opportunities. Don't touch this allocation for at least five years. Review annually but resist the urge to shift money during market corrections, because timing the market consistently fails. As you approach within five years of the goal, start the gradual shift to debt using the medium-term strategy above.

Step 4. Track and adjust your plan over time

Setting personal investment goals creates your roadmap, but markets shift, salaries change, and life throws surprises that make your original plan outdated. Tracking your progress every quarter prevents you from discovering five years later that you're nowhere near your target. Regular reviews also catch underperforming investments early, when you still have time to course-correct instead of scrambling in the final year before your goal date.

Schedule quarterly progress checks

Block two hours every three months to review each goal. Open your investment account statements and calculate the current value of each goal-specific portfolio. Compare this actual value against what your goal tracker says you should have by now. If you're investing ₹10,000 monthly toward a ₹25 lakh goal over 10 years at 12% returns, you should have specific milestones at 3 months, 6 months, 1 year, and so on. A 5-10% deviation from your projected amount signals the need to investigate whether your returns are underperforming or your contributions have been inconsistent.

Use this simple quarterly checklist to stay on track:

Adjust when circumstances shift

Life changes demand goal updates, not guilt about abandoning your original plan. A salary increase of 20% means you can accelerate goals or add new ones. Job loss requires temporarily pausing investments and protecting your emergency fund first. Marriage, childbirth, or elderly parent care introduces competing priorities that force you to extend timelines or reduce target amounts for lower-priority goals.

Successful investing adapts to your reality instead of forcing your life to fit outdated targets set years ago.

Rebalance your portfolio when your actual asset allocation drifts 10% or more from your target. If your 70% equity allocation grows to 80% because of strong market gains, sell some equity and move it to debt to maintain your risk profile.

Put your goals into action

You now have everything you need: a clear financial starting point, SMART goals with specific deadlines, investment products matched to each timeline, and a quarterly review system. The gap between planning and wealth creation closes only when you take the first step today. Most people spend months researching the perfect investment strategy but never actually open an account or start their first SIP. Every month you delay costs you compound growth that you can never recover, even with higher contributions later.

Your personal investment goals deserve better than sitting in a document or spreadsheet. Start building your goal-based investment plan with Invsify, where AI-powered insights help you track progress across all your targets in one place. The platform calculates exactly how much you need to invest monthly for each goal, monitors your portfolio automatically, and alerts you when rebalancing becomes necessary. Stop wondering if you're on track and get data-backed answers instead.