What Is Personalized Investment Advice In India? A Guide

Shlok Sobti

What Is Personalized Investment Advice In India? A Guide

Personalized investment advice means getting recommendations tailored to your specific financial situation, goals, and risk tolerance. Instead of generic tips that work for everyone, you get a plan built around your income, age, family needs, tax situation, and where you want to be financially. A qualified advisor or AI platform studies your complete picture and suggests investments that match your life, not someone else's. The difference shows up in real returns. When your portfolio aligns with your actual circumstances, you avoid products that don't fit and focus on strategies that push you toward your targets.

This guide walks you through everything you need to know about personalized investment advice in India. You'll learn why customized recommendations matter more than off-the-shelf products, how to access professional guidance through human advisors or robo platforms, and what SEBI regulations protect you from hidden fees and commissions. We'll compare your options, break down the costs, and show you how to pick the right service for your wealth goals. By the end, you'll know exactly what to look for and which type of advisor fits your needs.

Why personalized investment advice matters

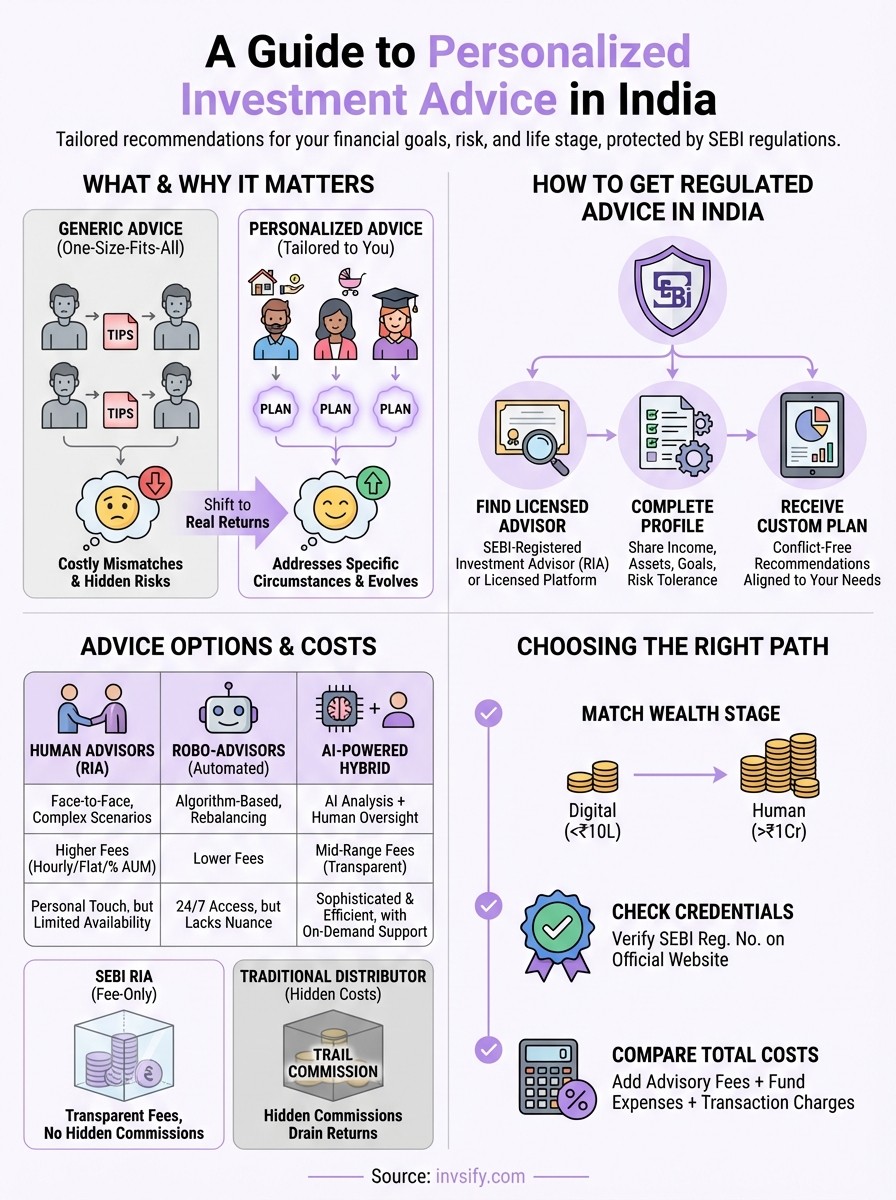

You lose money when you follow investment advice designed for someone else's life. Generic recommendations ignore your actual income level, your debt obligations, and your family's immediate needs. A strategy that works for a 25-year-old bachelor won't fit a 40-year-old parent saving for college fees while supporting aging parents. When you invest based on what worked for others, you end up taking either too much risk or too little, and both paths cost you returns over time. Personalized investment advice matters because it addresses your specific circumstances and builds a portfolio that matches where you are now and where you want to go.

Generic advice creates costly mismatches

Most investment content online treats every reader the same. Articles recommend mutual funds without knowing if you need liquidity next year or can lock funds for a decade. YouTube videos push equity allocations without understanding your risk tolerance or existing obligations. Following this broad guidance leads to portfolios filled with products that don't serve your goals. You might own tax-saving instruments when you're already maximizing deductions, or aggressive growth funds when you need stable income in five years. These mismatches compound as fees pile up on unsuitable investments.

Customized advice eliminates the trial-and-error approach that drains both time and capital.

Your financial situation is unique

Your earning pattern, monthly expenses, and future commitments differ from every other investor in India. A personalized approach accounts for your job stability, existing insurance coverage, outstanding loans, and whether you're planning to buy property or start a business. The advisor or platform considers your tax bracket, evaluates your current holdings, and identifies gaps in your financial protection before suggesting new investments.

Building wealth requires strategies that adapt as your life changes. When you get married, have children, or switch careers, your portfolio needs adjustment. Personalized investment advice evolves with you instead of offering the same fixed recommendations year after year. This ongoing alignment keeps your money working efficiently toward outcomes that matter specifically to you.

How to get personalized advice in India

Getting personalized investment advice in India requires you to work with qualified professionals or platforms that hold proper regulatory licenses. You can't rely on random WhatsApp groups, Twitter threads, or YouTube channels because they lack accountability and rarely understand your specific financial circumstances. The process starts with finding a SEBI-registered advisor or a licensed platform that offers customized recommendations based on thorough analysis of your financial situation. You'll need to complete detailed profiling, share documents about your income and assets, and clarify your short-term and long-term goals. This groundwork ensures the advice you receive addresses your actual needs instead of generic market trends.

Find a SEBI-registered investment advisor

Your first option is hiring a Registered Investment Advisor (RIA) who operates under SEBI's strict guidelines. These advisors charge transparent fees and cannot earn commissions from product manufacturers, which removes the conflict of interest that plagues traditional distributors. You can verify an advisor's registration on the SEBI website by checking their license number and ensuring they haven't faced any disciplinary actions. Look for advisors who specialize in your wealth bracket and financial stage, whether you're starting your career or managing retirement funds.

Working with a SEBI-registered advisor guarantees that recommendations serve your interests, not the advisor's commission structure.

The advisor will request bank statements, tax returns, existing investment proofs, and insurance policies during your first meetings. This documentation helps them calculate your net worth, assess your cash flow patterns, and identify gaps in your financial protection. Expect to answer detailed questions about your family obligations, career trajectory, and major expenses you anticipate in the coming years.

Use digital platforms with advisory licenses

Several Indian platforms now offer personalized investment advice through AI-powered tools combined with human oversight. These services operate under SEBI's investment advisory regulations but deliver recommendations through apps and websites instead of face-to-face meetings. Digital platforms typically charge lower fees than traditional advisors while maintaining the same regulatory standards. You complete your financial profile online, answer questions about your goals and risk tolerance, and receive a customized portfolio suggestion within minutes.

Platforms like Invsify combine artificial intelligence with SEBI registration to provide conflict-free recommendations without the markup costs of traditional channels. The technology analyzes thousands of data points about your finances and matches them against market opportunities that fit your profile. You get 24/7 access to your portfolio dashboard, real-time adjustments based on changing circumstances, and transparent fee structures that show exactly what you pay.

Complete your financial profile properly

Accurate profiling determines the quality of personalized investment advice you receive. Rushing through questionnaires or hiding debt obligations produces recommendations that don't match reality. Spend time documenting your complete income sources, including salary, rental income, business profits, and any freelance earnings. List all your existing investments with current values, your monthly expenses broken down by category, and outstanding loans with their interest rates and remaining tenures.

Your risk tolerance assessment matters as much as your financial data. Answer questions honestly about how you'd react to market downturns, whether you've invested in equity before, and how much volatility you can handle without losing sleep. Overestimating your risk appetite leads to aggressive portfolios that you'll abandon during corrections, while underestimating it locks you into conservative options that won't meet your growth targets.

Human, robo, and AI advice options in India

You have three main routes to access personalized investment advice in India: traditional human advisors, automated robo-advisors, and AI-powered hybrid platforms. Each approach offers different levels of interaction, pricing structures, and customization depth. Human advisors provide the most personal touch with face-to-face meetings and phone calls, while robo-advisors deliver algorithm-based recommendations at lower costs. AI-powered platforms combine machine learning with optional human oversight, giving you sophisticated analysis without the premium fees of full-service advisors. Understanding these options helps you match your preference for technology versus personal interaction with what you're willing to pay.

Human financial advisors

Traditional human advisors meet you in person or connect through video calls to discuss your financial situation in detail. They ask probing questions about your career plans, family dynamics, and concerns that numbers alone don't capture. These advisors excel at handling complex scenarios like business succession planning, multi-generational wealth transfer, or coordinating investments across different family members. You get someone who remembers your previous conversations and adjusts recommendations based on major life changes you discuss.

The downside is availability. Human advisors work during business hours and require appointments, which means you can't get instant answers at midnight when market news breaks. They also charge higher fees because you're paying for their time, expertise, and ongoing relationship management.

Robo-advisors and automated platforms

Robo-advisors use algorithms to create and manage portfolios based on questionnaires you complete about your goals and risk tolerance. These platforms automatically rebalance your investments, harvest tax losses, and adjust allocations as markets shift. You pay significantly lower fees than human advisors because computers handle the work, and you can access your account anytime through mobile apps.

Robo-advisors work best when your financial situation is straightforward and you don't need someone to explain strategy changes in detail.

These platforms struggle with nuanced decisions that require judgment calls. They can't factor in your side business plans, inheritance expectations, or unique family obligations unless those fit into pre-programmed categories.

AI-powered hybrid models

Modern AI platforms analyze thousands of data points about your finances and compare them against historical patterns and current market conditions. Unlike simple robo-advisors, these systems learn from your behavior, adjust to changing regulations, and provide explanations for recommendations instead of just showing portfolio allocations. You get the speed and efficiency of automation plus the depth of analysis that traditional algorithms miss.

Hybrid models often include human advisors on demand, letting you schedule calls when you need clarification or face major decisions. Platforms like Invsify combine SEBI-registered advisory with AI technology, offering 24/7 access to intelligent recommendations while keeping human experts available for complex questions. This setup gives you continuous monitoring and instant updates without paying for full-time human attention you don't always need.

Costs, SEBI rules, and hidden commissions

Understanding what you pay for personalized investment advice requires looking beyond advertised fees to the complete cost structure. Many investors in India lose significant returns to hidden commissions and indirect charges they never see itemized on statements. SEBI regulations attempt to protect you from conflicts of interest and ensure transparency, but the rules work only if you know what to look for. Your advisor's fee model determines whether they prioritize your returns or their own compensation, making this knowledge critical before you commit your capital.

SEBI regulations that protect you

SEBI mandates that Registered Investment Advisors (RIAs) operate on a fee-only basis, meaning they cannot accept commissions from mutual fund houses, insurance companies, or other product manufacturers. This rule eliminates the incentive to recommend high-commission products over better alternatives. RIAs must also maintain a fiduciary duty to act in your best interest at all times, document their rationale for recommendations, and disclose all conflicts of interest upfront.

The regulations require advisors to register with SEBI, pass qualification exams, carry professional indemnity insurance, and submit to regular audits. You can verify any advisor's registration status and check for disciplinary actions through SEBI's official website. These protections exist specifically to prevent the mis-selling that plagued Indian investors when distributors posed as advisors while earning undisclosed kickbacks.

Fee models for personalized investment advice

RIAs typically charge through one of three structures: flat annual fees, percentage of assets under management (AUM), or hourly consultation rates. Flat fees work best when you need ongoing advice but have a smaller portfolio, as you pay a fixed amount regardless of your investment value. AUM-based fees scale with your wealth, usually ranging from 0.5% to 2% per year, which aligns the advisor's earnings with your portfolio growth.

Hourly rates suit investors who want occasional guidance rather than continuous management. You pay for specific sessions to review your portfolio, plan tax strategies, or address major financial decisions. Digital platforms offering personalized investment advice often charge lower AUM fees (0.25% to 1%) because technology reduces their operational costs compared to traditional advisory firms.

Fee-only structures ensure the advisor profits when you profit, not when you buy specific products they're incentivized to push.

Hidden commissions in traditional distribution

Traditional distributors claim to offer "free advice" but earn trail commissions from mutual funds, often 0.5% to 1% annually, plus upfront commissions of 1% to 3% when you invest. These charges get deducted from your fund returns before you see them, making them invisible on statements. A distributor might recommend Fund A paying 1.5% commission over Fund B paying 0.5% commission, even when Fund B delivers better historical returns and lower expense ratios.

Insurance products carry even steeper hidden costs, with first-year commissions reaching 20% to 40% of your premium on ULIP policies. The distributor pockets this amount while your actual investment starts significantly below what you paid. Portfolio management services from banks often bundle relationship charges, account maintenance fees, and transaction costs that multiply your effective expense ratio beyond what the prospectus states.

How to choose the right advisor or platform

Choosing the right advisor or platform for personalized investment advice requires evaluating your specific needs against what each service actually delivers. You need to assess your wealth level, the complexity of your financial situation, your comfort with technology, and how much guidance you want versus self-directed control. A senior executive with multiple income sources needs different advisory depth than someone starting their first job with straightforward salary income. Your decision should balance the sophistication you require with fees you can justify based on your portfolio size and the value the service adds to your returns.

Match services to your wealth stage

Your investable assets determine which advisory models make financial sense. If you have less than ₹10 lakhs to invest, paying 1% AUM fees to a traditional advisor costs you ₹10,000 annually, which might exceed the value they add through better fund selection. Digital platforms and AI-powered services work better at this stage because their lower fee structures (often 0.25% to 0.5%) keep costs reasonable while providing sophisticated recommendations.

Wealthy investors with ₹1 crore or more benefit from comprehensive human advisors who handle estate planning, tax optimization across multiple jurisdictions, and complex portfolio strategies that algorithms can't fully address.

Check regulatory credentials first

Verify that any advisor or platform holds valid SEBI registration as an Investment Advisor before sharing financial information. You can confirm registration numbers on SEBI's official website and check for any past violations or client complaints. Platforms should clearly display their license details on their homepage, not bury them in fine print. Avoid services that claim to offer "free advice" because they're likely earning undisclosed commissions from product manufacturers instead of charging you transparent fees.

Compare total costs beyond stated fees

Calculate the all-in expense by adding advisory fees, fund expense ratios, transaction charges, and any platform fees. A traditional advisor charging 1% AUM might recommend direct mutual funds with 0.5% expense ratios, giving you 1.5% total annual cost. Compare this against a digital platform charging 0.5% that accesses the same funds. Factor in whether the service includes tax planning, portfolio rebalancing, and ongoing monitoring or charges separately for these functions. Higher fees justify themselves only when they produce measurably better after-cost returns or save you significant time managing investments yourself.

Key takeaways

Personalized investment advice transforms your portfolio from generic to goal-aligned by addressing your specific financial circumstances, risk tolerance, and life stage. You need SEBI-registered advisors or platforms that charge transparent fees instead of hidden commissions that drain returns. Human advisors provide deep customization for complex wealth situations, while AI-powered platforms deliver sophisticated recommendations at lower costs for straightforward portfolios. Always verify regulatory credentials, calculate total expenses including fund costs and platform charges, and ensure the service adapts as your life changes. The right choice depends on your investable assets, how much guidance you need, and whether technology or personal interaction matters more to you. Your wealth deserves strategies built around your reality, not someone else's template. Start building your conflict-free portfolio with transparent advice that puts your returns first.