RBI Inflation Calculator: Calculate Future Cost In India

Shlok Sobti

RBI Inflation Calculator: Calculate Future Cost In India

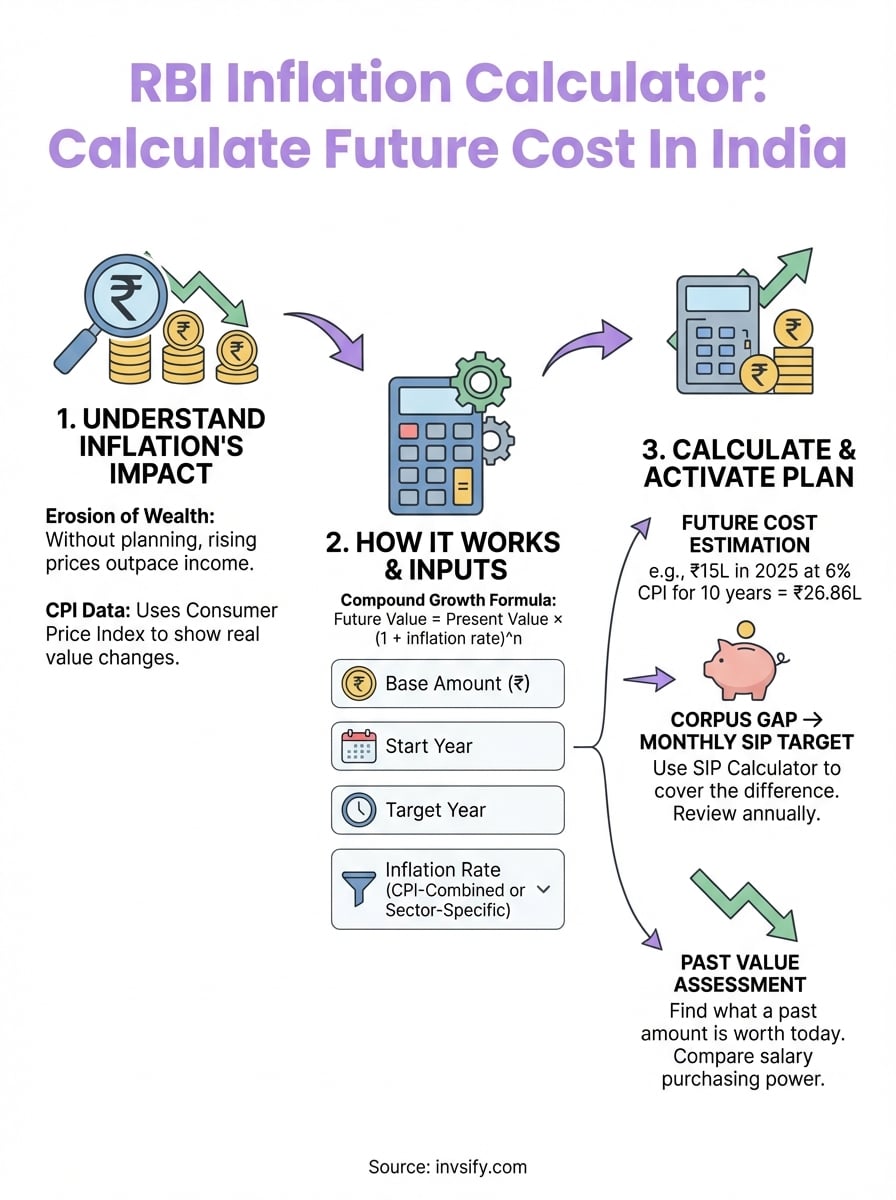

A liter of milk that cost ₹22 in 2010 now costs over ₹60. Your salary may have gone up, but has it kept pace with rising prices? Without running the numbers, most people assume they're doing fine, until retirement or a major expense reveals the gap. An RBI inflation calculator helps you put real numbers to that erosion by using Consumer Price Index (CPI) data published by the Reserve Bank of India.

This tool lets you estimate how much your expenses will grow over 5, 10, or 20 years, and what your money will actually be worth when you need it. Whether you're planning for your child's education, a home purchase, or retirement, understanding inflation's drag on your wealth is the first step toward building a plan that accounts for it.

At Invsify, we help salaried Indians grow and protect their wealth with AI-powered, conflict-free investment advice, and inflation planning is a core part of that. In this guide, we'll walk you through how the RBI inflation calculator works, how to use it step by step, and how to turn those numbers into actionable investment decisions.

What an RBI inflation calculator does

An RBI inflation calculator takes a base amount and a time period, then applies India's actual CPI inflation rates to show you two things: what a past amount is worth today, and what a current amount will cost in the future. Instead of guessing that inflation runs at "about 6%," you work with real data the Reserve Bank of India publishes through its CPI reports, which track price changes across food, fuel, housing, and services.

Using real CPI data instead of a rough estimate can shift your retirement or education corpus target by several lakhs.

How the math works

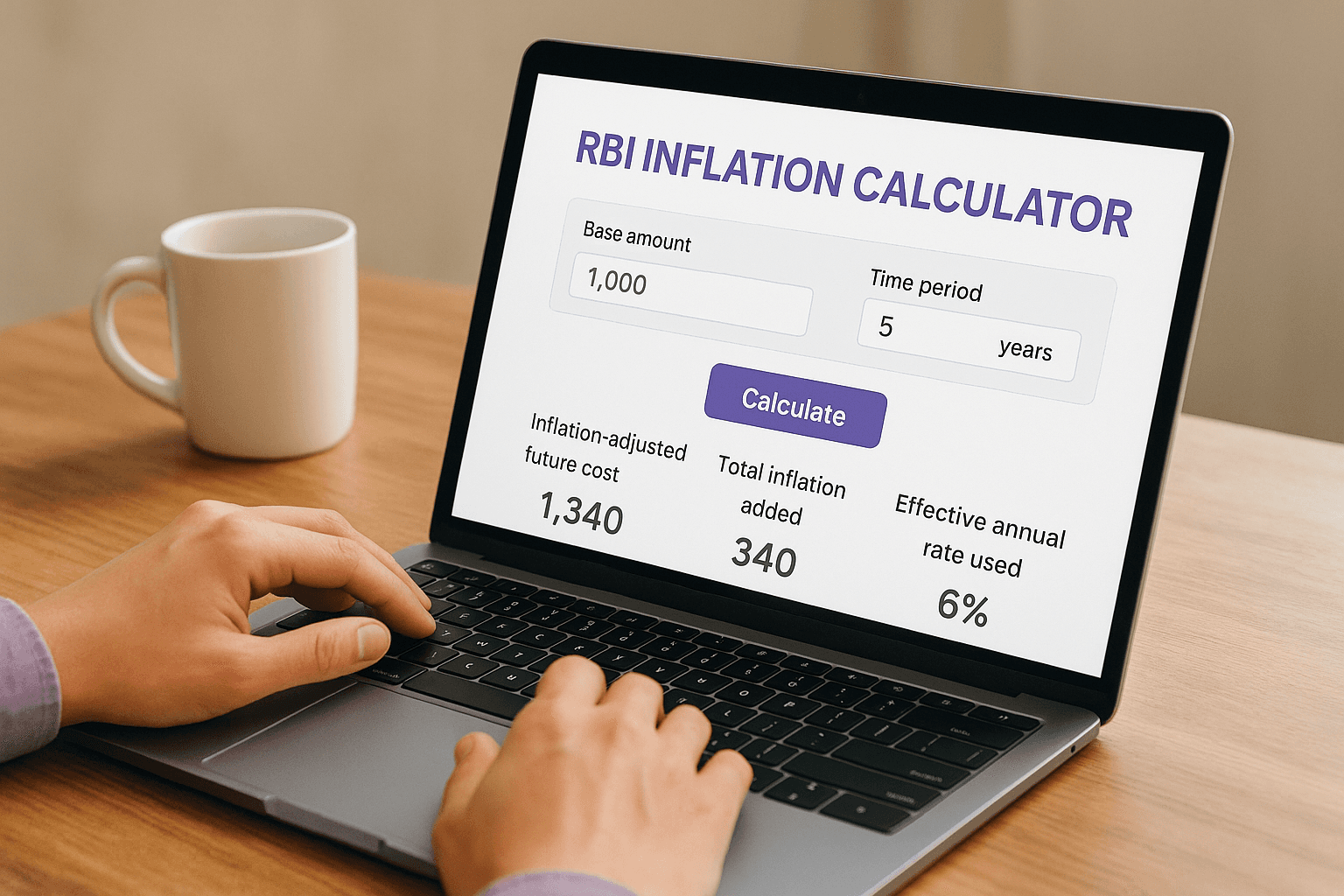

The calculator runs on a straightforward compound growth formula. To find the future cost of an expense, it applies: Future Value = Present Value × (1 + inflation rate)^n, where n is the number of years. To find the real value of a past amount in today's terms, it reverses that same calculation. For example, ₹5,00,000 set aside for a child's college education today will need to grow to roughly ₹8,95,000 in 10 years if inflation averages 6% annually.

What the calculator outputs for you

Most versions of the tool give you three clear outputs you can act on directly:

Output | What it tells you |

|---|---|

Inflation-adjusted future cost | How much you need to save by a target date |

Total inflation added | The rupee amount inflation will add to your expense |

Effective annual rate used | The rate applied so you can verify the calculation |

Some calculators also let you compare scenarios at different rates, like 5%, 6%, and 7%, so you can stress-test your goals. This matters because even a 1% difference in the assumed rate over 20 years can change your target corpus by lakhs.

What you need before you calculate

Before you open any RBI inflation calculator, gather three specific inputs. Having these ready means you get a result you can actually use, rather than a rough estimate you'll second-guess later.

The three inputs you'll enter

Each field in the calculator maps directly to a decision you're making about your financial future. Here's what to collect before you start:

Input | What to use | Example |

|---|---|---|

Base amount (₹) | The current cost of your goal or expense | ₹10,00,000 for a wedding |

Start year | The year your amount is valid from | 2025 |

Target year | The year you'll need the money | 2035 |

You'll also need to choose an inflation rate, which comes from the RBI's published CPI data. If the calculator auto-populates a rate, confirm it matches the latest CPI figure from the RBI's official database. For education or healthcare goals, consider using a rate 1-2% higher than the general CPI, since those categories historically inflate faster than the overall index.

Entering your actual goal amount, not a rounded estimate, is what makes the output worth planning around.

Step 1. Pick the right inflation rate series

The RBI publishes multiple CPI series, and plugging in the wrong one gives you a misleading savings target. The number you enter into the RBI inflation calculator determines your entire corpus estimate, so spend two minutes choosing the right series before you run any numbers.

CPI-Combined vs. sector-specific rates

CPI-Combined is the headline figure the RBI uses for monetary policy and works for general goals like retirement savings and emergency funds. For sector-specific goals, use a higher rate than CPI-Combined since healthcare and education historically outpace general inflation by a measurable margin.

Goal type | Suggested rate |

|---|---|

Retirement / emergency fund | CPI-Combined (latest) |

Child's education | CPI-Combined + 2% |

Medical expenses | CPI-Combined + 1.5% |

A 2% difference in your assumed rate over 15 years can shift your target corpus by 30-40%.

Where to find the current rate

Pull the latest CPI-Combined figure from the RBI's official database or the Ministry of Statistics and Programme Implementation (MoSPI). Look for the year-on-year percentage change for the most recent month, and use a 5-year rolling average if your goal is more than 10 years away, since a single month's reading can be skewed by seasonal food prices.

Step 2. Calculate future cost and past value

With your inflation rate selected, open the RBI inflation calculator and enter your three inputs: base amount, start year, and target year. The tool applies the compound formula automatically and returns your adjusted figures within seconds.

Running both calculations, future cost and past value, gives you a complete picture of what your money can and cannot do.

Calculate how much your goal will cost

Enter your current goal amount as the base value, set 2025 as the start year, then add your target year. For example, a ₹15,00,000 home renovation planned 10 years out at 6% CPI-Combined becomes approximately ₹26,86,000. That gap is what disciplined investing needs to close.

Base amount | Rate | Years | Future cost |

|---|---|---|---|

₹15,00,000 | 6% | 10 | ₹26,86,000 |

₹10,00,000 | 7% | 15 | ₹27,59,000 |

Find what a past amount is worth today

Reverse the calculation by entering a historical amount as the base value and setting the past year as the start. This tells you whether a salary, inheritance, or old savings balance has kept pace with real purchasing power. Use this check for:

Comparing a 2015 salary to its 2025 equivalent

Evaluating whether an old fixed deposit actually grew your wealth

Step 3. Use results for budgeting and goals

Once the RBI inflation calculator gives you an inflation-adjusted figure, your next move is to translate that number into a concrete monthly savings or investment target. Knowing you need ₹26,86,000 in 10 years is only useful if you attach a monthly SIP amount to that goal today.

Your corpus target without a monthly action plan stays a number on a screen.

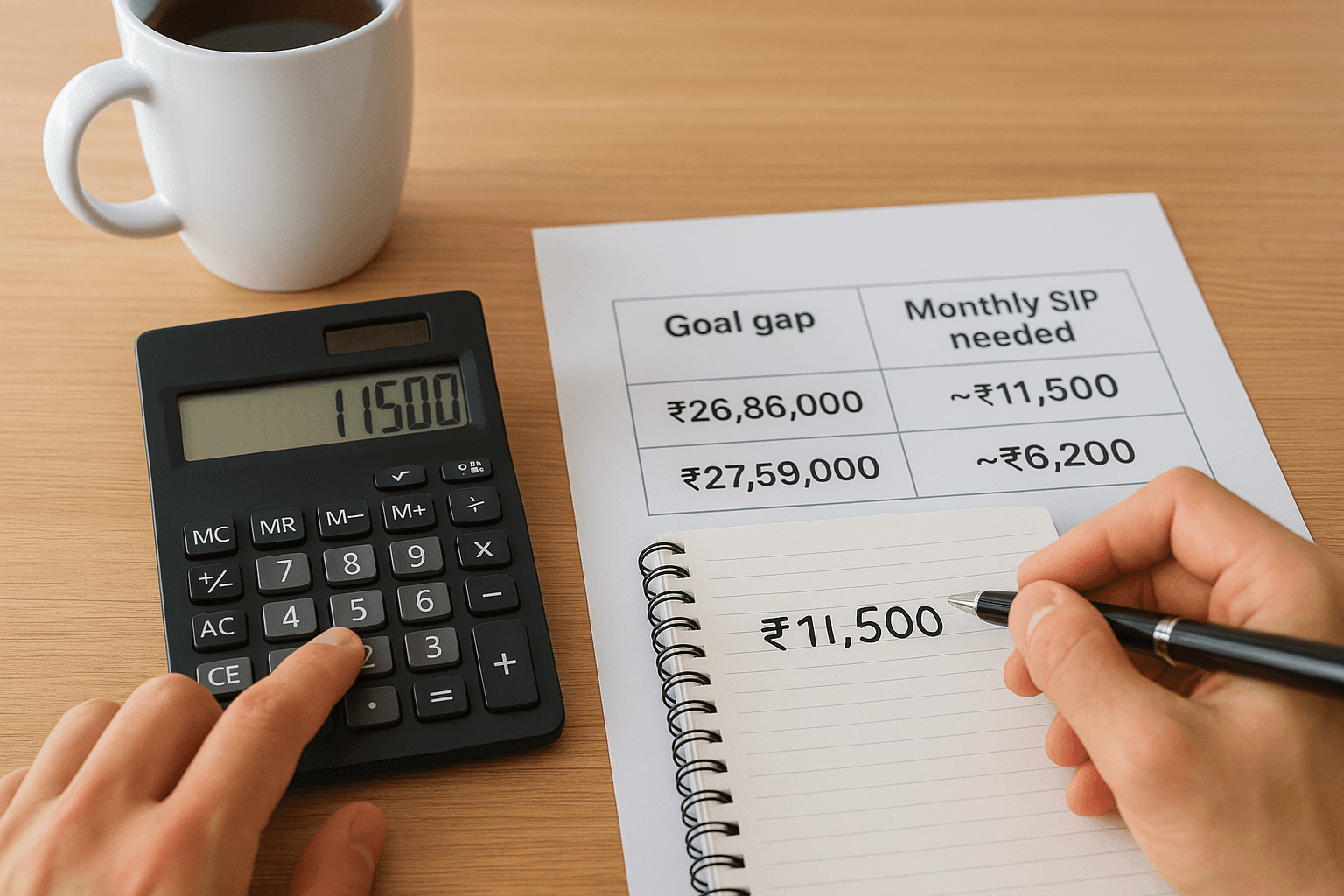

Set a monthly SIP target from your corpus gap

Take your inflation-adjusted future cost and subtract whatever you already have saved toward that goal. The remaining gap is your investment target. Use a SIP calculator to find the monthly amount needed at your expected return rate. For example, to reach a ₹26,86,000 gap in 10 years at 12% CAGR, you need roughly ₹11,500 per month.

Goal gap | Rate of return | Years | Monthly SIP needed |

|---|---|---|---|

₹26,86,000 | 12% | 10 | ~₹11,500 |

₹27,59,000 | 12% | 15 | ~₹6,200 |

Revisit your numbers annually

Inflation rates shift each year, so re-run your calculation every 12 months using the latest CPI data. If the rate rises from 6% to 7%, your corpus target and SIP amount both need an upward revision to stay on track. Set a calendar reminder to update three items each year:

The CPI rate from the latest RBI or MoSPI release

Your current savings balance toward each goal

Your SIP amount based on the revised corpus gap

Next steps

You now have a complete process for using an RBI inflation calculator: choosing the right CPI series, calculating your inflation-adjusted corpus target, and converting that number into a monthly SIP amount. Running these numbers once is a good start, but the real work is integrating them into a plan that adjusts as inflation shifts each year.

Three actions will move you forward immediately. First, pull the latest CPI-Combined figure from the RBI or MoSPI and re-run any goal estimate you made more than 12 months ago. Second, check whether your current SIP amounts still cover the revised corpus gap. Third, look at whether your portfolio is generating returns that consistently beat the inflation rate you used in your calculation.

Getting this right on your own takes time and discipline. Invsify's AI-powered advisors can do the math, track your goals, and flag when your plan needs adjustment. Start your free wealth assessment and build an inflation-proof investment strategy today.