Retirement Asset Allocation By Age: A Simple India Guide

Shlok Sobti

Retirement Asset Allocation By Age: A Simple India Guide

A 25-year-old and a 55-year-old shouldn't have the same portfolio. That sounds obvious, but a surprising number of Indian investors hold nearly identical asset mixes throughout their entire working lives, and then wonder why their retirement corpus falls short. Understanding retirement asset allocation by age is one of the most practical things you can do to make sure your money actually lasts when you stop earning. It's not about chasing returns. It's about matching your portfolio's risk to the years you have left.

The right allocation shifts as you move through life stages, from aggressive equity exposure in your 20s to a more conservative, income-focused mix closer to retirement. But most rules of thumb you'll find online are built around US markets, US tax structures, and US retirement accounts. Indian investors need a framework that accounts for EPF, PPF, NPS, domestic equity, debt funds, and the specific tax rules that apply here.

This guide breaks down exactly how to allocate your retirement assets at every age, with clear benchmarks, sample portfolios, and actionable steps tailored to India. At Invsify, our AI-powered advisory platform helps you build and adjust this kind of age-appropriate portfolio with conflict-free, data-backed recommendations, so your allocation stays aligned with your goals as life changes. Let's walk through what your portfolio should look like, decade by decade.

What retirement asset allocation means in India

Asset allocation is the practice of dividing your retirement savings across different investment categories, each carrying a different level of risk and potential return. You decide how much goes into growth assets like equities, how much goes into stable assets like debt instruments, and how much sits in alternatives like gold. The goal isn't to chase the highest possible returns at all costs. It's to build a portfolio that grows steadily, survives market downturns, and funds 20 to 30 years of retirement expenses without running dry.

Why India's context changes everything

Most international guides on this topic assume you're working with a 401(k), US Treasury bonds, and dollar-denominated assets. Indian investors operate inside a completely different ecosystem. You have government-backed instruments like the Employees' Provident Fund (EPF) and the Public Provident Fund (PPF), which offer guaranteed returns with full principal protection. You also have the National Pension System (NPS) with its own equity-to-debt split. Then there are equity mutual funds, debt mutual funds, fixed deposits, Sovereign Gold Bonds, and real estate, each with different tax treatment, liquidity constraints, and risk profiles.

Post-2023, debt mutual fund gains are taxed as per your income slab regardless of holding period, which directly affects how you use them in a retirement portfolio.

This variety is an advantage, but only if you use each instrument at the right life stage. A 28-year-old who parks all savings in fixed deposits because they feel safe is quietly losing ground to inflation. A 58-year-old who keeps 90% in equity mutual funds because "markets recover" is taking on risks their timeline can no longer absorb. Retirement asset allocation by age is the discipline that prevents both these mistakes.

The three building blocks of an Indian retirement portfolio

Before you set any target percentages, you need to understand the three core categories you're choosing between. Each plays a different role depending on where you are in your working life:

Category | Examples | Role in Portfolio |

|---|---|---|

Growth assets | Equity mutual funds, direct stocks, NPS equity tier | Build the corpus over the long term |

Stable/income assets | PPF, EPF, NPS debt tier, debt mutual funds, FDs | Preserve capital and reduce volatility |

Inflation hedges | Sovereign Gold Bonds, REITs, international funds | Protect purchasing power over decades |

Growth assets do the heavy lifting in your 20s, 30s, and early 40s, compounding your money over long periods. Stable assets take over as the anchor in your 50s and into retirement, protecting what you've built. Inflation hedges play a supporting role throughout but become especially relevant as retirement nears, since your real purchasing power matters far more once your salary stops.

How your time horizon drives every decision

Your time horizon, meaning the number of years before you retire and start drawing down your corpus, is the single biggest variable in any allocation decision. With 30 years ahead of you, a 30% market correction is a temporary setback your portfolio can recover from. With 3 years to retirement, that same correction can permanently reduce the corpus you rely on.

Longer time horizons justify higher equity exposure because you have the runway to ride out volatility and capture long-term growth. Shorter horizons demand more stability because the math simply doesn't give you time to recover. This is why your allocation must shift as you age. It's not a one-time setup. It's an ongoing calibration tied directly to how many working years you have left.

Step 1. Pick your target mix by age and timeline

Your first task is to set a target allocation based on your current age and the number of years you have until retirement. Think of this as your portfolio's anchor point. You'll build around it, adjust for your personal risk tolerance, and shift it over time. But before any of that, you need a concrete starting number. The benchmarks below are designed specifically for Indian investors and account for the tax treatment and instrument choices available here.

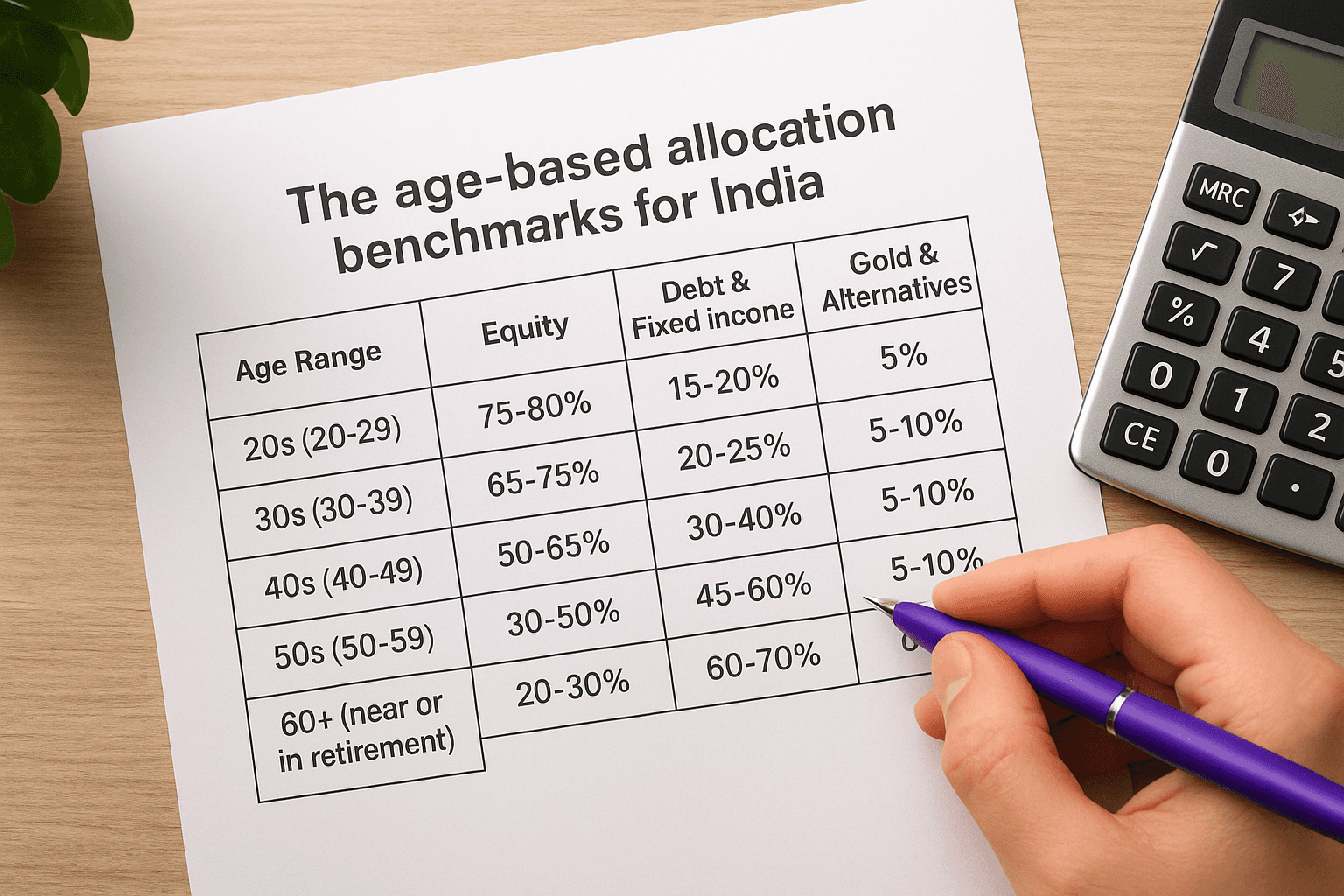

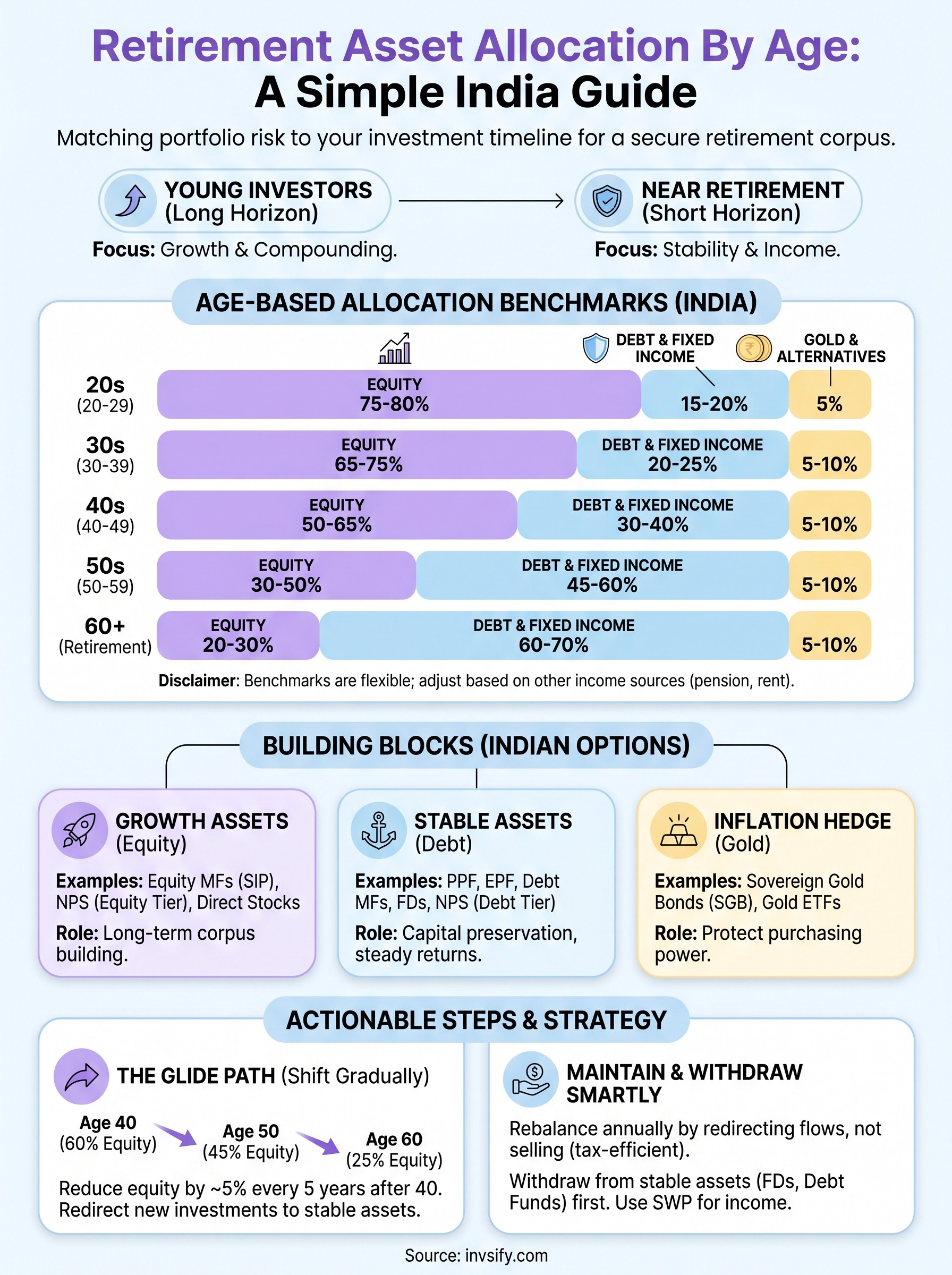

The age-based allocation benchmarks for India

These ranges give you a practical starting point for retirement asset allocation by age. The equity percentage includes equity mutual funds, direct stocks, and the equity tier of NPS. The debt percentage covers EPF, PPF, NPS debt tier, debt mutual funds, and fixed deposits. Gold and alternatives round out the remainder.

Keep in mind that these are benchmarks, not rigid rules. If you have a pension, a defined benefit from your employer, or rental income lined up for retirement, you can afford to hold slightly more equity for longer.

Age Range | Equity | Debt & Fixed Income | Gold & Alternatives |

|---|---|---|---|

20s (20-29) | 75-80% | 15-20% | 5% |

30s (30-39) | 65-75% | 20-25% | 5-10% |

40s (40-49) | 50-65% | 30-40% | 5-10% |

50s (50-59) | 30-50% | 45-60% | 5-10% |

60+ (near or in retirement) | 20-30% | 60-70% | 5-10% |

How to read and use these benchmarks

Start by locating your current age range in the table, then check where your existing portfolio actually sits. If you're 38 and holding 85% in equity, you're running hotter than the benchmark. That's not automatically wrong, but it means a sharp correction would hit your corpus harder than it needs to. If you're 42 and holding only 30% in equity, your corpus will likely underperform inflation over the next 15 years when it needs to be growing the most.

Once you know the gap between your current mix and the benchmark, set a realistic target allocation to move toward. You don't need to rebalance everything at once. For example, if you're 44 with 70% in equity and want to reach 55%, you can stop routing new SIP contributions into equity funds for a few months and redirect them to debt instruments instead. This gradual shift reduces unnecessary tax events and keeps transaction costs low while steadily moving you toward the right mix.

Step 2. Build it with Indian investment options

Knowing your target allocation percentages is only half the job. The other half is mapping those percentages to actual investment options available in India, each with its own tax rules, liquidity features, and expected return range. Once you understand which instruments fit which category, building your portfolio around retirement asset allocation by age becomes a straightforward exercise in filling the right buckets.

Growth assets: where to put your equity exposure

For the equity portion of your portfolio, the most practical starting point for most Indian investors is equity mutual funds through the SIP route. Large-cap funds provide stability with reasonable growth, while flexi-cap or mid-cap funds push returns higher over 10-plus-year horizons. If your employer offers NPS, the Tier I equity option (Scheme E) is worth using because contributions up to ₹50,000 per year qualify for an additional tax deduction under Section 80CCD(1B), over and above the Section 80C limit.

Avoid counting your EPF exposure as your "equity allocation." EPF is a debt instrument with a guaranteed rate, and it belongs in the stable asset bucket, not the growth one.

Direct stock investing can supplement mutual funds if you have time to research individual companies, but it should not form the core of your retirement equity strategy. SIPs into diversified equity mutual funds give you rupee-cost averaging and professional fund management, which matters more as your corpus grows and the stakes rise.

Stable assets: matching the right debt instruments to your goals

PPF is the anchor for most Indian investors on the debt side. The 15-year lock-in forces long-term discipline, the returns are government-backed, and the entire corpus, including interest, remains exempt from tax. EPF contributions through your salary also belong here, compounding at the rate set by EPFO each year. For amounts beyond what PPF and EPF can absorb, debt mutual funds and short-duration bond funds give you liquidity that fixed deposits don't, even though gains are now taxed at your income slab rate.

Here is a quick reference to match instruments to allocation categories:

Instrument | Category | Key Benefit |

|---|---|---|

Equity mutual funds / NPS Scheme E | Growth | Long-term compounding |

PPF | Stable | Tax-free, government-backed returns |

EPF | Stable | Employer contribution, steady rate |

Debt mutual funds | Stable | Better liquidity than fixed deposits |

Sovereign Gold Bonds | Inflation hedge | Interest income plus capital gains benefit |

Use this table as your instrument checklist when you review your portfolio each year. If a category is underfunded relative to your target mix, route your next investments there before adding more to buckets that are already full.

Step 3. Shift your mix as retirement gets closer

Your allocation doesn't stay fixed. The benchmarks in Step 1 show you where to be at each decade, but moving from one point to the next requires deliberate, phased action rather than a sudden overhaul. This gradual transition is called a glide path, and building one into your retirement plan is what protects your corpus from a poorly timed market correction just before you need it most.

The glide path: how to reduce equity gradually

A glide path is simply a pre-planned schedule for shifting money from growth assets to stable assets as you age. You don't need complex software to build one. The most practical approach for Indian investors is to reduce your equity allocation by roughly 5 percentage points every five years once you cross 40. That pace keeps you invested long enough to capture equity growth during your peak earning years, while consistently lowering your exposure to volatility as the retirement date approaches.

If you receive a large windfall, a bonus, or liquidate a property near retirement, route that lump sum directly into stable assets rather than equity, regardless of where markets stand at that moment.

Here is a simple glide path template you can adapt to your own situation:

Age | Equity Target | Action to Take |

|---|---|---|

40 | 60% | Redirect new SIPs partially toward debt funds |

45 | 55% | Stop increasing equity SIP amounts; add to PPF |

50 | 45% | Begin shifting equity gains into the NPS debt tier |

55 | 35% | Move maturing fixed deposits into short-duration bond funds |

60 | 25% | Consolidate corpus; shift bulk to stable income instruments |

What to do in the final five years before retirement

The five years leading up to retirement are the highest-stakes period in your entire investment journey. A sharp equity correction in this window can cut your corpus significantly, and you won't have salary income flowing in to compensate. Your priority shifts from growing the portfolio to protecting it, while keeping enough growth to stay ahead of inflation.

During this phase, review your retirement asset allocation by age every six months rather than annually. Move equity gains into stable assets systematically, and avoid the temptation to stay invested simply because markets look strong. Set a firm floor: no more than 30% in equity by the time you retire, regardless of market conditions.

Step 4. Maintain, rebalance, and withdraw smartly

Building your retirement asset allocation by age is a starting point, not a one-time task. Without regular maintenance, a strong equity bull run can quietly push your allocation 10 to 15 percentage points above your target, leaving you overexposed at exactly the wrong time. Review your portfolio at least once a year, compare it to the benchmarks from Step 1, and act when any category drifts more than 5 percentage points from its target.

Rebalancing without triggering unnecessary tax

Rebalancing in India requires you to account for capital gains tax before selling anything. Short-term capital gains on equity funds held under 12 months are taxed at 20%, while long-term gains above ₹1.25 lakh per year are taxed at 12.5%. Selling and buying purely to rebalance can erode your corpus if you do it carelessly.

The most tax-efficient way to rebalance is to redirect new investments rather than selling existing holdings. Pause SIPs into overweight categories and increase contributions to underweight ones first.

A practical rebalancing checklist to run each year:

Compare your current allocation against your age-appropriate target from Step 1

If equity is overweight, reduce or pause equity SIPs and direct new money to debt instruments

If debt is overweight, increase equity SIP amounts before considering any sale

Only sell assets when drift exceeds 10 percentage points and you qualify for LTCG treatment on those holdings

Withdrawing smartly to make your corpus last

How you draw down your retirement corpus matters as much as how you built it. A common mistake is withdrawing from equity funds first, which removes assets that still carry long-term compounding potential. Instead, withdraw from stable instruments like FDs and debt funds first, and let your equity holdings continue working in the background.

For most Indian retirees, a Systematic Withdrawal Plan (SWP) from a balanced or debt-oriented hybrid fund works well. It delivers predictable monthly income, spreads tax liability across years, and reduces the risk of liquidating equity during a downturn. Combining this approach with phased PPF and EPF withdrawals across the early retirement years gives your remaining corpus the runway it needs to stay ahead of inflation well into your 70s.

Your next move

You now have a complete framework for retirement asset allocation by age, built around Indian instruments, Indian tax rules, and the specific life stages that matter to Indian investors. The benchmarks, glide path, and withdrawal strategy in this guide give you everything you need to act today, not someday.

Start with one concrete step: check your current portfolio against the age-appropriate benchmark from Step 1. If your equity percentage is more than 10 points away from the target range for your age, that gap is costing you either growth or unnecessary risk right now.

Building and maintaining the right allocation is easier when you have data-backed guidance updating as your situation changes. Invsify's AI-powered platform tracks your portfolio, flags allocation drift, and gives you conflict-free recommendations tailored to your goals. Get started with smarter retirement planning and let your allocation work for you from this point forward.