Retirement Planning Expert in India: Roles, Fees, Hiring

Shlok Sobti

Retirement Planning Expert in India: Roles, Fees, Hiring

A retirement planning expert is a professional who helps you build and manage a financial strategy for life after work. They assess your current savings, project future needs, recommend investment vehicles and ensure your money lasts through retirement. Some focus on pension funds and annuities while others take a broader approach covering estate planning, tax optimization and healthcare costs. In India these experts can be SEBI registered investment advisors, PFRDA certified retirement advisors or chartered accountants with specialized training.

This article breaks down everything you need to know about hiring a retirement planning expert. You'll learn what services they offer, how they charge for their work and what credentials actually matter. We'll cover the difference between fee-only advisors and commission-based agents, explain when it makes sense to hire professional help and show you what questions to ask before signing up. You'll also see how modern AI tools can work alongside human advisors to give you better results at lower costs. Whether you're just starting to think about retirement or need help optimizing an existing plan, this guide will help you make an informed choice.

Why a retirement planning expert matters

Your retirement corpus will determine your quality of life for 20 to 30 years after you stop working. Most people underestimate how much they need, invest in the wrong products or fail to account for inflation properly. A retirement planning expert brings technical knowledge and objectivity that's hard to replicate on your own, especially when you're juggling a career and family responsibilities. They help you avoid costly errors that can take years to correct.

The cost of retirement mistakes compounds over time

Small planning errors in your 30s and 40s turn into massive shortfalls by retirement. If you pick the wrong asset allocation or withdraw from your corpus too early, you lose decades of potential compounding. For example, withdrawing ₹5 lakh from your retirement fund at age 35 doesn't just cost you ₹5 lakh. At an 8% annual return, that money would have grown to over ₹34 lakh by age 60. An expert helps you avoid these irreversible mistakes by setting up guardrails and showing you the long-term impact of every financial decision.

"The earlier you get your retirement plan right, the less you need to save each month and the more secure your future becomes."

Indian regulations and schemes add layers of complexity

India offers multiple retirement vehicles like NPS, EPF, PPF, Atal Pension Yojana and various annuity products, each with different tax treatments, lock-in periods and withdrawal rules. The tax code alone has multiple sections (80C, 80CCD, EEE vs EET) that affect how much you actually keep after taxes. PFRDA regulations for NPS, SEBI rules for mutual funds and insurance regulations for pension plans all intersect in ways that aren't obvious. Your advisor stays current with these rules and knows which combinations work best for your income level, age and risk tolerance. They also understand how changes in policy (like Budget announcements) might affect your existing strategy, so you don't have to track every regulatory update yourself.

How to work with a retirement expert and AI tools

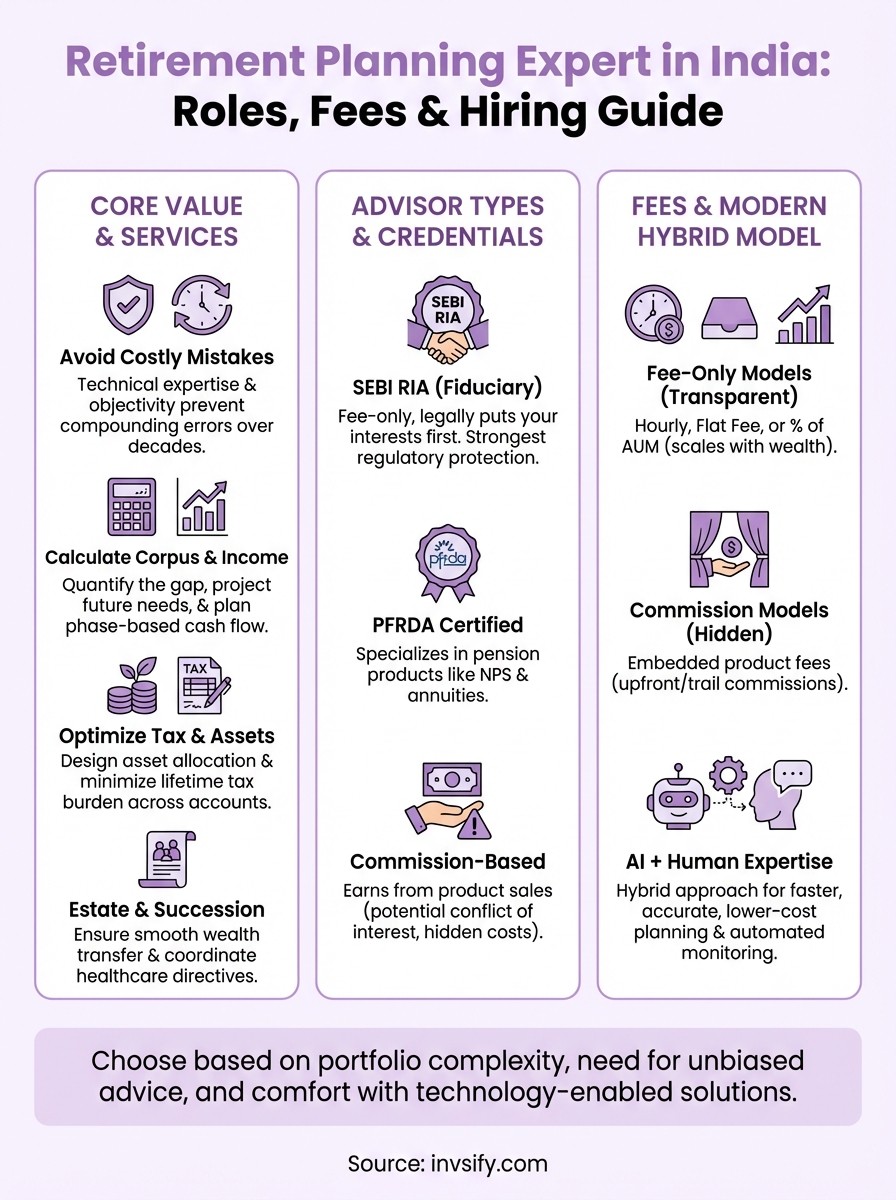

Modern retirement planning blends human expertise with AI-powered tools to give you faster, more accurate and cheaper advice. You get the strategic thinking and empathy of a professional advisor combined with the data-crunching power of algorithms that can analyze thousands of scenarios in seconds. This hybrid model is replacing the old approach where you'd meet an advisor once or twice a year, wait weeks for a plan and pay high fees for basic calculations. Most SEBI registered advisors now use some form of technology platform to track your portfolio, model different retirement scenarios and send you alerts when your plan needs adjustment.

The hybrid approach combines human judgment with AI speed

AI tools handle the repetitive analytical work like portfolio tracking, tax-loss harvesting and rebalancing calculations while your human advisor focuses on the parts that actually need expertise. The AI can instantly show you how a 2% increase in your SIP affects your retirement age or what happens if inflation runs higher than expected. Your advisor interprets those numbers, asks about your changing life goals and helps you make decisions when the math alone doesn't give a clear answer. For example, the AI might flag that you're overexposed to equity at your age, but your advisor will discuss whether that's appropriate given your risk tolerance, backup income sources and health situation.

"Technology automates the grunt work so your advisor spends more time understanding your unique situation and less time building spreadsheets."

Your typical workflow from onboarding to execution

You'll start with an online assessment that captures your current assets, income, expenses and retirement goals. The AI processes this data and generates an initial plan showing your projected corpus, monthly pension and gap analysis. Your retirement planning expert then reviews the output, adjusts assumptions based on your conversation and presents a customized strategy in a video or in-person meeting. After you approve the plan, the platform automates most of the execution through direct integrations with mutual funds, NPS and other investment accounts. You'll get regular AI-generated reports tracking your progress against goals, and your advisor will reach out quarterly or when the AI detects something that needs human attention. This workflow cuts planning time from weeks to days and reduces ongoing fees since the AI handles monitoring and basic adjustments automatically.

Key roles and services a retirement expert offers

Your retirement planning expert handles far more than picking mutual funds or calculating how much to save each month. They build a complete financial architecture that covers income projections, tax optimization, healthcare planning, estate distribution and contingency strategies. The scope depends on whether you hire a specialized retirement advisor or a comprehensive wealth manager, but most professionals offer a core set of services that address the major risks and decisions you'll face between now and your 80s. Understanding these roles helps you evaluate what you're actually paying for and whether the advisor's strengths match your specific needs.

They calculate your retirement corpus and income needs

Your advisor starts by quantifying the gap between what you have and what you'll need. They factor in your current age, planned retirement age, life expectancy, monthly expenses and expected inflation to calculate the total corpus required. This isn't just basic multiplication. They account for phase-based spending patterns where your expenses might be higher in the first decade of retirement (travel, hobbies) and then drop before rising again for healthcare in your 70s and 80s. They also model different scenarios like early retirement, part-time work or supporting elderly parents to show you how each choice affects your required savings rate. Most advisors provide a detailed year-by-year cash flow projection so you can visualize exactly when you'll draw from which accounts and how long your money will last under different assumptions.

They design your asset allocation strategy

Asset allocation determines most of your portfolio's performance and risk. Your retirement planning expert builds an allocation mix across equity, debt, gold and real estate based on your risk capacity, time horizon and income stability. Someone with 25 years until retirement can handle higher equity exposure for growth, while someone 5 years out needs more debt instruments for capital preservation. They don't just set allocation once and forget it. They establish a glide path that automatically shifts your portfolio from aggressive to conservative as you approach retirement, reducing the chance that a market crash right before you stop working wipes out years of gains. They also help you decide between mutual funds, NPS, ETFs, direct stocks and real assets based on factors like liquidity needs, tax treatment and management complexity.

"The right asset allocation can add 1 to 2 percentage points of annual returns without taking more risk, which translates to years of additional financial security."

They optimize your tax efficiency across accounts

Tax planning makes a measurable difference in your final corpus. Your advisor maps out which investments go into which account types to minimize your lifetime tax burden. They might recommend maxing out NPS Tier I for the Section 80CCD(1B) deduction, using PPF for tax-free returns under EEE and placing equity mutual funds in taxable accounts where long-term gains over ₹1.25 lakh get taxed at just 12.5%. They also time your withdrawals strategically. Pulling from tax-free sources first (PPF maturity, ELSS after 3 years) and deferring taxable income (NPS annuity) to years when you're in a lower bracket can save lakhs in taxes over a 20-year retirement. Your advisor stays current with annual Budget changes and alerts you when new opportunities or risks emerge.

They coordinate estate and succession planning

Retirement planning doesn't end when you die. Your advisor ensures your wealth transfers smoothly to your intended beneficiaries by reviewing nominee designations across all accounts, suggesting appropriate insurance coverage and coordinating with a lawyer for will drafting if needed. They make sure your spouse has clear instructions and access to all accounts in case something happens to you. They also discuss healthcare directives and powers of attorney so someone can make financial decisions on your behalf if you become incapacitated. While they're not estate lawyers, good advisors flag potential issues like inadequate liquidity to pay estate taxes or complicated ownership structures that could lead to family disputes after you're gone.

Regulation, licenses and credentials in India

India's regulatory framework for financial advisors is fragmented across multiple agencies, each governing different aspects of retirement planning. SEBI regulates investment advisors who recommend securities and mutual funds, PFRDA certifies advisors who specialize in pension products like NPS and IRDAI oversees insurance agents selling annuity plans. This means your retirement planning expert might hold one credential, multiple certifications or none at all depending on what services they offer and how they charge for advice. Understanding these credentials helps you identify who's accountable for the advice you receive and what legal protections you have if something goes wrong.

SEBI RIA registration offers the strongest regulatory protection

A SEBI Registered Investment Advisor (RIA) operates under the strictest fiduciary standards in India. They're legally required to put your interests first, disclose all conflicts of interest and charge transparent fees without earning commissions from product sales. To get registered, advisors must meet minimum qualification requirements (specific finance certifications or degrees), pass NISM exams, maintain professional indemnity insurance and submit to regular audits. Your advisor's RIA registration number appears on all official documents and you can verify their status on the SEBI website. This credential matters most when you need comprehensive retirement planning that covers multiple asset classes because RIAs can recommend mutual funds, stocks, bonds and other securities without bias toward high-commission products.

"SEBI RIA registration means your advisor earns money from your fees, not from selling you products, which eliminates the biggest conflict of interest in financial advice."

PFRDA retirement advisor certification focuses on pension products

PFRDA certified retirement advisors specialize in National Pension System (NPS), Atal Pension Yojana and other pension schemes regulated by the Pension Fund Regulatory and Development Authority. They help you choose between pension fund managers, decide on asset allocation within NPS and understand withdrawal rules at retirement. The certification requires passing the NISM Retirement Adviser Certification Examination which covers pension products, retirement mathematics and regulatory frameworks. These advisors can charge fees for their guidance or earn commissions from pension products depending on their business model. You'll typically work with a PFRDA advisor if NPS forms a major part of your retirement strategy or if you need specialized knowledge about government pension schemes.

Other relevant credentials and their actual value

Chartered accountants, certified financial planners (CFP) and chartered wealth managers (CWM) often provide retirement planning services based on their broader financial expertise. CFP certification from FPSB India requires extensive coursework covering all areas of financial planning including retirement, but it doesn't grant regulatory permissions to sell specific products. CAs bring tax optimization expertise that's valuable for retirement planning since tax efficiency directly affects your final corpus. Many retirement planning experts hold multiple credentials combining SEBI RIA registration with CFP or CA qualifications to offer comprehensive services. The credential matters less than whether your advisor operates under a fiduciary standard, charges transparent fees and has verifiable experience building retirement plans for clients similar to you in age, income level and complexity.

Types of retirement advisors and how they differ

Retirement advisors in India fall into distinct categories based on how they earn money, what credentials they hold and whether they prioritize your interests or product sales. The type you choose affects the quality of advice you receive, how much you pay and whether recommendations serve your goals or generate commissions. Fee-only advisors operate as fiduciaries with transparent pricing, while commission-based agents earn from product sales which creates conflicts of interest. Bank advisors and digital platforms offer their own trade-offs between convenience, cost and personalization. Understanding these differences helps you pick the right match for your retirement planning needs.

Fee-only advisors work exclusively for you

Fee-only retirement planning experts charge you directly through hourly rates, flat fees or percentage-based annual charges on assets under management. They don't accept commissions from mutual funds, insurance companies or any product provider, which eliminates the incentive to recommend high-commission investments over better alternatives. Most operate as SEBI Registered Investment Advisors and must legally act in your best interest. You pay for their time and expertise regardless of which products you buy, so their recommendations focus purely on what works for your situation. This model costs more upfront but typically saves you money over time because you avoid expensive insurance plans, high-expense-ratio funds and unsuitable products that commission-based advisors push to maximize their earnings.

"When your advisor's income doesn't depend on what you buy, you get unbiased recommendations that actually optimize your retirement outcomes."

Commission-based agents prioritize product sales

Traditional insurance agents and mutual fund distributors earn commissions every time you invest through them. They might call themselves advisors or planners but their income comes from product manufacturers, not from you. This creates obvious conflicts where they recommend ULIPs with 5% upfront commissions instead of low-cost index funds, or push insurance-heavy retirement plans because those pay higher commissions than pure investment products. Many operate under AMFI registration for mutual funds or IRDAI licensing for insurance but face no fiduciary obligation to put your interests first. Some provide genuinely helpful guidance despite these incentives, but you need to verify their recommendations independently and understand that their business model rewards sales volume over optimal client outcomes.

Bank relationship managers offer convenience with limits

Your bank's wealth management team provides retirement planning as part of broader relationship services, usually free if you maintain high balances or take other products. They have access to your complete banking relationship which simplifies data gathering and execution. The major limitation is that they primarily recommend proprietary products from their own asset management company even when better external options exist. Their advice tilts toward bank deposits, bank mutual funds and partnerships that generate revenue for the institution. You get convenience and integration with your existing accounts, but you sacrifice independence and often pay higher fees embedded in the bank's in-house products compared to what you'd access through an independent advisor.

AI-first platforms blend automation with human oversight

Digital platforms use artificial intelligence to automate portfolio construction, rebalancing and tax optimization while keeping human advisors available for complex questions. They charge significantly less than traditional advisors because algorithms handle most routine work. You answer questions online about your retirement goals, risk tolerance and current assets, then receive an automated plan with recommended investments. Human experts review your situation periodically and intervene when the AI flags something that needs judgment. This model works well if your retirement planning needs are straightforward and you're comfortable with technology, but it may not provide enough personalized attention if you have complicated assets, business ownership or unique family situations.

Fee models, commissions and typical costs

Your retirement planning expert charges for their services in several distinct ways, and the model you choose directly affects how much you pay over time and whether their incentives align with your goals. Fee-only advisors charge transparently for their work while commission-based advisors earn from product sales, often without disclosing the full cost to you. Understanding these structures helps you compare options fairly and avoid paying more than necessary for the advice you receive. Most advisors clearly state their fee model upfront, but you need to ask specific questions about total costs including embedded product fees that don't appear on their invoice.

Hourly and flat fee structures give you transparent pricing

Hourly rates for retirement planning experts in India typically range from ₹2,000 to ₹10,000 depending on the advisor's credentials, experience and location. You pay for the time they spend analyzing your situation, building your plan and answering your questions. This model works well if you need a one-time comprehensive plan and can execute it yourself without ongoing support. Expect to pay ₹15,000 to ₹50,000 for a complete retirement plan that includes corpus calculations, asset allocation recommendations and tax optimization strategies. Some advisors offer flat fee packages that bundle initial planning with limited follow-up reviews for a fixed annual charge between ₹25,000 and ₹1,00,000. These packages typically include quarterly portfolio reviews and adjustments as your circumstances change.

Assets under management fees scale with your wealth

Many retirement planning experts charge an annual percentage of the assets they manage on your behalf, usually between 0.5% and 2% depending on your portfolio size. A ₹1 crore portfolio at 1% AUM costs you ₹1 lakh per year, and this fee continues every year you work with the advisor. The percentage typically decreases as your assets grow since managing ₹5 crores doesn't take five times the work of managing ₹1 crore. This model aligns the advisor's income with your portfolio growth which motivates them to optimize performance. The downside is that you pay even in years when your portfolio doesn't grow, and the fees compound over decades reducing your final corpus. Calculate the total cost over your full retirement timeline before committing since a 1% annual fee can consume 20-25% of your potential gains over 30 years.

"The difference between a 1% and 1.5% annual advisory fee might seem small but costs you several lakhs in lost compounding over a typical retirement planning horizon."

Commission-based models hide the true cost

Commission-driven advisors don't charge you directly but earn from insurance companies and mutual fund houses when you buy their products. Insurance plans pay upfront commissions of 2% to 5% of your premium plus trail commissions for years afterward. Regular mutual fund plans pay trail commissions of 0.5% to 1% annually compared to direct plans with zero commissions. These costs come from your investment corpus rather than your bank account, making them less visible but equally real. A ₹25 lakh ULIP with 5% upfront commission costs you ₹1.25 lakh immediately, reducing your invested capital from day one. Over 20 years, the difference between regular and direct mutual funds on a ₹50 lakh portfolio exceeds ₹10 lakh due to the trail commission drag on returns.

Typical price ranges you'll encounter in India

Entry-level digital advisory platforms charge ₹5,000 to ₹20,000 annually for automated retirement planning with limited human support. Mid-tier independent advisors with SEBI RIA registration typically charge 0.75% to 1.5% on AUM or ₹30,000 to ₹75,000 for comprehensive planning with ongoing reviews. Premium wealth managers serving high net worth clients charge 0.5% to 1% on larger portfolios, often with minimum portfolio requirements of ₹1 crore or more. Specialized retirement planning experts might charge project fees of ₹50,000 to ₹2,00,000 for complex situations involving multiple income sources, international assets or business succession planning. You'll find the lowest costs with robo-advisors and the highest with boutique firms offering white-glove service, but the right choice depends on your portfolio complexity and how much hand-holding you need during execution.

How to choose the right expert for your situation

Choosing the right retirement planning expert requires matching their strengths to your specific circumstances rather than picking the most credentialed or cheapest option. Your portfolio complexity, life stage and comfort with technology determine which type of advisor serves you best. Someone with straightforward salaried income and standard retirement goals needs different expertise than a business owner with real estate holdings and international assets. Start by defining what you actually need help with, then evaluate advisors based on how well they deliver those specific services rather than general reputation or marketing claims.

Match credentials to your specific needs

Your situation determines which credentials actually matter. If you're building a corpus primarily through mutual funds and NPS, you need a SEBI Registered Investment Advisor who can recommend securities without product bias. Someone focused on pension products and annuities benefits more from a PFRDA certified advisor who specializes in retirement income planning. You should verify credentials directly through regulatory websites rather than trusting certificates displayed in offices. Ask specifically about their fiduciary obligation and whether they earn commissions from any products they recommend. The right credential mix depends on your asset types, but always prioritize advisors who operate under fiduciary standards requiring them to put your interests first.

Evaluate their fee structure against your portfolio size

Your portfolio size directly affects which fee model makes financial sense. Hourly or flat fee advisors work well when you have ₹25 lakhs to ₹1 crore and need a comprehensive plan you can mostly execute yourself. Assets under management fees become cost-effective above ₹1 crore since the percentage-based charge provides ongoing portfolio management and rebalancing. Calculate the total cost over 10 to 15 years under each model to see which minimizes your lifetime advisory expenses. Someone with ₹50 lakhs might pay ₹50,000 for a flat fee plan or ₹50,000 annually at 1% AUM, but the AUM model compounds that cost every year while the flat fee plan limits ongoing expenses to optional reviews.

"The cheapest fee structure today isn't always the best value over your full retirement timeline, especially when you factor in the cost of mediocre advice."

Assess their technology and service delivery model

Modern retirement planning requires technology integration for portfolio tracking, scenario modeling and automated rebalancing. You should ask what platforms they use and whether you get direct access to view your accounts in real time. Advisors using advanced tools can show you instantly how different decisions affect your retirement age or monthly income, while those relying on spreadsheets take weeks to model simple changes. Evaluate whether they offer video consultations, mobile apps and automated reporting or require in-person meetings for every interaction. Your comfort with technology matters too since AI-first platforms demand more self-service while traditional advisors provide more hand-holding. The right balance depends on how much personal attention you want versus how much you're willing to pay for it.

Verify their experience with clients like you

Generic retirement planning expertise doesn't translate to understanding your specific situation. You need an advisor who has successfully built retirement plans for people in your income bracket, age range and family structure. Ask for anonymized case studies or client scenarios similar to yours and how they addressed challenges you're likely to face. Someone who primarily serves high net worth clients might not understand the constraints and opportunities available to middle-income savers. Request references from current clients willing to share their experience, focusing on how the advisor handled market downturns, major life changes or disagreements about strategy. The best retirement planning expert for you is someone who has repeatedly solved problems similar to yours rather than someone with impressive credentials but no relevant experience.

When to hire a retirement expert and what to ask

You should consider hiring a retirement planning expert when your financial situation becomes too complex to manage alone or when you're approaching critical decision points that will affect decades of retirement security. The right timing depends on your age, asset complexity and confidence in making financial decisions, but certain life events clearly signal that professional guidance will pay for itself many times over. Waiting too long costs you potential returns and planning flexibility, while hiring too early might mean paying for advice you don't yet need.

Life events that signal you need professional help

Major life transitions create retirement planning pressure points where professional advice prevents costly mistakes. You should hire an expert when you receive a large windfall like an inheritance, property sale or business exit that needs to be allocated properly for retirement. Job changes involving retirement account rollovers require expertise since moving EPF to NPS or choosing between pension options has tax implications you can't easily reverse. Getting married, divorced or having children changes your retirement timeline and corpus requirements significantly enough that your old plan likely no longer works. Reaching age 40 without a formal retirement plan means you've lost valuable compounding years and need expert help to catch up through optimized contributions and asset allocation.

Health diagnoses or caring for aging parents also shift your retirement mathematics by adding healthcare costs and potentially reducing your working years. You need professional guidance to model these changes and adjust your strategy before small problems become unsolvable gaps in your corpus.

"The best time to hire a retirement expert is before a financial mistake, not after you're trying to fix one."

Questions to ask before you commit

Your first conversation with any retirement planning expert should answer specific questions that reveal how they work and whether they're right for you. Start by confirming their regulatory credentials and asking whether they operate as a fiduciary legally required to put your interests first. Understand exactly how they charge by asking for total costs including any embedded product fees, not just their direct invoice. You need clarity on what services come with their fee such as how often they review your plan, whether you get direct access to them or just junior staff and what happens if you need help outside scheduled meetings.

Ask about their specific experience building retirement plans for people in your income range and life stage since strategies that work for high net worth clients often don't translate to middle-income situations. Request their typical planning process from initial assessment through execution and ongoing monitoring so you know what to expect. Verify what technology platforms they use for portfolio tracking and scenario modeling since modern tools significantly improve the planning experience. Finally, ask how they handle disagreements since you need an advisor who will explain their reasoning and adjust recommendations rather than insist they know best regardless of your concerns.

Key takeaways

A qualified retirement planning expert brings technical knowledge, regulatory understanding and objectivity that most people can't replicate on their own. The right professional depends on your portfolio size, complexity and whether you need comprehensive wealth management or focused retirement guidance. Fee-only SEBI RIAs offer the strongest conflict-free advice since they earn from your fees rather than product commissions, while commission-based advisors create incentives that may not align with your goals. You should verify credentials directly through regulatory websites, understand total costs over your full planning timeline and evaluate whether the advisor has solved problems similar to yours.

Modern retirement planning works best when AI tools handle analytical work while human experts provide strategic judgment and personalized guidance. This hybrid approach cuts costs and improves accuracy compared to traditional models. If you want transparent, technology-enabled retirement advice that puts your interests first, explore how Invsify combines AI-powered insights with SEBI registered expertise to help you build and optimize your retirement corpus.