Retirement Planning For Beginners: A Step-By-Step Guide

Shlok Sobti

Retirement Planning For Beginners: A Step-By-Step Guide

Most people don't ignore retirement because they don't care about it. They ignore it because they don't know where to start. How much do you actually need? Where should you invest? What if you get it wrong? These questions pile up, and before you know it, another year passes without a plan. If that sounds familiar, you're not alone, and retirement planning for beginners doesn't have to feel this overwhelming.

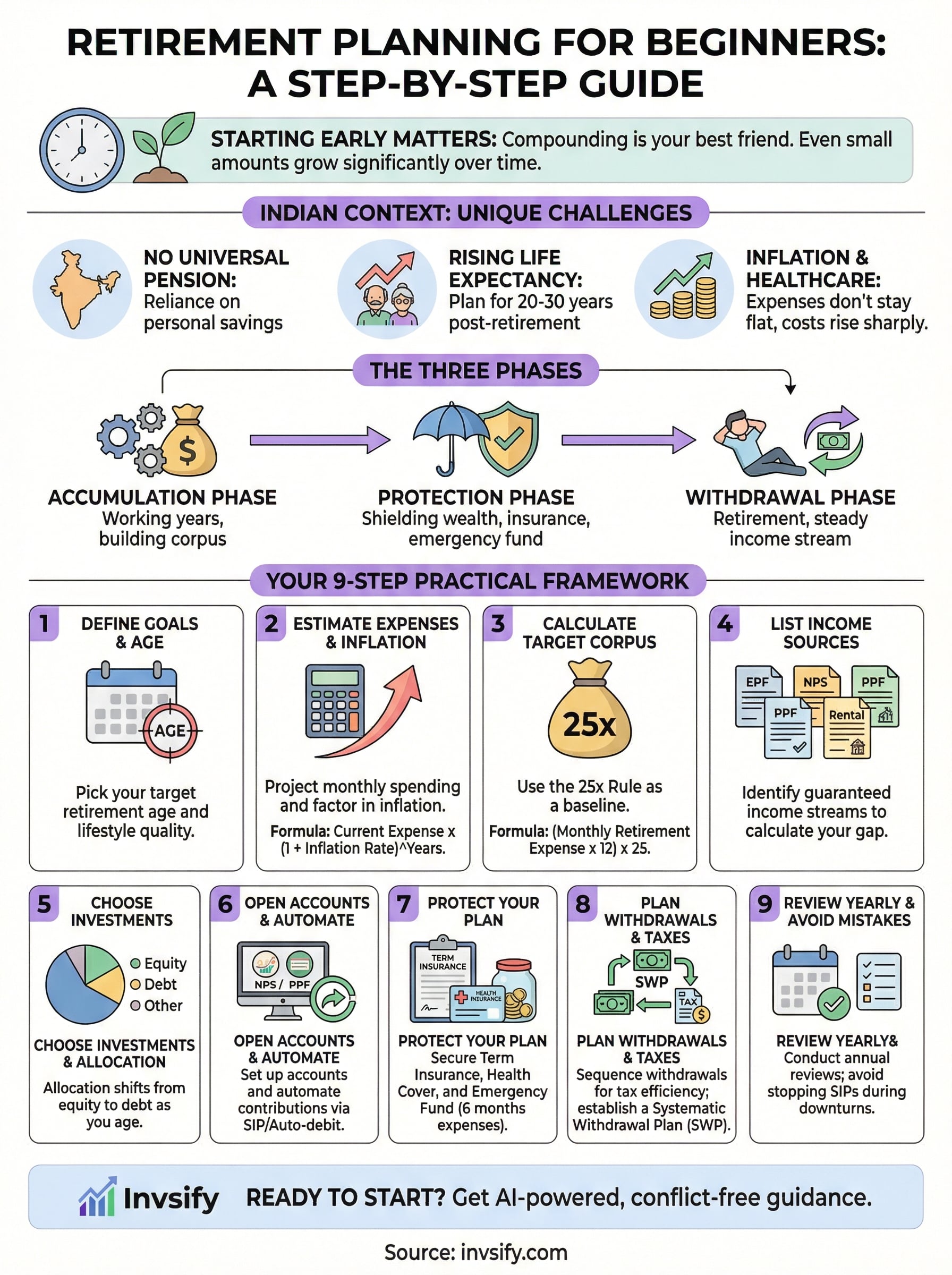

The truth is, starting early, even with small amounts, matters far more than starting perfectly. A 25-year-old investing ₹5,000 per month can build significantly more wealth than a 35-year-old investing ₹15,000 per month, purely because of how compounding works over time. The math is straightforward, but only if you actually begin.

This guide walks you through the entire process, step by step, from setting clear retirement goals and estimating how much you'll need, to choosing the right investment vehicles and avoiding common mistakes. No jargon-heavy theory, no vague advice. Just a practical framework you can act on today. And if you want AI-powered, conflict-free guidance tailored to your specific financial situation, that's exactly what we built Invsify to do, a SEBI Registered Investment Advisor that combines smart technology with transparent advice to help you grow, protect, and optimize your wealth at every stage of life.

Let's get into it.

What retirement planning means for Indian beginners

Retirement planning in India isn't just about saving money; it's about replacing your salary with a system that funds your life for potentially 25 to 30 years after you stop working. Unlike Western countries, India has no universal pension safety net for private sector employees. The government's EPFO covers salaried workers in the organized sector, but that alone rarely builds enough to live comfortably. So if you work in the private sector, the responsibility of funding your retirement sits almost entirely on your shoulders.

Why India's context is different

The Indian financial landscape creates unique challenges that most retirement planning for beginners guides written for other markets simply don't address. First, life expectancy is rising fast: someone retiring at 60 today can reasonably expect to live until 80 or beyond, which means your money needs to last two full decades. Second, India's inflation rate historically runs between 5% and 7% annually, which means your expenses don't stay flat. A lifestyle that costs ₹50,000 per month today could cost over ₹1,35,000 per month in 20 years.

The longer your money has to work, the more compounding rewards you. Starting at 25 instead of 35 can mean a difference of several crores by retirement age, using the same monthly investment amount.

There's also the cultural dimension. Many Indian families still rely on children to support aging parents, but this is shifting rapidly as nuclear families become the norm and children face their own financial pressures. Building your own retirement corpus is no longer just smart financial planning; it's a necessity. Depending on a spouse's income, family support, or an expected inheritance without a clear personal plan leaves you financially vulnerable.

Here's a quick snapshot of what makes retirement planning in India distinct from other markets:

No mandatory private sector pension beyond EPFO, and EPF balances alone are rarely sufficient

Inflation erodes purchasing power significantly over long retirement horizons

Healthcare costs rise sharply with age and are mostly out-of-pocket in India

Tax rules change frequently, making regular plan reviews essential

Joint family support is declining, increasing the need for individual financial self-sufficiency

The three phases every beginner must understand

Retirement planning isn't a single action; it's a process that runs across three distinct phases. The accumulation phase is when you're working and building your corpus through regular investments in instruments like PPF, NPS, mutual funds, and equity. This is where compounding does the heavy lifting, and the earlier you start, the greater the advantage. The protection phase overlaps with accumulation and involves shielding what you've built through adequate health insurance, term life cover, and an emergency fund so that a single financial crisis doesn't wipe out years of progress.

The third phase, the withdrawal phase, begins when you retire and need to convert your corpus into a steady income stream. This is where most people underestimate the complexity. Drawing too much too fast depletes the corpus before your life ends. Drawing too little might mean living below the standard you planned for. Getting this phase right requires a clear withdrawal strategy, tax-efficient planning, and regular portfolio reviews, all of which this guide covers in the steps ahead.

Step 1. Define your retirement goals and age

Everything in your retirement plan flows from two decisions: when you want to retire and what kind of life you want to fund. Without these anchors, you're saving blindly. Most people assume 60 is the default retirement age, but that number comes from government service rules, not personal financial logic. Your target could be 45, 55, or 65, and each choice changes how much you need to save and how aggressively you need to invest.

Pick your target retirement age

Your retirement age determines how many years you have to accumulate wealth and how many years your corpus needs to sustain you. If you retire at 55 and live until 85, your corpus must last 30 years. If you retire at 60, it needs to cover 25. That five-year difference shifts your required corpus by several lakhs to crores, depending on your lifestyle costs.

The younger your retirement target, the larger your required corpus, since you have fewer earning years and more retirement years to fund.

Use this table as a starting reference based on your current age and target retirement age:

Current Age | Target Retirement Age | Saving Years Left | Estimated Retirement Duration |

|---|---|---|---|

25 | 55 | 30 | 30+ years |

25 | 60 | 35 | 25+ years |

35 | 55 | 20 | 30+ years |

35 | 60 | 25 | 25+ years |

40 | 60 | 20 | 25+ years |

Clarify what your retirement actually looks like

The second part of retirement planning for beginners that most guides skip is defining the quality of your retirement, not just the age. "Retire comfortably" means nothing without specifics. Do you plan to travel internationally? Will you relocate to a smaller city to cut costs? Do you expect significant healthcare expenses? Will you support dependent parents or children through college?

Answer these questions in writing before you open a calculator:

Where will you live? Same city, smaller town, or somewhere else entirely?

What will your monthly lifestyle cost? Be specific about rent, food, leisure, and travel.

Do you have dependents? Factor in support for aging parents or children still in school.

When will your children's education expenses end? This affects your savings capacity significantly.

Will you work part-time after retiring? Even modest income reduces the corpus you need.

These answers give your plan a real shape. A number written down is a goal; a vague wish is just hope.

Step 2. Estimate expenses and account for inflation

Once you fix your retirement age, the next task is figuring out how much money you'll actually need to spend each month after you stop working. Most beginners either guess a number or copy someone else's figure, and both approaches usually lead to a corpus that falls short. Your expenses in retirement are unique to your lifestyle, your city, your health, and your family situation, so you need to build this estimate from the ground up.

Map your current monthly spending

Start with what you spend right now. Break your expenses into two groups: essential costs (housing, food, utilities, medicine, transport) and discretionary costs (travel, dining out, entertainment, hobbies). This separation matters because some discretionary spending might increase after retirement, while certain work-related costs like commuting and professional clothing disappear entirely.

Use this template to build your estimate:

Category | Current Monthly (₹) | Expected in Retirement (₹) |

|---|---|---|

Housing (rent/maintenance) | ||

Groceries and food | ||

Utilities and internet | ||

Healthcare and medicines | ||

Transport | ||

Travel and leisure | ||

Family support | ||

Miscellaneous | ||

Total |

Fill both columns honestly. Many retirement planning for beginners guides suggest using 70% to 80% of your current income as a retirement expense estimate, but this rule frequently underestimates healthcare costs, which rise sharply with age and are largely out-of-pocket in India.

Apply the inflation multiplier

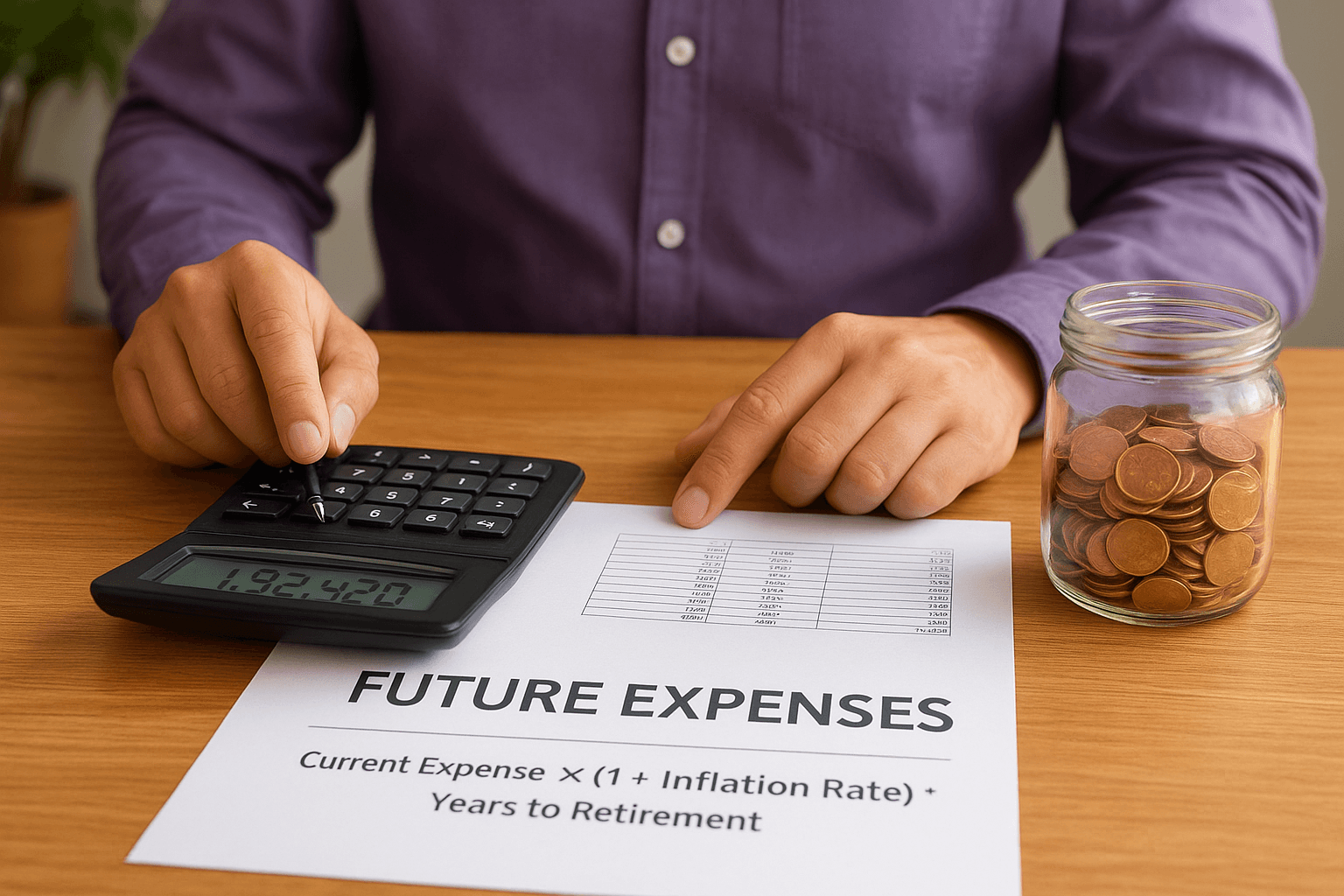

Once you have your estimated monthly retirement expense in today's rupees, you need to project that number forward for inflation. At India's historical average of around 6% annually, a ₹60,000 monthly lifestyle today will cost roughly ₹1,93,000 per month in 20 years. Ignoring this step means you will build a corpus that looks sufficient today but buys far less when you actually need it.

Skipping the inflation adjustment is the single most common mistake beginners make when estimating their retirement number.

Use this formula to calculate your future monthly expense:

Future Expense = Current Expense × (1 + Inflation Rate) ^ Years to Retirement

For example, if your current monthly expense is ₹60,000, inflation is 6%, and you retire in 20 years:

₹60,000 × (1.06)^20 = ₹60,000 × 3.207 = ₹1,92,420 per month

That projected figure becomes the foundation for calculating your total retirement corpus in the next step.

Step 3. Calculate your target retirement corpus

With your inflation-adjusted monthly expense from Step 2, you now have the most important input for this calculation. The goal here is to arrive at a single number: the total corpus you need to have accumulated on the day you retire so that it funds your life without running out. This is the step where retirement planning for beginners gets concrete, and where a rough guess turns into an actual savings target.

Use the 25x rule as your baseline

The 25x rule is a widely used starting point. It says your target corpus should equal 25 times your annual retirement expense. This is based on a 4% annual withdrawal rate, which research suggests a well-invested portfolio can sustain indefinitely without depleting the principal. In India's context, where inflation runs higher than in developed markets, treat this as a conservative minimum, not a ceiling.

Use the 25x number as your floor. If you plan a longer retirement or expect rising healthcare costs, build in a buffer of 10% to 20% on top.

Here is the formula:

Target Corpus = (Monthly Retirement Expense × 12) × 25

Using the example from Step 2, where the inflation-adjusted monthly expense was ₹1,92,420:

₹1,92,420 × 12 = ₹23,09,040 per year

₹23,09,040 × 25 = ₹5.77 crore target corpus

Break down what you actually need to save

Once you have the corpus target, you need to reverse-engineer how much you must invest each month to reach it. This depends on three variables: your current savings, your expected rate of return, and the number of years to retirement. Use the Future Value of Annuity formula, or input your numbers into any retirement calculator to get your required monthly SIP amount.

Variable | Example Value |

|---|---|

Target corpus | ₹5.77 crore |

Years to retirement | 25 |

Expected annual return | 10% (equity-heavy portfolio) |

Existing savings/investments | ₹2,00,000 |

Required monthly investment | ~₹28,500 |

The required monthly amount drops significantly the earlier you start, which is why delaying even two or three years makes a material difference. If your current income doesn't cover the required monthly investment, that tells you something important: you may need to push back your retirement age, reduce your planned lifestyle costs, or increase your income before your savings rate can catch up to your target.

Step 4. List income sources you can count on

Your corpus target from Step 3 assumes you'll fund retirement entirely from your own savings, but most salaried Indians have at least a few guaranteed or semi-guaranteed income streams that will run alongside their personal investments. Mapping these sources before you finalize your savings plan prevents you from over-saving on one hand or dangerously underestimating your needs on the other. Completing this step is a foundational part of retirement planning for beginners that most people skip until it's too late.

Income sources most salaried Indians can rely on

Most private sector employees have an Employee Provident Fund (EPF) account that accumulates throughout their working years. Both you and your employer contribute 12% of your basic salary each month, and this balance earns a government-declared interest rate annually. Beyond EPF, if you've contributed to the National Pension System (NPS), that corpus converts partially into a monthly annuity at retirement. PPF, maintained consistently, adds a tax-free lump sum at maturity.

Income Source | Type | How to Access |

|---|---|---|

EPF | Lump sum or partial annuity | Withdraw or transfer at retirement |

NPS | 60% lump sum + 40% annuity | Mandatory annuity purchase at age 60 |

PPF | Lump sum | Withdraw after 15-year maturity |

Rental income | Monthly cash flow | Property held before retirement |

Senior Citizen Savings Scheme (SCSS) | Quarterly interest | Open at age 60 with post-retirement funds |

Calculate your income gap

Once you list every predictable income source and estimate the monthly cash flow each one will generate, subtract that total from your inflation-adjusted monthly expense from Step 2. The difference is your income gap, and that gap is what your personal investment corpus must actually close. If your gap is smaller than expected, your required corpus from Step 3 drops accordingly, which directly lowers your required monthly savings amount.

Your income gap, not your total retirement expense, is the number your personal savings strategy needs to close.

Use this template to calculate your position clearly:

Source | Estimated Monthly Income (₹) |

|---|---|

EPF withdrawals or annuity | |

NPS annuity | |

PPF withdrawals (monthly equivalent) | |

Rental income | |

Part-time work | |

Total Projected Income | |

Inflation-Adjusted Monthly Expense | |

Monthly Gap (Expense minus Income) |

Fill every row with realistic, verified numbers rather than rough guesses. Log into your EPFO passbook and NPS account statement to check your current balance and projected payout before you estimate future income from those sources.

Step 5. Choose investments and set asset allocation

Knowing your target corpus and income gap tells you how much to invest. This step tells you where to invest it. For retirement planning for beginners, choosing the right instruments isn't about picking the hottest fund or timing the market. It's about building a mix of assets that grows your money aggressively when you have time and protects it when you don't. Getting this mix right from the start prevents the two most common portfolio mistakes: taking too much risk close to retirement or being too conservative too early.

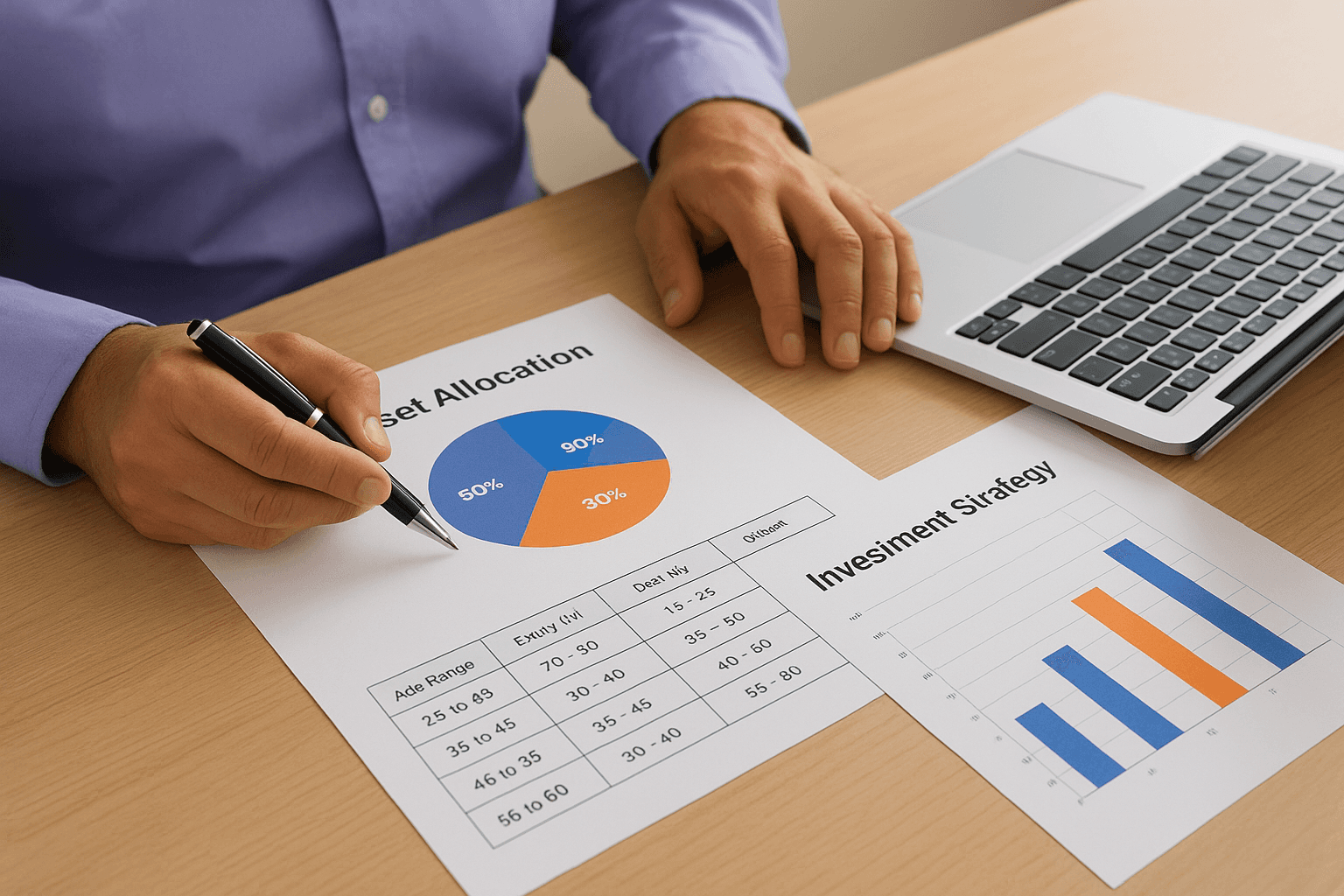

Match your asset allocation to your timeline

Your asset allocation (the percentage split between equity, debt, and other instruments) should reflect two things: how many years you have before retirement and how much volatility you can tolerate without abandoning your plan. When you're 25 with 30 years ahead, a heavy equity allocation makes sense because you have enough time to recover from market downturns. When you're 55 with five years remaining, preserving capital matters more than chasing returns, and your debt allocation should rise accordingly.

As a general rule, subtract your current age from 100 to get your approximate equity allocation percentage, then adjust based on your personal risk tolerance.

Use this table as a starting framework and shift gradually, not all at once:

Age Range | Equity (%) | Debt (%) | Other (Gold/REITs) (%) |

|---|---|---|---|

25 to 35 | 70 to 80 | 15 to 25 | 5 |

36 to 45 | 60 to 70 | 25 to 35 | 5 |

46 to 55 | 45 to 55 | 40 to 50 | 5 to 10 |

56 to 60 | 30 to 40 | 55 to 65 | 5 |

The core investment options for Indian salaried investors

India's investment landscape offers several reliable instruments for building a retirement corpus. Equity mutual funds (particularly index funds tracking the Nifty 50 or Nifty Next 50) give you broad market exposure without the risk of picking individual stocks, and they're accessible with SIPs starting at ₹500 per month. The National Pension System (NPS) combines equity and debt exposure with an additional tax deduction of up to ₹50,000 under Section 80CCD(1B), making it one of the most tax-efficient instruments available to salaried individuals.

For your debt allocation, PPF remains the strongest anchor: it offers guaranteed returns, full tax-free status at maturity, and sovereign backing. Within five to seven years of retirement, begin gradually shifting a portion of equity gains into debt mutual funds or fixed-income instruments to reduce the risk that a market downturn just before you retire wipes out years of accumulated gains.

Step 6. Open accounts and automate contributions

Choosing your instruments in Step 5 only works if the money actually moves. The biggest gap between people who build retirement wealth and those who don't isn't knowledge; it's execution. Opening the right accounts and automating your contributions removes the monthly decision entirely. You stop relying on willpower and let the system do the work.

Open the right accounts first

Before you automate anything, you need the correct accounts in place for each instrument in your allocation. For most salaried Indians starting retirement planning for beginners, this means three primary accounts: an NPS account (Tier I), a PPF account, and a mutual fund account linked to a verified KYC profile. Each serves a different purpose in your portfolio, and all three can be opened digitally.

Once your accounts are open and linked to your bank, automation takes less than 15 minutes to configure and runs without any further action from you.

Use this table to confirm what you need to open and where:

Account | Where to Open | Minimum Contribution | Tax Benefit |

|---|---|---|---|

NPS Tier I | eNPS portal or your bank | ₹500 per month | Up to ₹2 lakh under 80C + 80CCD(1B) |

PPF | Bank or post office (online) | ₹500 per year | Fully exempt under EEE status |

Mutual Fund (SIP) | Direct AMC or MF utility | ₹500 per month | ELSS qualifies under 80C |

Set up automation so you never miss a contribution

Once your accounts are active, set up a Standing Instruction (SI) or an auto-debit mandate from your salary account for each contribution. Time each debit to trigger within two to three days of your salary credit date so the money moves before you have a chance to spend it. This is the single most reliable habit in personal finance, not because it's clever, but because it removes human error from the equation.

Follow this setup sequence to get automation running:

Log into your bank's net banking portal and navigate to the "Standing Instructions" or "Auto Debit" section.

Add your PPF account number as a payee and schedule a monthly transfer on your chosen date.

Register a SIP mandate through your mutual fund account using UPI AutoPay or NACH, selecting the amount and fund.

Set your NPS contribution via eNPS using a recurring payment instruction tied to your bank account.

Confirm all mandates are active by checking your bank's scheduled payments section after the first cycle completes.

Your monthly investment now runs on its own. Review the amounts annually as your salary grows and adjust each instruction upward to keep pace with your corpus target.

Step 7. Protect your plan with insurance and buffers

Building a corpus is only half the job. A single medical emergency, an unexpected job loss, or a premature death in the family can wipe out years of accumulated savings if you haven't built a financial safety layer around your plan. This is the part of retirement planning for beginners that most guides treat as optional. It isn't. Protection isn't separate from your retirement plan; it's what keeps your plan intact when life doesn't go as expected.

Cover the two risks that can destroy a corpus

The first risk is premature death, which leaves your dependents with no income and no corpus to fall back on. A pure term insurance policy covers this at a low premium. If you earn ₹12 lakh per year and have 25 years until retirement, you need a cover of at least 10 to 15 times your annual income, which puts your target sum assured between ₹1.2 crore and ₹1.8 crore. Buy term cover only, not investment-linked plans, since those mix insurance with savings in a way that underdelivers on both.

The second risk, a major health event, is often more financially damaging than death because it depletes savings while you're still alive and still need income.

A comprehensive health insurance policy with a minimum cover of ₹10 lakh (preferably ₹25 lakh for families in metro cities) is non-negotiable for any retirement plan. Check that your policy covers hospitalization, critical illness, and daycare procedures. Don't rely on your employer's group cover since that policy disappears the moment you switch jobs or retire.

Build a financial buffer before you invest more

Your emergency fund is the buffer between your life and your investment portfolio. Without it, any financial shock forces you to redeem long-term investments at the wrong time, often at a loss. Build a fund that covers six months of your total household expenses and keep it entirely in a high-yield savings account or a liquid mutual fund so it's accessible within 24 hours.

Follow this sequence to build your buffer systematically:

Calculate six months of total expenses using the monthly figure you built in Step 2.

Open a separate savings account or liquid fund account and label it clearly as your emergency fund.

Set a monthly transfer to this account until the target balance is reached, then stop and redirect that amount to your retirement SIP.

Replenish immediately after any withdrawal so the buffer stays intact.

Once your term cover, health insurance, and emergency fund are in place, your investment portfolio works as intended, growing without interruption.

Step 8. Plan withdrawals, taxes, and cash flow

Most people spend decades building a corpus without ever thinking about how they'll actually pull money out of it. The withdrawal phase is where poor planning does the most damage: drawing too aggressively depletes your corpus before you die, while drawing too conservatively means living below the standard you worked toward. Both outcomes are avoidable if you build a clear withdrawal and cash flow system before you retire.

The order in which you withdraw from different accounts can save you several lakhs in taxes over a 20-year retirement.

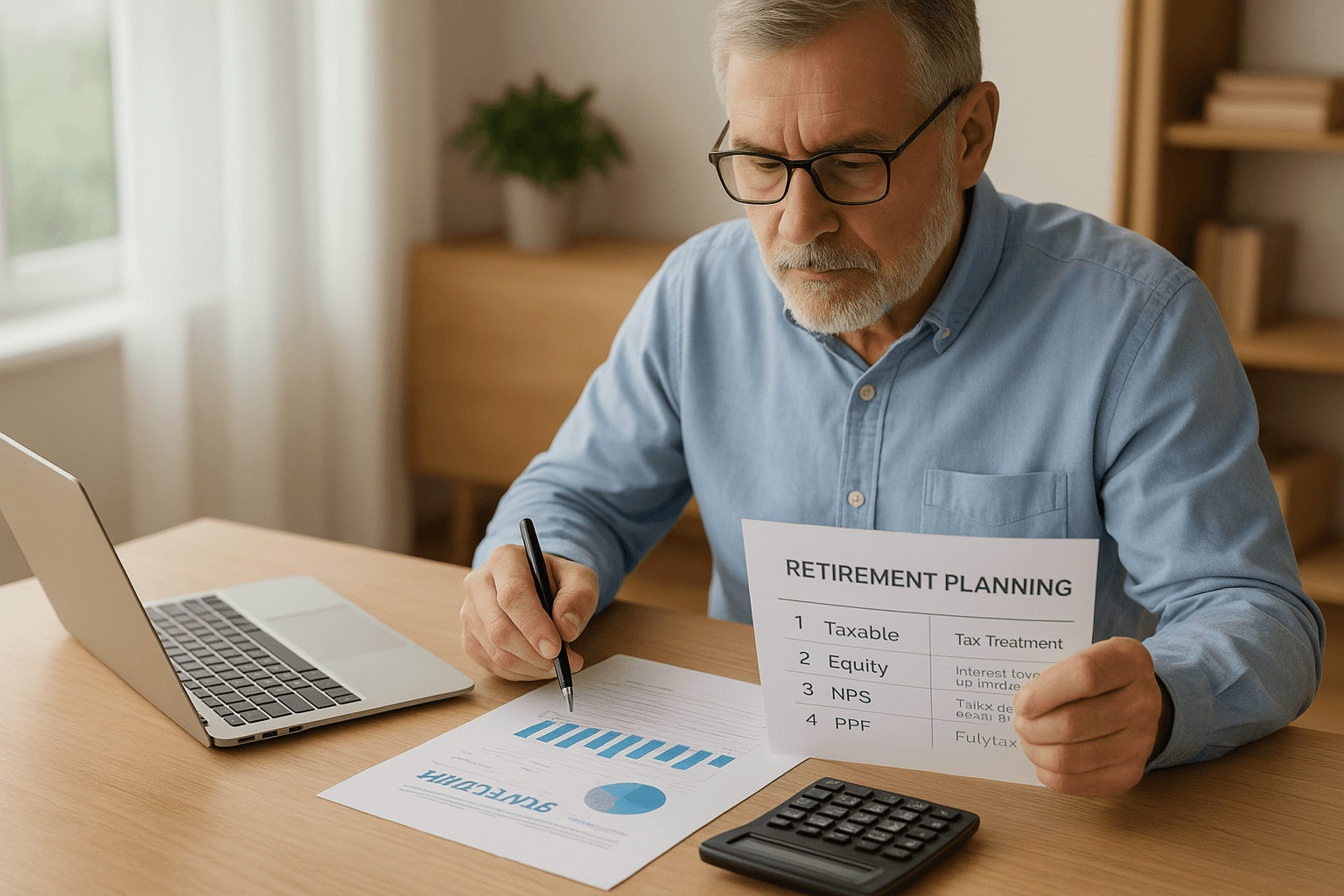

Sequence your withdrawals to minimize taxes

Different investment accounts carry different tax treatments, and the sequence in which you draw from them directly affects how much of your corpus you actually keep. In retirement planning for beginners, this tax-sequencing step is almost always overlooked until the first large withdrawal triggers an unexpected tax bill. The general rule is to withdraw from taxable accounts first, then tax-deferred accounts like NPS, and finally tax-exempt accounts like PPF, preserving the tax-free compounding for as long as possible.

Use this withdrawal order as your starting framework:

Priority | Source | Tax Treatment |

|---|---|---|

1 | Taxable savings and FDs | Interest taxed as income |

2 | Equity mutual funds (LTCG) | 12.5% on gains above ₹1.25 lakh |

3 | NPS annuity | Taxed as per your income slab |

4 | PPF withdrawals | Fully tax-exempt |

NPS annuity income is taxable in the year you receive it, so plan your total annual withdrawal carefully to stay within a lower income tax slab wherever possible.

Build a monthly cash flow system

Once you fix your withdrawal sequence, you need a concrete monthly cash flow structure that converts your corpus into predictable income. Set up a Systematic Withdrawal Plan (SWP) from your equity and debt mutual funds to credit a fixed amount to your bank account each month on a set date. Pair this with any annuity or interest income from SCSS or debt funds to cover your baseline monthly expenses without touching your emergency buffer.

Follow these steps to build your cash flow system:

Calculate your monthly income gap using the figure you mapped in Step 4.

Set your SWP amount to cover that gap precisely, not more.

Schedule SWP payouts two to three days before your regular bills are due.

Review your withdrawal rate annually to ensure it stays at or below 4% of your total remaining corpus.

Step 9. Review yearly and avoid common mistakes

Your retirement plan is not a document you file and forget. Markets shift, your income changes, life events happen, and a plan built on last year's assumptions can quietly drift off course without a single annual check. For anyone serious about retirement planning for beginners, building the review habit into your calendar is as important as automating your contributions. Set a fixed date each year, right after you file your income tax return, and run through the same checklist every time.

A plan reviewed once a year stays aligned with your life. A plan reviewed never becomes someone else's problem to solve.

Run an annual review in four steps

Your yearly review doesn't need to take more than an hour if you approach it systematically. Compare your actual corpus balance against your projected target using the original calculation from Step 3, and check whether the gap is narrowing at the rate you expected. If your portfolio has grown faster than projected, consider whether you can slightly reduce monthly contributions or bring your retirement date forward. If it has grown slower, you need to increase your SIP amounts or adjust your asset allocation before the shortfall compounds further.

Follow this four-step annual review process:

Pull your portfolio statement from your mutual fund, NPS, EPF, and PPF accounts and total your current corpus.

Recalculate your corpus target using your updated monthly expense figure and the remaining years to retirement.

Compare your current allocation against the target allocation for your age bracket from Step 5 and rebalance if any asset class has drifted more than 5%.

Review your insurance cover to confirm your term sum assured and health cover still match your current income and family responsibilities.

Mistakes that quietly kill retirement plans

The first and most damaging mistake is stopping SIPs during a market downturn. Markets recover, but the units you miss buying at lower prices during that period never come back. Stay invested through volatility and only adjust your allocation, never your contribution frequency. The second common error is over-investing in real estate while ignoring liquidity, which leaves you asset-rich but cash-poor in retirement when you need monthly income, not a property you struggle to sell.

Two further mistakes to actively avoid:

Ignoring healthcare inflation: Medical costs in India rise at 10% to 14% annually, well above general inflation. Review your health cover limit every two to three years and increase it accordingly.

Skipping nomination updates: Failing to update nominees on your EPF, NPS, PPF, and mutual fund accounts after major life events like marriage or the birth of a child creates legal complications your family should never have to face.

You now have a plan

Retirement planning for beginners comes down to nine concrete steps, and you now have all of them. You defined your goals, estimated your expenses with inflation factored in, calculated a real corpus target, mapped your income sources, chose your investments, automated your contributions, built a protection layer, designed your withdrawal strategy, and set up a yearly review process. Each step connects to the next, and the whole system works because you built it on your actual numbers, not generic assumptions.

The most important move you can make right now is to act on the first step today, not next month. Every month you delay costs you compounding you can never recover. If you want a personalized plan built around your specific income, goals, and risk profile, Invsify gives you AI-powered, conflict-free financial advice backed by a SEBI Registered Investment Advisor.

Start your retirement plan with Invsify and put your money to work from day one.