SBI Retirement Calculator: Estimate Corpus, SIP, Pension

Shlok Sobti

SBI Retirement Calculator: Estimate Corpus, SIP, Pension

Planning for retirement without knowing your numbers is like driving blindfolded. Most salaried Indians delay retirement planning because the math feels overwhelming, how much do you actually need, and how much should you save monthly to get there? An SBI retirement calculator can answer these questions in minutes, giving you clarity on your corpus requirements, SIP amounts, and projected pension income.

Whether you're exploring NPS, mutual funds, or a combination of both, understanding these projections early can save you lakhs in the long run. This guide walks you through how retirement calculators work, what inputs matter, and how to interpret the results for smarter financial decisions.

At Invsify, we help salaried professionals move beyond basic calculators to AI-powered, personalized retirement planning, but first, let's make sure you understand the fundamentals and get accurate estimates for your future.

What the SBI retirement calculator covers

An SBI retirement calculator estimates three critical numbers: the total corpus you need at retirement, the monthly SIP required to reach that goal, and the approximate pension you can draw from that corpus. These calculators typically focus on inflation-adjusted projections, meaning they account for rising living costs over the next 20 to 30 years. You input your current age, retirement age, monthly expenses, and expected return rate, and the tool generates your roadmap.

Core metrics the calculator generates

The calculator produces three primary outputs that shape your retirement strategy. First, it shows your retirement corpus, the lump sum amount you need to maintain your lifestyle post-retirement. Second, it calculates the monthly SIP contribution required today to accumulate that corpus, assuming a steady investment in NPS, mutual funds, or similar vehicles. Third, it estimates your monthly pension or withdrawal amount based on the corpus and expected post-retirement returns.

Understanding these three numbers gives you a concrete action plan instead of vague goals.

Key assumptions built into the model

Most retirement calculators assume a constant rate of return between 8% and 12% annually, depending on whether you choose debt, equity, or hybrid funds. They also factor in inflation rates, usually 6% to 7%, to adjust your future expenses. The calculator typically assumes you'll live 20 to 25 years post-retirement, a standard actuarial estimate for Indian life expectancy. These assumptions simplify complex variables, but you need to stress-test them against real-world volatility, which we'll cover later in this guide.

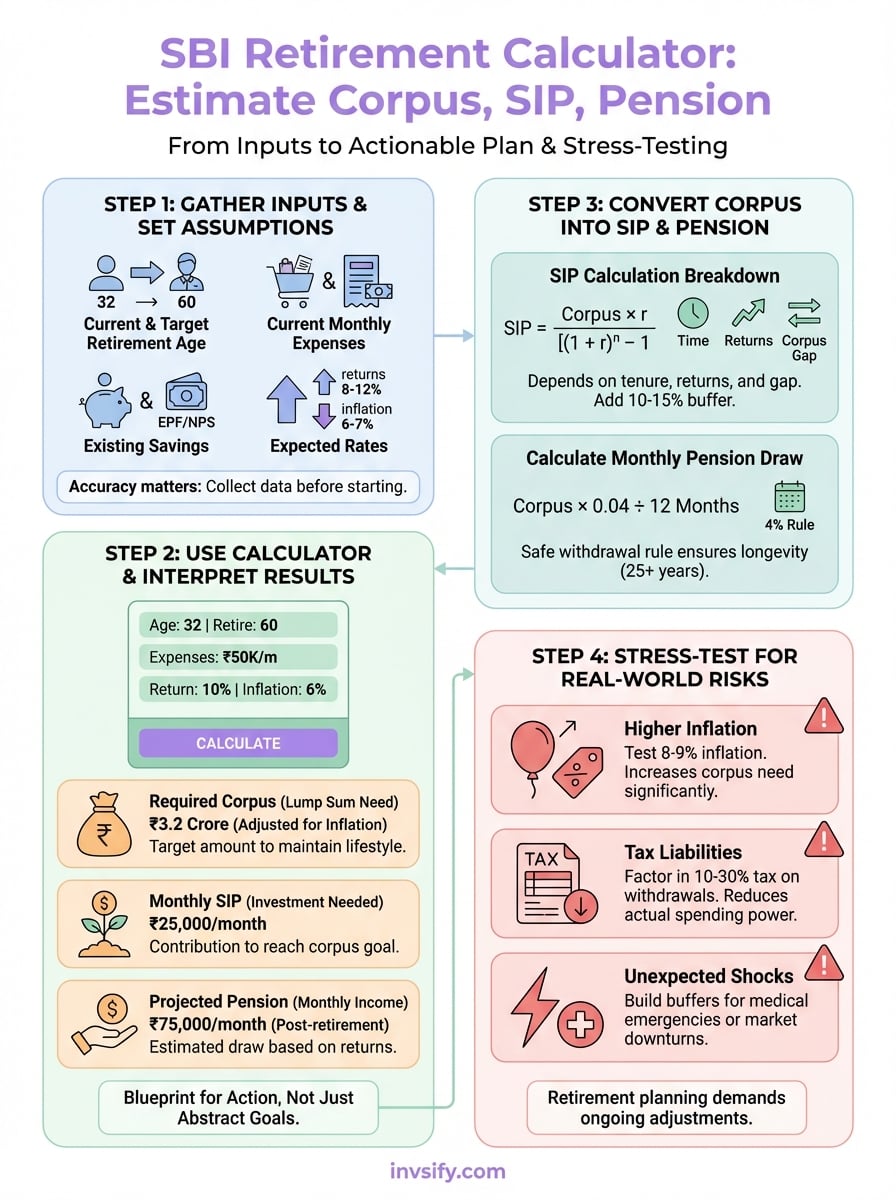

Step 1. Gather inputs and set assumptions

Before you open an SBI retirement calculator, collect five specific data points that drive your projections. You need your current age, target retirement age (typically 58 to 65), current monthly expenses, existing retirement savings, and expected annual returns. These inputs determine whether your calculations reflect reality or wishful thinking, so accuracy matters more than speed.

Prepare your financial baseline

Start by documenting your current monthly expenses in a spreadsheet or notes app. Include housing, utilities, groceries, insurance, healthcare, and discretionary spending. If you spend ₹50,000 monthly today, assume you'll need ₹80,000 to ₹1,00,000 monthly at retirement after adjusting for inflation. Next, list your existing retirement corpus, whether that's EPF, NPS, or mutual fund balances. This becomes your starting point for gap analysis.

Choose realistic growth and inflation rates

Set your expected return rate between 8% and 12% depending on your risk appetite. Conservative investors targeting debt-heavy portfolios should use 8%, while equity-focused strategies can assume 10% to 12%. Lock in an inflation rate of 6% to 7% for expenses, as this matches India's historical average. These assumptions shape your entire projection, so avoid overly optimistic numbers that leave you short at retirement.

Setting conservative assumptions now prevents unpleasant surprises 20 years later.

Step 2. Use the SBI calculator and read the results

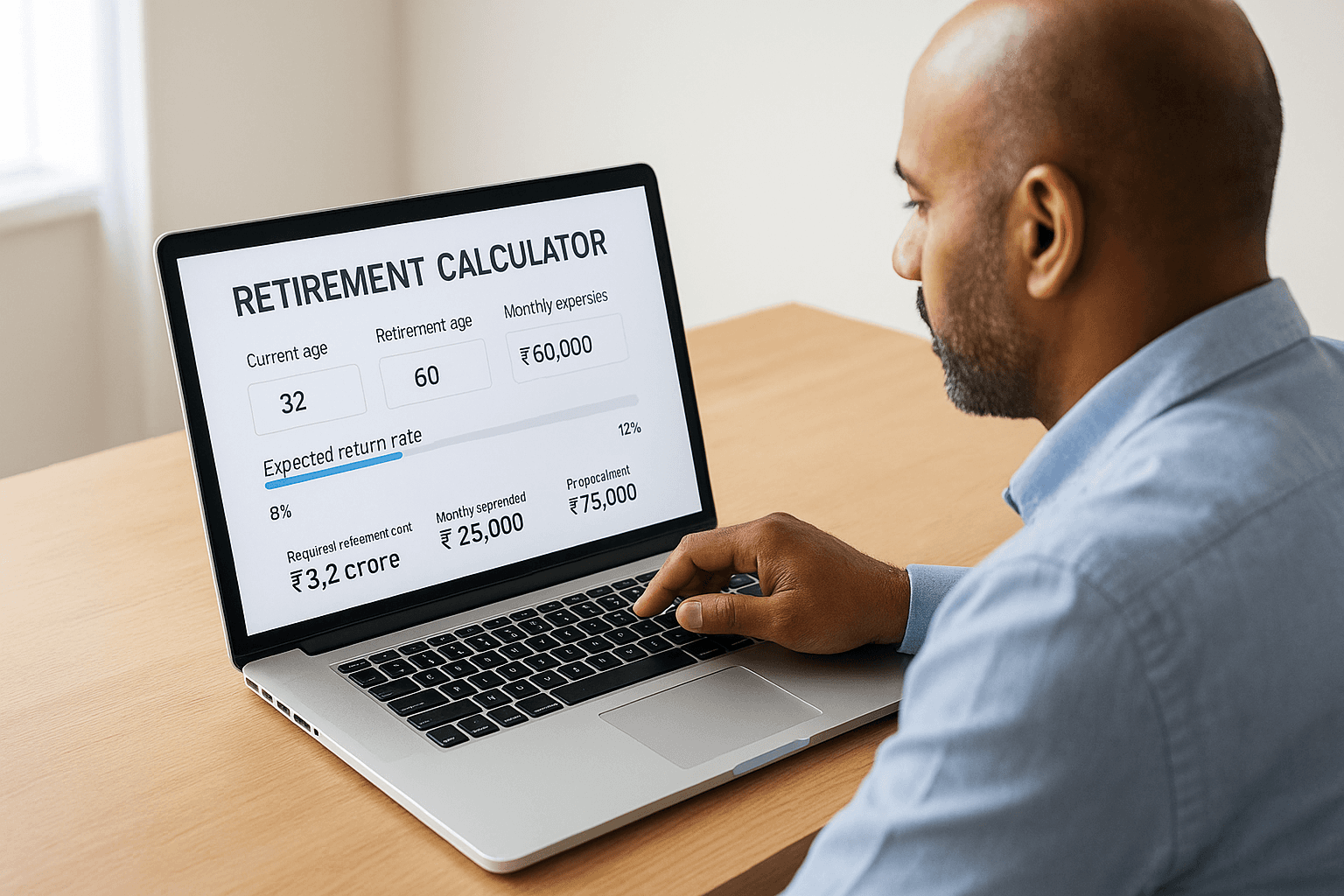

Open the SBI retirement calculator through your bank's investment portal or search for similar tools from HDFC, ICICI, or independent platforms like ClearTax. Enter your prepared inputs: current age, retirement age, monthly expenses, existing corpus, and expected returns. The calculator processes these numbers instantly and displays three critical outputs that define your retirement strategy. Review each metric carefully before making any investment decisions based on the projections.

Navigate the calculator interface

Input fields appear in sequential order, starting with personal details like current age (e.g., 32 years) and retirement age (e.g., 60 years). Next, you enter your current monthly expenses, say ₹50,000, and the tool automatically inflates this to future values. Finally, you select your expected annual return rate between 8% and 12% based on your risk profile. Most calculators include a slider or dropdown for each field, making adjustments easy if you want to test different scenarios.

Interpret your three key outputs

The results screen displays your required retirement corpus (e.g., ₹3.2 crore), the monthly SIP needed (e.g., ₹25,000), and your projected monthly pension (e.g., ₹75,000). Compare the SIP requirement against your current savings capacity to identify any shortfall. If the monthly SIP exceeds your budget, you'll need to either extend your retirement age or reduce projected expenses.

These three numbers form your actionable retirement blueprint, not just abstract goals.

Step 3. Convert corpus into monthly SIP and pension

Once you have your retirement corpus target, you need to translate that number into two actionable figures: the monthly SIP you must invest today and the pension income you'll receive later. The SBI retirement calculator handles this math automatically, but understanding the formulas lets you verify accuracy and adjust strategies independently. This conversion process bridges the gap between abstract corpus goals and concrete monthly commitments you can execute through your salary account.

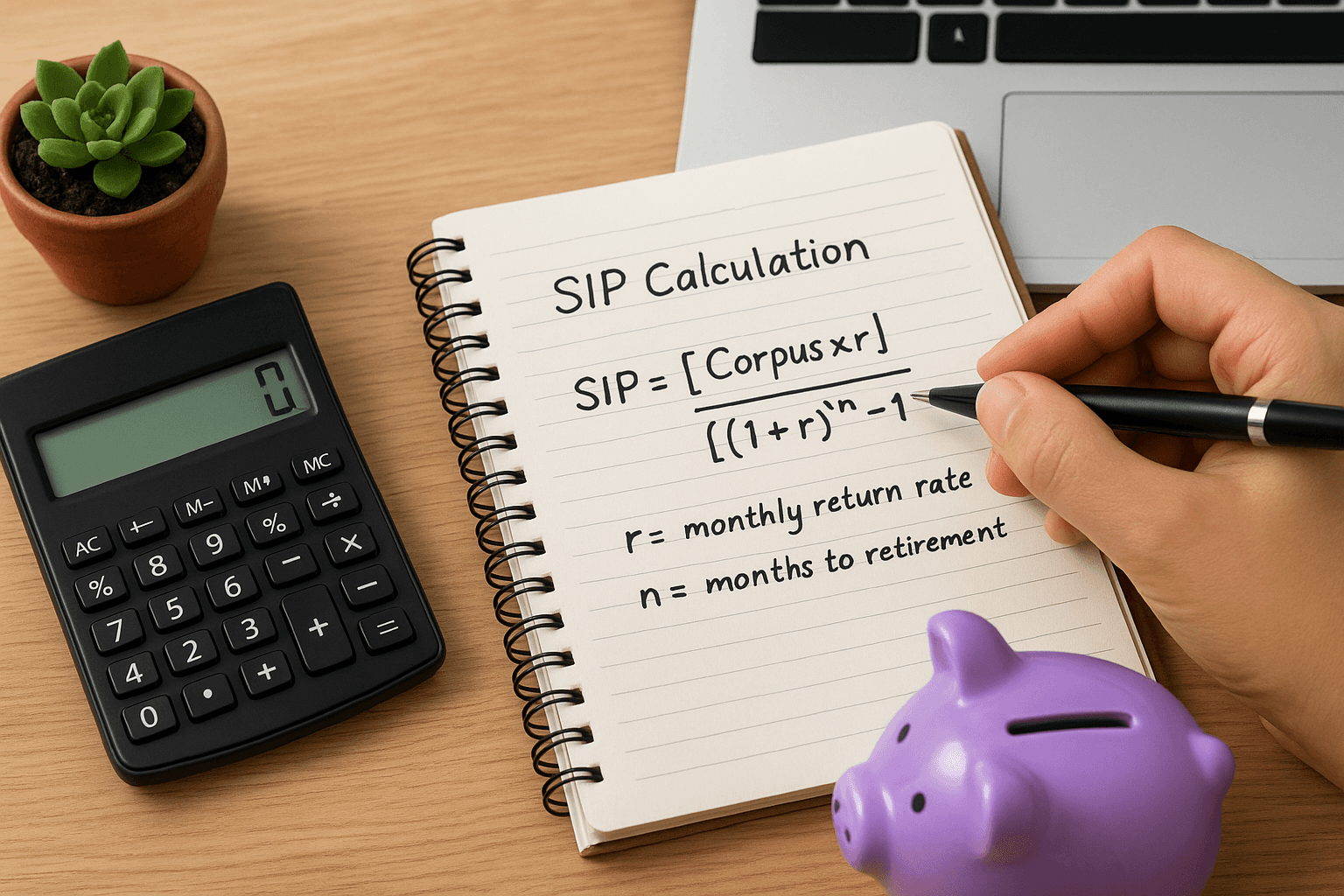

Break down the SIP calculation

Your required SIP depends on investment tenure (years until retirement), expected returns, and the corpus gap between your target and existing savings. The formula uses compound interest: SIP = [Corpus × r] / [(1 + r)^n - 1], where r is the monthly return rate and n is months to retirement. For example, if you need ₹3 crore in 28 years at 10% annual returns, your monthly SIP equals approximately ₹24,500. Adjust this figure upward by 10% to 15% as a safety buffer against market volatility.

Calculate your monthly pension draw

Your corpus converts to monthly income using the 4% safe withdrawal rule, a globally recognized standard for retirees. Multiply your corpus by 0.04, then divide by 12 months to get your starting pension. A ₹3 crore corpus yields ₹1 lakh monthly (₹3,00,00,000 × 0.04 ÷ 12 = ₹1,00,000). This assumes your remaining corpus continues earning returns that offset inflation.

The 4% rule ensures your corpus lasts 25+ years without depleting prematurely.

Step 4. Stress-test for inflation, taxes, and shocks

Your SBI retirement calculator projections assume ideal conditions, but real life delivers market crashes, medical emergencies, and tax changes that erode your corpus faster than expected. You need to stress-test your numbers against three specific risks: higher inflation than 6%, tax liabilities on withdrawals, and unexpected shocks that force early withdrawals. Run these scenarios now to identify gaps before they become irreversible shortfalls.

Test higher inflation scenarios

Recalculate your corpus using 8% to 9% inflation instead of the standard 6% to 7%. If your original ₹3 crore target assumed 6% inflation, bumping it to 8% pushes your requirement to ₹4.2 crore or higher. This 40% increase demands an extra ₹8,000 to ₹10,000 monthly SIP starting today. Healthcare and housing consistently outpace general inflation, so conservative planning means assuming worst-case rates for essential expenses.

Planning for 8% inflation today prevents corpus depletion 15 years into retirement.

Factor in tax liabilities

Your ₹1 lakh monthly pension faces 10% to 30% tax depending on income slabs and withdrawal sources. NPS withdrawals incur tax on 40% of corpus, while equity mutual funds carry capital gains tax. Calculate your post-tax pension by reducing gross withdrawals by 15% to 20%, lowering your ₹1 lakh target to ₹80,000 to ₹85,000 in actual spending power.

A simple wrap-up

You now have a complete framework for using an SBI retirement calculator to estimate your corpus, SIP contributions, and pension projections. Start by gathering accurate inputs, run the calculator with realistic assumptions, and translate those results into actionable monthly investments. The critical step most investors skip is stress-testing, adjust for higher inflation, factor in taxes, and build buffers against medical emergencies or market downturns that inevitably arrive.

Basic calculators give you starting numbers, but retirement planning demands ongoing adjustments as your salary grows, market conditions shift, and life goals evolve. Manually recalculating every year becomes tedious and error-prone, which is where automated, AI-powered tools create real advantage. If you want personalized retirement tracking that updates automatically based on your actual portfolio performance and expense patterns, explore Invsify's smart advisory platform for conflict-free guidance that goes beyond static calculators.