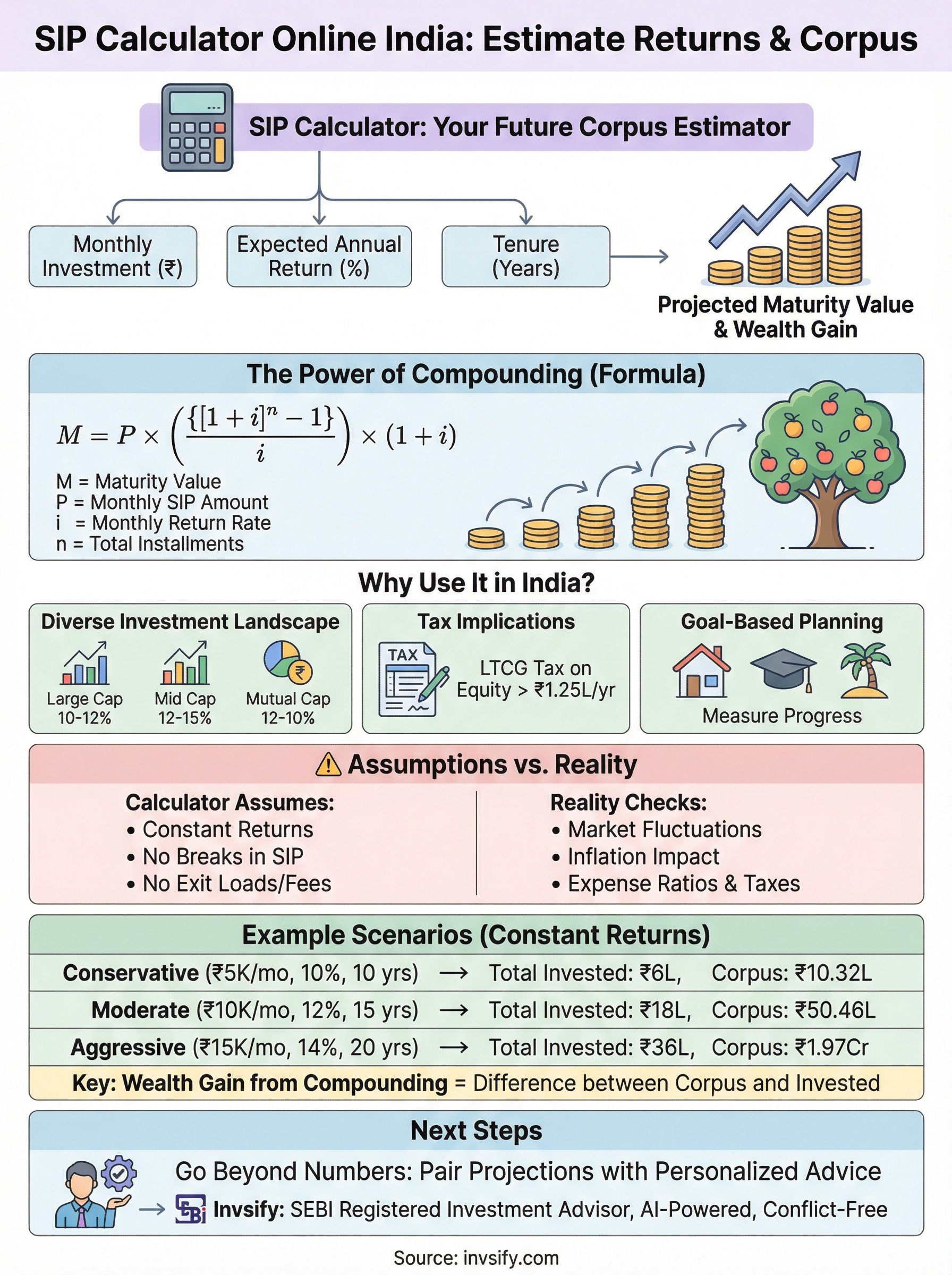

SIP Calculator Online India: Estimate Returns And Corpus

Shlok Sobti

SIP Calculator Online India: Estimate Returns And Corpus

You've decided to invest through SIPs, or you're seriously considering it. Either way, the first question is always the same: how much will my money actually grow? A SIP calculator online India tool gives you that answer in seconds, letting you estimate your future corpus based on your monthly investment, expected return rate, and time horizon.

Instead of guessing or relying on back-of-the-envelope math, a SIP calculator runs the compounding math for you. Plug in your numbers, adjust the variables, and instantly see how small monthly contributions can build into a significant corpus over 10, 15, or 20+ years. It removes the ambiguity from planning and gives you a concrete number to work toward.

At Invsify, we built our AI-powered advisory platform around this exact principle, making financial planning clear and actionable for salaried individuals across India. As a SEBI Registered Investment Advisor, we go beyond calculators by pairing data-backed projections with conflict-free, personalized investment recommendations that help you actually reach the corpus you're targeting.

This article breaks down everything you need to know about SIP calculators: how they work, the formula behind the numbers, what assumptions to watch out for, and how to use the results to make smarter investment decisions. Whether you're starting your first SIP of ₹500 or optimizing an existing portfolio, this guide will help you plan with precision rather than hope.

Why use a SIP calculator in India

Most people who invest through SIPs underestimate the power of compounding over long time horizons, not because they're careless, but because compound growth is genuinely difficult to visualize without a dedicated tool. A SIP calculator closes that gap instantly. You enter your monthly contribution, your expected annual return, and your investment period, and the calculator shows you exactly what corpus you can build rather than leaving you with a vague sense that things should work out eventually.

The earlier you run the numbers, the more clearly you see that the difference between starting at 25 and starting at 35 is not just 10 years of contributions but often several lakhs, or even crores, in final corpus.

India's investment landscape makes projection more important

India's mutual fund ecosystem has grown significantly over the past decade, with thousands of schemes across equity, debt, and hybrid categories offering very different expected return profiles. When you compare a large-cap fund targeting 10-11% annual returns against a mid-cap fund targeting 14-15%, the gap looks modest. Run those numbers through a sip calculator online india tool over 20 years, and the difference in final corpus can exceed ₹30-40 lakhs on a ₹10,000 monthly SIP. That magnitude changes how seriously you treat fund selection at the start.

The tax structure in India also makes planning more nuanced than it first appears. Long-term capital gains (LTCG) tax on equity mutual funds applies above ₹1.25 lakh in gains per financial year, while debt fund gains are taxed at your applicable income slab rate. When a calculator projects a large corpus for you, it helps you anticipate the post-tax reality and plan your redemptions or fund switches well ahead of time rather than discovering the tax bill at withdrawal.

Setting goals you can actually measure

One of the strongest reasons to use a SIP calculator is that it connects your savings behavior directly to a specific financial goal, whether that's a down payment on a flat, your child's higher education, or retirement. Without a concrete number in front of you, SIP investing can feel like a habit rather than a real strategy. With a projected corpus, you're measuring progress against a clear and defined target.

This benefit matters especially for salaried individuals in India who receive a fixed monthly income and need to split that income across multiple competing goals. Running separate projections for each goal tells you how much to allocate per SIP rather than dividing money arbitrarily and hoping for the best.

Adjusting for life changes before they happen

Your income, expenses, and financial priorities will shift over time, and a SIP calculator lets you model those changes in advance instead of reacting after the fact. You can test what happens if you step up your SIP by ₹2,000 following a salary hike, or how a six-month contribution pause affects your final corpus. Both scenarios take seconds to run, cost you nothing to test, and reveal the real financial weight of each decision before you make it.

These quick projections give you a clear picture of how today's choices affect tomorrow's wealth. That kind of disciplined, forward-looking planning is what separates investors who consistently hit their corpus targets from those who keep revising their timelines downward.

What a SIP calculator includes and assumes

Every sip calculator online india tool is built on the same three inputs and a fixed set of assumptions that determine how reliable your projections are. Understanding both sides, what you enter and what the calculator presumes to be true, helps you read the output with the right level of confidence rather than treating a projected number as a guarantee.

The three core inputs

A SIP calculator asks you for three things: your monthly investment amount, your expected annual return rate, and your investment tenure in years or months. You don't need to input fund-specific data, historical NAVs, or portfolio composition. The simplicity is intentional because the goal is to give you a fast, directional estimate of corpus and wealth gain, not a precise simulation of how a specific fund will perform.

Most calculators also display two output figures: total amount invested (your actual contributions) and estimated returns (the wealth gain from compounding). Seeing both figures side by side is one of the clearest ways to visualize how much of your final corpus comes from the market doing work rather than you simply saving.

The assumptions behind the numbers

Here is where you need to pay close attention. A standard SIP calculator assumes a constant annual return rate for the entire investment period, which is a simplification. Real mutual fund returns fluctuate year to year, with some years delivering strong growth and others delivering flat or negative performance. The projected corpus is the mathematical result of applying one steady rate across every compounding cycle, not a forecast of actual fund performance.

The return rate you choose is the single biggest variable in your projection. A 1% difference in assumed annual return, compounded over 20 years, can shift your estimated corpus by several lakhs.

The calculator also assumes no breaks in your SIP contributions, meaning every installment goes in on schedule for the full tenure. It does not account for inflation eroding your corpus's real purchasing power, nor does it factor in exit loads, expense ratios, or applicable taxes on redemption. These are real costs that reduce your net returns, and any serious financial plan should account for them beyond what the calculator shows.

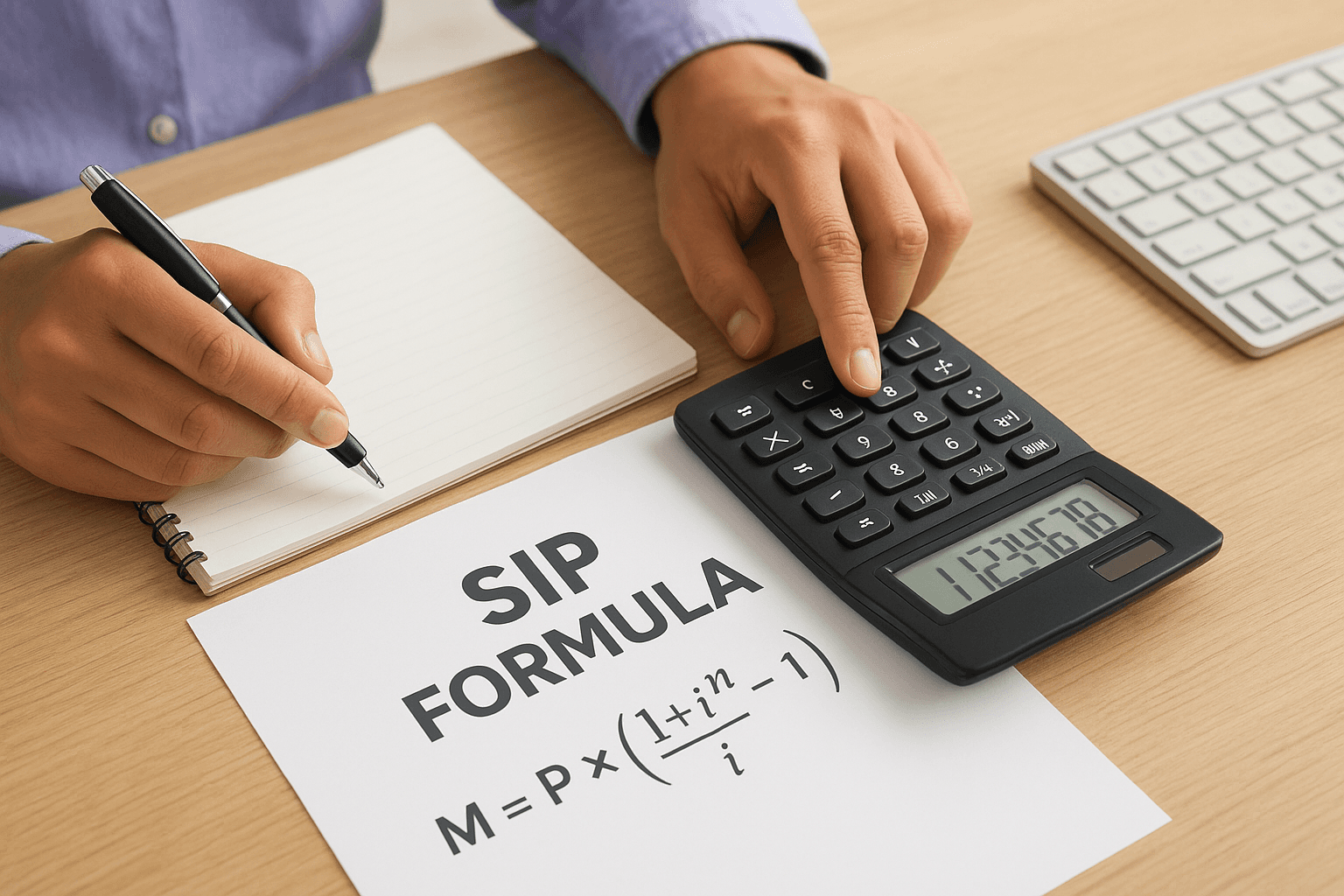

How a SIP calculator works and the formula

A sip calculator online india tool is not guessing at your corpus; it runs a specific mathematical formula every time you adjust an input. The formula treats each monthly SIP installment as a separate investment that compounds from the month it is made until the end of your chosen tenure. Because you invest a fixed amount each month, the first installment earns returns for the longest period, and the last installment earns returns for just one month. The calculator adds all these individual compounded values together to produce your final projected corpus.

The SIP formula explained

The formula behind every SIP calculator follows a standard future value of annuity model:

M = P × ({[1 + i]^n - 1} / i) × (1 + i)

Where:

M is the maturity value, meaning the total corpus at the end of your tenure

P is your monthly SIP contribution amount in rupees

i is the periodic rate of return, calculated as your annual return rate divided by 12

n is the total number of monthly installments across your investment period

This formula is classified as a future value of an annuity calculation, which is why it correctly models a series of equal payments made at regular intervals rather than a single lump-sum investment.

What the formula actually calculates

When you enter ₹10,000 per month, a 12% annual return, and a 15-year tenure, the calculator converts 12% into a monthly rate of 1% and sets n at 180 installments. It then applies the formula to produce a projected maturity value and subtracts your total contributions of ₹18,00,000 to show your estimated wealth gain from compounding alone, which is the figure that often surprises first-time users.

Running the same numbers yourself confirms why small input changes create large output shifts. Raising your monthly contribution from ₹10,000 to ₹12,000 increases your total invested amount by ₹3.6 lakhs over 15 years, but it raises your projected corpus by significantly more because every additional rupee compounds across all remaining months from the point it enters. That multiplier effect is what makes consistent, uninterrupted SIP investing over long periods far more powerful than a series of one-time lump-sum deposits made at irregular intervals.

How to use a SIP calculator online step by step

Using a sip calculator online india tool takes under two minutes, but the quality of your projection depends entirely on how carefully you choose each input. Entering numbers without thinking them through produces a result that looks precise but reflects wishful thinking rather than a real plan.

Step 1: Enter your three inputs

A SIP calculator asks for three values. Enter each one deliberately and honestly rather than optimistically:

Monthly investment amount: Use the amount you will actually transfer each month, not the amount you hope to eventually reach. Overestimating here inflates your projected corpus and causes you to under-save for your actual goal.

Expected annual return rate: Base this on the fund category you plan to use. Large-cap equity funds in India have historically delivered 10-12% annualized returns, while mid-cap or flexi-cap funds have averaged 12-14%. Use the lower bound of whichever range applies to your choice.

Investment tenure: Enter the exact number of years until you need the corpus. Rounding down to make the monthly number look smaller defeats the purpose of projecting at all.

Step 2: Read the output as a range, not a guarantee

Once the calculator runs, you will see two figures: total amount invested and estimated maturity value. The gap between them is your projected wealth gain from compounding. Look at this gap carefully because it tells you how much of your final corpus the market is expected to generate versus what you are contributing directly from your income.

The projected maturity value is a mathematical estimate based on a constant return rate. Treat it as a planning reference point, not a confirmed outcome, and stress-test it by running the same inputs at a return rate 2% lower than your base assumption.

Step 3: Adjust until the numbers match your goal

If the projected corpus falls short of your financial goal, increase your monthly contribution first before stretching your tenure. Adding more capital from the beginning means every additional rupee compounds for the full remaining period. If you cannot increase the contribution right now, set a step-up reminder tied to your next salary increment so the adjustment happens automatically rather than getting postponed indefinitely.

Running multiple scenarios side by side also helps you weigh trade-offs clearly. Testing three or four combinations of contribution amount and tenure takes less than five minutes and gives you a concrete sense of which adjustment delivers the most corpus gain for the least additional financial strain each month.

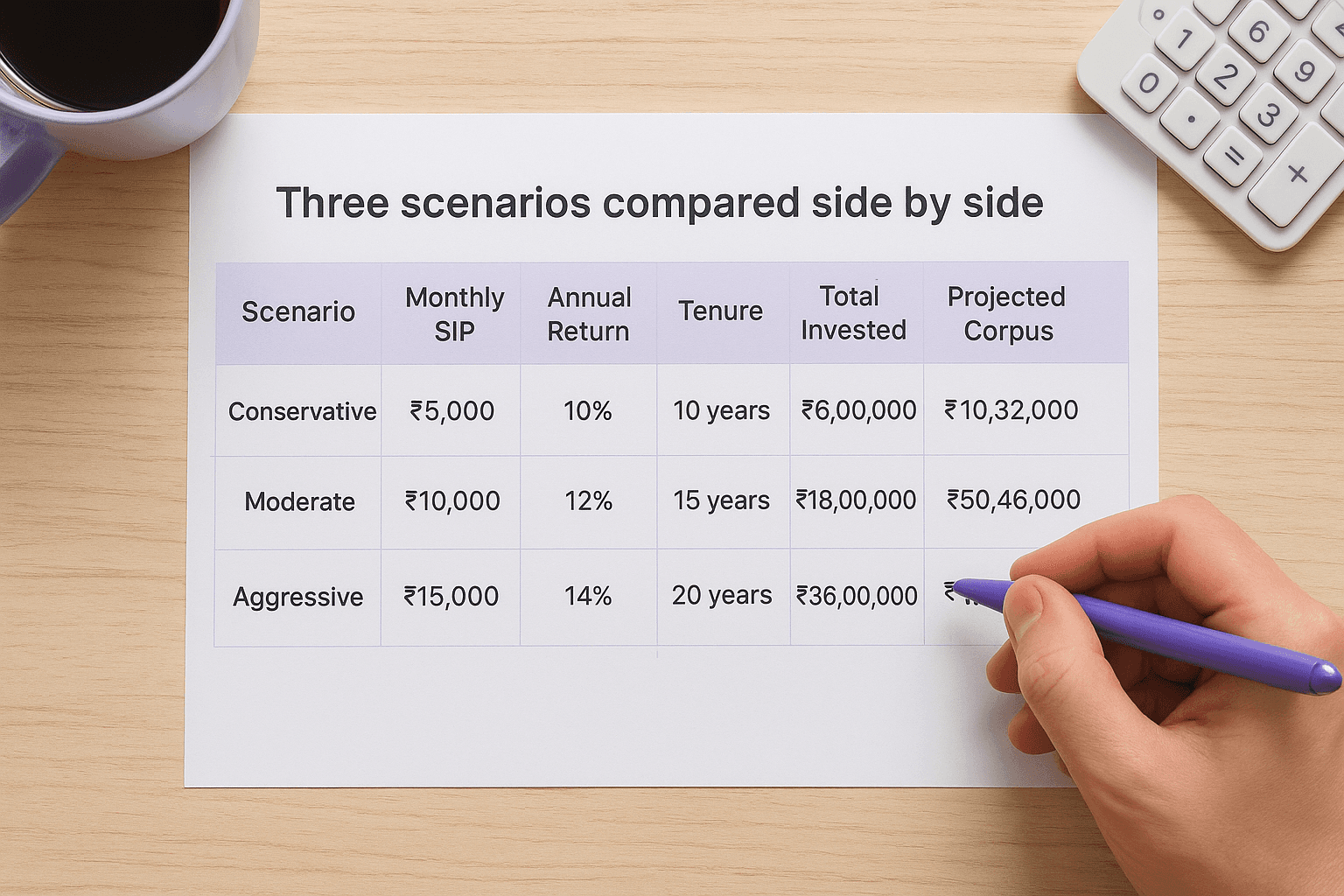

Examples of SIP returns for common scenarios

Seeing the formula in action with realistic numbers makes the math feel concrete rather than theoretical. The three scenarios below represent common investment profiles among salaried individuals in India, ranging from a beginner putting aside a modest amount to a mid-career professional investing more aggressively. Run each of these through any sip calculator online india tool and you will get the same figures, which confirms the formula is working correctly.

Three scenarios compared side by side

The table below uses the standard SIP formula and assumes constant annual returns with no contribution breaks. These return assumptions sit within the historical performance bands for their respective fund categories.

Scenario | Monthly SIP | Annual Return | Tenure | Total Invested | Projected Corpus | Wealth Gain |

|---|---|---|---|---|---|---|

Conservative | ₹5,000 | 10% | 10 years | ₹6,00,000 | ₹10,32,000 | ₹4,32,000 |

Moderate | ₹10,000 | 12% | 15 years | ₹18,00,000 | ₹50,46,000 | ₹32,46,000 |

Aggressive | ₹15,000 | 14% | 20 years | ₹36,00,000 | ₹1,97,00,000 | ₹1,61,00,000 |

The aggressive scenario shows that compounding generates over four times the investor's actual contribution, which is the clearest illustration of why tenure matters more than any single contribution increase.

What these numbers reveal about your own plan

The conservative scenario shows that even a ₹5,000 monthly commitment, which is achievable on most starting salaries, builds a corpus of over ₹10 lakhs in a decade. That result comes from ₹6 lakhs of your own money and ₹4.32 lakhs generated entirely through compounding. For someone saving toward a down payment on a two-wheeler, a travel fund, or an emergency buffer, this scenario is a realistic and reachable target.

The moderate scenario is where the compounding effect becomes visually striking. Your ₹18 lakhs in contributions grow to over ₹50 lakhs, meaning the market contributes nearly ₹32.5 lakhs without any additional effort on your part. This is the scenario most relevant to salaried professionals targeting a goal like their child's undergraduate education or a partial home loan repayment.

Studying the aggressive scenario alongside the moderate one reveals the real value of starting early rather than investing more. Someone who starts at 25 with ₹10,000 per month over 20 years will, in many cases, outperform someone who starts at 35 with ₹20,000 per month over 10 years, simply because compound growth needs time more than it needs capital.

Mistakes to avoid when reading SIP results

A sip calculator online india tool is only as useful as your ability to interpret what it shows you. The number at the end is not a promise; it is a mathematical result built on assumptions you chose, and reading it without questioning those assumptions can lead you to plan for a corpus that reality will not deliver. Knowing where investors routinely go wrong helps you use the output correctly from the start.

Treating the projected corpus as a guaranteed outcome

The most common mistake is accepting the maturity value as a confirmed figure. Every SIP calculator assumes a constant annual return rate throughout the entire tenure, but actual mutual fund returns vary year to year based on market conditions. Equity funds can deliver 18-20% in a strong year and negative returns in a downturn. Your final corpus will differ from the projection, sometimes by a meaningful margin, depending on the sequence of returns your fund actually experiences over your investment period.

Run your projection twice: once at your base expected return rate, and once at 2-3% lower. The gap between these two outcomes defines the planning range you should work within, not a single fixed number.

Ignoring costs that reduce your actual returns

Most calculators show gross returns before any deductions, which means they do not factor in the expense ratio your mutual fund charges annually, exit loads if you redeem before the stipulated period, or the tax you owe on gains at withdrawal. An equity fund with a 1% annual expense ratio effectively reduces your net return by 1% each year, and compounded over 15-20 years, that shaves several lakhs off your final corpus. Add the applicable LTCG tax on equity gains above ₹1.25 lakh per financial year, and the amount you actually receive at redemption can fall noticeably below what the calculator projected.

Stopping at one scenario

Many investors run a single projection using their current monthly contribution and treat that as their plan. Your income will grow over time, and a SIP that felt stretched at 25 will feel routine at 32. Not testing a step-up scenario means you are planning for a lower corpus than you could realistically build. Run a second calculation that increases your monthly amount by ₹1,000 to ₹2,000 each year, compare the final corpus against your base scenario, and let that gap inform your next salary increment conversation with yourself.

Your next step

A sip calculator online india tool gives you the numbers, but numbers alone do not build wealth. What actually moves you forward is pairing those projections with personalized, conflict-free advice that accounts for your actual income, goals, tax situation, and risk tolerance. Running a calculation is step one. Acting on it with a clear, structured investment plan is step two.

Invsify is built to help you take that second step. As a SEBI Registered Investment Advisor, Invsify provides AI-powered recommendations with no hidden commissions or distributor bias, so the advice you receive reflects your goals, not someone else's sales targets. You get a personalized Wealth Wellness Score, real-time advisory, and human support whenever you need it. Your corpus target is already in front of you.

Start your investment plan with Invsify and turn your SIP projection into a strategy that actually reaches the number you calculated.