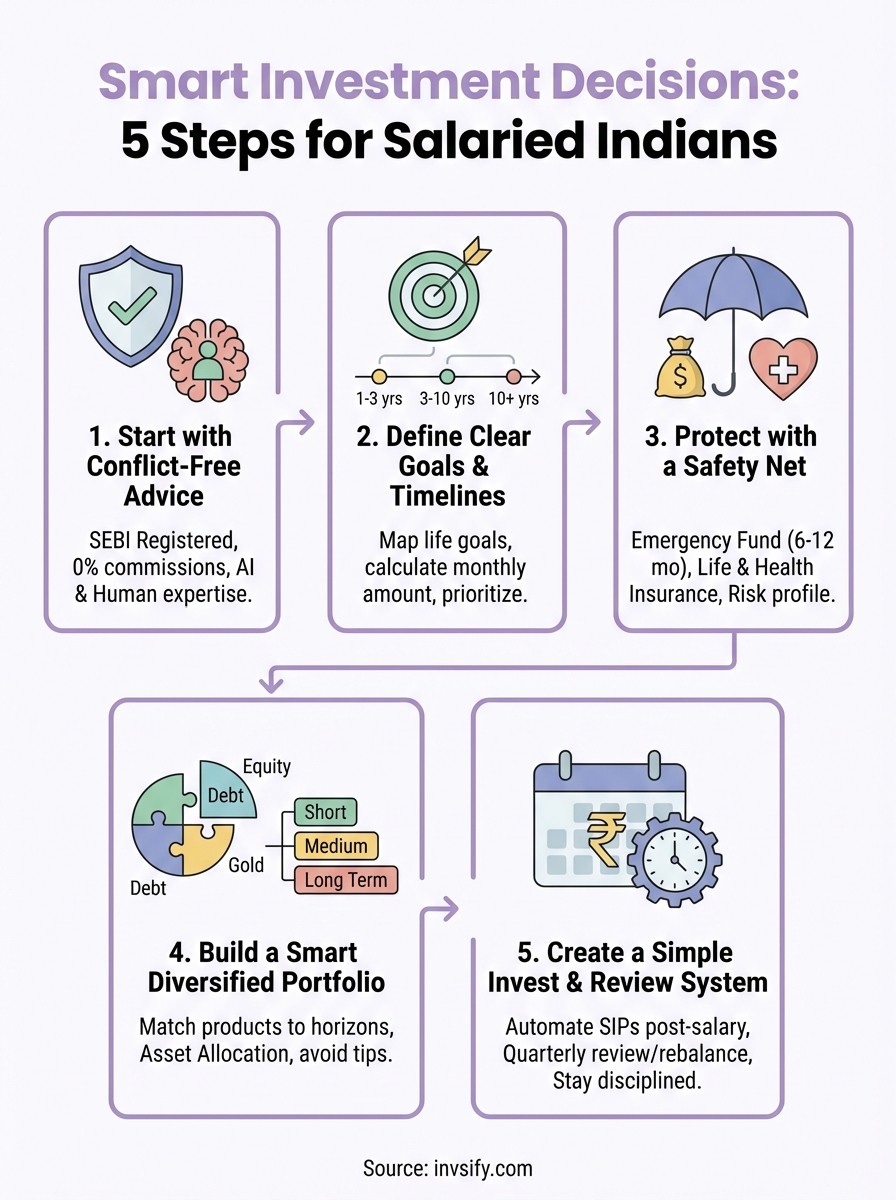

Smart Investment Decisions: 5 Steps for Salaried Indians

Shlok Sobti

Smart Investment Decisions: 5 Steps for Salaried Indians

You get your salary each month. You know you should invest. But where? Mutual funds or stocks? Gold or real estate? Should you follow that WhatsApp tip from a friend or listen to that Instagram finance guru? Every source tells you something different. Traditional advisors push products that earn them fat commissions. Online forums give free advice but no one knows if it actually works. You end up doing nothing or making random choices that keep you awake at night wondering if you made the right call.

This guide cuts through the noise. We'll walk you through five practical steps that help you make smart investment decisions without getting overwhelmed. You'll learn how to set clear goals, build a safety net, create a diversified portfolio, and establish a system that works with your salary cycle. Each step is designed specifically for salaried Indians who want to grow wealth without falling for hidden fees or conflicting advice. By the end, you'll have a clear roadmap to invest with confidence and sleep better at night.

1. Start with conflict free advice from Invsify

You need a foundation that keeps your interests first. Most traditional financial advisors earn commissions from the products they sell, which means their advice tilts toward what pays them best, not what serves you best. Invsify operates as a SEBI Registered Investment Advisor, which legally binds the platform to put your financial goals ahead of any commissions. This conflict-free model ensures every recommendation focuses on growing your wealth, not someone else's wallet.

Why conflict free advice matters

Traditional distributors pocket 1 to 2% of your investment value every year through hidden commissions. You never see these fees directly, but they eat into your returns silently. Over 20 years, these hidden charges can cost you lakhs of rupees that should have stayed in your portfolio. Conflict-free advice removes this drag on your returns because you pay a transparent fee for advice, and your advisor has zero incentive to push expensive products. Your money grows faster when no one is siphoning off a cut behind the scenes.

How Invsify blends AI and human expertise

Invsify's Conversational RM AI gives you 24/7 access to financial guidance in multiple languages, answering questions about tax saving, portfolio strategy, or market movements whenever you need clarity. The platform analyzes your complete financial picture and delivers a personalized Wealth Wellness Score that shows exactly where you stand. When you face complex decisions or need a second opinion, you get human support with a 30-second callback for urgent queries, combining the speed of AI with the judgment of experienced advisors.

Smart investment decisions start with advice that serves only your interests, not hidden commission targets.

What to set up in your Invsify account first

Begin with the seamless KYC process and risk profiling that takes just minutes to complete. This step maps your comfort with market fluctuations and helps the AI understand your tolerance for ups and downs. Next, link your existing investments using the advanced portfolio tracking feature so you get a complete view of everything you own in one place. The platform will then generate your first set of AI-powered recommendations based on your risk profile, current holdings, and financial gaps that need attention.

2. Define clear goals and timelines

You cannot make smart investment decisions without knowing what you're investing for. Vague wishes like "I want to be rich" or "I should invest something" lead to random product purchases that don't serve any real purpose. Clear goals with specific timelines turn investing from a guessing game into a systematic plan. Your salary becomes a tool to fund specific life events, and every rupee you invest has a defined job to do.

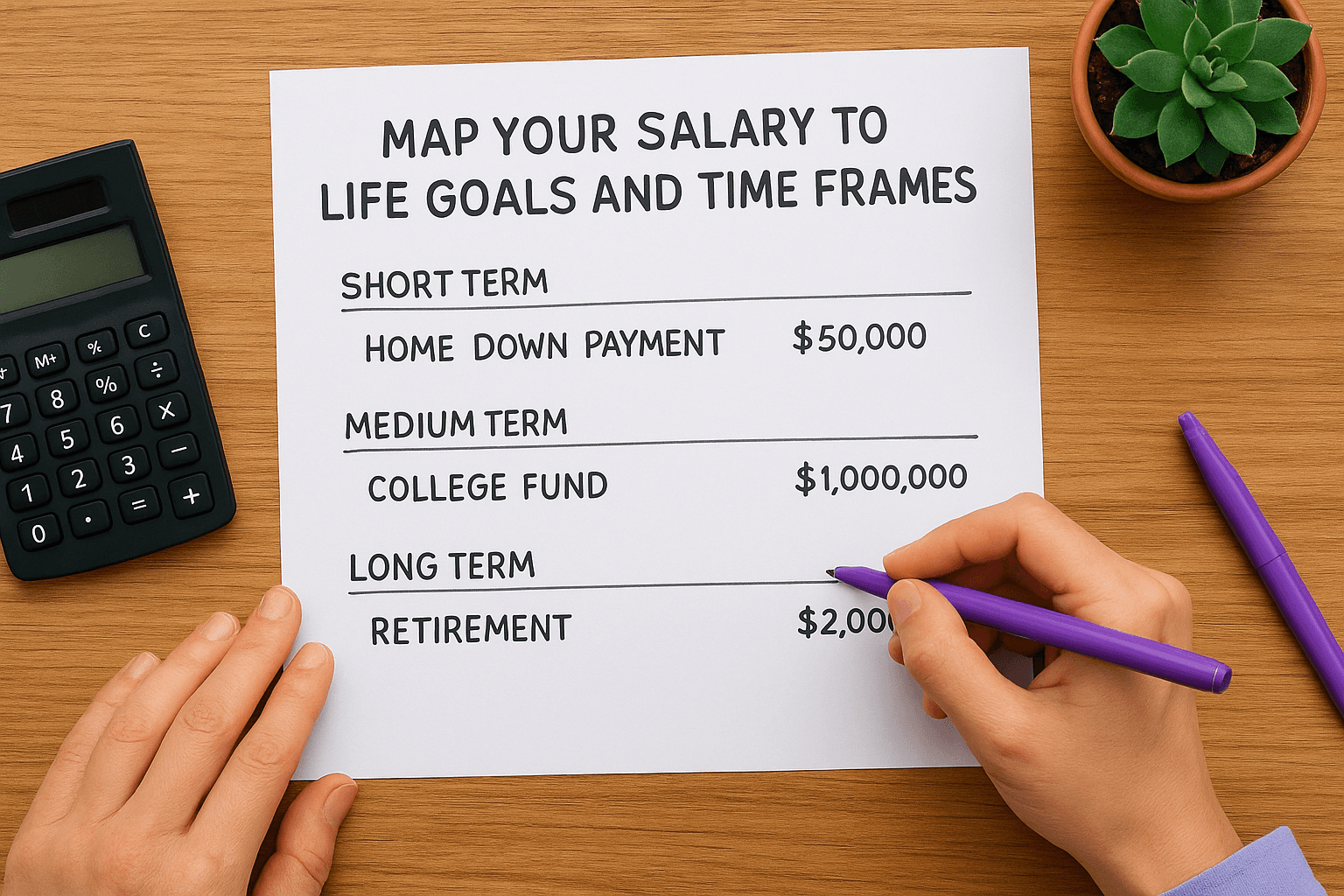

Map your salary to life goals and time frames

Start by writing down every financial goal you can think of over the next 30 years. Your child's college education in 12 years, a home down payment in 5 years, or retirement in 25 years all belong on this list. Attach a realistic cost in today's money to each goal, then group them by timeline: short term (1 to 3 years), medium term (3 to 10 years), and long term (beyond 10 years). This mapping exercise shows you exactly where your salary needs to flow and how much time you have to reach each target.

Turn goals into monthly investment amounts

Calculate how much you need to invest each month to hit each goal by using the power of compounding. A 10 lakh education fund needed in 12 years requires roughly 4,500 rupees monthly at a 12% annual return, while the same goal in just 5 years demands closer to 12,000 rupees monthly. Break down every goal into a monthly number that fits your salary cycle, making the path forward concrete and actionable rather than overwhelming.

Goals without monthly investment targets remain wishes that never materialize into real wealth.

Prioritize goals when money feels tight

When your salary cannot fund every goal at once, you must rank goals by urgency and importance. Emergency funds and critical insurance come first, followed by goals with shorter timelines like your child's school admission next year. Long-term goals can start small and increase later when you get salary hikes or bonuses, giving breathing room for immediate priorities without abandoning future wealth building entirely.

3. Protect yourself with a safety net

Smart investment decisions start only after you secure your financial base against life's unexpected hits. Your salary can vanish overnight through job loss, a medical emergency can drain your savings in weeks, or a family crisis can force you to sell investments at the worst possible time. Building a safety net first means you never have to liquidate your long-term investments during a market downturn, and you avoid taking on expensive debt when emergencies strike. This foundation separates investors who stay the course from those who panic and lose money.

Calculate the right emergency fund for your family

Multiply your monthly household expenses by 6 to 12 months to arrive at your target emergency fund size. Single-income families need the higher end of this range because losing one salary means zero income, while dual-income households can lean toward 6 months since both partners rarely lose jobs simultaneously. Park this money in a liquid fund or savings account where you can access it within 24 to 48 hours without penalty, not in fixed deposits with early withdrawal charges or equity investments that fluctuate daily.

Get basic insurance in place before investing more

Purchase term life insurance covering 10 to 15 times your annual income to protect your family if you're no longer around to earn. Add health insurance with a minimum 5 lakh coverage per family member to prevent medical bills from wiping out your emergency fund and investment corpus. These two insurance types cost a fraction of your salary but shield your wealth-building plan from catastrophic financial hits that derail everything you've worked toward.

Insurance protects your investments by handling risks that money alone cannot solve.

Understand your risk profile and comfort level

Answer honestly whether you can sleep peacefully when markets drop 20% in a month or if you panic and want to exit everything immediately. Your risk profile determines how much equity versus debt you should hold, with aggressive investors comfortable holding 80% equity and conservative investors preferring 40% equity or less. Invsify's risk profiling process matches your comfort level to appropriate investment products, ensuring you never take on more volatility than you can emotionally and financially handle.

4. Build a smart diversified portfolio

Diversification protects you from putting all your eggs in one basket and losing everything when that basket breaks. A smart diversified portfolio spreads your money across different asset classes, time horizons, and risk levels so no single investment can wreck your financial plan. Your salary-based investing works best when you match specific products to specific goals, ensuring each rupee lands in the right place based on when you need it and how much risk that goal can tolerate.

Choose products for short medium and long term

Short-term goals within 3 years need liquid funds or ultra short-term debt funds that preserve capital and provide predictable returns without market volatility threatening your target amount. Medium-term goals between 3 and 10 years perform well with balanced advantage funds or hybrid funds that mix equity growth with debt stability, capturing market upside while cushioning downside risk. Long-term goals beyond 10 years belong in equity mutual funds like large cap, mid cap, or flexi-cap funds where time allows you to ride out market cycles and benefit from compounding at higher rates.

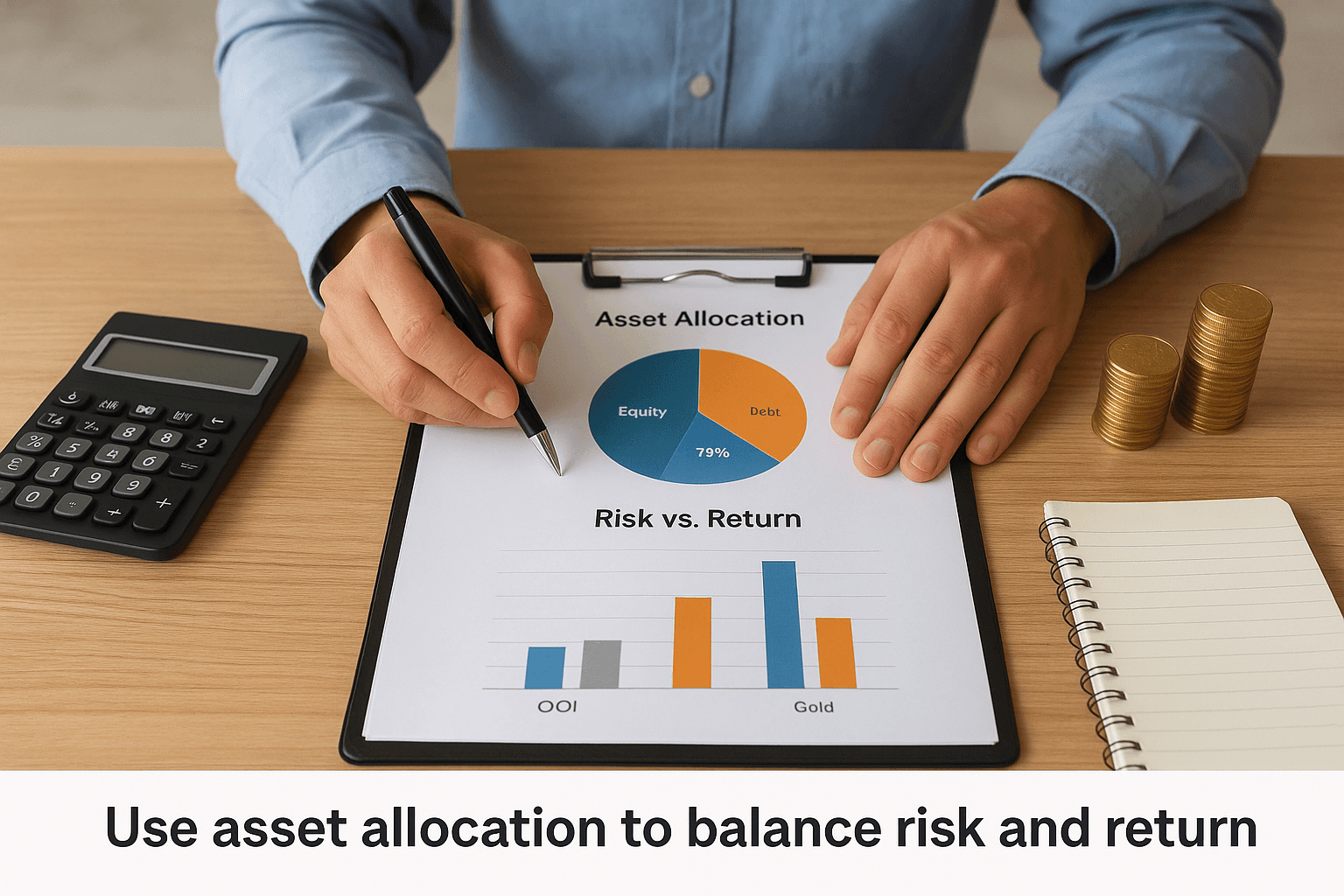

Use asset allocation to balance risk and return

Your asset allocation determines what percentage of your portfolio sits in equity versus debt versus gold, creating the risk-return balance that matches your goals and comfort level. A 30-year-old aiming for retirement might hold 70% equity and 30% debt, while someone 5 years from retirement shifts toward 40% equity and 60% debt to protect accumulated wealth. Rebalance annually by selling winners and buying laggards to maintain your target allocation, which forces you to sell high and buy low systematically.

Asset allocation matters more than individual fund selection in determining your long-term returns.

Avoid common mistakes like chasing hot tips

Resist the urge to buy last year's best-performing fund because past performance rarely repeats and you often buy at peak valuations right before corrections hit. Stay away from unregulated investment schemes promising guaranteed returns above 12% since legitimate investments carry risk disclosures and SEBI registration requirements that protect you. Focus on building a portfolio through Invsify's AI-powered recommendations based on your complete financial picture rather than random product picks from social media influencers who earn commissions pushing specific funds.

5. Create a simple invest and review system

Consistency beats timing when building wealth from your salary. Most salaried Indians fail at investing not because they pick wrong products but because they invest irregularly and check portfolios obsessively during market swings. A simple system removes emotion from the equation and ensures you invest every month without thinking, then review only when it actually matters.

Automate investing around your salary date

Set up SIP dates 2 to 3 days after your salary hits your account so money flows into investments before daily expenses consume it. Invsify's platform lets you automate investments across multiple funds simultaneously, eliminating the manual work of logging in each month to place orders. This automation ensures you never miss an investment month regardless of how busy life gets, and you benefit from rupee cost averaging by buying more units when markets fall and fewer when markets rise.

Review and rebalance on a fixed schedule

Check your portfolio once every quarter or twice a year instead of daily, focusing on whether your asset allocation matches your target percentages. Markets move constantly, but rebalancing too frequently generates unnecessary costs and tax implications that eat into returns. Use Invsify's advanced portfolio tracking to spot when any asset class drifts more than 5% from target, then sell the overweight category and buy the underweight one to restore balance.

Smart investment decisions succeed through disciplined execution, not constant tinkering with your strategy.

Decide when to change course and when to stay put

Change your investment plan only when life events alter your goals or risk capacity, such as marriage, childbirth, job changes, or major salary increases. Stay put through market volatility, election results, or news headlines that trigger panic but do not change your personal financial situation. Trust the system you built and let time do the heavy lifting.

Next steps

You now have a clear roadmap to make smart investment decisions that work with your salary cycle and life goals. Start by securing conflict-free advice through a platform that puts your interests first, then define specific goals with timelines and monthly investment amounts. Build your safety net with emergency funds and basic insurance before putting serious money into markets, and construct a diversified portfolio that matches different products to different time horizons. Finally, automate your investing around salary dates and review only when it actually matters, not when headlines scream panic.

The difference between wishing for wealth and actually building it lies in taking the first step today. Stop letting confusion or conflicting advice keep your money sitting idle in a savings account earning 3% while inflation eats 6%. Create your free Invsify account and complete the risk profiling in under 5 minutes to get your first AI-powered investment recommendations tailored to your exact financial situation. Your future self will thank you for starting now.