Standard Deduction For Salaried Employees: Limits & Rules

Shlok Sobti

Standard Deduction For Salaried Employees: Limits & Rules

Every rupee counts when it comes to reducing your tax liability. For salaried employees in India, the standard deduction for salaried employees is one of the simplest ways to lower taxable income, no receipts required, no complicated paperwork, just a flat deduction applied directly to your salary.

Here's the catch: the deduction amount varies depending on your chosen tax regime. Under the old regime, you get ₹50,000, while the new regime now offers ₹75,000 following Budget 2024. This difference might seem small on paper, but it directly affects how much tax leaves your pocket each year.

This guide covers everything you need to know about Section 16(ia), who qualifies, how the deduction applies under both regimes, and what it means for your overall tax planning. At Invsify, we help salaried professionals in India optimize their wealth through AI-powered insights and conflict-free advice. Understanding deductions like this one is a fundamental step toward keeping more of what you earn.

What standard deduction means in India

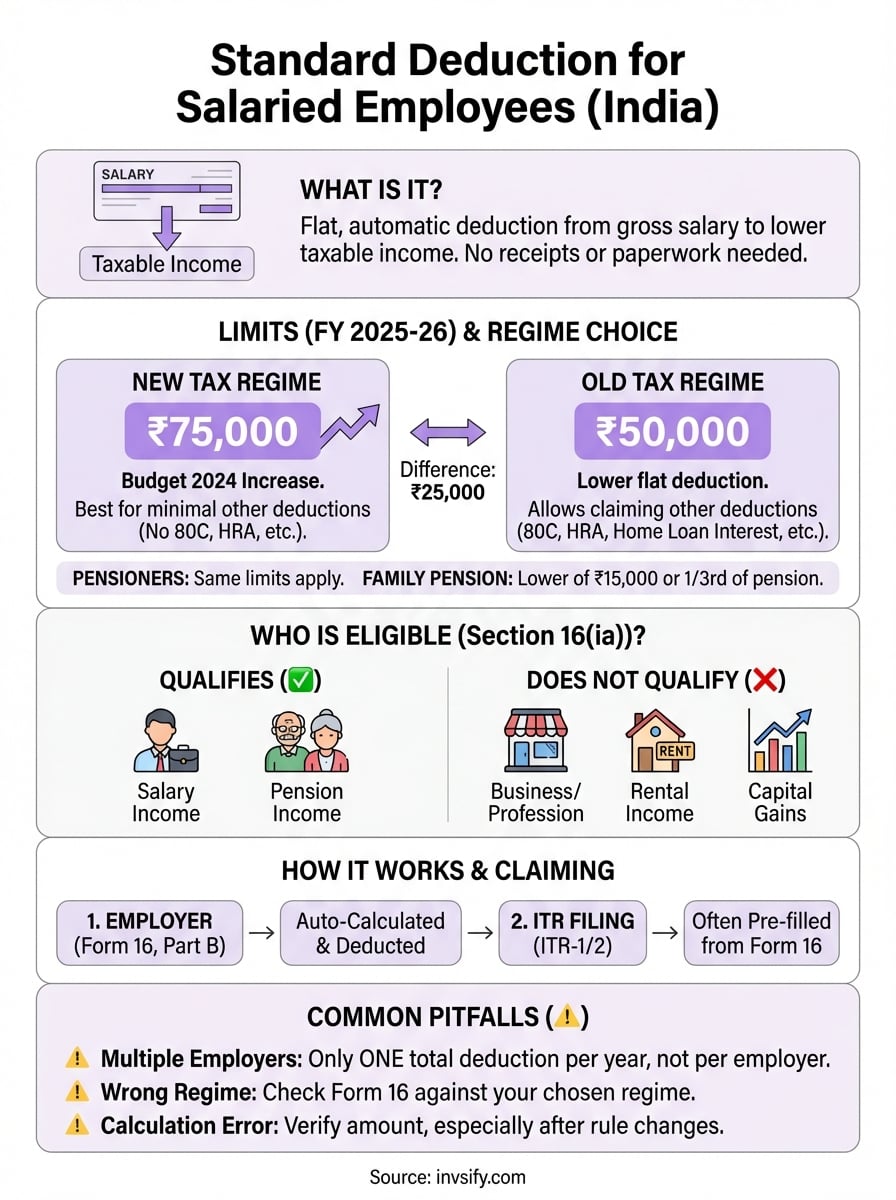

The standard deduction for salaried employees is a fixed amount the Income Tax Department allows you to subtract from your gross salary before calculating tax. You don't need to submit rent receipts, medical bills, or investment proofs to claim it. The government introduced this deduction in Budget 2018, replacing the earlier transport and medical allowance system that required documentation.

The basic concept explained

Think of standard deduction as a baseline discount the tax system offers every salaried person. Your employer automatically applies this deduction when calculating your taxable income each month. If you earn ₹8,00,000 annually under the new regime, the system subtracts ₹75,000 upfront, so you only pay tax on ₹7,25,000.

This mechanism differs completely from itemized deductions where you prove each expense. Standard deduction operates on the assumption that every salaried employee incurs basic work-related costs like commuting, clothing for office, or maintaining professional tools. Instead of tracking these small expenses, the tax code provides a uniform benefit to simplify compliance.

The standard deduction acknowledges that earning a salary comes with unavoidable costs, even if you never file a single receipt.

How it differs from other deductions

Section 80C investments, HRA claims, and LTA benefits all require documentation and have specific qualifying conditions. Standard deduction stands apart because it applies universally to your salary income without any proof of expenditure. You cannot lose this deduction by failing to invest in tax-saving instruments or by living in your own house instead of renting.

Other deductions also have variable limits based on your choices. You might claim ₹1,50,000 under Section 80C one year and nothing the next, depending on your investments. Standard deduction remains constant regardless of your financial decisions throughout the year. This predictability helps you estimate your tax liability more accurately when planning your finances.

The standard deduction also differs in timing. Your employer factors it into every salary payment, reducing your monthly TDS automatically. Deductions like Section 80C often require you to submit proof at year-end, which means you might overpay tax initially and get a refund later when filing your ITR.

Real impact on your paycheck

For someone in the 30% tax bracket, a ₹75,000 standard deduction saves ₹23,400 in taxes annually (plus applicable cess). That's ₹1,950 extra in your pocket every month without lifting a finger. Lower tax brackets see proportional savings, but the benefit remains significant.

Your Form 16 shows this deduction as a separate line item under "Income chargeable under the head 'Salaries'." Employers must account for it when computing your net taxable salary for TDS purposes. If they miss it, you're paying excess tax throughout the year, which you'll only recover after filing your return.

Standard deduction also affects your take-home calculation indirectly. Since it reduces taxable income, it can push you into a lower tax slab if you're near a threshold. Someone earning ₹7,60,000 in the new regime pays tax partly at 15% for income above ₹7,00,000. The ₹75,000 deduction brings taxable income to ₹6,85,000, keeping you fully within the 10% slab instead.

Standard deduction limits for FY 2025-26

Budget 2024 raised the standard deduction for salaried employees to ₹75,000 for the new tax regime, while the old regime continues at ₹50,000. This split creates a direct financial difference of ₹25,000 in deductible income, which translates to varying tax savings depending on your slab. Understanding which limit applies to your situation determines how much taxable income you can shield right at the source.

The government structured these limits to make the new regime more attractive without completely abandoning taxpayers who prefer itemized deductions. Your chosen regime affects not just the standard deduction but your entire tax calculation strategy. Let's break down exactly what you can claim in FY 2025-26 based on your tax regime selection.

New regime deduction amount

You get ₹75,000 as standard deduction under the new tax regime for FY 2025-26. This increase from the previous ₹50,000 came into effect from April 1, 2024, making it applicable to your entire current financial year. The government positioned this hike as compensation for giving up other deductions like Section 80C, HRA, and interest on home loans that the new regime doesn't allow.

For someone earning ₹10,00,000 annually, this ₹75,000 deduction brings your taxable salary down to ₹9,25,000 before applying slab rates. If you fall in the 20% tax bracket, you save ₹15,000 in taxes purely from this deduction. Higher earners in the 30% bracket save ₹22,500, making it a meaningful reduction regardless of income level.

Old regime deduction amount

The old tax regime maintains the ₹50,000 standard deduction that's been in place since Budget 2019. This lower amount remains constant because the old regime compensates through multiple other deductions you can stack on top. You can still claim Section 80C investments, HRA exemption, LTA, and various other benefits that significantly reduce taxable income beyond what standard deduction alone provides.

Calculate carefully before assuming the higher standard deduction makes the new regime better. Someone claiming ₹1,50,000 under Section 80C, ₹2,00,000 HRA exemption, and ₹2,00,000 home loan interest in the old regime gets far more total deductions than the extra ₹25,000 standard deduction the new regime offers.

The regime with the lower standard deduction often delivers better tax outcomes when you actively use investment-linked deductions.

Pensioners and family pension rules

Pensioners receive the same ₹75,000 or ₹50,000 standard deduction depending on their chosen tax regime, treating pension income like salary for this purpose. Family pension recipients, however, get only ₹15,000 or one-third of the pension amount, whichever is lower. This reduced benefit reflects the different nature of family pension as survivor income rather than earned salary.

Your pension-paying authority applies this deduction automatically when calculating monthly TDS. Family pension cases require more attention since banks or other paying entities might not always apply the correct deduction rate without proper documentation.

Why the standard deduction matters

The standard deduction for salaried employees creates a guaranteed reduction in your tax liability that requires zero documentation, zero compliance burden, and zero risk of rejection. This matters because every other tax benefit comes with strings attached: investment lock-ins, spending proofs, or eligibility conditions you might not meet every year. Standard deduction shows up automatically on your Form 16, reducing your taxable income from day one of the financial year without asking you to do anything.

Most salaried professionals underestimate how this single deduction shapes their entire tax planning approach. You can build your investment strategy around it because you know exactly how much base relief you're getting before considering any other tax-saving moves. Understanding its role helps you decide whether maximizing Section 80C makes sense or if the new regime's higher standard deduction delivers better results for your situation.

Direct tax savings without effort

Your employer calculates this deduction while processing your monthly salary, which means lower TDS throughout the year rather than waiting for a refund after filing your ITR. Someone earning ₹60,000 monthly sees this benefit reflected in every paycheck, not just at year-end. This automatic application prevents you from accidentally overpaying tax because you forgot to claim a deduction.

Traditional deductions demand active participation: buying insurance, opening fixed deposits, or submitting rent agreements. Standard deduction works passively in the background, making it the only tax benefit you literally cannot mess up. You don't need financial literacy, accounting knowledge, or investment discipline to benefit from it.

Standard deduction is the one tax break that helps you whether you're a tax planning expert or someone who ignores finances completely.

Planning certainty for your finances

Knowing you have ₹75,000 or ₹50,000 shielded from tax lets you calculate your exact take-home before the financial year even starts. This predictability helps when negotiating salary packages, planning EMI commitments, or deciding how much you can comfortably spend monthly. Variable deductions like HRA depend on your actual rent payments, which might change if you relocate or renegotiate lease terms.

Your standard deduction stays constant regardless of market conditions, personal circumstances, or policy changes mid-year. This stability becomes crucial when you're comparing job offers or evaluating whether a salary hike actually improves your post-tax income.

Protection against inflation and rising costs

Work-related expenses keep increasing: commuting costs rise with fuel prices, professional clothing gets more expensive, and maintaining work-from-home setups adds new financial burdens every year. The government increased the new regime's standard deduction from ₹50,000 to ₹75,000 partly to acknowledge these escalating costs without forcing you to itemize petty expenses.

This deduction recognizes that earning a salary inherently costs you money, whether through daily transportation, professional attire, or the basic infrastructure needed to perform your job. The fixed amount saves you from the impossible task of tracking every rupee spent on work-related necessities throughout the year.

Section 16(ia) rules and who can claim it

Section 16(ia) of the Income Tax Act governs the standard deduction for salaried employees and specifies exactly who can benefit from it. The provision states that any individual receiving salary income or pension qualifies for this deduction, subject to the limits set by your chosen tax regime. Your eligibility depends entirely on the nature of your income, not your employer type, salary amount, or job role. Government employees, private sector workers, and pensioners all fall under the same rules without discrimination.

The law treats this deduction as a basic right for anyone earning through employment rather than a discretionary benefit requiring approval. You don't need your employer's permission or special authorization to claim it. The deduction applies automatically to your gross salary before calculating taxable income, making it a universal feature of salary taxation rather than an optional claim.

Who qualifies under Section 16(ia)

You qualify if you receive salary or pension income during the financial year, regardless of whether you work full-time, part-time, or hold multiple jobs simultaneously. Contractual employees on company payroll, consultants receiving salary with TDS deducted, and even employees working from home all get the same standard deduction rights. Your work arrangement doesn't matter as long as your income falls under the "Income from Salaries" head in tax calculations.

Directors drawing salaries from their companies qualify because the Income Tax Act treats director remuneration as salary income. Retired employees receiving pension also claim this deduction since Section 16(ia) explicitly includes pension alongside salary in its scope. Family pension recipients get a different, lower deduction limit as mentioned earlier, but they still fall under Section 16(ia) coverage.

Section 16(ia) draws the line at how you receive income, not how much you earn or who pays you.

Income types that don't qualify

Freelancers, consultants operating as independent contractors, and business owners cannot claim this deduction because their earnings fall under "Profits and Gains of Business or Profession" instead of salary income. The distinction matters: if you receive a professional fee invoice rather than a salary slip, you're outside Section 16(ia) scope even if the work looks identical to employment.

Rental income, capital gains, and interest earnings similarly don't qualify since these income heads have their own deduction rules. You might earn crores from property or investments, but without salary income, Section 16(ia) offers you nothing. This limitation reinforces that standard deduction specifically targets employment-related costs, not general wealth management expenses.

Conditions and restrictions

No minimum salary threshold exists for claiming this deduction. Someone earning ₹2,00,000 annually gets the full ₹75,000 deduction under the new regime, even though it wipes out 37.5% of their gross income. The tax system doesn't penalize low earners or restrict benefits based on income adequacy tests common in other countries.

You cannot split or transfer your standard deduction to family members or claim it multiple times across different income sources. Each individual gets one deduction per financial year, calculated once against total salary income. If you switch jobs mid-year, both employers apply the deduction proportionally, but your total benefit never exceeds the annual limit of ₹75,000 or ₹50,000 depending on your regime choice.

How to claim standard deduction in Form 16 and ITR

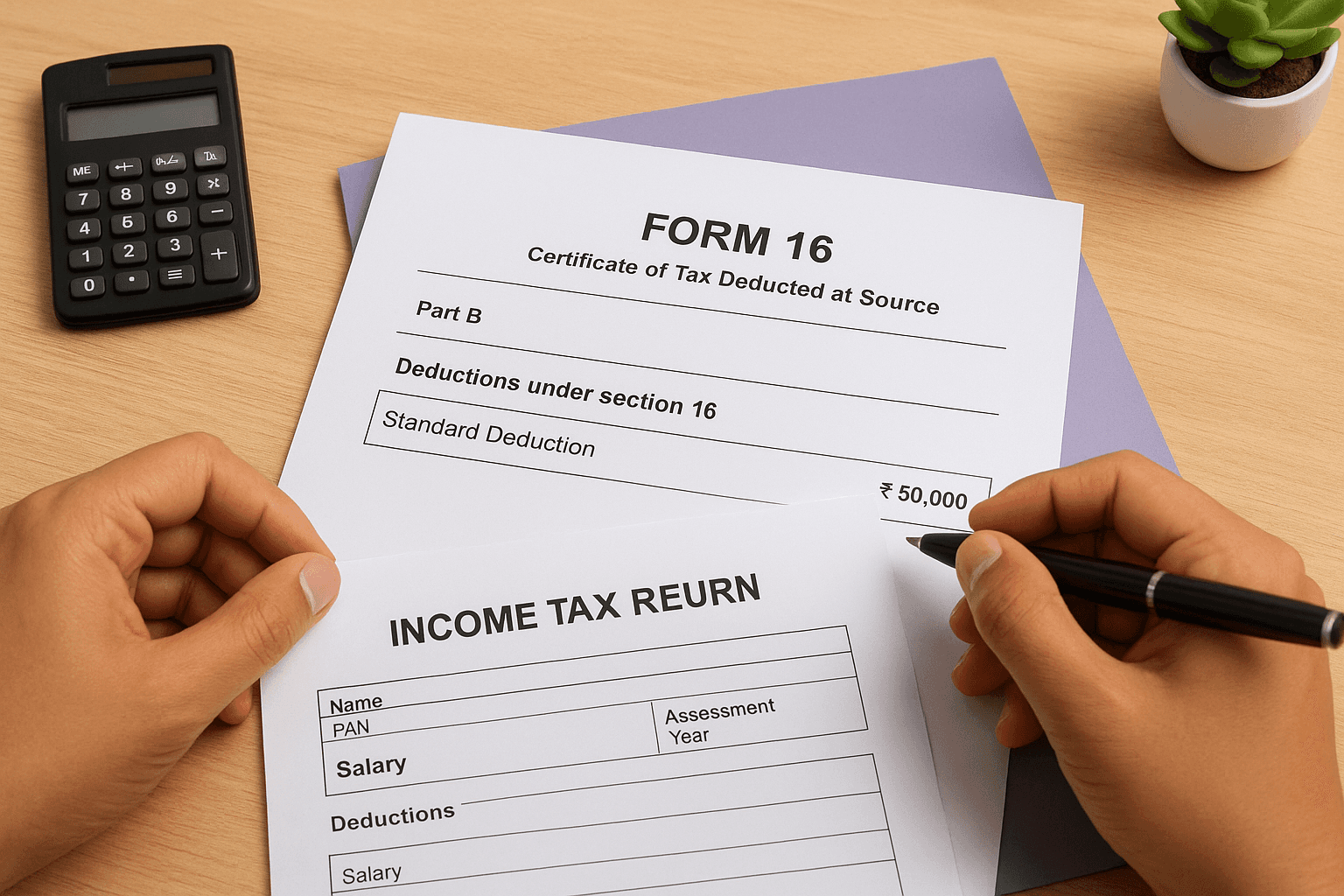

The standard deduction for salaried employees appears on your Form 16 automatically, which means you rarely need to take manual action to claim it. Your employer calculates this deduction when preparing your salary income statement and reflects it in Part B of Form 16 under "Deductions under section 16." This automatic inclusion eliminates the documentation headaches that come with claiming other tax benefits, making standard deduction one of the simplest tax breaks you'll ever receive.

Your ITR filing process remains straightforward because the deduction transfers directly from Form 16 to your tax return. Most salaried employees use ITR-1 or ITR-2, both of which have dedicated fields for standard deduction that auto-populate when you import data from Form 26AS or the Annual Information Statement (AIS). Understanding how this process works helps you verify that you're getting the full benefit without overpaying tax or triggering unnecessary scrutiny from the Income Tax Department.

What Form 16 shows automatically

Your Form 16 Part B lists standard deduction as a separate line item under allowances and deductions, typically showing ₹75,000 for new regime taxpayers or ₹50,000 for old regime followers. This amount gets subtracted from your gross salary to arrive at income chargeable under the head salaries. You'll find this section right after your employer lists basic salary, allowances, and perquisites but before applying other deductions like professional tax.

Check this figure carefully when you receive Form 16 in June after the financial year ends. Some employers make calculation errors or apply outdated limits if their payroll software hasn't updated to reflect Budget 2024 changes. Spotting a ₹50,000 deduction when you opted for the new regime means you've been paying excess TDS all year.

If your Form 16 shows the wrong standard deduction amount, you'll need to file your ITR with the correct figure and claim the excess TDS as a refund.

Steps for filing ITR with standard deduction

You simply carry forward the standard deduction amount from Form 16 to your ITR without modification in most cases. When filing ITR-1 online through the income tax portal, the system automatically fills Schedule S with your salary details including standard deduction when you choose the pre-fill option. You verify the ₹75,000 or ₹50,000 figure matches your chosen tax regime and proceed with the rest of your return.

Manual filers entering data directly need to locate the "Deduction under section 16" field in their ITR form's salary income section. You input the applicable amount based on your tax regime selection made earlier in the form. The system recalculates your taxable income instantly, showing you exactly how much tax you owe after accounting for the deduction.

When manual intervention is needed

You must manually enter standard deduction if you're filing ITR without Form 16, which happens when you switch jobs and your final employer doesn't have complete salary details from your previous employer. Calculate your total annual salary from all sources, then apply the full ₹75,000 or ₹50,000 deduction once against the combined income. You cannot claim multiple deductions just because you worked at different companies during the year.

Pensioners sometimes need to add standard deduction manually if their pension-disbursing authority fails to issue a proper Form 16. Banks paying family pension particularly miss this detail, leaving you to claim the ₹15,000 or one-third benefit yourself while filing.

Old vs new tax regime and when each wins

Choosing between the old and new tax regime determines not just your standard deduction for salaried employees amount, but your entire tax liability for the year. The new regime offers ₹75,000 standard deduction plus lower tax slab rates, while the old regime sticks with ₹50,000 but allows you to claim multiple investment-linked deductions on top. Your optimal choice depends on how many traditional tax-saving instruments you actively use, making this decision highly personal rather than universally favorable to either side.

Most salaried professionals rush this decision during salary declaration season without calculating their actual tax under both scenarios. You need to run the numbers with your real income, actual HRA payments, existing investments, and home loan interest before committing to a regime. The government lets you switch between regimes annually if you have only salary income, so your choice isn't permanent, but getting it right from the start saves you from paying excess TDS throughout the year.

When the new regime wins

You benefit more from the new regime when you have minimal investments in Section 80C instruments like PPF, ELSS, or life insurance premiums. Someone earning ₹8,00,000 with no home loan, no significant insurance policies, and living with parents who don't charge rent saves more under the new regime because the ₹75,000 standard deduction plus lower slab rates beat the old regime's ₹50,000 deduction alone.

Young professionals early in their careers often find the new regime advantageous because they haven't accumulated assets that generate tax deductions. You avoid the pressure of locking money into tax-saving investments just to meet Section 80C limits, freeing up liquidity for emergency funds or near-term goals instead.

The new regime rewards you for financial simplicity, making it ideal when your tax planning stops at standard deduction.

When the old regime wins

The old regime delivers better outcomes when you're already maxing out Section 80C (₹1,50,000), paying significant rent that qualifies for HRA exemption, or servicing a home loan with substantial interest payments. Someone claiming ₹2,00,000 HRA, ₹1,50,000 in 80C investments, and ₹2,00,000 home loan interest gets ₹5,50,000 in total deductions under the old regime, far exceeding what the new regime's extra ₹25,000 standard deduction and slightly lower rates provide.

Homeowners with large mortgages particularly favor the old regime because home loan interest deductions (up to ₹2,00,000 for self-occupied property) disappear completely under the new regime. Calculate whether your interest payments alone justify staying in the old regime before switching.

Quick comparison framework

Your break-even analysis needs actual numbers from your financial life. List every deduction you currently claim: 80C investments, HRA, home loan interest, 80D medical insurance premiums, and NPS contributions under 80CCD(1B). Add these up and compare against the ₹25,000 extra standard deduction plus marginal rate benefits the new regime offers. When your old regime deductions exceed ₹3,00,000, you almost always save more by staying there.

Tricky situations and common mistakes

The standard deduction for salaried employees causes confusion when your income situation deviates from a simple single-employer setup throughout the year. You might work at multiple companies, switch jobs mid-year, or discover your employer applied the wrong tax regime to your salary calculations. These scenarios create tax complications that require manual intervention during ITR filing, and missing these details costs you money either through excess tax payments or penalties for incorrect returns.

Most errors happen because you assume your employer handles everything perfectly or because you blindly accept Form 16 figures without verification. Understanding where mistakes commonly occur helps you spot problems before filing your return and saves you from dealing with Income Tax Department notices months later demanding explanations for discrepancies.

Multiple employers and mid-year job changes

You get only one standard deduction per financial year, regardless of how many employers paid you during that period. Your problem arises because each employer applies the deduction independently without knowing about your other income sources. If you worked at two companies and both deducted ₹75,000 from your salary, your combined Form 16s show ₹1,50,000 in standard deduction, which exceeds your legal limit by ₹75,000.

Manually correct this when filing your ITR by claiming only ₹75,000 total standard deduction against your combined salary from all sources. You'll owe additional tax on the excess ₹75,000 that shouldn't have been deducted, so prepare to pay this amount when filing rather than expecting a refund. Failure to correct this error triggers automated system notices from the Income Tax Department after processing your return.

Multiple Form 16s don't multiply your standard deduction, you still get just one fixed amount per year no matter how many jobs you held.

Employer applies wrong regime without consent

Some employers default everyone to the new regime without explicitly asking your preference, which becomes a problem when you have significant 80C investments or HRA claims that make the old regime better for your situation. You discover this mistake only when reviewing Form 16 and finding you've paid higher TDS all year because the employer calculated tax using the wrong regime's rates and deduction limits.

Contact your HR department immediately if you catch this error before year-end to switch regimes for remaining months. After the financial year closes, you must file your ITR under your preferred regime and claim refund for excess TDS paid throughout the year.

Form 16 calculation errors you must verify

Employers sometimes apply outdated standard deduction amounts, particularly if their payroll software didn't update after Budget 2024 raised the new regime deduction to ₹75,000. You might see ₹50,000 deducted when you should get ₹75,000, resulting in excess TDS of several thousand rupees depending on your tax bracket.

Cross-check your Form 16's standard deduction figure against your chosen regime before filing ITR. Manually override incorrect amounts in your return and provide correct calculations in the appropriate fields to claim your full entitled deduction.

Key takeaways and next steps

The standard deduction for salaried employees reduces your taxable income by ₹75,000 or ₹50,000 depending on your tax regime choice, and you don't need a single receipt to claim it. Your employer applies this deduction automatically through Form 16, but you must verify the amount matches your regime selection to avoid paying excess tax throughout the year. Section 16(ia) covers everyone receiving salary or pension income without minimum thresholds or complex eligibility tests.

Calculate your tax under both regimes before deciding which one saves you more money. The new regime's higher deduction suits you when you have minimal investments, while the old regime wins when you max out Section 80C, HRA, and home loan interest deductions that exceed what the extra ₹25,000 standard deduction offers. Review your Form 16 carefully every June for calculation errors, especially if you switched jobs or worked at multiple companies during the year.

Smart tax planning starts with understanding deductions like this one, but optimizing your entire financial strategy requires looking at your complete picture. Get personalized wealth advice from Invsify to identify tax-saving opportunities tailored to your salary structure and life goals.