Tax Efficient Investment Strategies in India: Reduce Taxes

Shlok Sobti

Tax Efficient Investment Strategies in India: Reduce Taxes

You work hard for your money and invest diligently to build wealth. But here's the harsh reality taxes can silently eat up a significant chunk of your investment returns each year. Many Indian investors focus solely on picking the right stocks or mutual funds while ignoring how much the Income Tax Department takes from their gains. That oversight can cost you lakhs over time.

Tax efficient investment strategies help you legally minimize your tax burden while maximizing returns. By choosing the right accounts, timing your transactions wisely, and placing your investments strategically, you can keep more of what you earn. These strategies work within India's tax framework using deductions, exemptions, and preferential tax rates.

This guide walks you through practical steps to invest tax efficiently in India. You'll learn how Indian tax slabs affect your investments, which accounts offer the best tax benefits, and how to structure your portfolio to reduce your annual tax bill. We'll also cover specific tactics like asset location and capital gains planning that work for salaried individuals managing their own wealth.

What is tax efficient investing in India

Tax efficient investing means structuring your investments to minimize the taxes you pay on returns while staying fully compliant with Indian tax laws. You achieve this by choosing the right investment vehicles, timing your buy and sell decisions strategically, and utilizing available deductions and exemptions. The goal is to maximize your after-tax returns rather than just gross returns.

Core components of tax efficiency

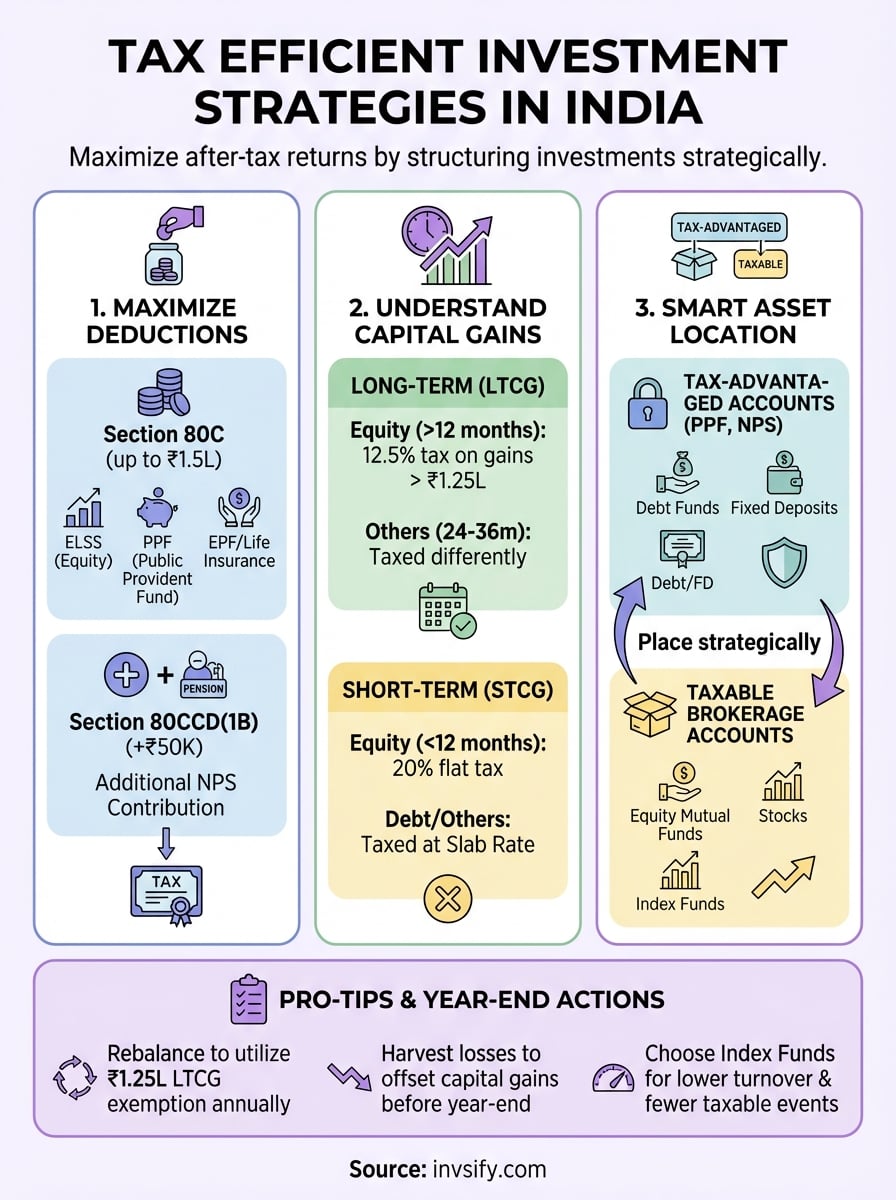

Indian tax laws offer multiple pathways to reduce your tax burden legally. Section 80C deductions allow you to claim up to ₹1.5 lakh annually through instruments like ELSS mutual funds, PPF, and life insurance premiums. Long-term capital gains (LTCG) on equity investments exceeding ₹1.25 lakh are taxed at only 12.5%, while short-term gains face much higher rates. Your investment choices directly impact how much tax you owe each year.

Tax efficient investment strategies work best when you match your investment type with the appropriate account structure and holding period.

Real impact on your wealth

Consider two investors who both earn ₹5 lakh in investment returns annually. Investor A pays ₹1.5 lakh in taxes by ignoring tax planning, while Investor B pays only ₹50,000 using tax efficient strategies. Over 20 years, this ₹1 lakh annual difference compounds to approximately ₹57 lakh (assuming 8% returns). That's real money staying in your portfolio instead of going to the tax department.

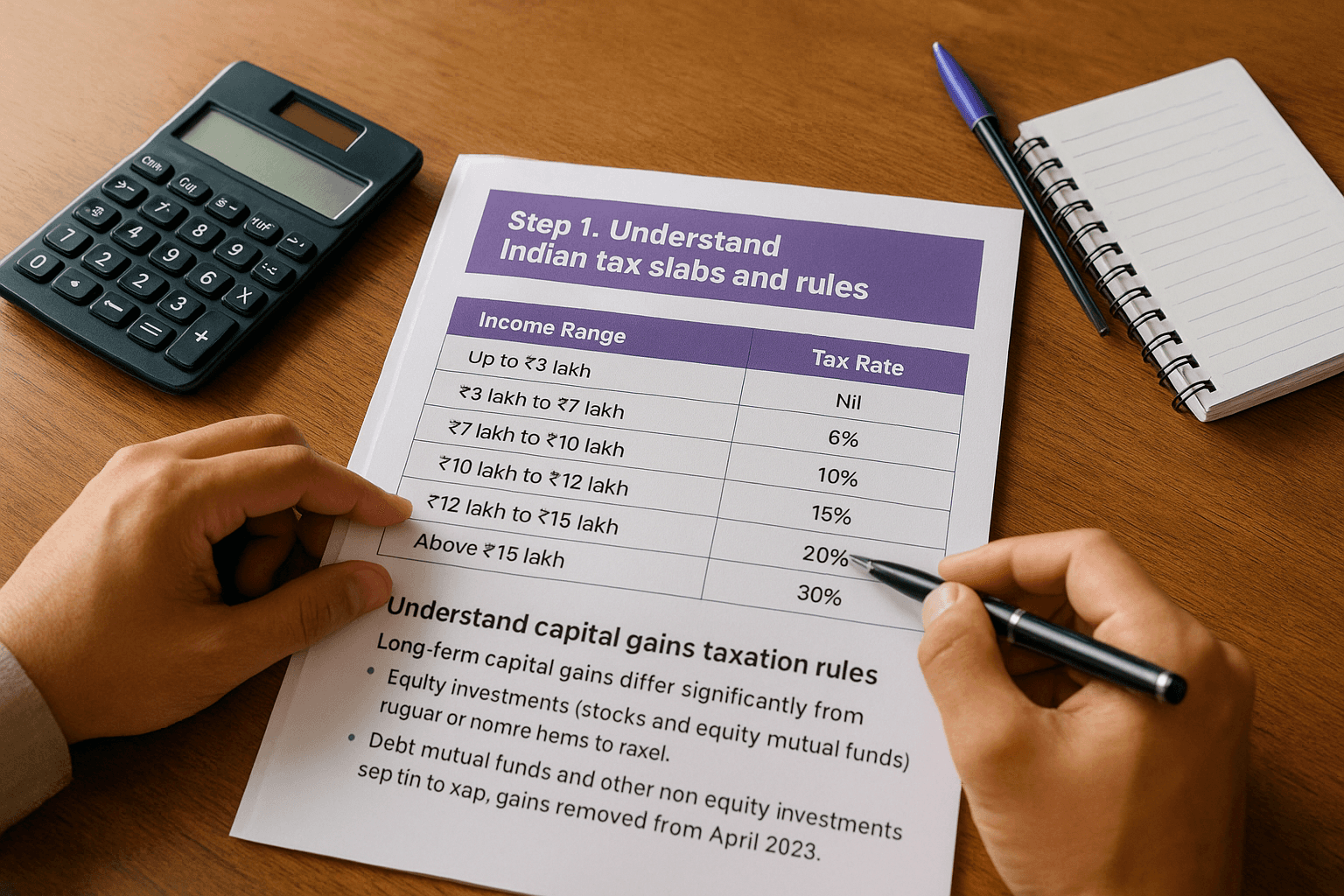

Step 1. Understand Indian tax slabs and rules

Your income tax slab determines how much you pay on interest income, short-term capital gains, and other taxable returns. Understanding these slabs helps you calculate your actual tax liability and plan your investments accordingly. The new tax regime (default from FY 2023-24) offers lower rates but removes most deductions, while the old regime allows deductions under Section 80C and other sections.

Know your applicable tax slab

India uses progressive tax slabs where higher income attracts higher tax rates. Your total taxable income (including salary, interest income, and short-term gains) falls into one of these brackets under the new regime:

Income Range | Tax Rate |

|---|---|

Up to ₹3 lakh | Nil |

₹3 lakh to ₹7 lakh | 5% |

₹7 lakh to ₹10 lakh | 10% |

₹10 lakh to ₹12 lakh | 15% |

₹12 lakh to ₹15 lakh | 20% |

Above ₹15 lakh | 30% |

Your slab dictates how interest from fixed deposits, savings accounts, and bonds gets taxed. These earnings add to your total income and face your marginal tax rate. If you fall in the 30% bracket, that bank FD earning 7% actually delivers only 4.9% after tax.

Tax efficient investment strategies start with knowing exactly which slab you fall into and what that means for different investment types.

Understand capital gains taxation rules

Capital gains rules differ significantly from regular income taxation. Equity investments (stocks and equity mutual funds) held for more than 12 months qualify as long-term, taxed at 12.5% on gains exceeding ₹1.25 lakh annually. Selling before 12 months makes your gains short-term, taxed at a flat 20% regardless of your income slab.

Debt mutual funds and other non-equity investments follow different timelines. You need to hold these for 36 months to qualify for long-term status. Long-term gains on debt funds now face taxation at your slab rate with indexation benefits removed from April 2023. Short-term debt fund gains also get taxed at your slab rate, making the holding period less relevant for debt investments.

Gold, real estate, and international equity funds require 24 months of holding for long-term treatment. Physical gold and property enjoy indexation benefits on long-term gains, while debt funds lost this advantage recently. Understanding these specific timelines helps you plan when to sell and which investment types suit your tax situation best.

Step 2. Use tax saving accounts and deductions

India's tax code gives you multiple deduction opportunities that directly reduce your taxable income. These deductions work best when you combine them strategically rather than treating them as isolated choices. Start by maximizing Section 80C deductions first, then layer additional benefits through other sections to build comprehensive tax savings.

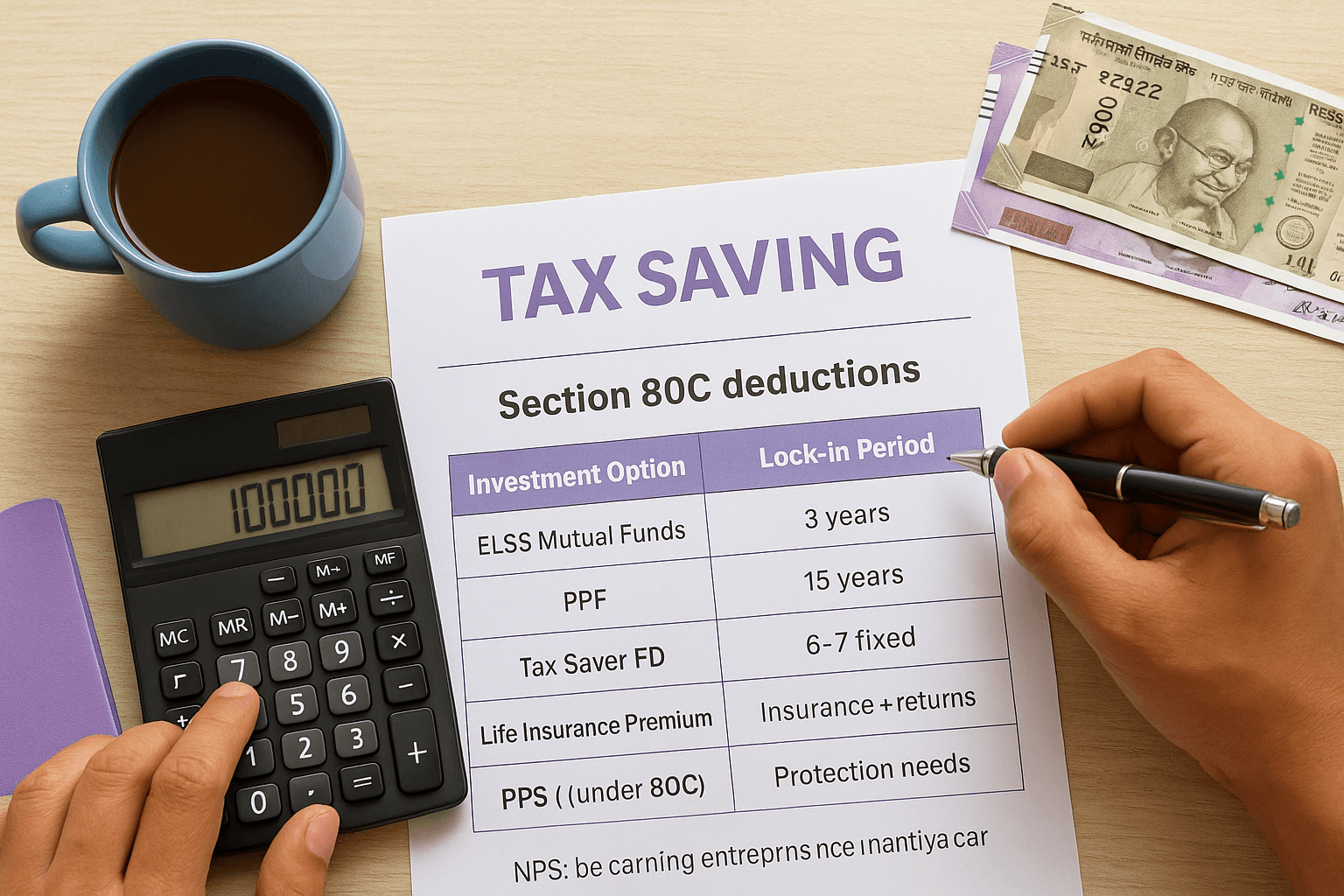

Maximize Section 80C deductions strategically

Section 80C allows you to claim up to ₹1.5 lakh annually in deductions through specific investment instruments. ELSS (Equity Linked Savings Scheme) mutual funds stand out as the most tax efficient investment strategies under this section because they offer dual benefits: tax deduction on investment plus potential for equity returns. These funds require only a 3-year lock-in period, the shortest among 80C options, and long-term capital gains above ₹1.25 lakh face just 12.5% tax.

Investment Option | Lock-in Period | Returns Type | Best For |

|---|---|---|---|

ELSS Mutual Funds | 3 years | Market-linked equity | Growth seekers |

PPF | 15 years | 7.1% fixed (current) | Risk-averse, long-term |

Tax Saver FD | 5 years | 6-7% fixed | Conservative investors |

Life Insurance Premium | Policy term | Insurance + returns | Protection needs |

NPS (under 80C) | Till retirement | Market-linked | Retirement planning |

The key to Section 80C efficiency is choosing instruments that match your financial timeline while maximizing post-tax returns.

Your actual benefit depends on your tax slab. Someone in the 30% bracket saves ₹46,800 in taxes (including cess) by investing the full ₹1.5 lakh under 80C. Calculate your savings by multiplying ₹1.5 lakh by your marginal tax rate plus 4% cess.

Claim additional NPS deductions

Beyond Section 80C, you can claim an extra ₹50,000 deduction specifically for National Pension System (NPS) contributions under Section 80CCD(1B). This benefit works independently of your 80C limit, giving you total deductions of ₹2 lakh annually when combined. NPS offers market-linked returns through equity, corporate bonds, and government securities, with mandatory annuitization at retirement.

Employer contributions to NPS provide another advantage under Section 80CCD(2), allowing deductions up to 10% of basic salary (14% for government employees) without any upper limit. These employer contributions don't count against your 80C or 80CCD(1B) limits, creating a third layer of tax benefits.

Use tax-free instruments for interest income

Certain government-backed instruments deliver completely tax-free returns that don't count toward your taxable income at all. The Public Provident Fund (PPF) offers tax-free interest currently at 7.1% annually, with contributions qualifying for 80C deductions and maturity proceeds exempt from tax. This triple tax exemption (EEE status) makes PPF attractive despite its 15-year lock-in.

Sukanya Samriddhi Yojana provides similar EEE benefits specifically for parents with daughters below 10 years, offering higher interest rates (currently 8.2%). Your interest earnings compound tax-free over the 21-year tenure, and the maturity amount faces no tax. Senior citizens above 60 can claim ₹50,000 annual deduction on interest from savings accounts under Section 80TTB, beyond the standard ₹10,000 deduction available to all taxpayers under Section 80TTA.

Step 3. Build a tax smart investment portfolio

Your portfolio structure matters as much as your individual investment choices when it comes to tax efficiency. The same investment can produce different after-tax returns depending on where you hold it and how you balance your overall allocation. Tax efficient investment strategies require matching each asset type with the account that minimizes its tax burden while maintaining your desired risk profile.

Place investments in the right accounts

Asset location forms the foundation of tax efficient portfolio construction. You want to hold tax-inefficient assets in tax-advantaged accounts and tax-efficient assets in regular taxable accounts. Fixed deposits, debt mutual funds, and bonds generate regular interest income taxed at your slab rate, so these belong inside your PPF, NPS, or EPF where growth happens tax-deferred or tax-free.

Equity mutual funds and direct stocks work better in taxable brokerage accounts because they already enjoy preferential long-term capital gains treatment at 12.5%. Keeping them outside retirement accounts preserves your tax-advantaged space for assets that genuinely need protection from annual taxation. This placement strategy alone can save you ₹50,000 to ₹1 lakh annually depending on your portfolio size.

Match each asset type with the account structure that minimizes its specific tax burden rather than randomly spreading investments across accounts.

Choose tax efficient funds and instruments

Index funds and passive ETFs create fewer taxable events than actively managed funds because they trade less frequently. Lower portfolio turnover means fewer capital gains distributions that trigger tax obligations during the year. When comparing two equity funds with similar returns, pick the one with turnover below 30% to reduce unnecessary tax friction.

Dividend-paying stocks and funds generate taxable income annually regardless of whether you sell, while growth-oriented investments defer taxes until you exit. For taxable accounts, favor growth stocks and accumulation plan mutual funds that reinvest rather than distribute earnings. Save dividend-focused investments for your retirement accounts where that annual income won't immediately hit your tax bill.

Balance equity and debt for tax optimization

Your ideal equity-debt split should factor in both risk tolerance and tax efficiency. Equity allocations naturally favor long-term holding periods, aligning perfectly with the 12.5% LTCG rate after 12 months. Structure your equity portion to include 60-70% diversified equity funds you won't touch for 5+ years, allowing tax-efficient compounding.

Portfolio Component | Recommended Allocation | Primary Tax Benefit |

|---|---|---|

Equity index funds | 40-50% | Low turnover, LTCG rate |

Active equity funds | 10-20% | ELSS for 80C deduction |

Debt in tax-free instruments | 20-30% | PPF/SSY tax exemption |

Gold ETFs | 5-10% | LTCG after 24 months |

Emergency liquid funds | 10-15% | Quick access, minimal tax |

Debt investments require more careful tax planning. Instead of holding regular debt funds in taxable accounts where gains face slab-rate taxation, channel debt allocations through PPF contributions (up to ₹1.5 lakh annually) and NPS (additional ₹50,000 under 80CCD(1B)). Any remaining debt exposure can go into tax-free bonds or short-duration funds you'll hold during lower-income years.

Rebalance your portfolio by selling equity units strategically when your gains stay below the ₹1.25 lakh annual LTCG exemption threshold. This lets you book profits tax-free while maintaining your target allocation. Time these rebalancing moves near financial year-end after calculating your total capital gains to maximize the exemption benefit.

Additional tools and checklists for investors

You need practical tools to track your tax efficiency throughout the year rather than scrambling during tax season. Creating simple checklists and tracking systems helps you monitor capital gains, utilize exemptions fully, and make timely investment decisions. These tools turn complex tax efficient investment strategies into manageable monthly tasks that prevent costly mistakes.

Year-end tax planning checklist

Run through this checklist every November to optimize your tax position before the financial year ends. Verify your Section 80C investments total ₹1.5 lakh and confirm your NPS contributions reach the additional ₹50,000 limit under 80CCD(1B). Calculate your total long-term capital gains to see if you've crossed the ₹1.25 lakh exemption threshold.

Review these action items:

Total 80C contributions: ₹______ / ₹1,50,000

NPS contributions (80CCD(1B)): ₹______ / ₹50,000

Long-term capital gains booked: ₹______ / ₹1,25,000

Loss-making investments to harvest: List assets

Equity allocation above target: Rebalance needed?

Use November and December to harvest tax losses strategically while your annual gains picture becomes clear.

Capital gains tracking template

Maintain a simple spreadsheet tracking every investment sale with purchase date, sale date, holding period, and gain amount. Calculate whether each transaction qualifies as short-term or long-term based on the asset type's specific timeline. Your tracking sheet should separate equity gains (12-month threshold) from debt and gold gains (24 or 36-month thresholds) to avoid confusion about applicable tax rates.

Tie your tax plan together

You now have the framework to reduce your tax burden legally while maximizing investment returns. Your strategy combines choosing the right accounts (PPF, NPS, ELSS), timing your transactions to capture long-term capital gains treatment, and placing assets strategically across taxable and tax-advantaged spaces. These tax efficient investment strategies work together to keep more money working for you instead of going to the tax department.

Start by reviewing your current investment placement and identifying quick wins where you're paying unnecessary taxes. Move high-interest debt funds into PPF or NPS contributions, verify you've maxed out all Section 80C deductions, and check if you can harvest any losses before year-end. Small adjustments compound into significant savings over decades.

Need personalized guidance on structuring your portfolio for maximum tax efficiency? Create your free Invsify account to access AI-powered recommendations that analyze your specific tax situation and suggest optimal investment placement strategies tailored to your income slab and financial goals.