Tax Efficient Retirement Planning in India: A How-To Guide

Shlok Sobti

Tax Efficient Retirement Planning in India: A How-To Guide

You spent decades building your retirement corpus. You maxed out your PPF contributions, invested in ELSS funds, and maybe even opened an NPS account. But here's what most Indians miss: without a tax strategy, you could lose 20% to 30% of your retirement income to taxes. Your pension gets taxed as salary. Interest from fixed deposits pushes you into higher slabs. And when you turn 75, those RMDs from your PF kick in whether you need the money or not.

Smart sequencing changes everything. By choosing which accounts to tap first, timing your withdrawals strategically, and mixing taxable and tax-free income sources, you keep more of what you saved. Think of it as a withdrawal blueprint that works with India's tax structure instead of against it.

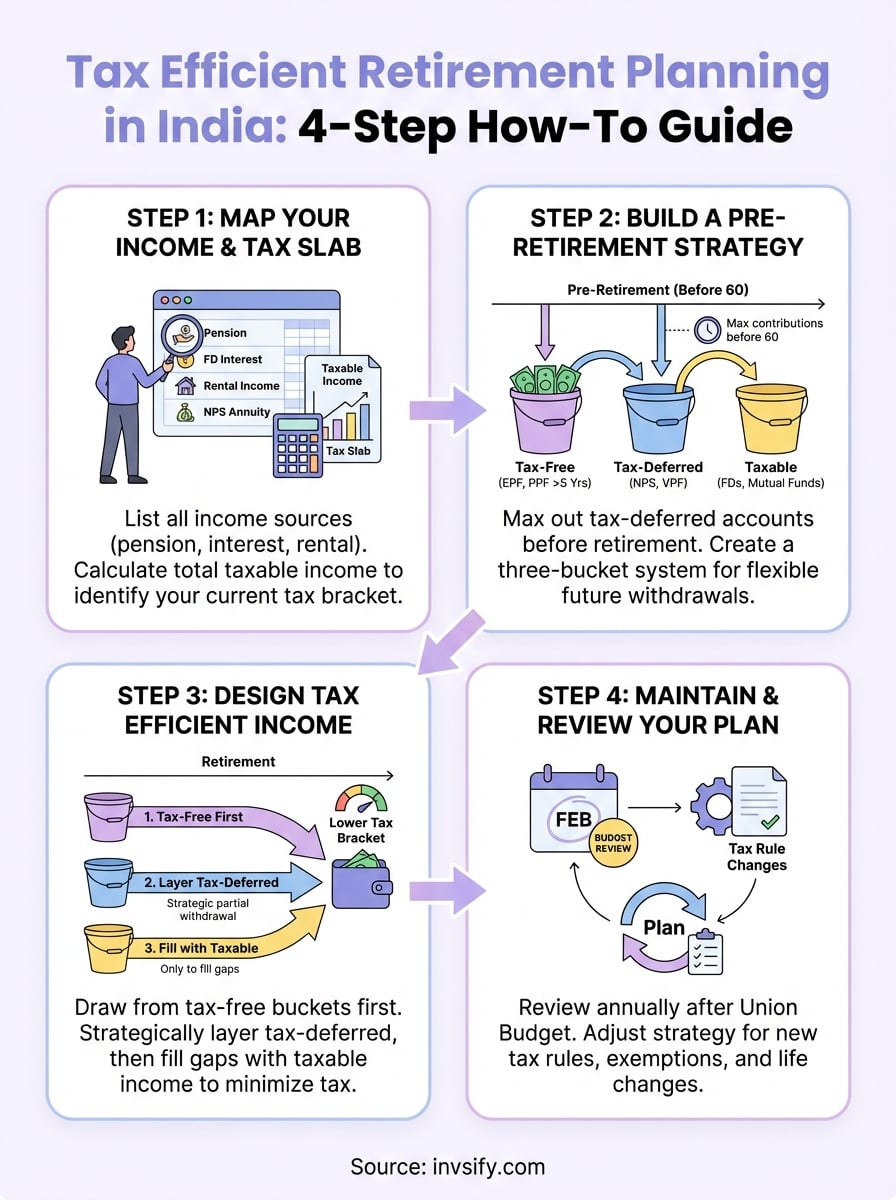

This guide walks you through four practical steps to build your tax-efficient retirement plan. You'll learn how to map your income sources and tax exposure, structure your pre-retirement investments for maximum benefit, design a withdrawal sequence that minimizes your tax bill, and adjust your strategy as rules change. No jargon. Just clear actions you can implement yourself.

Why tax efficient retirement planning matters in India

India's tax structure treats retirement income harshly. Your uncommuted pension gets taxed as salary, pulling you into the same slabs you faced while working. Fixed deposits and recurring deposits generate interest income taxed at your marginal rate, which can reach 30% for amounts above ₹10 lakh. Even your NPS withdrawals face partial taxation if you don't structure them correctly. Without tax efficient retirement planning, you hand over lakhs to the government instead of using that money for your expenses.

The compounding loss over 25 years

Consider this: if you withdraw ₹5 lakh annually from taxable sources and pay 20% in taxes, you lose ₹1 lakh every year. Over a 25-year retirement period, that's ₹25 lakh gone to taxes alone. Smart sequencing of withdrawals can cut this bill by half or more. You could redirect those savings into healthcare, travel, or leaving a larger inheritance for your family.

Poor withdrawal planning doesn't just cost you taxes this year. It locks you into higher tax slabs for decades.

Why most retirees get this wrong

Most Indians focus only on accumulation. You buy ULIPs, max out Section 80C deductions, and contribute to EPF religiously. But you never ask: which account should I tap first in retirement? Should you exhaust your PPF before touching your NPS? When should you convert part of your corpus to a Roth-style account to avoid future taxes? These sequencing decisions determine whether you keep 70% or 85% of your retirement income. The difference funds an extra decade of comfortable living or forces you to compromise on your lifestyle.

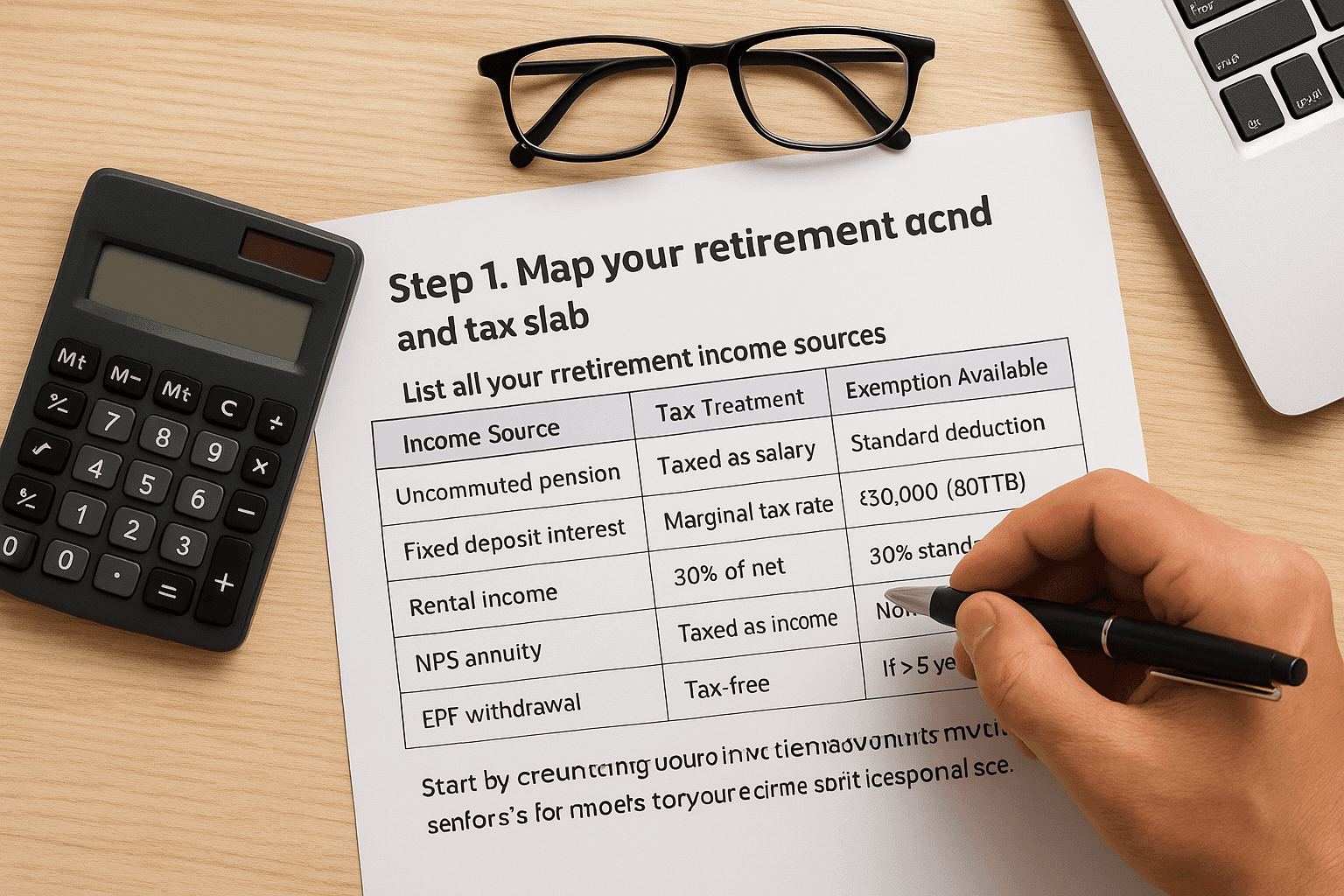

Step 1. Map your retirement income and tax slab

You cannot plan for tax efficient retirement planning without knowing exactly what money comes in and where it gets taxed. Most retirees underestimate their taxable income because they forget about interest, dividends, and rental income that stack on top of their pension. This first step forces you to see the complete picture. You will list every rupee you expect to receive and identify which portions face taxation. Only then can you make smart decisions about withdrawal sequencing.

List all your retirement income sources

Start by creating a simple income inventory. Open a spreadsheet and create four columns: source name, annual amount, tax treatment, and notes. Go through every account you own and every payment you expect to receive. Your pension falls under salary taxation rules. Interest from your fixed deposits, recurring deposits, and savings accounts counts as "income from other sources" and faces your marginal tax rate. Rental income from property gets taxed after standard deductions. EPF and PPF withdrawals might be tax-free if you meet specific conditions, but partial withdrawals before five years could trigger taxes.

Use this structure to map your income:

Income Source | Annual Amount (₹) | Tax Treatment | Exemption Available |

|---|---|---|---|

Uncommuted pension | 6,00,000 | Taxed as salary | Standard deduction |

Fixed deposit interest | 1,80,000 | Marginal tax rate | ₹50,000 (80TTB) |

Rental income | 3,60,000 | 30% of net | 30% standard |

NPS annuity | 2,40,000 | Taxed as income | None |

EPF withdrawal | 15,00,000 | Tax-free | If >5 years service |

Calculate your expected tax slab

Once you have your income list, add up all taxable amounts to find your total income. Apply the current tax slabs for senior citizens if you are 60 or above. Under the old regime, you pay zero tax up to ₹3 lakh, then 5% on ₹3 to ₹5 lakh, 20% on ₹5 to ₹10 lakh, and 30% above ₹10 lakh. The new regime offers different rates but removes most deductions you relied on during your working years.

Knowing your tax slab today tells you which withdrawal moves will push you into higher brackets tomorrow.

Take the example above. Your total taxable income reaches ₹13,80,000 (₹6,00,000 pension + ₹1,30,000 FD interest after ₹50,000 exemption + ₹2,52,000 net rental + ₹2,40,000 NPS annuity). Under the old regime, you would pay approximately ₹2,66,000 in taxes annually. That number becomes your baseline. Every withdrawal strategy you design in the next steps aims to reduce this figure by at least 20% to 30% through smart sequencing and account selection.

Step 2. Build a tax smart pre retirement strategy

The decisions you make in the five to ten years before retirement lock in your tax outcomes for decades. You cannot fix poor account allocation once you cross 60 because most tax-advantaged accounts stop accepting contributions after retirement. This step shows you exactly which accounts to prioritize, how much to contribute, and when to make strategic moves that reduce your future tax bill. You will restructure your portfolio to create multiple withdrawal buckets with different tax treatments, giving you maximum flexibility when you start drawing income.

Max out tax-deferred accounts before age 60

Your NPS, EPF, and PPF offer the best tax-deferral benefits available in India. Contributions reduce your current taxable income under Section 80C (up to ₹1.5 lakh) and Section 80CCD(1B) (additional ₹50,000 for NPS). More importantly, these accounts grow tax-free until withdrawal, compounding your returns faster than taxable alternatives. Focus your last working years on maximizing these contributions because you lose this opportunity forever once you retire.

Calculate your remaining contribution capacity using this approach. If you earn ₹15 lakh annually and plan to work five more years, you can still contribute ₹2 lakh per year to tax-deferred accounts. That adds ₹10 lakh to your corpus while saving approximately ₹3 lakh in taxes over five years. Front-load your contributions if you expect salary increases since higher income years deliver larger tax savings per rupee invested.

Build a three-bucket withdrawal system

Tax efficient retirement planning requires you to create three distinct account categories before you retire. Your tax-free bucket includes fully matured EPF (more than five years), PPF at maturity, and Section 10(10D) exempt insurance proceeds. Your tax-deferred bucket holds NPS accumulations, VPF contributions, and gratuity. Your taxable bucket contains fixed deposits, mutual funds, and rental properties. You will draw from these buckets in a specific sequence during retirement to minimize your annual tax bill.

Set up your buckets using this template:

Bucket Type | Accounts | Current Value | Annual Withdrawal Capacity |

|---|---|---|---|

Tax-free | EPF, PPF, Insurance | ₹45,00,000 | ₹3,00,000 |

Tax-deferred | NPS, VPF | ₹32,00,000 | ₹2,50,000 |

Taxable | FDs, Mutual Funds | ₹28,00,000 | ₹4,50,000 |

Building three withdrawal buckets before retirement gives you the flexibility to control your tax slab every single year.

Time your EPF and PPF withdrawals

Both EPF and PPF become completely tax-free after specific holding periods, but premature withdrawals trigger full taxation on the employer contribution and interest portions. You must complete five years of continuous service for EPF withdrawals to remain tax-exempt. PPF requires a 15-year maturity period for complete tax-free treatment, though you can make partial withdrawals after seven years without losing the tax benefit.

Plan your withdrawal timeline now, before you retire. If your PPF matures in 2027 but you plan to retire in 2026, consider extending your employment by one year or arranging a consulting contract to bridge the gap. Similarly, if you have multiple EPF accounts from different employers, consolidate them before retirement to ensure you meet the five-year continuous service requirement. These timing decisions prevent you from paying unnecessary taxes on money that should be tax-free.

Step 3. Design tax efficient income in retirement

Once you retire, your withdrawal sequence determines how much tax you pay each year. You cannot simply withdraw money whenever you need it because every rupee you take out affects your tax slab for that entire year. This step gives you the exact order to tap your accounts, shows you how to balance taxable and tax-free income, and provides specific withdrawal rules that keep your tax bill minimal. You will create a year-by-year withdrawal plan that adapts to your changing needs while preserving your purchasing power.

Draw from tax-free buckets first

Your fully matured EPF and PPF should fund your first five to seven years of retirement expenses. These withdrawals trigger zero taxes while keeping you in the lowest possible tax bracket. Start by withdrawing the maximum you need from EPF since it offers complete tax exemption after five years of service. Your PPF becomes entirely tax-free at maturity, making it perfect for early retirement when you want to avoid pushing yourself into higher slabs with taxable income.

Calculate your annual needs and match them to your tax-free corpus. If you need ₹6 lakh per year and hold ₹42 lakh in tax-free accounts, you can cover seven full years without paying a single rupee in income tax. During this period, let your tax-deferred and taxable accounts continue growing since you are not forced to withdraw from them yet. This delay compounds your remaining corpus and reduces the total amount you need to extract later.

Exhausting tax-free accounts first creates a tax holiday that lets your other investments compound for years longer.

Layer in tax-deferred withdrawals strategically

After depleting your tax-free buckets, shift to your NPS and VPF accounts. NPS forces you to purchase an annuity with 40% of your corpus at maturity, and that annuity income gets taxed as regular income. The remaining 60% offers partial tax benefits if you withdraw it as a lump sum. You can withdraw up to 60% tax-free, but any amount beyond the minimum annuity requirement faces taxation. Structure your NPS withdrawal to take the maximum tax-free lump sum first, then manage the annuity income by timing it with lower-income years.

Your VPF withdrawals follow EPF tax rules. If you maintained your VPF account for more than five years after your last EPF contribution, the withdrawal remains tax-free. Use this account after exhausting EPF and PPF but before touching fully taxable investments. This sequencing keeps you in lower tax brackets for at least a decade into retirement.

Fill gaps with taxable income sources

Only tap your fixed deposits, mutual fund redemptions, and rental income when you have exhausted tax-free and tax-deferred options. Even then, manage these withdrawals carefully. Redeem only enough from equity mutual funds to fill the gap between your expenses and tax-free income. Long-term capital gains on equity funds remain tax-free up to ₹1.25 lakh annually, so you can extract this amount every year without paying taxes.

Your fixed deposit interest gets taxed at your marginal rate, but senior citizens receive a ₹50,000 exemption under Section 80TTB. Structure your FD portfolio to generate exactly ₹50,000 in interest each year, keeping the remainder in tax-free instruments until you need it. Break large FDs into smaller deposits with staggered maturity dates so you can control exactly when interest income hits your tax return. This tactic prevents lumpy income that pushes you into higher brackets in any single year.

Step 4. Maintain and review your plan

Tax laws change every budget cycle, and your income needs shift as you age. A withdrawal strategy that worked perfectly in 2025 might cost you lakhs in unnecessary taxes by 2030 if you never revisit it. You must review your tax efficient retirement planning at least once annually to catch rule changes, adjust for new exemptions, and rebalance your withdrawal buckets. This maintenance step prevents tax surprises and ensures your strategy stays optimized as India's retirement tax landscape evolves with each Finance Bill.

Set annual review triggers

Mark every February in your calendar as your mandatory review month, right after the Union Budget announcement. Check whether Section 80TTB exemption limits changed, whether NPS withdrawal rules shifted, or whether capital gains thresholds moved. Compare your actual withdrawals from the previous year against your original plan to identify any deviations. Create a simple review checklist that tracks three items: changes in tax slabs for seniors, modifications to retirement account rules, and updates to exemption limits on interest and capital gains.

Your review should also capture life changes that affect your withdrawal needs. Medical expenses might force you to tap accounts earlier than planned. Conversely, reduced spending could let you delay taxable withdrawals by another year, keeping you in a lower bracket. Document these adjustments in a spreadsheet with columns for year, planned withdrawal, actual withdrawal, tax paid, and notes explaining any changes.

Adjust for tax law changes

When the government announces tax reforms, recalculate your entire withdrawal sequence within 30 days. The 2023 budget introduced new capital gains rules that affected LTCG exemptions, forcing retirees to restructure their equity fund redemption schedules. You might need to shift money between buckets or accelerate certain withdrawals before unfavorable rules take effect. Track all amendments that touch retirement income, including changes to pension taxation, annuity treatment, and senior citizen deductions, then update your year-by-year withdrawal plan immediately.

Putting it all together

You now have a complete framework for tax efficient retirement planning. Map your income sources and calculate your tax slab. Build your three-bucket system during your working years. Withdraw from tax-free accounts first, then tax-deferred, and finally taxable sources. Review your plan every February after the budget announcement.

This strategy reduces your lifetime tax bill by lakhs while preserving your purchasing power. But tracking multiple accounts, calculating optimal withdrawal amounts, and adjusting for tax law changes requires constant attention. Invsify's AI-powered retirement planning tools automate these calculations and alert you when rule changes affect your strategy. Start your free trial and let our platform optimize your withdrawal sequence based on your specific tax situation.