Tax Planning for Salaried Individuals: India 2025 Guide

Shlok Sobti

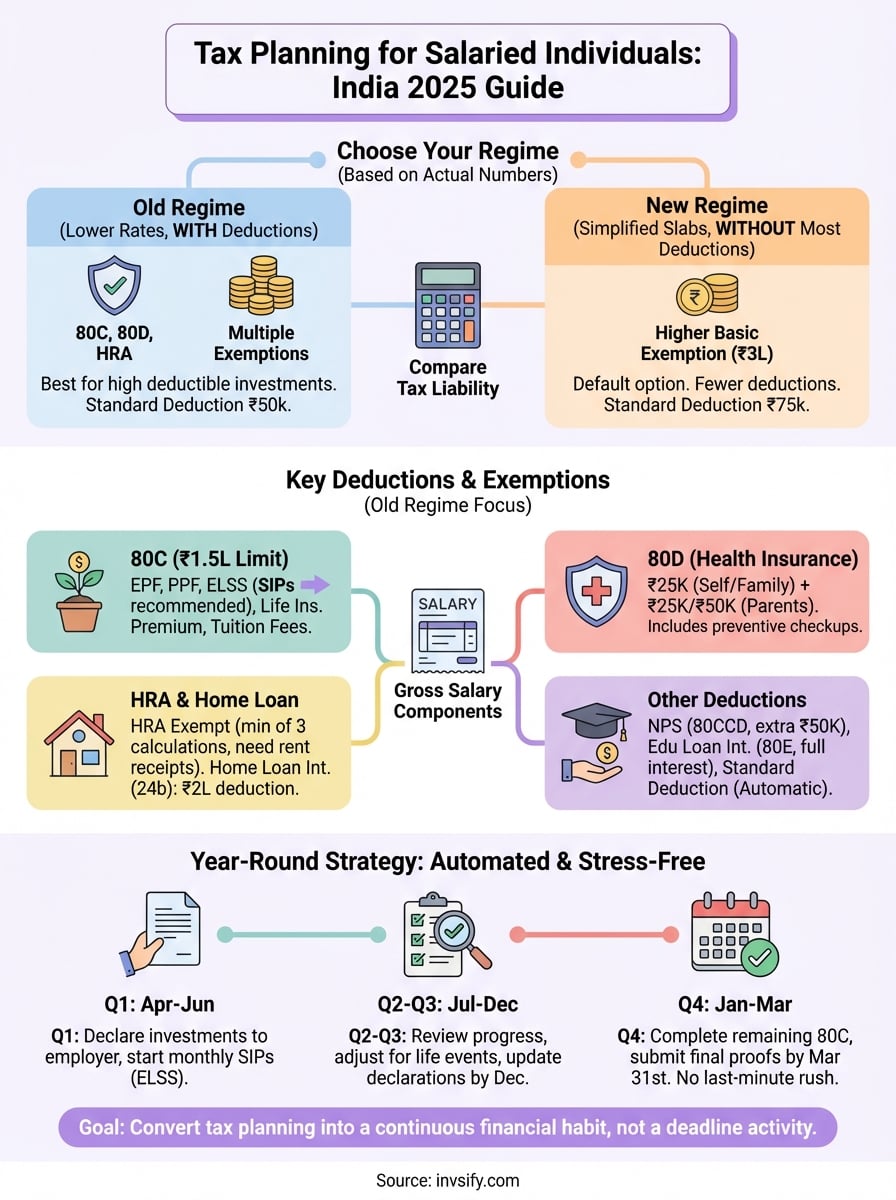

Tax Planning for Salaried Individuals: India 2025 Guide

Every March, millions of salaried Indians realize they could have saved thousands in taxes. You submit investment proofs at the last minute, miss key deductions, and wonder why your payslip shows less take-home than expected. The problem isn't your salary. It's the lack of a structured approach to tax planning throughout the year.

Smart tax planning means understanding your salary components, choosing the right tax regime, and timing your investments correctly. It's not about complicated schemes or chasing the latest tax-saving product. You need a clear framework that reduces your tax liability while aligning with your financial goals.

This guide breaks down tax planning for Indian salaried individuals in 2025. You'll learn how to read your salary structure for hidden tax benefits, use Section 80C and other deductions effectively, and build a year-round tax strategy. We'll cover practical steps you can implement immediately, compare the old and new tax regimes with real numbers, and show you exactly which investments make sense for your situation.

What tax planning means in India 2025

Tax planning means structuring your income and investments to pay the minimum legal tax amount. You arrange your finances throughout the year, not just in March, to maximize deductions, exemptions, and rebates under the Income Tax Act. The goal isn't tax evasion (which is illegal) but tax optimization through legitimate strategies available to every salaried employee.

The two tax regime system

India now operates under two parallel tax systems that you must choose between. The old regime offers lower tax rates with multiple deductions under sections like 80C, 80D, and HRA exemptions. The new regime provides simplified slab rates without most deductions, introduced in Budget 2020 and made default from FY 2023-24. You can switch between regimes each year based on your investment profile and salary structure.

The regime you choose determines whether you save more through lower rates or higher deductions.

Your focus areas for 2025

Tax planning for salaried individuals in 2025 requires analyzing both regimes with actual numbers from your salary slip. You need to calculate your taxable income under each system by factoring in standard deduction (₹75,000 in new regime, ₹50,000 in old), investments qualifying for 80C (up to ₹1.5 lakh), health insurance premiums (80D), and house rent allowance. Most employees with annual investments below ₹2.5 lakh find the new regime beneficial, while those with higher deductible investments prefer the old regime.

Your employer deducts TDS based on your chosen regime and investment declarations submitted at the year's start. If you don't declare investments properly, you face higher TDS throughout the year and wait for refunds after filing returns. Smart planning means projecting your investments in April, updating declarations by January, and ensuring your actual investments match your projections by March 31st.

Step 1. Decode your salary and tax slabs

Your salary slip contains multiple components that determine your final tax liability. Most employees focus only on gross salary, missing the tax treatment differences between basic pay, allowances, and perquisites. Understanding which components qualify for exemptions and how each gets taxed forms the foundation of effective tax planning for salaried individuals. You can reduce your taxable income significantly by structuring these components correctly with your employer.

Your salary components and what's taxable

Basic salary forms 30 to 50% of your CTC and is fully taxable without any exemptions. Your employer calculates provident fund, gratuity, and other benefits as a percentage of this amount. Allowances like House Rent Allowance (HRA), Leave Travel Allowance (LTA), and special allowances receive different tax treatments based on specific conditions and documentation you provide.

HRA qualifies for exemption if you pay rent and submit proof through rent receipts or agreements. The exemption equals the minimum of three calculations: actual HRA received, 50% of basic salary for metro cities (40% for non-metros), or rent paid minus 10% of basic salary. Transport allowance disappeared from FY 2018-19 when the government introduced the standard deduction. Meal coupons up to ₹50 per meal remain tax-free, and reimbursements for phone bills, internet, and books can reduce your taxable income if your company policy allows them.

Your salary structure, not just gross amount, determines your take-home pay and tax liability.

Tax slabs comparison for 2025

The old regime starts taxation at ₹2.5 lakh with rates of 5%, 20%, and 30% across different income brackets. You get the ₹50,000 standard deduction plus access to all Section 80C, 80D, and other deductions. The new regime offers higher basic exemption at ₹3 lakh with six tax slabs (5%, 10%, 15%, 20%, and 30%) but removes most deductions except employer NPS contribution and standard deduction of ₹75,000.

Income Range | Old Regime Rate | New Regime Rate |

|---|---|---|

Up to ₹2.5L / ₹3L | 0% | 0% |

₹2.5L to ₹5L / ₹3L to ₹7L | 5% | 5% |

₹5L to ₹10L / ₹7L to ₹10L | 20% | 10% |

₹10L+ / ₹10L to ₹12L | 30% | 15% |

Above ₹12L to ₹15L | 30% | 20% |

Above ₹15L | 30% | 30% |

Calculate your actual tax liability

Start with your gross salary minus standard deduction to arrive at your net taxable income before other deductions. Subtract your 80C investments (up to ₹1.5 lakh), health insurance premiums (80D), and home loan interest (Section 24b) if you choose the old regime. Calculate tax on this final amount using the applicable slab rates, then add 4% cess on the computed tax.

Take a ₹12 lakh salary example with ₹1.5 lakh in 80C investments and ₹25,000 health insurance. Under the old regime: ₹12L minus ₹50K standard minus ₹1.5L minus ₹25K equals ₹9.75L taxable, resulting in approximately ₹1.12 lakh tax. Under the new regime: ₹12L minus ₹75K equals ₹11.25L taxable, resulting in approximately ₹1.05 lakh tax. The new regime saves ₹7,000 in this scenario despite having fewer deductions.

Step 2. Use deductions and exemptions wisely

Deductions and exemptions convert your gross salary into actual taxable income, creating immediate tax savings you can calculate and verify. You need to understand which deductions apply under your chosen tax regime, document them properly, and time your investments correctly to maximize benefits. Tax planning for salaried individuals succeeds when you treat deductions as financial planning tools, not just tax-saving checkboxes to tick in March.

Section 80C investments that actually work

Section 80C offers ₹1.5 lakh deduction across multiple investment options, but not all choices serve your financial goals equally. Your employer's Employee Provident Fund (EPF) contribution automatically consumes part of this limit, typically 12% of your basic salary. If your basic salary is ₹50,000 monthly, EPF takes ₹72,000 of your 80C space, leaving ₹78,000 for voluntary investments.

Public Provident Fund (PPF) provides 7.1% interest with complete tax exemption on maturity and fits the 80C limit perfectly for long-term wealth building. Equity Linked Savings Schemes (ELSS) offer market-linked returns with just 3 years lock-in, the shortest among 80C options, making them suitable when you need both tax savings and growth potential. National Savings Certificates (NSC) deliver 7.7% interest with 5-year maturity, ideal when you prefer guaranteed returns over equity exposure.

Life insurance premiums qualify for 80C, but you should buy insurance for protection, not tax savings. Choose term insurance based on your coverage needs (typically 10-15 times annual income), then count the premium as a 80C benefit. Unit-Linked Insurance Plans (ULIPs) combine insurance with investment but carry higher charges and longer lock-ins than standalone ELSS funds. Home loan principal repayments also claim 80C benefits, though interest payments get separate deduction under Section 24b up to ₹2 lakh.

Your 80C strategy should match your financial timeline and risk appetite, not just fill the deduction limit.

Health insurance and medical deductions

Section 80D allows ₹25,000 deduction for health insurance premiums paid for yourself, spouse, and dependent children. You get an additional ₹25,000 for premiums paid for your parents, increasing to ₹50,000 if your parents are senior citizens (60+ years). Preventive health checkups count within these limits up to ₹5,000, covering annual health packages for your family.

Calculate your 80D benefit with actual scenarios. A 35-year-old paying ₹15,000 for family health insurance and ₹30,000 for parents' senior citizen policy claims ₹45,000 total deduction (₹15,000 + ₹30,000). At 30% tax bracket, this saves ₹13,500 in taxes while ensuring comprehensive health coverage. Medical expenses for senior citizen parents qualify up to ₹50,000 even without insurance, provided you maintain bills and receipts for all treatments.

House rent and housing benefits

HRA exemption requires you to submit rent receipts for monthly rent above ₹8,000 (PAN details needed if annual rent exceeds ₹1 lakh). Calculate your exemption as the minimum of three amounts: actual HRA received, 50% of salary for metro cities (Mumbai, Delhi, Kolkata, Chennai) or 40% for other cities, and rent paid minus 10% of salary.

Take a Mumbai employee with ₹60,000 basic salary, ₹25,000 HRA, paying ₹20,000 monthly rent. The three calculations yield: ₹25,000 (actual HRA), ₹30,000 (50% of basic), and ₹14,000 (rent minus 10% basic). Your exemption equals ₹14,000 monthly or ₹1.68 lakh annually, the minimum of these three amounts. Submit rent receipts to your employer before January to adjust TDS calculations correctly.

Home loan interest under Section 24b provides ₹2 lakh deduction for self-occupied property. You claim this in addition to 80C benefits on principal repayment, creating significant tax savings for home buyers. First-time home buyers get extra ₹50,000 deduction under Section 80EEA for loans sanctioned between April 2019 and March 2022, provided property value doesn't exceed ₹45 lakh.

Lesser-known deductions you shouldn't miss

Section 80E covers complete interest on education loans without any upper limit, available for eight years or until loan closure. You cannot claim principal repayment, but the interest deduction helps significantly during the initial high-interest years. This applies to loans taken for higher education for yourself, spouse, children, or a student for whom you are legal guardian.

National Pension System (NPS) contributions claim separate ₹50,000 deduction under 80CCD(1B) over and above the ₹1.5 lakh limit in 80C. Employer contributions to NPS qualify under 80CCD(2) up to 10% of salary without any monetary limit, available in both old and new tax regimes. Section 80G covers donations to specified charitable institutions with 50% or 100% deduction depending on the organization's qualification, requiring receipts with the institution's 80G registration number.

Standard deduction applies automatically: ₹75,000 in new regime and ₹50,000 in old regime for all salaried employees. You don't need to claim this separately. Your employer factors it into TDS calculations, reducing your taxable salary without requiring any documentation or investment proof.

Step 3. Build a year round tax saving plan

Tax planning for salaried individuals fails when you treat it as a March deadline activity instead of a continuous financial process. You create real value by spreading your investments across 12 months, matching each contribution to your cash flow and financial goals. This approach eliminates the pressure of finding ₹1.5 lakh in March and ensures you capture market opportunities throughout the year for equity-linked instruments like ELSS.

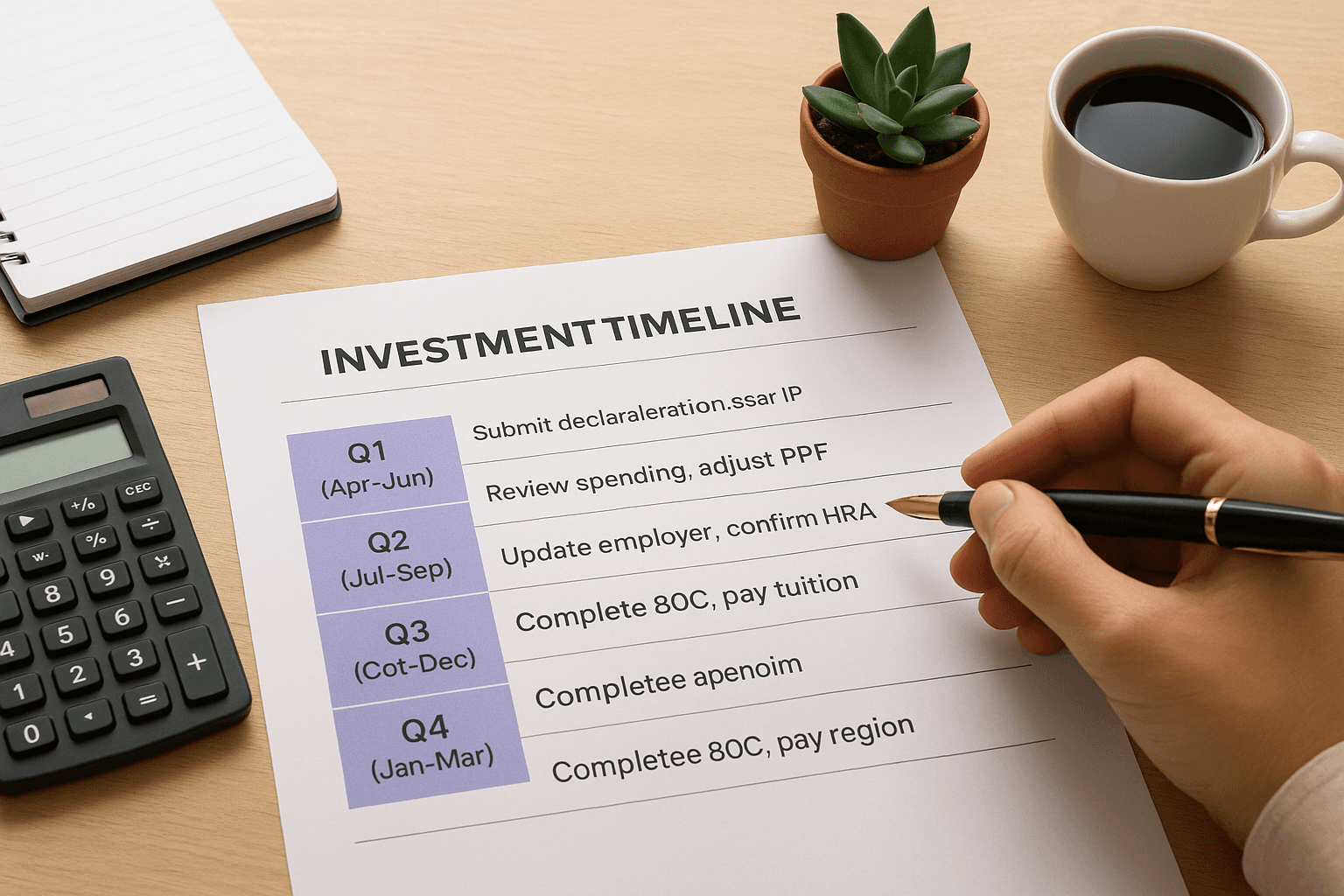

Your April to March investment timeline

Start your financial year by declaring your expected investments to your employer in April or May. Your HR department uses these projections to calculate monthly TDS, directly affecting your take-home salary from the first paycheck. Submit Form 12BB with estimated amounts for 80C investments, health insurance premiums, home loan interest, and HRA details to ensure accurate TDS deduction from day one.

Execute your investments using this quarterly approach:

Quarter | Action Items | Deadline |

|---|---|---|

Q1 (Apr-Jun) | Submit investment declarations, start SIP for ELSS, renew health insurance | May 31 |

Q2 (Jul-Sep) | Review half-year spending, adjust PPF contributions, pay LIC premiums | September 30 |

Q3 (Oct-Dec) | Update employer with revised declarations, confirm HRA documentation | December 31 |

Q4 (Jan-Mar) | Complete remaining 80C investments, pay tuition fees, file final proofs | March 31 |

Systematic Investment Plans (SIPs) in ELSS funds solve the timing problem completely by investing fixed amounts monthly. You set up ₹12,500 monthly SIP to exhaust your ₹1.5 lakh limit automatically, removing the need to track or remember deadlines. This method also provides rupee cost averaging benefits in equity investments, potentially improving your returns compared to lump sum investments in March.

Spreading investments across 12 months converts tax planning from a stressful deadline into an automated financial habit.

Track declarations vs actual investments

Create a simple tracking sheet in Google Sheets or Excel with these columns: Investment Type, Declared Amount, Invested Amount, Month, and Remaining Balance. Update this monthly when you make any 80C or 80D qualifying investment to maintain real-time visibility of your tax-saving progress. Compare your actual investments against declarations by December to identify gaps requiring immediate action before year-end.

Your employer requires updated Form 12BB by January 15th if your actual investments differ from April declarations. Submit revised figures with supporting documents to adjust remaining TDS calculations for January, February, and March salaries. Missing this deadline means you pay higher TDS for three months and wait for refunds after filing returns in July.

Adjust for salary changes and life events

Salary increments, job changes, marriage, childbirth, or home purchases trigger immediate tax planning reviews. You need to recalculate your optimal regime choice and investment amounts whenever your annual income changes by more than ₹2 lakh. A ₹15 lakh salary might benefit from the new regime, but a jump to ₹18 lakh with a new home loan could make the old regime superior due to additional 24b deductions.

Document your adjustments with specific actions. Getting married adds your spouse to 80D coverage, increasing your health insurance deduction capacity. Having a child qualifies you for ₹1.5 lakh annual tuition fee deduction under 80C, automatically reducing the amount you need from other 80C instruments. Each major life event creates new deduction opportunities that require you to update both your investment strategy and employer declarations within the same financial year.

Additional tools and examples

You need practical tools and real calculations to execute your tax planning for salaried individuals effectively. Numbers clarify which regime works better for your specific salary and investment profile, removing guesswork from financial decisions. Use these templates and examples to calculate your exact tax liability and create a tracking system that keeps you organized throughout the year.

Your tax comparison template

Create a simple comparison sheet to calculate your tax under both regimes each year. Start with your gross salary, subtract standard deduction, then work through all applicable deductions in the old regime column. Calculate tax on both final amounts using current slab rates to identify which regime delivers lower tax liability.

Component | Old Regime | New Regime |

|---|---|---|

Gross Salary | ₹10,00,000 | ₹10,00,000 |

Standard Deduction | (₹50,000) | (₹75,000) |

80C Investments | (₹1,50,000) | 0 |

80D Premium | (₹25,000) | 0 |

HRA Exemption | (₹1,00,000) | 0 |

Taxable Income | ₹6,75,000 | ₹9,25,000 |

Tax Payable | ₹70,000 | ₹77,500 |

Real scenarios with actual numbers

Consider a Bangalore employee earning ₹8 lakh with ₹60,000 EPF, ₹40,000 PPF, and ₹20,000 health insurance. Under the old regime, taxable income reaches ₹6.7 lakh (after ₹50,000 standard and ₹1.2 lakh total deductions), resulting in ₹46,800 tax. The new regime shows ₹7.25 lakh taxable income with ₹36,250 tax, saving ₹10,550 annually despite fewer deductions.

A Delhi employee at ₹15 lakh with home loan (₹2 lakh interest), full 80C usage, and ₹50,000 parents' health insurance calculates differently. Old regime delivers ₹1.45 lakh tax on ₹11 lakh taxable income (after ₹4 lakh deductions). New regime shows ₹1.95 lakh tax on ₹14.25 lakh income, making the old regime superior by ₹50,000.

Your regime choice depends entirely on your actual deduction amounts, not theoretical maximums.

Next steps for your tax plan

Your tax planning for salaried individuals requires immediate execution, not delayed decisions. Calculate your optimal tax regime using your actual salary numbers, set up automated monthly investments in ELSS or PPF, and update your employer declarations by next week. These three actions convert today's knowledge into measurable tax savings when you file returns in July.

Sign up with Invsify to access AI-powered tax optimization that tracks your investments year-round, sends timely reminders for declaration updates, and ensures you capture every eligible deduction.