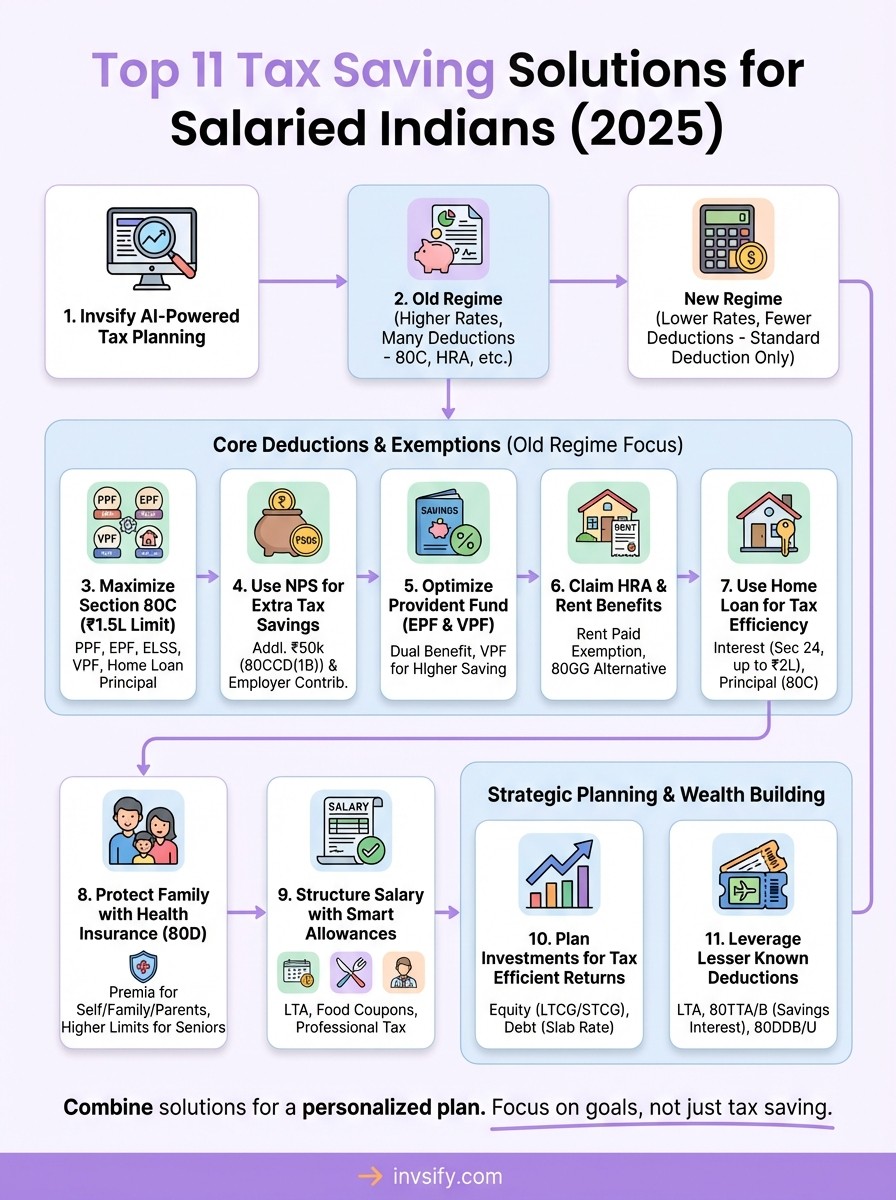

Top 11 Tax Saving Solutions for Salaried Indians (2025)

Shlok Sobti

Top 11 Tax Saving Solutions for Salaried Indians (2025)

You work hard for your salary, but a large chunk disappears to income tax every year. Most salaried Indians struggle to figure out which tax saving options actually make sense—especially with the choice between old and new tax regimes adding another layer of confusion. You might be investing in 80C options without knowing if they fit your goals, or missing out on deductions you qualify for simply because nobody explained them clearly.

This article breaks down 11 practical tax saving solutions built specifically for salaried Indians in 2025. We start with AI powered tax planning through Invsify, then walk through regime selection, core deductions like 80C and NPS, home loan benefits, health insurance, salary structuring, and several lesser known exemptions that can reduce your tax bill. Each solution includes when to use it, how it works across both tax regimes, and who benefits most. By the end, you will have a clear roadmap to legally minimize your taxes while building real wealth—not just throwing money at random investments before March 31st.

1. Invsify AI tax planning and advisory

You need a system that connects tax planning with your overall wealth strategy instead of treating them as separate tasks. Invsify combines AI powered insights with human expertise to help you identify the right tax saving solutions based on your actual financial situation, not generic advice that ignores your goals. The platform analyzes your income, investments, and life stage to recommend specific deductions and structuring moves that reduce your tax bill while building long term wealth.

How Invsify optimizes your tax and investments

Invsify runs a comprehensive analysis of your salary structure, existing investments, and risk profile to identify every tax saving opportunity you qualify for. The AI evaluates whether you should stick with the old regime or switch to the new one, then suggests the optimal mix of 80C instruments, NPS contributions, and other deductions that align with your financial goals. You get personalized recommendations that go beyond random investment tips you find online, because the system considers your entire portfolio and future plans before suggesting any move.

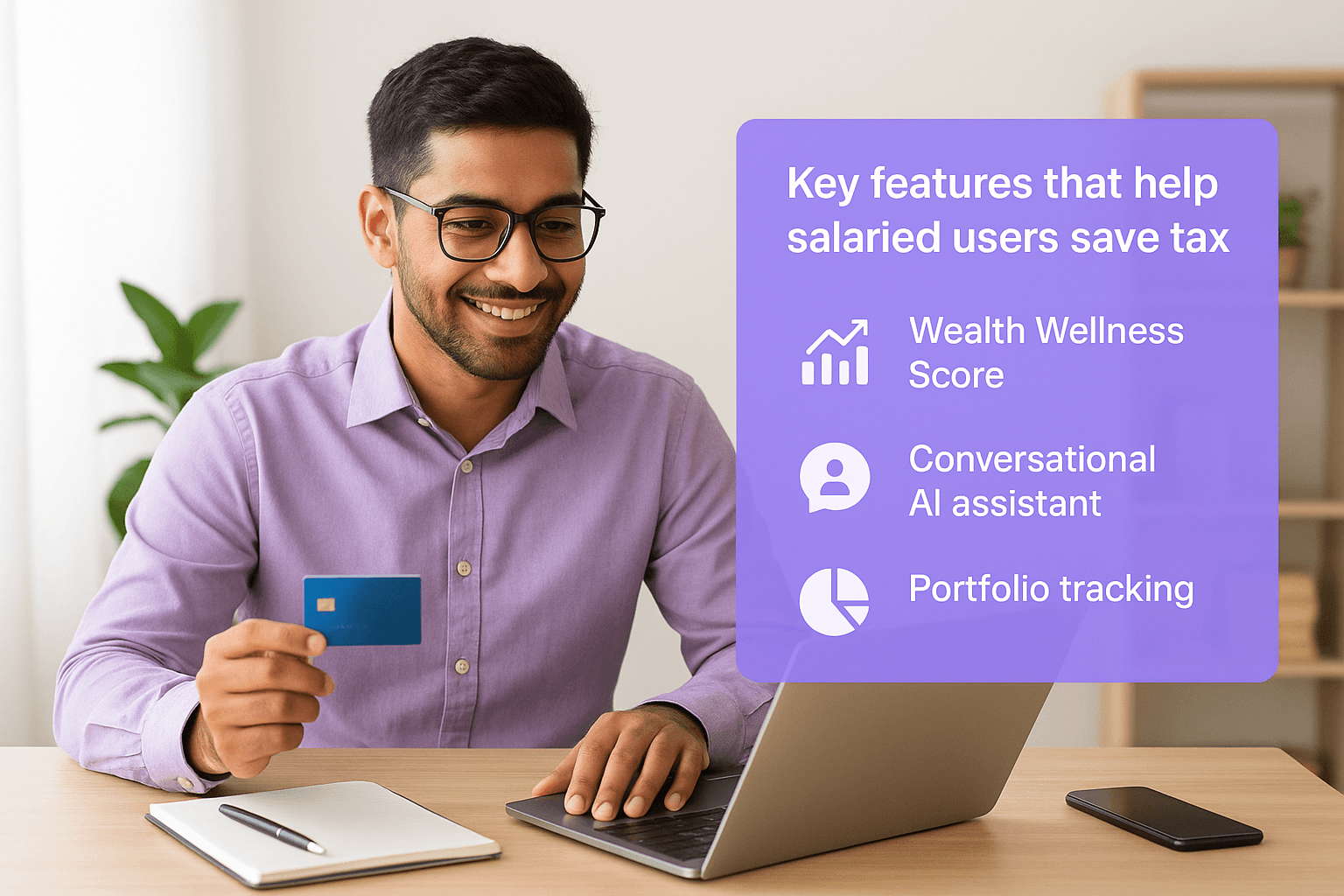

Key features that help salaried users save tax

The platform offers a Wealth Wellness Score that shows exactly where you stand on tax efficiency and financial health. You access a conversational AI assistant 24/7 for questions about specific deductions, regime comparisons, or investment choices. Daily audio snippets keep you updated on tax rule changes and planning opportunities. Advanced portfolio tracking shows how your current investments contribute to tax savings, while real time AI advisory alerts you when better options become available or when you approach deduction limits.

"The Hidden Fee Calculator reveals how much traditional distributors cost you through commissions, making conflict free advice financially visible."

When to use Invsify in your financial journey

Start with Invsify when you want to move beyond basic 80C investments and build a comprehensive wealth plan that includes smart tax management. The platform works best for salaried professionals who currently self manage their money using online forums or generic advice but need data backed, personalized recommendations instead. You benefit most if you earn enough to face meaningful tax liability but lack the time to research every deduction, investment, and regime rule yourself.

Costs transparency and conflict free advice

Invsify operates as a SEBI Registered Investment Advisor, which means the platform earns through advisory fees rather than product commissions. You pay for advice directly, so every recommendation prioritizes your financial benefit over pushing high commission products. This structure eliminates the conflicts traditional distributors face when they earn more by selling certain funds or insurance policies regardless of whether those products suit your needs.

2. Choose the right tax regime

Your choice between the old and new tax regimes determines which tax saving solutions work for you and how much you ultimately pay. The government made the new regime the default option from FY 2023-24, but you can still opt for the old regime if it lowers your tax bill. Most salaried professionals rush this decision without calculating their actual tax liability under both systems, leaving money on the table every year.

Differences between old and new regimes

The new regime offers lower tax slab rates but removes most deductions and exemptions that the old regime allows. You face higher rates under the old regime (5% starting at ₹2.5 lakh income) but gain access to dozens of deductions like 80C, HRA, home loan interest, and more. The new regime starts taxation at ₹3 lakh with a standard deduction of ₹75,000 for salaried individuals, while keeping the tax structure simpler with fewer compliance requirements.

Role of deductions exemptions and standard deduction

Deductions under the old regime reduce your taxable income directly before calculating tax, making them powerful tools if you invest or spend in qualifying categories. The new regime strips away 80C, HRA, LTA, and most other exemptions but compensates with lower rates and the standard deduction. Your choice hinges on whether the deductions you claim under the old regime save more tax than the lower rates under the new regime deliver.

Income levels where the new regime often wins

The new regime typically benefits you if your annual income falls between ₹7 lakh and ₹15 lakh and you make minimal tax saving investments. You save more under the new system when you cannot maximize 80C or claim HRA, or when you prefer liquidity over locked investments. The rebate under section 87A (up to ₹25,000 for incomes up to ₹7 lakh) makes the new regime attractive for entry level salaries.

When the old regime still works better

High earners who max out 80C, pay home loan interest, and claim HRA often find the old regime cuts their tax bill significantly despite higher rates. You benefit from the old regime when your total deductions exceed ₹3 lakh annually or when you live in expensive cities with high rent. The old regime rewards structured financial planning with multiple deduction categories working together.

"Calculate your tax under both regimes each year because your income, investments, and expenses change, altering which system saves you more."

How to decide your regime each financial year

Run actual calculations comparing your tax liability under both regimes before filing your return or when your employer asks for regime preference. Factor in all deductions you claim, not just 80C, including home loan interest, HRA, NPS, and health insurance. Salaried employees can switch regimes every year, giving you flexibility as your financial situation evolves.

3. Maximize section 80C deductions

Section 80C remains the most popular tax saving route for salaried Indians, letting you deduct up to ₹1.5 lakh annually from your taxable income. This deduction works only under the old tax regime, so you sacrifice it entirely when you switch to the new regime. The category includes multiple investment and payment options, giving you flexibility to choose instruments that match your financial goals rather than forcing you into products that do not fit your needs.

Salary linked options EPF and voluntary PF

Your mandatory EPF contribution (12% of basic salary) automatically qualifies for 80C deduction, requiring no extra action from you. You can add Voluntary Provident Fund (VPF) contributions on top of the mandatory amount to reach the ₹1.5 lakh limit while earning the same interest rate EPF offers. VPF suits conservative savers who want guaranteed returns without market risk, though the money locks until retirement or specific withdrawal conditions apply.

Safe choices like PPF and tax saving fixed deposits

Public Provident Fund (PPF) offers government backed safety with tax free interest and a 15 year maturity period that works for long term goals like retirement. Tax saving fixed deposits provide 5 year lock in with guaranteed returns but tax you on the interest earned. Banks offer these FDs with slightly higher rates than regular deposits, making them suitable when you need capital protection but can accept lower post tax returns compared to equity options.

Market linked options ELSS ULIPs and other funds

Equity Linked Savings Schemes (ELSS) give you equity market exposure with only a 3 year lock in, the shortest among all 80C tax saving solutions. ULIPs combine insurance with investment but carry longer lock in periods and higher charges that eat into returns. ELSS works better for wealth building if you already have adequate term insurance coverage, while ULIPs suit those needing both insurance and investment in one product.

Using term insurance and home loan principal

Premium payments for term insurance qualify for 80C deduction while providing life cover for your family. Your home loan principal repayment also falls under 80C, along with stamp duty and registration charges paid during property purchase. These deductions work particularly well because they serve dual purposes instead of forcing you into investments purely for tax savings.

Prioritizing 80C based on your risk profile

Choose EPF and PPF for guaranteed returns when you cannot handle market volatility or approach retirement age. Pick ELSS for higher growth potential when you have a long investment horizon and accept short term market fluctuations. Balance your 80C portfolio across safety and growth instruments based on your age, income stability, and existing emergency funds.

"Use 80C deductions that genuinely fit your financial plan rather than buying random products just to save tax before March 31st."

4. Use NPS for extra tax savings

National Pension System (NPS) delivers additional tax deductions beyond the ₹1.5 lakh 80C limit, making it one of the most powerful tax saving solutions for salaried Indians under the old regime. You access multiple deduction categories through a single retirement focused investment, though the locked nature until age 60 requires careful planning before you commit funds.

Basics of NPS structure and investment choices

NPS lets you allocate contributions across equity, corporate bonds, and government securities based on your risk appetite. You choose between active choice (you decide asset allocation) or auto choice (the system adjusts allocation based on your age). The Tier I account qualifies for tax benefits but locks your money until retirement, while Tier II offers liquidity without any tax advantages.

Deductions under sections 80CCD 1 and 1B

Your employee contributions to NPS Tier I qualify for deduction under 80CCD(1) within the overall ₹1.5 lakh 80C limit. You gain an extra ₹50,000 deduction under section 80CCD(1B) that sits outside the 80C cap, bringing your total potential deduction to ₹2 lakh annually. This additional benefit works only under the old tax regime.

Employer contribution benefits under section 80CCD 2

Employer contributions to your NPS account qualify for separate deduction under section 80CCD(2) up to 14% of your basic salary plus DA. This deduction reduces your taxable salary directly and works under both old and new tax regimes. You gain tax savings without the contribution counting against your 80C or 80CCD(1B) limits.

Withdrawal and taxation rules at exit

You withdraw up to 60% of your corpus tax free at retirement, while the remaining 40% must purchase an annuity. Premature exit before age 60 forces you to annuitize 80% of the corpus, limiting your flexibility. Partial withdrawals during accumulation phase attract restrictions and potential tax implications.

When NPS fits your goals and when it does not

NPS works best when you prioritize tax savings and accept lock in until retirement while building a corpus. Skip NPS if you need liquidity before age 60 or already have sufficient retirement savings through other instruments. The mandatory annuity requirement reduces flexibility compared to purely investment focused options.

"Use NPS when the combined tax benefit across multiple sections outweighs the long lock in period that limits access to your money."

5. Optimize provident fund contributions

Provident fund offers you dual benefits of tax savings and retirement corpus building through a government backed instrument. Your Employee Provident Fund (EPF) contribution automatically qualifies for section 80C deduction under the old tax regime, making it one of the most accessible tax saving solutions for salaried Indians. The structure allows you to increase contributions beyond the mandatory amount through Voluntary Provident Fund, giving you control over how much you save while reducing taxable income.

How EPF contributions reduce taxable salary

Your mandatory EPF contribution (12% of basic salary plus dearness allowance) gets deducted from your gross salary before tax calculation. This reduces your taxable income directly, lowering the tax you pay each month rather than requiring year end adjustments. Employers match your contribution with another 12%, though their contribution does not appear in your 80C limit.

Using voluntary provident fund for higher saving

Voluntary Provident Fund (VPF) lets you contribute additional amounts beyond the mandatory 12% into the same EPF account. You earn the same interest rate EPF offers (currently around 8.15% annually) while these extra contributions count toward your 80C deduction limit. VPF suits you when you want guaranteed returns without market risk and can lock money until retirement or specific withdrawal events.

Interest rate tax rules and withdrawal conditions

Interest earned on EPF contributions stays tax free when your annual employee contribution stays below ₹2.5 lakh. Contributions exceeding this threshold attract tax on the interest earned above the limit. You access your corpus tax free after five years of continuous service, making it a patient wealth building tool.

Deciding between PF VPF and other options

Choose VPF when you prioritize capital safety over higher returns and already have adequate emergency funds. Pick ELSS or NPS for potentially higher growth when you can handle market volatility and want diversification across asset classes. Balance your 80C allocation based on your age and risk capacity.

"Use VPF to fill your 80C limit when you want guaranteed returns without the complexity of managing multiple investment accounts."

6. Claim HRA and rent benefits

House Rent Allowance (HRA) gives you substantial tax relief when you live in rented accommodation, making it one of the most valuable tax saving solutions for salaried Indians under the old regime. Your employer typically includes HRA as part of your salary structure, and you claim exemption by submitting rent receipts and landlord details. The benefit directly reduces your taxable salary without requiring you to lock money into investments, though you must actually pay rent to qualify for the deduction.

Conditions you must meet to claim HRA exemption

You qualify for HRA exemption when you receive HRA in your salary structure and actually pay rent for your residence. You need rent receipts for monthly rent exceeding ₹3,000 along with your landlord's PAN if annual rent crosses ₹1 lakh. Your rented property cannot be owned by you, and you must live in the property you claim rent for, not your own house.

Simple way to estimate your HRA tax benefit

Your exempt HRA equals the lowest of three values: actual HRA received, 50% of basic salary for metro cities (40% for non-metros), or actual rent paid minus 10% of basic salary. Calculate each amount and pick the smallest number to determine your tax free portion. The remaining HRA gets added to your taxable income.

Dealing with rent paid to parents or other relatives

You can pay rent to your parents and claim HRA exemption if they own the property and declare this rental income in their tax return. Your parents must report the rent as income from house property, though they can claim deductions for property tax and standard deduction against this income. Keep proper rent receipts and maintain a formal rental agreement.

HRA treatment under the new tax regime

The new tax regime eliminates HRA exemption entirely, making this benefit unavailable when you choose lower tax rates. You receive the HRA amount as part of your salary, but it becomes fully taxable without any exemption. This loss significantly impacts the regime comparison for people paying high rent in expensive cities.

Options if you do not receive HRA in your salary

You claim deduction under section 80GG when your salary lacks HRA and you live in rented accommodation. This benefit allows ₹5,000 monthly or 25% of total income (whichever is lower) as deduction, capped at actual rent minus 10% of total income. Self employed individuals and those without HRA use this route for rent related tax savings.

"Calculate your HRA benefit accurately each year because improper claims trigger scrutiny and potential tax demands from the department."

7. Use home loan for tax efficiency

Home loans unlock multiple tax saving solutions that work across different sections of the Income Tax Act, making property ownership financially attractive beyond wealth creation. You reduce your taxable income through interest payments and principal repayment, with additional benefits for first time buyers. The deductions apply differently under old and new tax regimes, requiring you to understand which benefits remain available based on your property type and regime choice.

Tax benefits on home loan interest under section 24

You deduct interest paid on your home loan up to ₹2 lakh annually for self occupied property under section 24(b) when you choose the old tax regime. The new regime eliminates this deduction entirely for self occupied homes, making it unavailable despite lower tax rates. Your interest payment reduces taxable income directly, delivering savings proportional to your tax slab.

Principal repayment and stamp duty under section 80C

Your home loan principal repayment qualifies for section 80C deduction up to the ₹1.5 lakh overall limit under the old regime. Stamp duty and registration charges paid during property purchase also fall under 80C in the year you incur these expenses. These deductions work only under the old regime, vanishing when you switch to the new system.

Extra benefits that may apply to first time buyers

First time home buyers get an additional ₹50,000 deduction under section 80EEA for interest on loans sanctioned between April 2019 and March 2022, provided the property value stays below ₹45 lakh. This benefit sits outside the ₹2 lakh section 24 limit, though specific conditions around loan sanction dates and property value restrict eligibility.

Maximizing deductions with joint home loans

Joint home loans let both borrowers claim individual deductions for their share of interest and principal payments. You and your co-borrower each access the full ₹2 lakh interest deduction limit and ₹1.5 lakh 80C limit, effectively doubling the household tax benefit when both owners pay tax.

Impact of self occupied versus let out property

Let out properties allow you to deduct the entire interest amount without the ₹2 lakh cap under both tax regimes, making rental properties more tax efficient. Self occupied property faces the limit, though you claim the benefit only under the old regime. Your property classification determines deduction availability and quantum.

"Calculate whether the combined home loan deductions under the old regime exceed the tax savings from lower rates under the new regime before choosing."

8. Protect family with health insurance

Health insurance premiums qualify for section 80D deduction under the old tax regime, giving you tax relief while securing medical coverage for your family. You reduce your taxable income by paying premiums for yourself, spouse, children, and parents, with separate deduction limits for different age groups. The new tax regime eliminates this deduction entirely, making health insurance a purely protection focused expense without any tax benefit when you choose lower rates.

Section 80D limits for different age groups

You claim deduction up to ₹25,000 annually for premiums paid toward health insurance for yourself, spouse, and dependent children when all of you stay below 60 years of age. The limit increases to ₹50,000 when you or your spouse crosses 60 years, recognizing higher medical costs for senior citizens. You get an additional ₹25,000 deduction for parents below 60 and ₹50,000 for parents who are senior citizens, allowing total deductions up to ₹1 lakh annually under the old regime.

Choosing between individual and family floater plans

Family floater policies offer single premium coverage for your entire family while qualifying for the same ₹25,000 deduction limit. Individual policies provide dedicated sum insured for each member but cost more in total premiums. Floater plans work better when your family members stay healthy, while individual policies deliver more value when multiple members need hospitalization simultaneously.

Tax benefits for parents and senior citizen cover

You claim separate deductions for parent premiums regardless of whether they depend on you financially. Your parents must be alive and the policy must be in your name or theirs for you to claim the deduction. Senior citizen coverage delivers higher deduction limits, making it one of the valuable tax saving solutions that simultaneously protects your family.

Preventive health check ups and other nuances

Preventive health check up expenses qualify for deduction up to ₹5,000 within the overall section 80D limit, not as an additional benefit. You need valid payment receipts from recognized diagnostic centers to claim this amount. Government insurance schemes and CGHS contributions also fall under section 80D.

Aligning health insurance with your overall plan

Buy health insurance based on adequate coverage for medical emergencies rather than just tax savings. Calculate your section 80D benefit to determine whether the old regime makes financial sense compared to the new regime. Your insurance decisions should prioritize protection first, with tax benefits serving as a secondary advantage.

"Choose health insurance coverage that genuinely protects your family rather than buying minimal policies purely for tax deductions."

9. Structure salary with smart allowances

Your salary structure determines how much of your income faces taxation before you even consider investments. Strategic restructuring of salary components converts taxable elements into tax exempt allowances and reimbursements, reducing your tax liability without requiring additional spending. You negotiate these changes during job offers or annual reviews, working with your employer to maximize tax efficient compensation while staying within legal limits.

Key tax efficient salary components to request

Ask your employer to include specific allowances like LTA, medical reimbursement, and food coupons in your salary structure instead of receiving everything as basic pay. Request that your total compensation stays the same but gets split across tax advantaged components. Companies often agree to restructuring because it costs them nothing while helping you save tax.

Allowances that remain exempt in both regimes

Leave Travel Allowance (LTA) and transport allowance for differently abled employees remain exempt under both old and new tax regimes. Daily allowance for official travel and conveyance allowance for official duties also keep their tax free status across both systems. These allowances deliver value regardless of which regime you choose.

Perquisites that are tax free or low tax

Your employer provides telephone connections, internet bills, and official laptops as tax free perquisites when used for business purposes. Refreshment during office hours and recreational facilities avoid taxation for all employees. Corporate provided health insurance, meal coupons up to ₹50 per meal, and professional development courses offer tax efficient compensation alternatives.

Using reimbursements for official expenses

Submit genuine bills for official travel, mobile expenses, and business related purchases for tax free reimbursement instead of receiving taxable allowances. Maintain proper documentation proving business purpose to satisfy tax scrutiny. Your company processes these reimbursements without deducting tax when you provide valid proof of expenditure.

Approach for high income salaried professionals

Higher earners benefit from maximizing performance bonuses structured as variable pay that gets paid in the following financial year, deferring tax liability. Request that your employer contributes more to NPS under section 80CCD(2), giving you tax free income that builds retirement corpus. These tax saving solutions work particularly well when you already exhaust basic deduction limits.

Common salary structuring mistakes to avoid

Skip structuring allowances you will not actually use because unused allowances become fully taxable at year end. Avoid excessive splitting that triggers scrutiny from tax authorities questioning the genuineness of components. Balance your structure across legitimate allowances rather than converting entire salary into borderline arrangements that invite departmental attention.

"Structure your salary thoughtfully during job negotiations rather than trying to fix poor structures after you join the company."

10. Plan investments for tax efficient returns

Your investment returns face different tax treatments based on asset type, holding period, and income level, making tax efficiency as important as picking the right funds. You lose significant wealth to taxes when you ignore these rules while chasing returns. Understanding how equity, debt, and hybrid instruments get taxed helps you structure your portfolio for maximum after-tax gains, turning tax planning into a return enhancing strategy rather than just a compliance exercise.

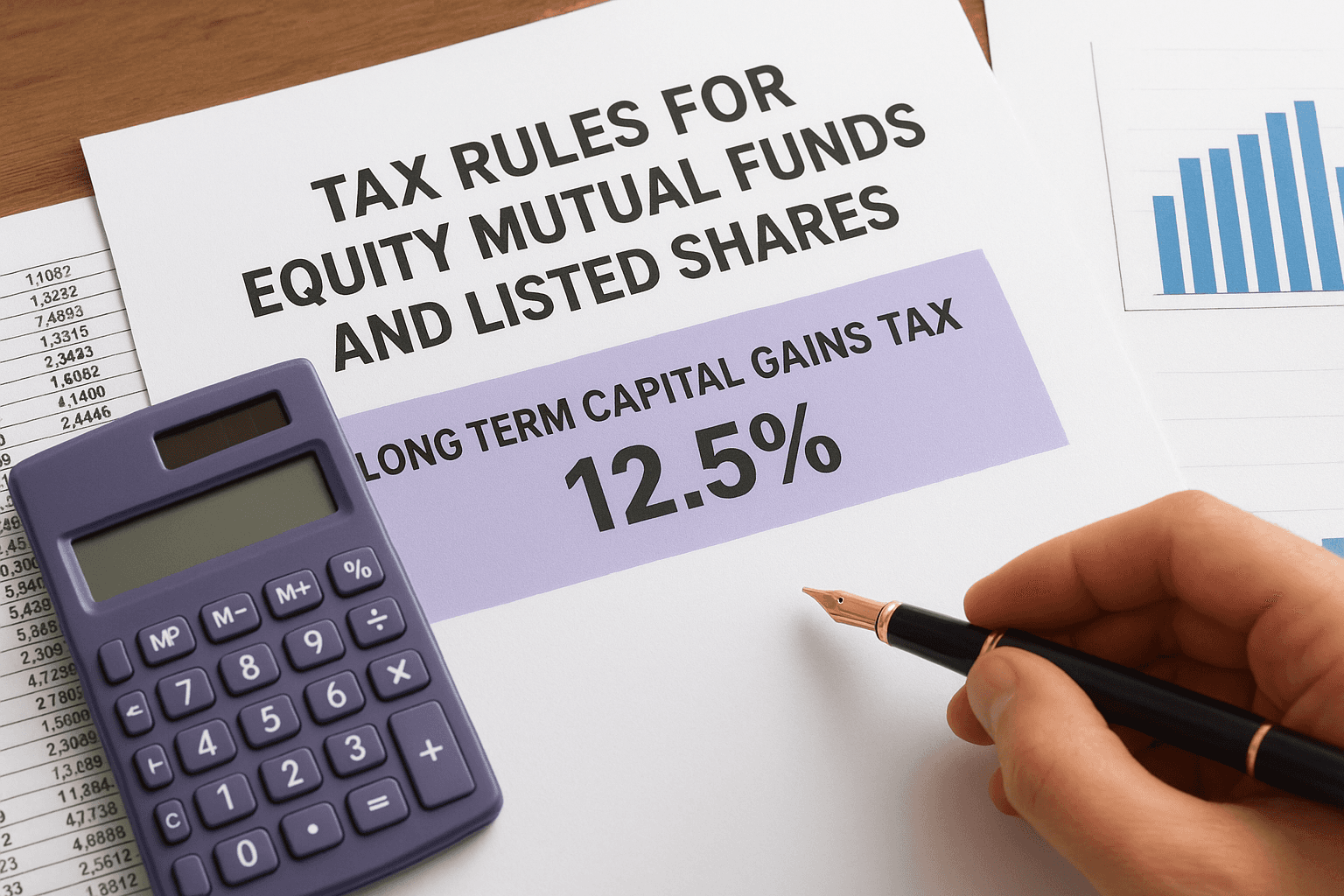

Tax rules for equity mutual funds and listed shares

Equity mutual funds and listed shares face long term capital gains tax at 12.5% when you hold beyond 12 months, with gains up to ₹1.25 lakh annually remaining tax free. Short term gains (sold within 12 months) attract flat 20% tax regardless of your income slab. This structure makes equity one of the most tax efficient tax saving solutions for wealth building when you maintain patience.

Tax rules for debt mutual funds and fixed deposits

Debt mutual funds purchased after April 2023 get taxed as per your income tax slab on all gains, eliminating the earlier indexation benefit. Fixed deposit interest gets added to your total income and taxed at your slab rate, making them inefficient for high earners. Tax free bonds and certain government schemes offer better post tax returns when you fall in higher brackets.

Holding periods and when indexation is available

Properties and debt funds purchased before April 2023 still qualify for indexation benefits after 24 months holding, adjusting your purchase cost for inflation. Newer debt fund investments lose this advantage entirely. Your holding period determines short term versus long term classification, directly impacting tax rates across asset classes.

Using ELSS and other funds for long term goals

ELSS combines section 80C deduction with equity returns and only 3 year lock in, making it suitable for goals beyond five years. Regular equity funds work better for longer horizons when you already exhaust 80C limits. Match your fund choice to goal timelines rather than tax savings alone.

Tax loss harvesting and year end planning

You offset capital gains by booking losses on underperforming investments before March 31st, reducing your tax bill while cleaning your portfolio. Repurchase the same securities after settlement if you want continued exposure. This strategy delivers immediate tax savings without changing your long term investment thesis.

"Structure your portfolio across asset classes and holding periods to minimize tax drag while achieving your financial goals."

11. Leverage other lesser known deductions

You overlook significant tax savings opportunities that sit outside the popular 80C and NPS categories, leaving money on the table each year. These lesser known deductions work under specific conditions and income limits, making them easy to miss during routine tax planning. Understanding these tax saving solutions helps you claim every rupee you qualify for without triggering compliance issues.

Leave travel allowance and how to claim it

Leave Travel Allowance (LTA) gives you tax exemption on domestic travel expenses for you and your family twice in a block of four calendar years under the old regime. You claim this benefit by submitting travel tickets and boarding passes to your employer, covering only the journey cost, not accommodation or sightseeing expenses. The exemption equals the actual travel cost or LTA received, whichever is lower.

Leave encashment gratuity and retirement payouts

Your leave encashment at retirement qualifies for exemption up to ₹25 lakh under specific calculation rules based on salary and years of service. Gratuity payments remain tax free up to ₹20 lakh when you satisfy continuity and other conditions. These exemptions reduce your tax burden during retirement year.

Interest on savings accounts under section 80TTA

Section 80TTA allows deduction up to ₹10,000 annually on interest earned from savings accounts, recurring deposits, and cooperative bank deposits for individuals below 60 years. Senior citizens access higher ₹50,000 deduction under section 80TTB covering all bank interest, making it a valuable benefit.

Deductions for disability and specified diseases

You claim deduction under section 80U for yourself or section 80DD for dependent disabled family members, ranging from ₹75,000 to ₹1.25 lakh based on disability severity. Medical treatment for specified diseases qualifies for section 80DDB deduction up to ₹40,000 or ₹1 lakh for senior citizens.

Commonly missed small exemptions and limits

Your children's education allowance (₹100 per month per child) and hostel allowance (₹300 per month per child) for up to two children qualify for exemption under the old regime. Daily food coupons, telephone bills for official use, and professional tax paid deliver incremental savings that add up across the year.

"Claim these smaller deductions systematically rather than dismissing them as insignificant, because together they meaningfully reduce your tax liability."

Bringing your tax plan together

You now have 11 practical tax saving solutions that work for salaried Indians across different income levels and financial goals. Your tax strategy should combine regime selection with smart investments, salary structuring, and claiming every deduction you qualify for rather than randomly picking options before March 31st. The old regime rewards systematic planning through 80C, NPS, HRA, and home loan deductions, while the new regime delivers value through simplicity and lower rates when you make minimal investments.

Build your tax plan around your actual financial goals instead of chasing deductions that lock money without serving your wealth building needs. Track your salary structure, investment contributions, and eligible exemptions throughout the year to avoid last minute scrambling. Your tax savings compound when you integrate them with proper portfolio construction and long term planning.

Start your free analysis with Invsify to discover which tax saving solutions fit your specific situation and get personalized recommendations that maximize your savings while building real wealth.