Taxation Of Mutual Funds In India: STCG, LTCG & Budget 2024

Shlok Sobti

Taxation Of Mutual Funds In India: STCG, LTCG & Budget 2024

Your mutual fund returns look great on paper, until taxes take their cut. Understanding the taxation of mutual funds in India is essential if you want to keep more of what you earn. With the Budget 2024-25 changes reshaping tax rates and exemption limits, what you knew last year may no longer apply.

Equity funds, debt funds, and hybrid funds are all taxed differently. The distinction between short-term and long-term capital gains (STCG and LTCG) determines how much you owe, and getting this wrong can cost you thousands in unnecessary taxes. Yet most investors either ignore these details or rely on outdated information.

At Invsify, we help you make smarter, conflict-free investment decisions, and that includes understanding exactly how your gains are taxed. This guide breaks down the current tax rules, holding periods, and rates you need to know, so you can plan your investments with complete clarity.

Why mutual fund taxation matters for Indian investors

You invest to grow wealth, but your actual returns depend on what remains after taxes. Understanding the taxation of mutual funds in India directly affects how much money stays in your pocket. Every rupee you pay in taxes is a rupee that stops compounding, and over years, this difference becomes substantial. Investors who ignore tax implications often discover they earned 10% returns but kept only 6-7% after the government's share.

Tax rates changed significantly in Budget 2024-25, altering the landscape for equity and debt fund investors. What worked as a tax-efficient strategy last year may now cost you more. Without knowing these updates, you risk paying higher taxes than necessary or making investment decisions based on outdated rules.

Your net returns depend entirely on tax efficiency

Gross returns tell only half the story. If your equity fund delivers 15% annual growth but you pay LTCG tax on redemption, your actual post-tax return drops. The holding period determines whether gains qualify as short-term or long-term, and this classification directly changes your tax rate and final wealth accumulation. Two investors with identical gross returns can end up with vastly different final amounts based solely on when they sell and which fund category they chose.

Tax efficiency matters more as your portfolio grows. A Rs 10 lakh investment that grows to Rs 20 lakh triggers different tax liabilities depending on fund type and holding period. Equity funds taxed at one rate, debt funds at another, and hybrid funds follow their own rules. Choosing the wrong fund type for your investment horizon can cost you thousands in unnecessary taxes.

Investors who understand tax structures keep 15-20% more of their gains compared to those who plan investments without considering tax impact.

Budget changes reshape your investment planning

The government adjusts tax rates and exemption limits regularly through annual budgets. Budget 2024-25 introduced specific changes to LTCG exemption thresholds and tax percentages that affect millions of mutual fund investors. If you invested based on old tax assumptions, you need to recalculate whether your strategy still makes sense. Tax rules evolve, and your investment approach must evolve with them.

Recent changes impact both new investments and existing holdings. Your existing equity fund units purchased before the budget changes may have different tax treatment than units bought after. Knowing these dates and thresholds helps you time redemptions better and plan new investments with accurate tax projections. Ignoring these updates means leaving money on the table.

Different fund categories trigger different tax obligations

Equity funds, debt funds, and hybrid funds face separate tax rules. The government classifies funds based on their equity exposure percentage, and this classification determines your tax rate. An equity fund with 65% equity allocation gets taxed differently than a debt fund with 65% debt allocation. This distinction affects which fund you should choose for specific financial goals.

Your investment timeline should match the fund's tax structure. If you need money in two years, choosing a fund with favorable short-term capital gains treatment makes sense. For ten-year goals, funds with better LTCG rates work better. Many investors pick funds based only on past performance, completely ignoring how taxation will affect their actual take-home returns. Performance numbers you see in marketing materials are always pre-tax, so your real returns will be lower.

Understand how mutual fund taxation works in India

The government taxes you only when you sell mutual fund units and make a profit. Your purchase price (cost of acquisition) and sale price determine your capital gain, which becomes your taxable income. The taxation of mutual funds in India follows a straightforward principle: longer holding periods generally result in lower tax rates, encouraging investors to stay invested for wealth creation.

Mutual fund taxation differs entirely from how the government taxes your salary or business income. You pay nothing while your investment grows inside the fund. Tax liability arises only at redemption, when you convert units back to cash. This allows your money to compound without annual tax deductions, a significant advantage over traditional fixed deposits where you pay tax on interest every year.

How the government classifies funds for taxation

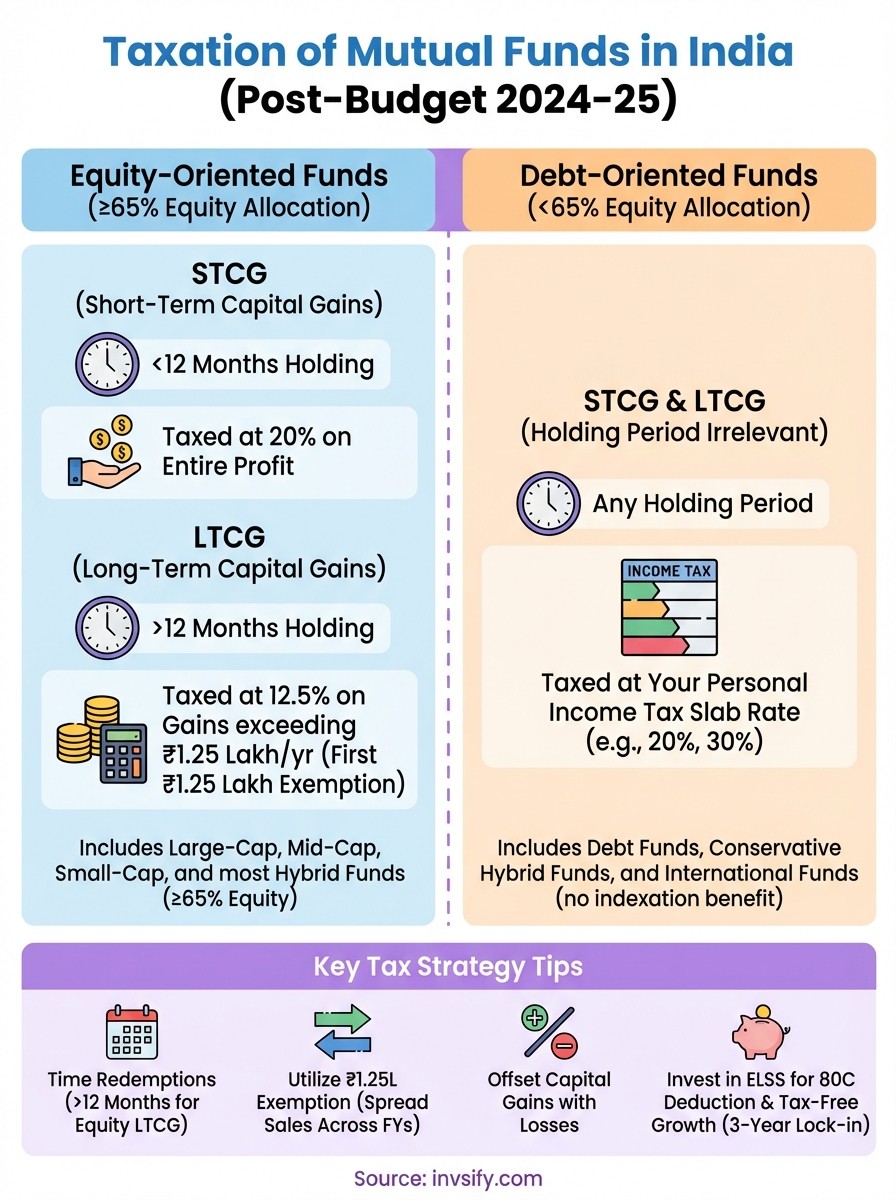

Fund classification determines your entire tax treatment. The government divides mutual funds into equity-oriented and debt-oriented categories based on their portfolio composition. A fund qualifies as equity-oriented if it maintains at least 65% of assets in Indian equity shares. Anything below this threshold gets treated as a debt fund, regardless of what the fund house calls it in marketing materials.

Hybrid funds follow the same rule. If your balanced advantage fund holds 68% in stocks and 32% in bonds, it receives equity fund tax treatment. Switch the ratio, and suddenly you face debt fund taxation rules. This classification happens automatically based on the fund's average monthly equity allocation, so you need to verify the exact category before investing.

Fund houses report the equity allocation percentage in their monthly factsheets, so check this document before making tax assumptions about any fund.

Holding period determines your tax rate

The clock starts ticking from your purchase date to your redemption date, and this duration decides whether you pay short-term or long-term capital gains tax. Equity funds require you to hold for more than 12 months to qualify for LTCG rates. Debt funds previously had a different holding period, but recent changes unified the structure.

Your holding period applies separately to each purchase. If you invest Rs 50,000 in January and another Rs 50,000 in July, these become separate transactions with different holding period calculations. When you redeem, the fund uses FIFO (First In First Out) method, selling your oldest units first. This matters because your oldest units may already qualify for LTCG treatment while newer purchases still count as STCG.

Tax rates vary significantly between short-term and long-term gains. Planning your redemptions around these holding period thresholds can save you substantial amounts in taxes, especially on large investment values.

Know the tax rules for equity funds and ELSS

Equity funds receive preferential tax treatment compared to other investment categories in India. The government defines equity funds as those maintaining at least 65% of assets in Indian equity shares, and this classification gives you access to lower tax rates. Your gains from these funds face taxation based on how long you hold the investment, with clear thresholds separating short-term from long-term treatment.

Understanding the taxation of mutual funds in India for equity categories helps you plan redemptions strategically. The tax burden on equity funds remains lower than debt instruments specifically to encourage long-term equity participation and capital market growth. These rules apply uniformly across all equity fund types, including large-cap, mid-cap, small-cap, and sectoral funds.

Short-term capital gains on equity funds

You pay STCG tax at 20% if you sell equity fund units within 12 months of purchase. This rate applies to your entire profit from the sale, calculated as the difference between your sale price and purchase price. No exemption threshold exists for short-term gains, so even a Rs 1,000 profit triggers the 20% tax liability.

Short-term gains get added to your income but taxed at this flat 20% rate regardless of your income tax slab. This means a person earning Rs 5 lakh annually and another earning Rs 50 lakh both pay the same percentage on equity STCG. You cannot offset these gains against losses from other income sources, though you can set them off against capital losses from other equity investments.

Long-term capital gains and exemption limits

Holding equity funds for more than 12 months qualifies your gains for LTCG treatment. Budget 2024-25 set the LTCG tax rate at 12.5% on gains exceeding Rs 1.25 lakh per financial year. Your first Rs 1.25 lakh in long-term gains remains completely tax-free, and you pay 12.5% only on amounts above this threshold.

Calculate your exemption across all equity fund redemptions in a financial year. If you book Rs 2 lakh in LTCG, you pay 12.5% tax on Rs 75,000 (the amount exceeding Rs 1.25 lakh), which equals Rs 9,375 in total tax. This exemption resets every April, so timing large redemptions across financial years can help you utilize the threshold twice.

Spreading large equity fund redemptions across two financial years lets you use the Rs 1.25 lakh exemption twice, potentially saving Rs 15,625 in taxes.

Special tax benefits of ELSS funds

ELSS (Equity Linked Savings Scheme) funds offer Section 80C deduction benefits up to Rs 1.5 lakh per year, reducing your taxable income. You invest in ELSS, claim the deduction when filing returns, and your tax liability drops immediately based on your income slab. These funds function exactly like other equity funds but come with a mandatory three-year lock-in period.

After the lock-in expires, ELSS gains face the same equity taxation rules described above. Your LTCG beyond Rs 1.25 lakh attracts 12.5% tax, while gains within three years (which you cannot book due to lock-in) would face 20% STCG treatment. ELSS combines upfront tax savings with long-term wealth creation, making it useful for both tax planning and equity exposure.

Know the tax rules for debt and hybrid funds

Debt and hybrid funds follow different tax structures compared to equity funds, and understanding these differences directly affects your investment returns. The government classifies any fund with less than 65% equity allocation as a debt-oriented fund, regardless of how the fund house markets it. These funds face taxation rules similar to other debt instruments, which means higher tax rates for most investors.

Recent budget changes eliminated the indexation benefit that debt funds previously enjoyed for long-term holdings. This shift significantly altered the tax landscape for debt fund investors, making the taxation of mutual funds in India more uniform but also removing a key advantage that helped reduce tax liability on inflation-adjusted gains.

Debt fund taxation follows your income slab

You pay tax on debt fund gains at your applicable income tax slab rate, whether you hold for the short term or long term. A person in the 30% tax bracket pays 30% on debt fund gains, while someone in the 20% bracket pays 20%. No differentiation exists between holding periods for debt funds, so selling after one month or ten years makes no tax difference.

Calculate your tax liability by adding the capital gains to your total annual income and applying your slab rate. If you earn Rs 12 lakh in salary and book Rs 2 lakh in debt fund gains, your total taxable income becomes Rs 14 lakh, pushing you into a higher tax bracket potentially. This integration with income tax slabs means debt fund taxation can become expensive for high earners compared to equity fund rates.

Debt fund investors in the 30% tax bracket pay more than double the tax rate compared to equity fund LTCG, making equity funds significantly more tax-efficient for wealth accumulation.

How hybrid funds get taxed based on equity exposure

Hybrid fund taxation depends entirely on whether the fund maintains 65% or more in equity shares. Check your hybrid fund's monthly factsheet to verify its equity allocation percentage, as this single number determines your entire tax treatment. Funds above the 65% threshold follow equity taxation rules, while those below face debt fund treatment.

Aggressive hybrid funds typically qualify for equity taxation by maintaining 65-80% equity exposure, giving you the 12.5% LTCG rate after one year. Conservative hybrid funds usually stay below 65% equity and therefore face taxation at your income slab rate. Balanced advantage funds actively shift between equity and debt, so their tax classification can potentially change, though most maintain equity status consistently.

Your investment choice between hybrid fund types should factor in tax implications alongside risk appetite. A conservative hybrid fund returning 8% but taxed at 30% leaves you with only 5.6% post-tax, while an aggressive hybrid delivering 10% taxed at 12.5% LTCG retains 8.75% after taxes.

Calculate, file, and reduce taxes legally

You need to calculate your mutual fund taxes correctly, report them in the right ITR forms, and apply legal strategies to minimize your liability. Most investors struggle with this process because the taxation of mutual funds in India involves tracking multiple purchases, calculating gains separately, and understanding which income schedule to use. Getting these steps wrong can trigger notices from the tax department or cause you to pay more than necessary.

Calculate your capital gains accurately

Your capital gain equals sale value minus purchase cost, but calculating this becomes complex when you make multiple investments in the same fund. Mutual funds use the FIFO (First In First Out) method, selling your oldest units first when you redeem. Track each purchase separately with date, units bought, and price per unit to determine which specific units you sold.

Most fund houses provide a capital gains statement that shows your transaction history with purchase dates, sale dates, and calculated gains. Download this statement from your AMC portal or request it from your distributor. Verify the calculations yourself by checking whether the holding period classification matches equity or debt rules and whether STCG or LTCG applies to each transaction.

File taxes through ITR forms correctly

Report your mutual fund capital gains in Schedule CG (Capital Gains) of your income tax return. Equity STCG goes under Section 111A, equity LTCG under Section 112A, and debt fund gains under income from capital gains at slab rates. You must file ITR-2 if you have capital gains from mutual funds, as ITR-1 does not allow reporting of such income.

Enter each transaction separately with purchase date, sale date, cost, and proceeds. The income tax portal calculates your tax liability automatically once you input these details. Keep your capital gains statements, contract notes, and bank statements ready as supporting documents in case the department requests verification.

Filing accurate capital gains details prevents future notices and helps you claim the Rs 1.25 lakh LTCG exemption correctly without triggering scrutiny.

Reduce your tax burden through legal strategies

You can legally reduce taxes by timing your redemptions to cross the 12-month holding period and qualify for lower LTCG rates instead of paying 20% STCG. Spread large redemptions across financial years to utilize the Rs 1.25 lakh exemption threshold twice. Offset capital gains against capital losses from other investments by selling losing positions strategically.

Invest in ELSS funds to claim Section 80C deductions up to Rs 1.5 lakh, reducing your taxable income immediately. Consider systematic withdrawal plans (SWP) instead of lump-sum redemptions to spread gains over multiple years and stay within lower tax brackets. Rebalance your portfolio by switching between funds of the same category without triggering exit loads, though switching still creates taxable events that you must report.

Conclusion

Understanding the taxation of mutual funds in India directly impacts your final returns and overall wealth accumulation over time. You now know the exact tax rates for equity funds (20% STCG, 12.5% LTCG beyond Rs 1.25 lakh), debt funds (taxed at your income slab), and how Budget 2024-25 changes affect your existing and future investments. The distinction between holding periods, fund classifications, and strategic redemption timing can save you thousands in unnecessary taxes every single year if applied correctly.

Planning your investments without properly considering tax implications means leaving substantial money on the table unnecessarily. You can maximize your post-tax returns by choosing the right fund categories for your specific timeline, timing redemptions strategically around holding period thresholds, and utilizing legal exemptions fully. Invsify helps you make conflict-free, tax-efficient investment decisions that align perfectly with your financial goals while minimizing your tax burden through AI-powered insights and completely transparent, unbiased advice.