How to Use a Term Insurance Calculator in India for Free

Shlok Sobti

How to Use a Term Insurance Calculator in India for Free

You know you need term insurance. Your family depends on your income. But when you check premium rates, the numbers seem random. One insurer quotes ₹500 per month, another wants ₹800 for the same cover. You wonder if you need 50 lakhs or 1 crore. The whole process feels like guesswork, and you hate making financial decisions blind.

Term insurance calculators solve this problem. These free online tools show you estimated premiums in seconds based on your age, income, and family situation. You can test different cover amounts, compare multiple insurers, and find a plan that fits your budget. Best part? Many calculators work without asking for your phone number or email.

This guide walks you through using term insurance calculators the right way. You will learn how premiums get calculated, how to pick the right coverage amount, which calculators to trust, and how to compare quotes properly. By the end, you will know exactly what term plan you need and what it should cost.

Why a term insurance calculator matters

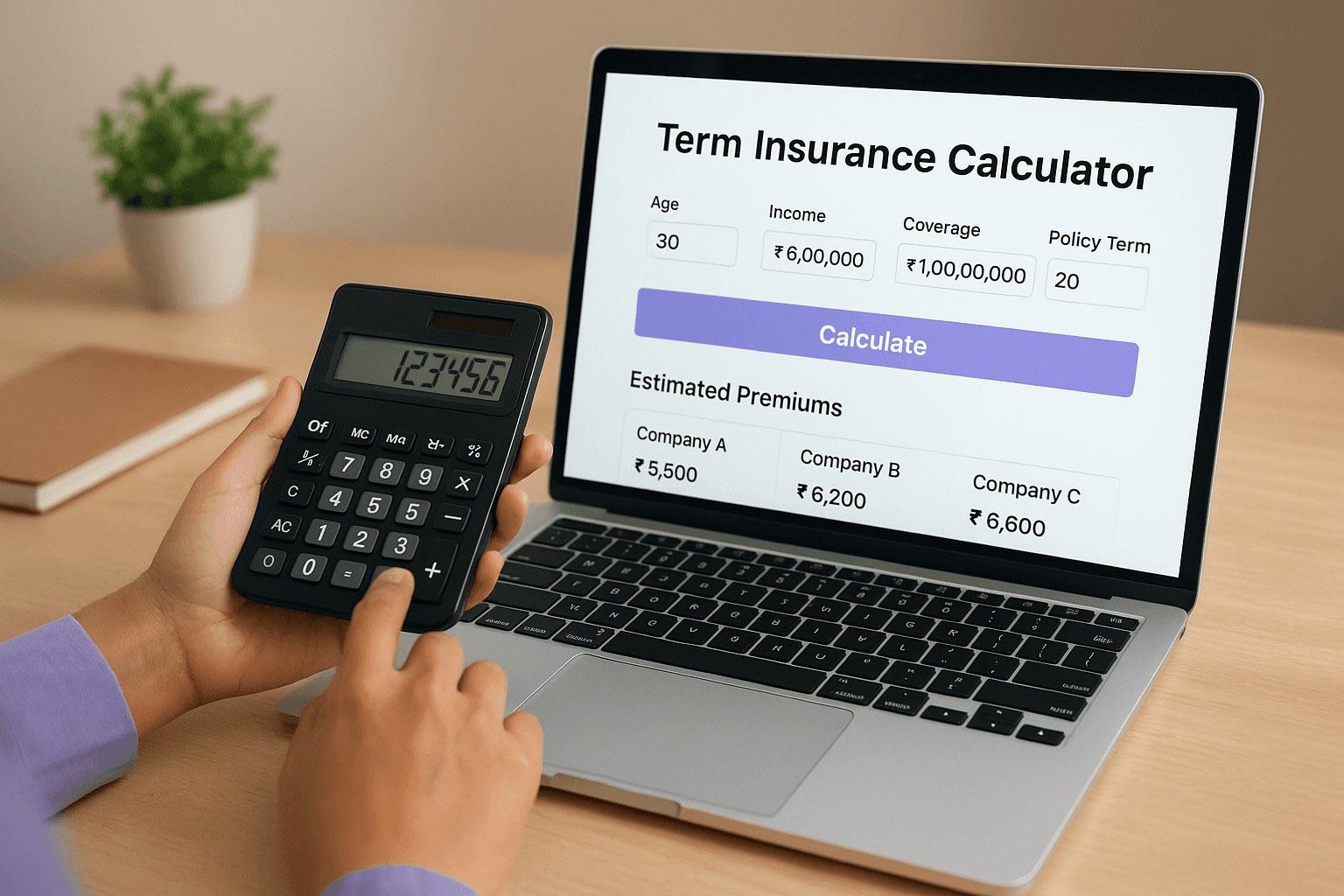

You could spend hours calling agents, filling forms at multiple insurance offices, and waiting days for quotes. A term insurance calculator india tool cuts this down to minutes. You type in your age, income, and desired cover, then see instant estimates from multiple insurers. This speed matters when you need to make decisions quickly or compare dozens of options before buying.

Saves time and money

Traditional insurance agents earn commissions that can add 10-15% to your premiums. They often push plans that benefit them, not you. A free calculator shows you direct premium rates without intermediary markups. You see what the actual policy costs, not what someone wants to charge you after their cut. This transparency helps you spot overpriced policies immediately.

Calculators also eliminate back-and-forth negotiations. You adjust coverage amounts, policy terms, and add-ons yourself. The tool recalculates instantly. No need to schedule meetings, wait for callbacks, or deal with sales pressure. Most calculators give accurate estimates in under 60 seconds.

Helps you avoid costly mistakes

Many people either buy too little coverage or pay for more than they need. A calculator based on your income and liabilities suggests appropriate cover amounts. It factors in your loans, dependents, and future expenses. This data-driven approach prevents the two most common errors: underinsurance that leaves your family struggling, or overinsurance that drains your monthly budget.

Term insurance calculators remove guesswork from one of your most important financial decisions.

You also catch red flags before committing. If one insurer charges double what others do for identical coverage, the calculator makes this obvious. You notice when certain riders or benefits inflate premiums unnecessarily. Side-by-side comparisons reveal which features actually matter and which ones are marketing fluff. This clarity protects you from impulse purchases driven by slick sales pitches.

Calculators give you control. You experiment with different scenarios without obligation. Want to see how quitting smoking affects your premium? Change one field. Curious what happens if you extend coverage by 10 years? The answer appears instantly. This freedom to explore options helps you understand what you are actually paying for.

Step 1. Learn how term insurance premiums work

Insurance companies calculate your premium based on risk assessment. They look at how likely you are to die during the policy term. The higher your risk, the more you pay. Understanding these factors helps you use a term insurance calculator india tool effectively. You will know which inputs matter most and how changing them affects your quote.

Your age drives the base premium

Insurers use age as the primary pricing factor. A 25-year-old pays significantly less than a 45-year-old for identical coverage. Your body is healthier, you face fewer chronic disease risks, and you have decades before typical mortality age. This simple math explains why buying term insurance early saves you thousands over the policy lifetime.

Delaying term insurance by just five years can increase your premiums by 30-40%.

Premium jumps happen in brackets. You might pay ₹8,000 annually at age 30, but that same plan costs ₹15,000 at age 40 for the same 1 crore cover. Most calculators show this clearly. Change your age input by a few years and watch the premium shift. This feature helps you understand the cost of waiting versus buying now.

Coverage amount affects premium linearly

Double your coverage, and you roughly double your premium. A 50 lakh policy might cost ₹400 monthly, while 1 crore costs ₹800. Insurers keep this relationship straightforward because their payout risk scales directly with the sum assured. Higher coverage means bigger claims, so they charge proportionally more.

This linear relationship makes calculators predictable. If you need to test different coverage amounts, you can estimate quickly. Want 75 lakhs instead of 50? Expect premiums about 50% higher. Planning helps you find the sweet spot between adequate protection and affordable payments.

Lifestyle habits create premium penalties

Smoking, tobacco use, and alcohol consumption increase your premiums by 30-60%. Insurers classify these as high-risk behaviors that shorten life expectancy. A non-smoking 35-year-old might pay ₹12,000 yearly, while a smoker pays ₹18,000 for identical coverage. Calculators always ask about tobacco use for this reason.

Your occupation matters too. High-risk jobs like mining, aviation, or defense carry premium surcharges. Office workers pay standard rates. Calculators from specific insurers account for this, though basic tools might not. Be honest about your work because false declarations void your policy during claims.

Gender affects pricing as well. Women typically pay 10-20% less than men for the same coverage. Statistical data shows women live longer on average, reducing insurer risk. Medical history plays a role if you have pre-existing conditions. Diabetes, heart disease, or blood pressure issues trigger medical tests and potential premium increases of 20-50%. Most free calculators assume you are healthy, but detailed ones let you input existing conditions for accurate estimates.

Step 2. Estimate the right cover for your family

Most people pick random numbers when choosing coverage. They ask friends, copy what colleagues bought, or let agents decide. This guessing game leaves families either underprotected or overpaying. You need a systematic approach to calculate your ideal cover amount. Several proven methods help you arrive at the right number before you even touch a term insurance calculator india tool.

Calculate using the income replacement method

Take your annual income and multiply it by 10 to 15. This simple formula ensures your family maintains their lifestyle if you die. Earning ₹10 lakhs yearly? Your coverage should range between ₹1 crore to ₹1.5 crore. The exact multiplier depends on your age and career stage. Younger professionals with 30-35 working years ahead should use 15. Those closer to retirement can use 10.

This method assumes your family invests the insurance payout conservatively at 6-8% annual returns. The interest income replaces your salary. A ₹1 crore investment generating 7% yields ₹7 lakhs yearly. Your family gets this amount without touching the principal, maintaining financial stability for decades.

Your term insurance cover should generate enough annual returns to replace your current income completely.

Factor in your debts and future expenses

Outstanding loans need immediate coverage. Add your home loan balance, car loans, personal loans, and credit card debt. If you owe ₹40 lakhs on a home loan and ₹5 lakhs in other debts, that is ₹45 lakhs your family must repay. Without insurance, they might lose your home or destroy their credit trying to clear these obligations.

Children's education costs grow yearly. Private school plus college fees for two kids can hit ₹50 lakhs over 15 years. Marriage expenses add another ₹20-30 lakhs per child. These future commitments do not disappear when you die. Your insurance should cover them. Add these amounts to your base calculation.

Use the Human Life Value formula

This comprehensive method accounts for everything. Calculate it this way:

Human Life Value = (Annual Income × Working Years Remaining) - (Living Expenses × Years)

Example calculation for a 30-year-old:

Annual income: ₹12 lakhs

Working years remaining: 30

Personal living expenses: ₹3 lakhs yearly

HLV = (₹12L × 30) - (₹3L × 30) = ₹360L - ₹90L = ₹2.7 crore

This number represents your economic value to your family. It shows the total income you will generate minus what you consume yourself. Your family needs this amount to maintain their standard of living without you.

Add all three calculations together, then find the average. This balanced approach prevents both under-insurance and excessive coverage. If income replacement suggests ₹1.5 crore, debt coverage needs ₹70 lakhs, and HLV shows ₹2.7 crore, your ideal coverage sits around ₹1.5 to ₹2 crore. This range gives you a solid starting point when you open any term insurance calculator.

Step 3. Gather your details before you start

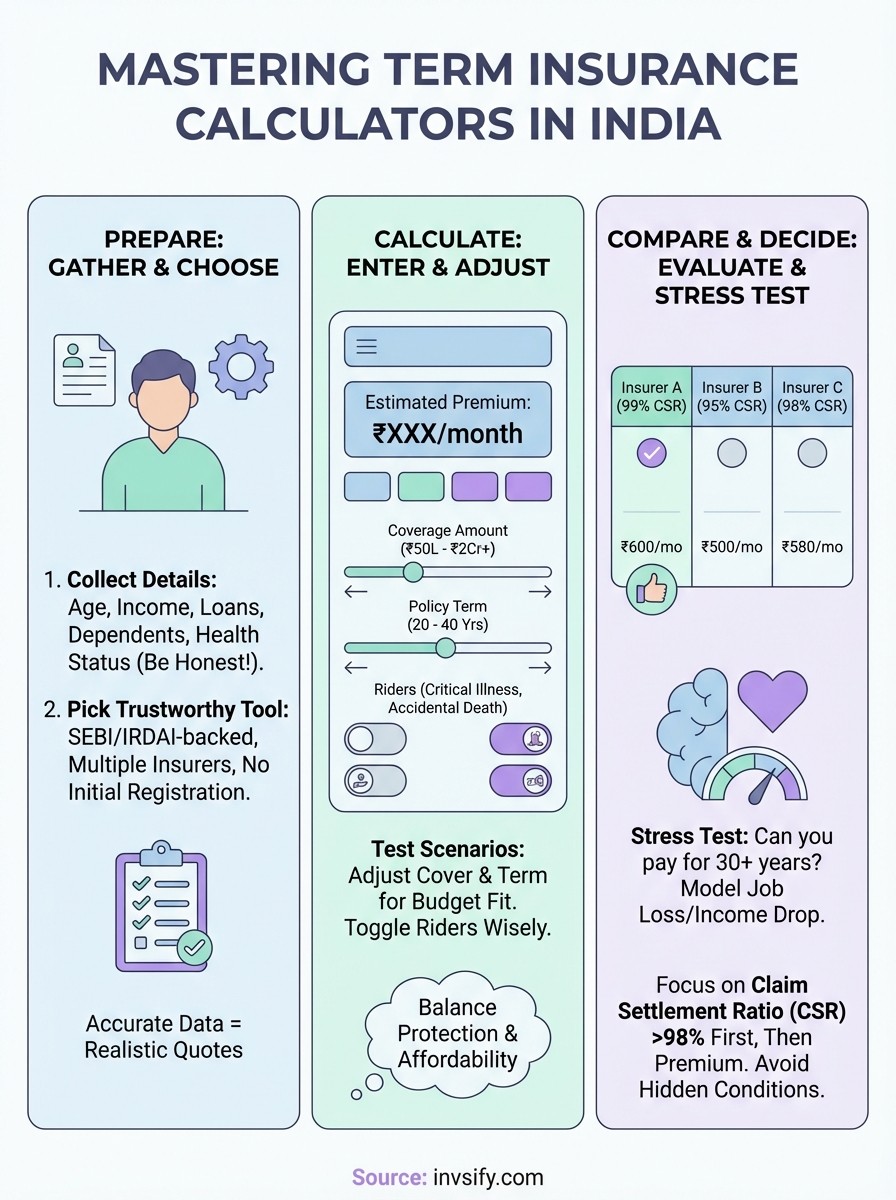

Opening a term insurance calculator india tool without preparation wastes time. You fill half the form, realize you need information you do not have, then abandon it. Later you start over and forget your previous inputs. Spending five minutes gathering documents saves you from this frustration. You complete the calculation in one sitting and get accurate quotes immediately.

Basic personal information you need

Every calculator requires your date of birth or current age. Grab your Aadhaar card, passport, or any government ID. You also need to know your exact annual income. Check your latest salary slip or Form 16 for this number. Do not guess. Rounding ₹8.5 lakhs to ₹10 lakhs changes your premium calculations significantly.

Keep these details ready before you start:

Your exact age in years

Annual gross income (before taxes)

Current employment type (salaried, self-employed, business owner)

Smoking or tobacco use status

Gender

Most calculators ask about your education level too. Graduate, postgraduate, or professional degrees affect how insurers assess your profile. Have this information memorized or written down.

Financial details to calculate accurately

Pull up your loan statements. You need exact outstanding balances for home loans, car loans, and personal loans. Add any credit card debt you carry month to month. Write these numbers on paper or in a notes app.

List your monthly household expenses next. Include rent or EMIs, school fees, utilities, groceries, and transport costs. Multiply this monthly total by 12 to get your annual family expenses. This number helps you determine if your chosen coverage adequately replaces your income.

Accurate financial inputs give you realistic premium quotes that match your actual needs.

Count your dependents. Your spouse, children, parents, or siblings who rely on your income. Note each dependent's age. Younger children need coverage for 20-25 more years until they become independent. Older parents might need 10-15 years of support. These timeframes guide your policy term selection in the calculator.

Step 4. Pick a trustworthy free calculator for India

Not all term insurance calculator india tools give you accurate results. Some inflate premiums to earn commissions. Others show outdated rates that do not match current market prices. You need a calculator that sources data directly from insurers and updates regularly. Trustworthy calculators display clear methodology and transparent calculations. They explain how they arrive at premium estimates instead of showing random numbers.

Look for SEBI-registered or insurer-backed tools

Calculators from SEBI-registered investment advisors or directly from insurance companies give you reliable data. These organizations face regulatory scrutiny. They cannot mislead you with false quotes or hidden markups. Check the website footer for registration numbers or regulatory certifications. Legitimate platforms display these credentials prominently.

Insurance aggregator sites licensed by IRDAI also maintain accuracy standards. They pull premium data through official APIs connected to insurer systems. This real-time integration means you see actual rates, not estimates someone typed into a spreadsheet months ago. Avoid calculators on random blogs or comparison sites that refuse to disclose their data sources.

Calculators backed by regulated entities give you premium quotes you can actually trust when you buy.

Check if the calculator shows multiple insurers

Single-insurer calculators push you toward one company regardless of whether they offer the best deal. You want a tool that displays quotes from at least 10-15 major insurers simultaneously. This comparison feature reveals which companies charge less for identical coverage. You spot premium differences of ₹200-500 monthly for the same 1 crore cover.

Quality calculators let you sort results by premium, claim settlement ratio, or insurer rating. You filter out companies with poor customer service track records. Look for tools that show you exact policy names alongside premiums. Generic results like "Term Plan A" tell you nothing useful. Specific names like "HDFC Click 2 Protect" or "ICICI iProtect Smart" help you research those exact products later.

Verify the calculator works without registration

Many tools force you to enter your phone number and email before showing results. This requirement exists solely to capture leads for sales calls. Trustworthy calculators give you premium estimates first. They ask for contact details only when you decide to proceed with buying. Test this by opening the calculator and checking if it demands registration upfront. If it does, find another option that respects your privacy during the research phase.

Step 5. Enter details and fine tune options

You open your chosen term insurance calculator india tool and see a form with multiple fields. Start with the mandatory basics before exploring advanced options. Most calculators follow a logical top-to-bottom flow. Fill each field carefully because one wrong input throws off your entire quote. Take your time here instead of rushing through and getting inaccurate results.

Fill in mandatory fields first

Begin with your age and gender. These two inputs create your base premium bracket. Select whether you consume tobacco or smoke. Remember that even occasional smoking counts as tobacco use. Insurers define this as any tobacco consumption within the past 12 months. Lying here creates claim rejection risks later.

Enter your annual income accurately. Type the exact number from your salary slip or tax return. The calculator uses this to suggest appropriate coverage amounts. Choose your occupation category next. Most tools offer options like salaried, self-employed, or business owner. Select the one that matches your primary income source.

Input your desired sum assured or coverage amount. If you completed Step 2 properly, you already know this number. Type ₹1 crore, ₹1.5 crore, or whatever amount you calculated earlier. Pick your policy term next. This determines how many years the coverage lasts. Common choices range from 20 to 40 years depending on your current age and when your dependents become financially independent.

Always enter your actual details, not idealized versions, to get premium quotes that match what you will actually pay.

Adjust coverage amount and policy term

Most calculators let you test different scenarios using sliders or dropdown menus. Drag the coverage slider from 50 lakhs to 2 crore and watch how premiums change. This interactive testing helps you find your affordability limit. Maybe 1.5 crore feels expensive but 1.25 crore fits your budget perfectly.

Experiment with policy terms too. A 30-year term might cost ₹15,000 yearly while a 25-year term costs ₹12,000. You save ₹3,000 annually by reducing coverage by five years. Decide if this trade-off makes sense. Will your children still need financial support after 25 years? Does your spouse have independent income by then? These questions guide your term selection.

Toggle optional riders and add-ons

Calculators display checkboxes for riders like critical illness cover, accidental death benefit, or waiver of premium. Each rider adds to your base premium. Critical illness riders typically increase premiums by 15-25%. They pay out if you get diagnosed with cancer, heart attack, or stroke even while you are alive.

Accidental death benefit doubles your payout if you die in an accident. This rider costs less than 5% extra premium but gives your family twice the coverage in accident scenarios. Waiver of premium excuses future payments if you become permanently disabled. Evaluate each rider individually. Check the box only if the added protection justifies the extra cost for your situation.

Step 6. Compare quotes and plan features

You see premium numbers from multiple insurers displayed on your term insurance calculator india screen. Resist the urge to pick the cheapest one immediately. A ₹500 monthly premium might look attractive until you discover that insurer settles only 85% of claims while a ₹600 option settles 98%. Those extra ₹100 monthly payments become irrelevant if your family faces claim rejection. Systematic comparison prevents this mistake.

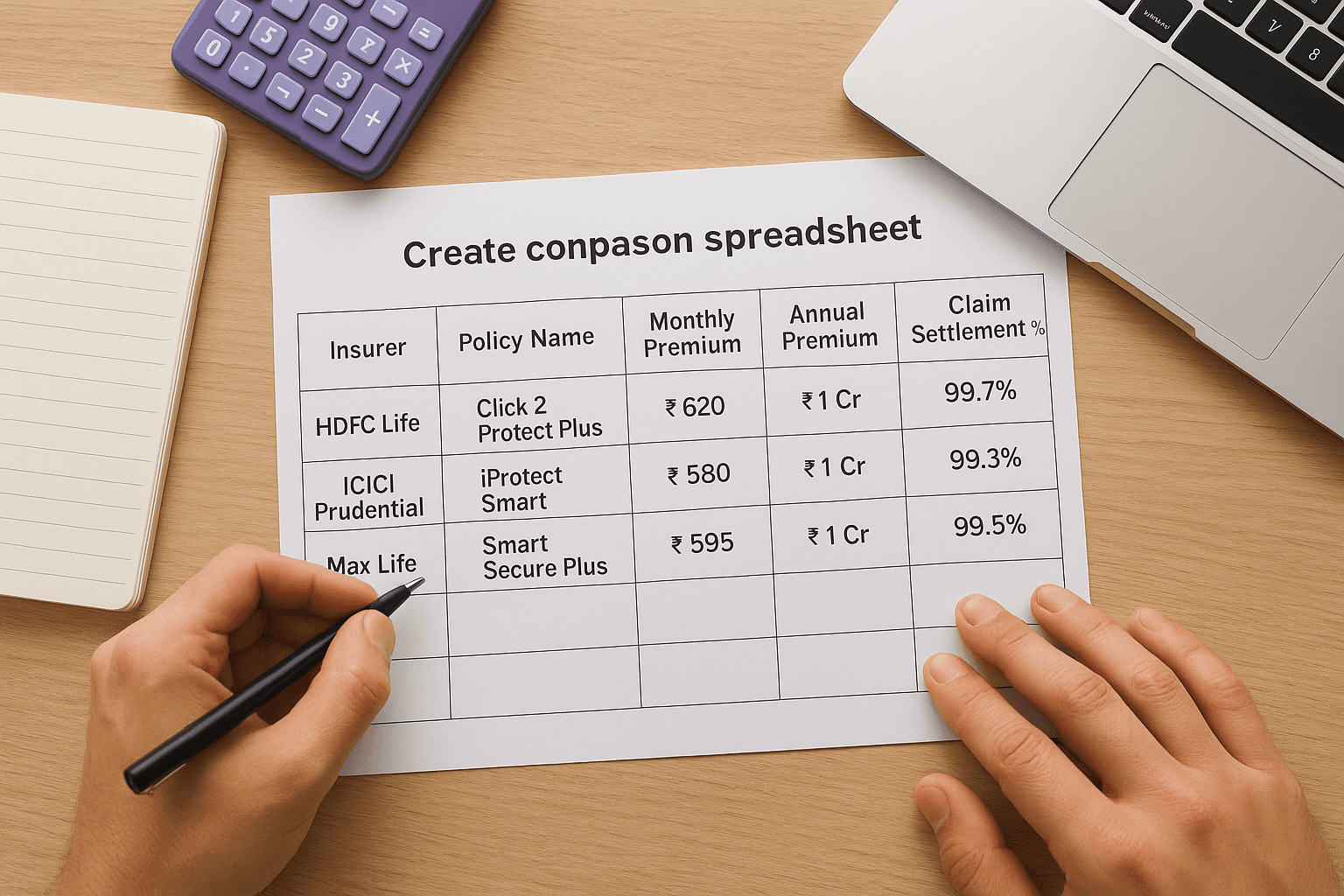

Create a comparison spreadsheet

Open a simple spreadsheet or use pen and paper. List five to seven insurers that show competitive premiums for your desired coverage. Create columns for insurer name, monthly premium, annual premium, policy term, sum assured, and claim settlement ratio. Add extra columns for any riders you selected like critical illness or accidental death benefit.

Copy the exact numbers from your calculator results into this sheet. Include the specific policy name each insurer offers because companies run multiple term plans with different features. HDFC offers both Click 2 Protect Plus and Click 2 Protect Super. These products have different premium structures and benefits despite similar names. Your spreadsheet prevents confusion later when you research individual policies.

Here is a basic template you can use:

Insurer | Policy Name | Monthly Premium | Annual Premium | Sum Assured | Claim Settlement % | Critical Illness Rider |

|---|---|---|---|---|---|---|

HDFC Life | Click 2 Protect Plus | ₹620 | ₹7,440 | ₹1 Cr | 99.7% | ₹95 |

ICICI Prudential | iProtect Smart | ₹580 | ₹6,960 | ₹1 Cr | 99.3% | ₹88 |

Max Life | Smart Secure Plus | ₹595 | ₹7,140 | ₹1 Cr | 99.5% | ₹92 |

Focus on these key metrics first

Premium differences matter but claim settlement ratio deserves equal attention. This percentage shows how many death claims an insurer approved versus rejected last year. Anything above 98% indicates reliable claim processing. Companies below 95% raise red flags. Check IRDAI annual reports for verified claim settlement data because some calculators display outdated percentages.

An insurer with 99% claim settlement ratio and slightly higher premiums protects your family better than a 94% ratio insurer charging less.

Policy term flexibility matters too. Some insurers let you extend coverage until age 85 or 90 while others stop at 75. If you want protection into your retirement years, this feature becomes crucial. Look for options that allow premium payment completion before retirement even if coverage continues beyond that point.

Sum assured limits tell you maximum coverage each insurer offers. Planning for ₹2 crore or ₹3 crore coverage? Verify each insurer actually provides these high limits at your age. Some companies cap coverage at ₹1.5 crore for applicants over 45. Your calculator might not show this restriction until you try to proceed with purchase.

Evaluate waiting periods and exclusions

Read the fine print boxes most calculators display below premium quotes. Insurers impose 12 to 24 month waiting periods for suicide claims. Some exclude adventure sports deaths or terrorism-related incidents. Companies with fewer exclusions provide broader protection even if they charge marginally higher premiums.

Check if the insurer requires medical tests. Non-medical limit policies skip health checkups if your coverage stays below ₹50 lakhs or ₹75 lakhs depending on your age. This speeds up policy issuance significantly. Medical test requirements appear in calculator details or insurer terms. Factor in the hassle of blood tests and waiting for results when comparing otherwise similar options.

Step 7. Use calculators without sharing personal data

Many term insurance calculator india tools trap you into giving your phone number and email before showing results. Sales teams then bombard you with calls for weeks. You want premium estimates without this hassle. Smart users test calculators first by checking if they can view quotes before registration. Look for tools that display "View Plans" or "Compare Quotes" buttons without forcing you through a contact form. These calculators respect your privacy during research.

Test the calculator anonymously first

Open the calculator in an incognito or private browsing window. This prevents cookies from tracking your activity across multiple visits. Fill in your age, income, coverage amount, and other financial details completely. Click through to the results page. Legitimate calculators show you premium ranges and insurer names immediately. They ask for contact details only when you click "Apply Now" or "Get Detailed Quote."

Privacy-focused calculators give you all comparison data upfront, requesting contact information only at the purchase stage.

If the tool blocks results and demands your mobile number, use these tactics. Enter your details into all fields except the phone number. Try clicking "Calculate" or "View Results" anyway. Some poorly designed forms let you bypass mandatory fields. Alternatively, bookmark that calculator and move to a different one. Dozens of comparison sites exist. At least five major platforms show quotes without registration.

Use temporary contact details strategically

Sometimes you need a detailed quote PDF or personalized calculation that requires registration. Create a disposable email address specifically for insurance research. Gmail lets you add +tags to your existing email without creating new accounts. Use yourname+insurance@gmail.com instead of your regular address. All emails still reach your main inbox but you can filter them easily.

For phone numbers, consider getting a secondary SIM card or virtual number through apps that provide Indian mobile numbers. These services let you receive verification OTPs without exposing your primary contact. Once you select an insurer and decide to purchase, switch to your real details. This approach gives you control over when sales teams can reach you instead of getting unwanted calls during your research phase.

Step 8. Stress test the quote against your budget

You found a term plan with attractive premiums on your term insurance calculator india tool. The monthly payment looks affordable right now. Before you proceed to buy, you need to verify that you can sustain these payments for 20 to 40 years without financial strain. Life circumstances change. Your income might stagnate, expenses could spike, or unexpected emergencies drain your savings. Stress testing reveals whether this policy remains affordable under realistic future scenarios.

Run through worst-case financial situations mentally. Imagine you lose your job for six months. Can you still pay premiums without touching emergency funds? What if medical expenses increase by ₹10,000 monthly? Does the term insurance payment force you to skip other critical financial goals? These questions expose vulnerabilities before you commit to decades of premium obligations.

Calculate total cost over policy lifetime

Take your annual premium and multiply by the policy term. A ₹12,000 yearly premium for 30 years totals ₹3,60,000 over the policy lifetime. This complete cost perspective matters more than focusing solely on monthly affordability. You commit to spending nearly ₹4 lakhs over three decades. Compare this total against the ₹1 crore sum assured your family receives. The math shows you pay 3.6% of the coverage amount for complete protection.

Break this calculation down further. Divide your annual premium by 12 to get the exact monthly outflow. Add this to your existing monthly commitments like EMIs, rent, school fees, and SIP investments. If your total fixed monthly obligations exceed 60% of your take-home salary, you overcommit financially. Aim to keep premiums below 2-3% of your annual income for sustainable long-term payments.

Your term insurance premium should feel like a necessary expense you barely notice, not a burden that strains your monthly budget.

Test against income fluctuations

Project your income three different ways. First, assume zero growth where your salary stays flat for five years due to economic downturns or career plateaus. Can you continue premium payments comfortably? Second, model a 10% pay cut scenario from job loss or business slowdown. Does cutting discretionary spending cover the premium? Third, calculate premiums as a percentage of your base salary excluding bonuses. Variable income components disappear during tough times but your premium obligation remains constant.

Build a simple monthly budget check:

Current monthly take-home: ₹80,000

Fixed obligations (EMI + rent + fees): ₹45,000

Term insurance premium: ₹1,000

Remaining for expenses: ₹34,000

Reduce your take-home by 20% to simulate income loss:

Reduced monthly take-home: ₹64,000

Fixed obligations: ₹45,000

Term insurance premium: ₹1,000

Remaining for expenses: ₹18,000

If the remaining amount covers essentials comfortably, your premium passes the stress test. Tight margins indicate you should reduce coverage slightly or extend the policy term to lower annual premiums.

Step 9. Avoid common mistakes people make

People rush through term insurance calculator india tools and make preventable errors that cost them money or leave their families underprotected. You might enter wrong details, misunderstand results, or focus on the wrong comparison factors. These mistakes compound over time because term insurance locks you into decades of premium payments. Catching these errors before you buy saves you from regret later. Understanding common pitfalls helps you use calculators correctly and choose policies that actually protect your family.

Hiding medical conditions or lifestyle habits

You might feel tempted to select "non-smoker" even though you smoke occasionally or to skip mentioning your diabetes in the calculator. This dishonesty gives you artificially low premium quotes that do not reflect what you will actually pay. When you apply for the policy, insurers conduct medical tests that reveal these conditions. Your real premium jumps by 30-50%, destroying your budget planning.

Worse consequences happen during claims. Insurers investigate thoroughly when someone dies. They review medical records, interview doctors, and check lifestyle patterns. If they discover you lied about smoking, diabetes, or heart conditions, they reject your claim completely. Your family receives nothing despite years of premium payments. The calculator exists to help you plan accurately, not to give you false hope through manipulated inputs.

Always enter your actual health status and lifestyle habits in calculators to get premium quotes that match what you will actually pay.

Buying based only on the lowest premium

The cheapest quote often comes from insurers with poor claim settlement ratios or terrible customer service. You save ₹200 monthly now but risk claim rejection that costs your family crores later. Premium differences of ₹300-500 monthly between insurers matter less than whether they actually pay claims when your family needs them. Focus on insurers with 98%+ claim settlement ratios first, then compare premiums within that filtered group.

Lowest premiums also hide coverage gaps. Some insurers exclude common death causes or impose strict documentation requirements during claims. Others delay claim processing for months while your family struggles financially. Check what the base policy actually covers before celebrating low premiums. A comprehensive plan costing ₹600 monthly beats a restricted plan at ₹450 if the expensive one protects against scenarios the cheap one excludes.

Ignoring claim settlement track records

Calculators display premiums prominently but bury claim settlement percentages in fine print or omit them completely. You compare five insurers based solely on monthly payments without checking how many families actually received money when someone died. One insurer settling 85% of claims means 15 out of 100 families got rejected. That rejected family might be yours.

Research each insurer's track record separately after getting calculator results. Visit the IRDAI website and download their annual claim settlement reports. Look for consistent high settlement rates over three to five years, not just one good year. Companies maintaining 98-99% settlement ratios demonstrate reliable claim processing. Cross-reference this data with your calculator results to eliminate risky insurers regardless of their attractive premiums.

Key takeaways and next steps

A term insurance calculator india tool gives you premium estimates in minutes without waiting for agent callbacks or office visits. You learned how premiums work, how to calculate the right coverage amount for your family, and which calculator features matter most. Remember to enter accurate details about your age, income, health, and tobacco use. Compare quotes based on claim settlement ratios first, then premiums. Avoid the trap of choosing the cheapest option that might reject your family's claim later.

Start by using a free calculator today to test different coverage amounts and policy terms. Once you know what you need, research the top three insurers from your results. Beyond term insurance, your family needs a complete financial plan that includes investments, emergency funds, and tax optimization. Get personalized wealth advice from Invsify to build a comprehensive protection strategy that covers all your financial goals.