Understanding Investment Risk: What It Is and How to Manage

Shlok Sobti

Understanding Investment Risk: What It Is and How to Manage

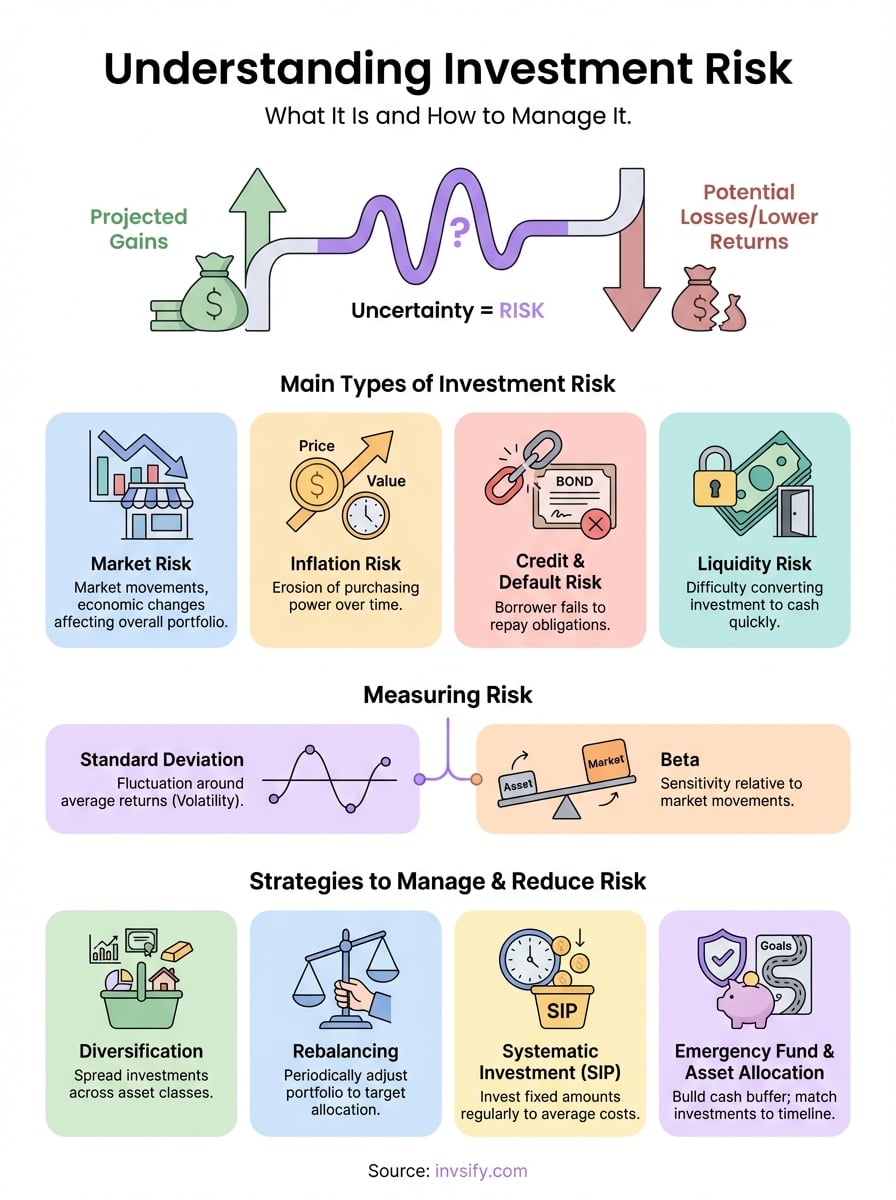

Investment risk is the possibility that your investment returns will differ from what you expect. When you invest money, there's no guarantee you'll earn the projected gains or even get back your full principal amount. The value of your stocks, mutual funds, or bonds can go down due to market movements, company performance, inflation, or economic changes. This uncertainty is what we call risk. Higher potential returns typically come with higher risk, while safer investments usually offer lower returns.

This guide breaks down everything you need to know about investment risk as an Indian investor. You'll learn how to evaluate your own comfort level with uncertainty, understand the main types of risks affecting your portfolio, and discover practical ways to measure risk in your holdings. Most importantly, we'll show you proven strategies to manage and reduce risk without giving up on your financial goals. Whether you're starting your investment journey or looking to optimize your current portfolio, understanding risk helps you make smarter decisions about your money.

Why understanding investment risk matters

Your wealth depends on the investment decisions you make today. Without understanding investment risk, you might choose investments that don't match your goals, panic during market downturns, or miss opportunities for growth. Many Indian investors lose money not because markets fail them, but because they don't recognize the risks they're taking.

Risk awareness helps you avoid costly mistakes that can derail your wealth-building plans. When you understand risk, you can anticipate potential losses and prepare for them instead of reacting emotionally when your portfolio drops. This knowledge prevents you from selling at the worst times or chasing unrealistic returns that expose you to dangers you can't handle.

Understanding risk transforms you from a reactive investor into a strategic planner who makes informed choices.

Your ability to reach financial milestones like buying a home, funding your child's education, or retiring comfortably depends on matching your investments to your risk capacity. If you take too little risk, inflation eats away at your purchasing power and you might fall short of your goals. If you take excessive risk, one market crash could wipe out years of savings. The right balance comes from understanding what you're dealing with and how much uncertainty fits your situation and timeline.

How to assess your own risk level

Your risk tolerance depends on both your financial capacity and your emotional ability to handle market volatility. Start by examining your investment timeline, since longer horizons give you more time to recover from losses. If you need money within three years, you can't afford significant risk. If you're investing for retirement 20 years away, you have much more flexibility to ride out market swings.

Your personal risk factors

Age plays a crucial role in understanding investment risk and setting your boundaries. A 25-year-old can typically accept more volatility than a 55-year-old because they have decades to recover from losses. Your personality matters too. Some investors sleep soundly through 20% portfolio drops, while others panic and sell at the bottom. Ask yourself: How would you react if your portfolio lost ₹1 lakh in a week? If that scenario keeps you awake at night, you need lower-risk investments regardless of your age.

Your emotional response to losses matters as much as your financial capacity to absorb them.

Your financial situation

Calculate how much you can genuinely afford to lose without affecting your lifestyle. Take your total savings and subtract your emergency fund (six months of expenses), any money needed for short-term goals, and funds you absolutely cannot risk. What remains is your true risk capital. Your income stability matters too. If you have a secure government job with steady income, you can take more risk than someone with variable freelance earnings. Debt levels also affect your capacity. High EMI payments reduce your ability to weather investment losses, so you need safer allocations until you clear those obligations.

Main types of investment risk in India

Understanding investment risk requires knowing the specific dangers that can affect your portfolio. Indian investors face several distinct types of risk that operate differently and demand separate attention. Each risk type can reduce your returns in unique ways, and they often interact with each other to compound losses. Recognizing these categories helps you identify which risks affect your current holdings and prepare appropriate defenses.

Market risk

Market risk affects your investments when the broader stock market or specific sectors decline. Your equity mutual funds or direct stock holdings can lose value even if the companies are performing well, simply because the overall market is falling. In India, events like policy changes, monsoon failures affecting agricultural stocks, or global economic concerns regularly trigger market-wide drops. The Sensex fell nearly 40% during the 2020 pandemic crash, showing how market risk impacts all equity investors regardless of their specific holdings.

This type of risk cannot be eliminated through diversification within the same asset class. If the entire Indian stock market drops 20%, your diversified equity portfolio will likely fall too, though perhaps not by the full 20%. Systematic risk, another term for market risk, requires protection through asset allocation across different categories like debt, gold, and real estate rather than just holding more stocks.

Inflation risk

Inflation erodes your purchasing power over time, making your investment returns less valuable in real terms. If your fixed deposit earns 6% annually but inflation runs at 7%, you're actually losing money in terms of what you can buy with those returns. This risk particularly affects conservative investors who keep too much money in savings accounts or fixed deposits that barely keep pace with rising prices.

Real returns, not just nominal returns, determine whether your wealth actually grows or shrinks over time.

Indian inflation often runs higher than developed markets, making this risk especially relevant for your portfolio. Your retirement corpus might seem large today, but if inflation averages 6% annually, prices double roughly every 12 years. What costs ₹50 lakhs today will cost ₹1 crore in 12 years, so your investments must grow faster than inflation to maintain your standard of living.

Credit and default risk

Credit risk emerges when borrowers fail to repay their obligations on time or at all. Corporate bonds, debt mutual funds, and fixed deposits all expose you to this danger. If a company whose bond you hold goes bankrupt, you might lose your entire investment in that security. Indian markets saw several high-profile defaults in recent years, including infrastructure companies and NBFCs, which devastated investors who thought their debt investments were safe.

Credit rating agencies like CRISIL and ICRA assess this risk, but their ratings aren't guarantees. AAA-rated securities can get downgraded quickly when companies face unexpected troubles. Your debt mutual funds carry credit risk based on the quality of bonds they hold. Schemes investing in lower-rated papers offer higher yields but expose you to greater default probability. Banking deposits remain safer due to DICGC insurance coverage up to ₹5 lakhs per depositor per bank.

Liquidity risk

Liquidity risk appears when you cannot easily convert your investment into cash without significant loss. Real estate exemplifies this problem in India, where selling property can take months or years and often requires accepting prices below your expectations. Some debt mutual funds also faced liquidity issues during the 2020 credit crisis, preventing investors from redeeming their units smoothly.

Certain equity stocks with low trading volumes present liquidity challenges too. Small-cap stocks might double in price on paper, but selling large quantities pushes prices down because buyers are scarce. Lock-in periods on tax-saving instruments like ELSS funds create deliberate liquidity constraints, though for your benefit. Balance your portfolio between liquid assets you can access quickly and less liquid investments that might offer higher returns over extended periods.

Currency risk

Currency fluctuations affect your returns when you invest in international assets or hold foreign currency. If you invest in US stocks when the rupee trades at ₹80 per dollar, then the rupee strengthens to ₹75, your investment loses value in rupee terms even if the dollar price stays constant. Indian investors using international mutual funds or direct foreign investments face this additional layer of uncertainty beyond the underlying asset's performance.

Global mutual funds that invest abroad carry inherent currency risk that adds volatility to your portfolio. Sometimes this works in your favor when the rupee weakens, but it can reduce returns when the rupee appreciates. This risk doesn't affect purely domestic investments in Indian stocks, bonds, or real estate, making it a consideration only for those diversifying internationally.

Measuring risk in your investments

Quantifying risk helps you compare different investments objectively and track your portfolio's true exposure. While understanding investment risk conceptually matters, you need concrete numbers to make informed decisions about where to put your money. Financial analysts use several statistical measures to capture different aspects of risk, each revealing something unique about how an investment behaves. These metrics transform vague feelings about danger into measurable data you can analyze and act upon.

Standard deviation and volatility

Standard deviation measures how much an investment's returns fluctuate around their average over time. A mutual fund with 15% average annual return but 25% standard deviation swings wildly, sometimes gaining 40% and other times losing 10%. Your portfolio with lower standard deviation delivers more predictable results, making it easier to plan and reducing the emotional stress of investing. High volatility means larger price swings in both directions, creating opportunities for gains but also exposing you to steeper losses.

Indian equity funds typically show higher standard deviation than debt funds, reflecting the inherent volatility differences between asset classes. You can find this metric in fund fact sheets or financial websites. Compare it across similar funds to identify which ones offer smoother journeys toward their returns. Lower volatility doesn't always mean better investments, but it helps you understand what kind of ride you're signing up for.

Beta and market sensitivity

Beta tells you how much an investment moves relative to the overall market. A beta of 1.0 means the investment moves exactly with the market, while 1.5 suggests it moves 50% more than market swings. If the Sensex drops 10%, a fund with 1.5 beta typically falls 15%. Defensive investments like gold or debt show betas below 1.0, offering stability when markets tumble.

Beta reveals whether your investment amplifies or dampens market movements, helping you predict behavior during crashes.

This measure matters most for equity investments where market correlation runs high. You want some high-beta holdings when you're confident markets will rise, but they hurt more during downturns. Balanced portfolios mix different beta levels across holdings to smooth out overall volatility while maintaining growth potential.

Risk-adjusted returns

Sharpe ratio and other risk-adjusted metrics show whether your returns justify the risks you're taking. A fund returning 12% with minimal volatility deserves more credit than one returning 14% with wild swings. These ratios divide returns by risk measures to calculate efficiency. Higher ratios indicate better performance per unit of risk, helping you identify managers who deliver results without excessive danger to your capital.

Calculate these metrics yourself or review them on fund comparison platforms. Your goal isn't just high returns but high returns relative to the uncertainty you endure to achieve them.

Strategies to manage and reduce risk

Managing investment risk effectively protects your capital while allowing your wealth to grow steadily over time. You can't eliminate risk entirely, but you can reduce its impact on your portfolio through proven strategies that balance protection with growth. Understanding investment risk leads naturally to implementing these defensive techniques that successful investors use to preserve wealth through market cycles. Each strategy addresses different aspects of risk, and combining multiple approaches creates the strongest protection for your financial future.

Diversification across asset classes

Spreading your investments across different asset types reduces the damage any single category can inflict on your portfolio. When you hold only stocks and the market crashes 30%, your entire portfolio suffers that loss. Adding debt instruments, gold, and real estate means losses in one area get offset by stability or gains elsewhere. Indian investors benefit from allocating between equity mutual funds, debt funds, gold bonds or ETFs, and perhaps real estate or REITs depending on their capital and goals.

Different assets react differently to the same economic events. Inflation might hurt bonds but boost commodity prices and real estate values. Rising interest rates typically pressure stocks but improve returns on new fixed deposits. Your diversified portfolio smooths out these opposing movements, delivering steadier overall returns than concentrated holdings in one asset class. Aim for allocations that match your risk tolerance, with younger investors holding more equities and older investors shifting toward debt as retirement approaches.

Regular portfolio rebalancing

Your portfolio drifts away from your target allocation as different assets grow at different rates. If you started with 60% equity and 40% debt, a strong stock market rally might push you to 75% equity without you buying anything. This increases your risk exposure beyond your comfort level and leaves you vulnerable to the next downturn. Rebalancing means selling overweight positions and buying underweight ones to restore your target allocation.

Rebalancing forces you to sell high and buy low automatically, removing emotion from your investment decisions.

Schedule rebalancing at fixed intervals like annually or when allocations drift 5-10% from targets. This discipline prevents your portfolio from becoming too aggressive during bull markets or too conservative during crashes. You lock in gains from winning assets and add to positions that fell, positioning yourself for the next cycle. Tax implications matter for Indian investors, so consider rebalancing within tax-advantaged accounts or timing sales to minimize capital gains taxes on equity holdings.

Systematic investment approach

Investing fixed amounts regularly through Systematic Investment Plans (SIPs) reduces the impact of market timing risk on your returns. Instead of trying to predict the best entry points, you buy consistently regardless of market levels. This rupee cost averaging means you purchase more units when prices fall and fewer when prices rise, lowering your average cost per unit over time. Your emotions stay out of the equation because you automate the process.

Start SIPs in equity mutual funds for long-term goals and continue them through market crashes without stopping. Panic selling during downturns locks in losses permanently, while continuing to invest buys assets at discounted prices that generate strong returns during recovery. Your discipline during bad markets determines your wealth during good ones. Increase SIP amounts annually as your income grows to accelerate wealth building and maintain the real value of your contributions against inflation.

Emergency fund and asset allocation

Building a cash emergency fund before aggressive investing protects you from forced liquidation during market lows. Keep six months of expenses in savings accounts or liquid funds that you can access instantly without selling investments. This buffer lets you ride out job losses, medical emergencies, or other crises without touching your long-term portfolio when markets might be down 30-40%.

Asset allocation based on your goals and timeline forms your primary defense against inappropriate risk. Money needed within three years belongs in debt instruments or fixed deposits, not equity markets. Retirement funds decades away can tolerate higher equity exposure because you have time to recover from crashes. Write down your allocation strategy matching each goal to appropriate investments, then execute it systematically. Review annually but avoid changing strategies based on short-term market movements or predictions about the future.

Final thoughts

Understanding investment risk transforms you from an uncertain investor into a confident decision-maker who knows exactly what you're dealing with. Your wealth depends on balancing growth opportunities with appropriate protection, and that balance comes from knowing which risks affect your portfolio and how to manage them. The strategies we covered work together to create a resilient investment approach that withstands market turbulence while pursuing your financial goals.

You don't need to navigate investment risk alone or rely on conflicting advice from online forums. Modern AI-powered advisory platforms offer personalized guidance that adapts to your specific situation, risk tolerance, and goals. Get started with Invsify's AI-driven investment advisor to receive conflict-free recommendations backed by data analysis and SEBI-registered expertise. Your financial future deserves professional guidance that puts your interests first without hidden fees or biased product pushing.