Vanguard Asset Allocation Models: How They Work and Why

Shlok Sobti

Vanguard Asset Allocation Models: How They Work and Why

Vanguard manages over $9 trillion in global assets, and a big reason for that trust comes down to one thing: a disciplined approach to portfolio construction. Vanguard asset allocation models are among the most referenced frameworks in investing, built around the simple idea that how you split your money between stocks, bonds, and short-term reserves matters more than which individual funds you pick. Whether you're a conservative investor or someone with a higher appetite for risk, these models offer a structured starting point.

For Indian investors, Vanguard's models aren't directly investable products. But the principles behind them, diversification based on risk tolerance, time horizon, and financial goals, are universally applicable. Understanding these frameworks helps you evaluate your own portfolio with sharper clarity, especially when you're making decisions about mutual funds, equities, or debt instruments available in India.

At Invsify, we use AI-driven advisory to help you build a portfolio that aligns with your goals, much like the logic behind Vanguard's allocation models, but tailored to Indian markets and your specific financial situation. This article breaks down how Vanguard's models work, the thinking behind each allocation tier, and how you can apply those principles to your own wealth strategy.

What Vanguard asset allocation models are

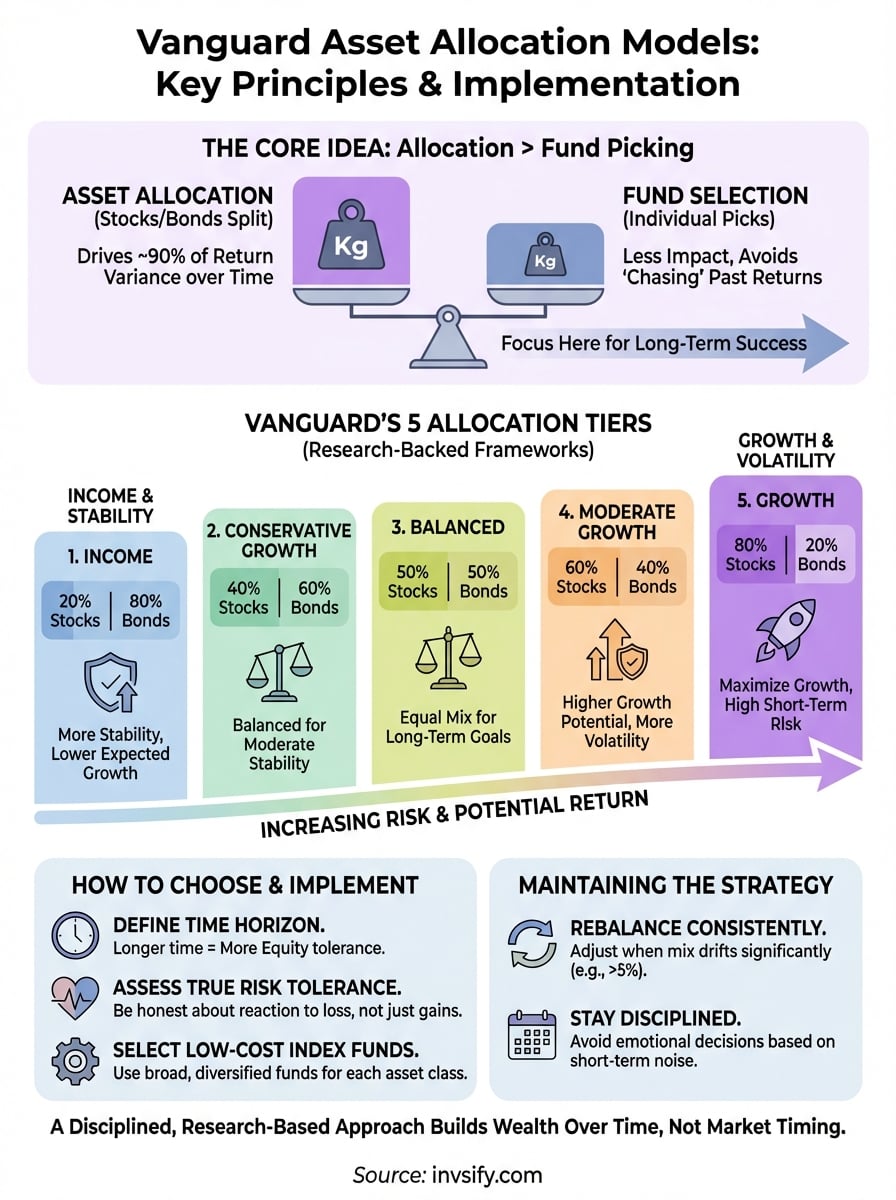

Vanguard asset allocation models are pre-built portfolio frameworks that divide investments across three core asset classes: stocks (equities), bonds (fixed income), and short-term reserves (cash equivalents). Each model represents a different risk level, ranging from income-oriented (more bonds) to growth-oriented (more stocks). Vanguard designed these models so that investors, whether managing their own portfolios or working with advisors, have a clear, research-backed starting point for building a portfolio that matches their goals and tolerance for volatility.

The allocation between asset classes, not the selection of individual securities, is the primary driver of long-term portfolio returns.

The core asset classes involved

Each Vanguard model is built around three building blocks: equities, fixed income, and short-term reserves. Equities generate growth over time but carry higher short-term volatility. Bonds provide income and stability, acting as a cushion when stock markets fall. Short-term reserves, such as money market instruments, protect capital and offer liquidity, though they generate the lowest returns. The balance between these three determines how your portfolio behaves during both bull and bear markets.

A growth-heavy allocation might put 80 to 100% of the portfolio in stocks and little to nothing in bonds. An income-focused allocation does the reverse, prioritizing bonds and reserves to reduce risk. Most investors land somewhere in between, depending on how many years they have before they need the money and how much short-term loss they can tolerate without making panic-driven decisions.

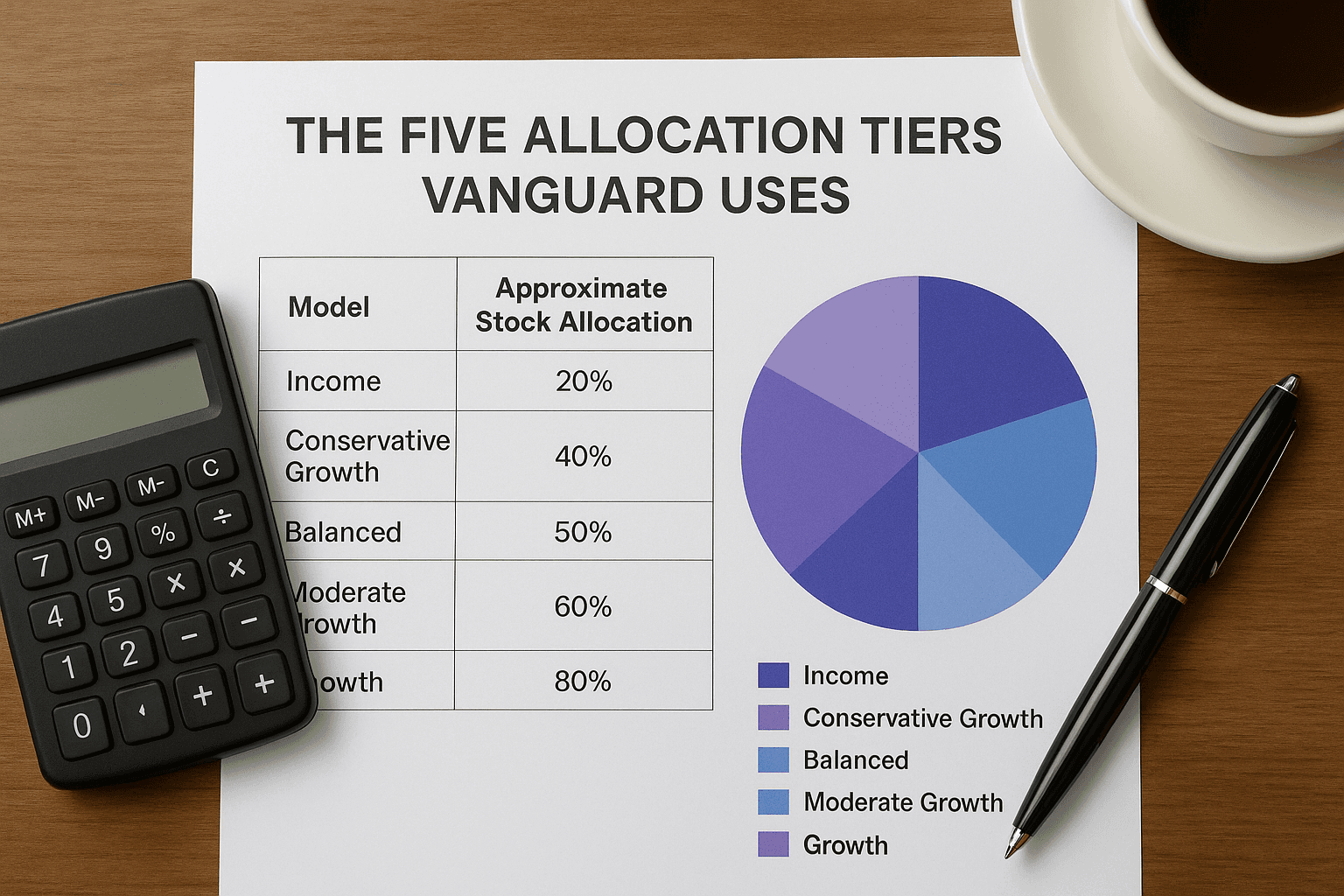

The five allocation tiers Vanguard uses

Vanguard organizes its models into five broad tiers based on the stock-to-bond ratio. These range from income (around 20% stocks, 80% bonds) to growth (around 80% stocks, 20% bonds), with conservative growth, balanced, and moderate growth sitting in between. Each tier reflects a different expected return and risk profile over a long-term investment horizon.

Model | Approximate Stock Allocation | Approximate Bond Allocation |

|---|---|---|

Income | 20% | 80% |

Conservative Growth | 40% | 60% |

Balanced | 50% | 50% |

Moderate Growth | 60% | 40% |

Growth | 80% | 20% |

These numbers are not arbitrary. Vanguard backs each allocation tier with decades of capital markets research, analyzing how different mixes have performed across economic cycles. The goal is to give you a statistically grounded framework, not a guess, so your portfolio construction starts from a position of evidence rather than intuition.

Why asset allocation matters more than fund picking

Most investors spend the bulk of their time researching which fund to buy next. That instinct is understandable, but research consistently shows it's the wrong problem to focus on. The division of your portfolio across asset classes, not the specific funds within those classes, drives the majority of long-term investment outcomes. Vanguard's own research, and multiple independent studies, point to asset allocation as the dominant factor in determining how your portfolio performs over time.

Your allocation decision explains most of your portfolio's return variance, far more than any individual fund selection ever will.

The research behind the decision

A landmark 1986 study by Brinson, Hood, and Beebower found that asset allocation explained roughly 90% of the variation in portfolio returns over time. While the exact figure has been debated since, the core finding holds: how you split between stocks and bonds matters far more than which specific securities you hold within those buckets. Vanguard asset allocation models are built on this same evidence base, which is why the framework focuses first on getting the mix right, then on selecting low-cost, diversified funds to fill each category.

Why chasing returns fails most investors

When you shift money into last year's top-performing fund, you're essentially making a bet based on backward-looking data. Markets mean-revert, sectors rotate, and the fund that outperformed last year often underperforms the next. This behavior, known as performance chasing, consistently destroys returns for retail investors.

A stable asset allocation forces discipline into your investment process. Instead of reacting to short-term noise, you maintain a target mix and rebalance when your portfolio drifts. That structure removes emotion from the equation, which is where most investment mistakes actually happen.

How Vanguard builds its model portfolios

Vanguard asset allocation models don't emerge from gut instinct or market trends. Vanguard's investment strategy group starts the process with capital markets research, projecting the expected returns, volatility, and correlations of different asset classes over a 10-year horizon. That data-driven foundation is what separates a structured model portfolio from a rough guess about where markets might go.

Starting with capital markets assumptions

Vanguard publishes its Capital Markets Model (VCMM) annually, which runs thousands of simulations to estimate how different asset mixes might perform across a wide range of economic scenarios. These simulations account for inflation, interest rate shifts, equity valuations, and global economic conditions. The output gives Vanguard a probability-weighted view of returns, not a single prediction, so each allocation tier reflects a realistic range of outcomes rather than a best-case projection.

The value of a model portfolio isn't that it predicts the future accurately; it's that it forces you to think in probabilities and manage risk before a market event forces you to react.

Building with broad, low-cost index funds

Once the target allocation is set, Vanguard fills each tier using broadly diversified index funds that cover domestic equities, international equities, and fixed income. The emphasis on low expense ratios is deliberate. Vanguard's research shows that costs compound over time and directly reduce net returns, so every basis point saved in fees translates into measurable long-term gains. Within each asset class, the funds span thousands of securities, reducing concentration risk significantly. This broad exposure means you're not betting on a single sector or region to carry your portfolio, but rather capturing market-wide returns across geographies and industries.

How to choose a model for your goal and risk

Picking the right model starts with two honest answers: how long until you need the money, and how much short-term loss you can absorb without selling. Most investors underestimate both variables. They overstate their risk tolerance in a bull market, then sell in panic during a correction. Vanguard asset allocation models are designed to prevent that by anchoring your allocation to facts about your situation, not your mood in the moment.

Start with your time horizon

Your time horizon is the clearest signal for which tier you belong in. A 25-year-old saving for retirement has decades to recover from a market downturn, which makes a growth-heavy allocation rational. Someone five years from a major financial goal, whether that's buying a house or funding a child's education, needs more stability and less volatility, pointing toward a conservative growth or balanced model. The further out your goal, the more equity exposure you can justify carrying.

Time in the market matters more than timing the market, and your allocation should reflect how much time you actually have.

Match the model to your risk tolerance

Risk tolerance isn't just about math; it's about behavior. If a 30% portfolio drop would force you to sell, then an 80% equity allocation is wrong for you regardless of your time horizon. Be honest about your reaction to loss, not your ideal reaction, but your actual one. A useful test is to look at how you responded during a past market drop. If you held, you likely have higher tolerance. If you sold, a more conservative model will keep you invested through the next correction, which is what actually builds wealth over time.

How to implement and maintain the allocation

Once you've identified the right model for your goals and risk tolerance, implementation is straightforward but requires consistency. Vanguard asset allocation models work best when you treat your target percentages as fixed commitments, not suggestions you revisit every time markets move. Your job at this stage is to select low-cost, diversified funds that represent each asset class in your chosen ratio, then automate contributions so you're not making timing decisions month to month.

Opening your positions

Start by mapping your target allocation to the fund categories available to you. If you're an Indian investor, this means identifying equity mutual funds for your stock allocation and debt mutual funds or government securities for your fixed income side. You don't need dozens of funds to build a structured portfolio. Three to five broadly diversified funds typically cover all the buckets you need:

Equity funds (large-cap index or flexi-cap): covers your stock allocation

International equity funds: adds geographic diversification

Debt mutual funds or bond funds: covers your fixed income allocation

Keep expense ratios as low as possible. Every extra basis point in annual costs compounds against you over time and directly reduces your net returns.

A simple, consistent portfolio beats a complex one every time because complexity creates more opportunities to make behavioral mistakes.

Rebalancing when your mix drifts

Markets move, and your allocation will drift from its target without you adding or withdrawing anything. A portfolio you set at 70% equity might quietly shift to 78% after a strong equity run, which increases your risk exposure beyond what you originally planned. Rebalance once or twice a year, or whenever any asset class moves more than five percentage points from its target. This isn't about reacting to every fluctuation; it's about making a deliberate, scheduled correction that brings your portfolio back to the risk level you actually chose.

Final takeaways

Vanguard asset allocation models give you a research-backed framework for building a portfolio that matches your actual risk tolerance and time horizon, not just your current market confidence. The core insight is simple: your split between stocks, bonds, and short-term reserves drives most of your long-term returns, not the individual funds you pick within each category. Start with an honest assessment of how long you have until you need the money and how much short-term loss you can realistically absorb without selling.

From there, pick a model tier, fill it with low-cost, diversified funds, and rebalance consistently when your allocation drifts. That discipline, applied repeatedly over years, is what actually builds wealth. If you want a smarter, more personalized way to apply these principles to your Indian portfolio, get started with Invsify and let AI-powered advisory help you build a conflict-free plan built around your goals.