13 Wealth Growth Strategies for Indian Salaried Investors

Shlok Sobti

13 Wealth Growth Strategies for Indian Salaried Investors

You earn a decent salary. You want your money to grow. But between EMIs, monthly expenses, and that nagging feeling you should invest more, actually building wealth feels like solving a puzzle with missing pieces. Most advice you find online either assumes you have crores to spare or pushes products with hidden agendas. Meanwhile, your savings account returns barely keep pace with inflation, and another year slips by.

This guide walks you through 13 practical wealth growth strategies built specifically for salaried Indians. You'll learn how to set goals that stick, protect what matters, automate your investments, and make smarter choices with every rupee you earn. Each strategy fits together to create a complete system that works whether you're just starting out or already have investments scattered across platforms. No jargon. No theoretical concepts. Just clear steps you can start using this month to take control of your financial future and grow real wealth over time.

1. Use AI powered advice with Invsify

Traditional financial advisors earn commissions from products they sell you. This creates a direct conflict of interest that can cost you lakhs over time. Invsify flips this model by combining AI-powered insights with SEBI-registered advisory to deliver unbiased recommendations that prioritize your wealth growth, not someone else's commissions.

What Invsify does for salaried investors

Invsify analyzes your complete financial picture to create personalized wealth growth strategies. You get a Wealth Wellness Score that shows exactly where you stand, plus daily audio snippets that break down complex topics into simple insights. The platform tracks all your investments in one place, from mutual funds to EPF, giving you a clear view of what's working and what needs adjustment. Your conversational RM AI answers questions 24/7 in multiple languages, so you never wait for guidance when markets move or opportunities arise.

Why conflict free advice boosts returns

Commission-based distributors push products that pay them the most, not what serves your goals best. This single difference can cost you 2-3% annually in hidden fees and suboptimal choices. Over 20 years, that drag compounds into significant wealth erosion. Invsify's conflict-free model means every recommendation maximizes your returns, not advisor commissions.

"The best wealth growth strategies start with advice that serves only your interests."

How to get started with Invsify

Sign up takes minutes. Complete your KYC and risk profiling through the streamlined process. Your AI analyzes your situation and presents personalized recommendations immediately. Within days, you'll have clarity on what to do next.

Using Invsify with your existing investments

You don't need to liquidate current holdings. Link your existing portfolios to the platform for comprehensive tracking. Invsify reviews everything you own and suggests improvements where needed, helping you optimize what you already have while building smarter for tomorrow.

2. Set clear goals and a money plan

All effective wealth growth strategies start with knowing exactly what you want your money to do. Without specific targets, you drift between investing fads and miss opportunities that actually match your life. Your brain needs concrete milestones to stay motivated, and your money needs clear destinations to grow efficiently.

Turn vague wishes into specific goals

Replace "I want to be rich" with measurable outcomes like "accumulate ₹50 lakhs for a home down payment" or "build ₹2 crore retirement corpus." Write down exactly what you want to achieve, why it matters to you, and what it looks like when you reach it. The more specific your goal, the easier it becomes to build a plan that delivers results instead of just hope.

Link each goal to a time frame and amount

Every goal needs a deadline and a rupee figure. Your child's college fund needs ₹25 lakhs in 12 years. Your vacation home requires ₹1 crore in 20 years. These two details completely change how you invest. Short deadlines demand safer instruments while longer horizons let you take calculated risks for higher returns.

"Goals without timelines are just dreams. Goals without amounts are just wishes."

Prioritize goals for your salary and stage of life

Your salary can't fund everything at once. Rank goals by urgency and importance, not just what excites you most. Emergency funds and insurance come before luxury purchases. Retirement planning often gets ignored until it becomes urgent, which makes it exponentially harder to fund later.

Create a simple monthly cash flow plan

Track where your salary actually goes each month. Allocate fixed percentages to savings buckets before discretionary spending. A straightforward split might dedicate 20% to goal-based investments, 10% to emergency funds, and maintain clear boundaries for lifestyle expenses. Adjust these ratios as your income grows or goals shift.

3. Build a strong emergency fund

Most wealth growth strategies fail because life happens first. Medical emergencies, job loss, or urgent family needs force you to liquidate investments at the worst possible time, often at significant losses. Your emergency fund acts as a financial shock absorber that lets your long-term investments compound undisturbed while protecting you from everyday crises that derail even the best plans.

Why an emergency fund comes before investing

You cannot build lasting wealth on shaky ground. Jumping into equity markets or long-term goals without liquid savings means every unexpected expense becomes a wealth-destroying event. When your car breaks down or a family member needs hospitalization, you either raid your investments and pay exit penalties or pile up expensive credit card debt. Both options set your financial progress back by months or years.

How much salaried Indians should keep aside

Save between three to six months of your essential expenses in immediately accessible funds. If you support parents or have unstable income, push toward nine months or more. Calculate your actual monthly needs including rent, EMIs, groceries, utilities, and insurance premiums, then multiply by your chosen safety margin.

"Your emergency fund determines whether a crisis becomes a temporary setback or a permanent wealth destroyer."

Best places to park your safety buffer

Store this money in high-yield savings accounts or liquid funds that you can access within 24 hours. Avoid fixed deposits with lock-in periods or equity investments that fluctuate. Your emergency fund prioritizes availability over returns, so earning 4-6% while maintaining instant access beats chasing higher returns you cannot touch when needed.

Rules for using and refilling this fund

Touch this money only for genuine emergencies, not sales or vacations. Define what qualifies as an emergency before you need it. When you do withdraw, make replenishing this fund your top financial priority until it reaches the original level, even if that means pausing other investments temporarily.

4. Protect your family with insurance

Wealth growth strategies collapse instantly if a health crisis or loss of income wipes out everything you've built. Insurance converts unpredictable catastrophes into predictable costs you budget for monthly. Your family's financial security depends on protecting against the risks that destroy wealth faster than any investment can rebuild it.

Why term insurance is non negotiable

Your salary supports everyone who depends on you. When that income disappears, your family faces immediate financial collapse unless adequate term life insurance replaces your earning capacity. Term plans provide maximum coverage at minimum cost because they focus purely on protection, not investment returns. You need this foundation before chasing higher returns elsewhere.

How much life cover you really need

Multiply your annual expenses by 15 to 20 years to estimate the corpus your family needs if you're gone tomorrow. Add outstanding loans and upcoming goals like children's education. This total determines your minimum coverage amount, typically 10 to 15 times your annual salary. Buy more coverage when you're younger because premiums increase sharply with age and health changes.

Getting adequate health cover for your family

Medical inflation runs at 12 to 15% annually, far exceeding general inflation. A hospitalization that costs ₹5 lakhs today will demand ₹10 lakhs in just five years. Secure family floater plans covering at least ₹10 to 15 lakhs, more if you live in metro cities where treatment costs soar higher.

"Insurance doesn't prevent disasters. It prevents disasters from destroying your wealth."

Other risks like disability and critical illness

Long-term disability stops your income while expenses continue indefinitely. Critical illness cover provides lump sum payouts for cancer, heart attacks, or strokes, covering treatment costs and income loss during recovery. These riders cost relatively little but protect against scenarios that devastate finances even when you survive.

5. Automate savings and SIP investing

Manual investing fails because willpower depletes every month. You face endless decisions about when to invest, how much to allocate, and whether markets look favorable. Automation removes these friction points by making wealth growth strategies execute automatically regardless of your mood, busy schedule, or market headlines. Your investments happen before you can second-guess yourself or find excuses to skip a month.

Pay yourself first through auto debit

Set up standing instructions that transfer money from your salary account to investment accounts on the same day your paycheck arrives. This reverses the typical pattern where you invest whatever remains after spending. When automation moves money first, your lifestyle adjusts around what's left, and your wealth building becomes non-negotiable rather than optional.

Why SIPs suit salaried investors

Systematic Investment Plans match perfectly with monthly salary patterns by converting large lump sum requirements into affordable recurring amounts. Markets fluctuate constantly, but SIPs buy more units when prices drop and fewer when prices rise, automatically averaging your purchase cost over time. This removes the impossible task of timing markets while keeping you invested through all conditions.

Choosing SIP dates and amounts wisely

Schedule SIP dates for two to three days after your salary credits to ensure funds availability. Start with amounts you can sustain comfortably, even 10 to 15% of your take-home pay. Consistency matters more than starting big because regular investing builds discipline and compounds faster than sporadic large investments.

"The best wealth growth strategies run on autopilot, not motivation."

Increasing SIPs with every salary hike

Commit to raising your SIP amounts by at least half of every increment or bonus you receive. Your lifestyle expenses rise naturally with income, but deliberately directing raises toward investments accelerates wealth accumulation without feeling like sacrifice. This single habit transforms modest starting SIPs into substantial wealth over a decade.

6. Maximize EPF VPF and NPS for retirement

Your employer already contributes to your retirement through mandatory schemes, but most salaried Indians leave enormous wealth on the table by not maximizing these tax-advantaged instruments. EPF, VPF, and NPS form the foundation of smart retirement planning because they combine safety, tax benefits, and long-term compounding that private investments struggle to match. These government-backed options deserve priority in your wealth growth strategies before you explore higher-risk alternatives.

Understand how EPF builds your retirement pool

Your EPF account grows through mandatory contributions of 12% from your salary plus matching employer deposits. This money compounds tax-free at rates typically between 8 to 8.5% annually, revised quarterly by the government. The entire corpus remains exempt from tax at withdrawal after five years of continuous service, making it one of the most tax-efficient retirement vehicles available to salaried Indians.

When to use VPF for extra safe compounding

Voluntary Provident Fund lets you contribute additional amounts beyond the mandatory 12%, up to 100% of your basic salary. VPF carries the same interest rate and tax treatment as EPF, making it ideal when you need guaranteed returns without market risk. Consider maxing out VPF if you have conservative goals or already sufficient equity exposure elsewhere in your portfolio.

Using NPS for tax breaks and long term income

National Pension System offers an extra ₹50,000 deduction under Section 80CCD(1B) beyond the standard ₹1.5 lakh under Section 80C. Your NPS investments split between equity, corporate bonds, and government securities based on your chosen allocation. At retirement, you receive 60% as lump sum and convert the remaining 40% into monthly pension through annuities.

"Government-backed retirement schemes deliver tax-free compounding that most private investments cannot replicate."

Balancing these with other retirement investments

Don't put everything into EPF and NPS despite their benefits. These instruments lack liquidity and limit your asset allocation flexibility. Maintain balanced exposure across EPF, VPF, NPS, and equity mutual funds to optimize returns while preserving accessibility and growth potential your retirement truly needs.

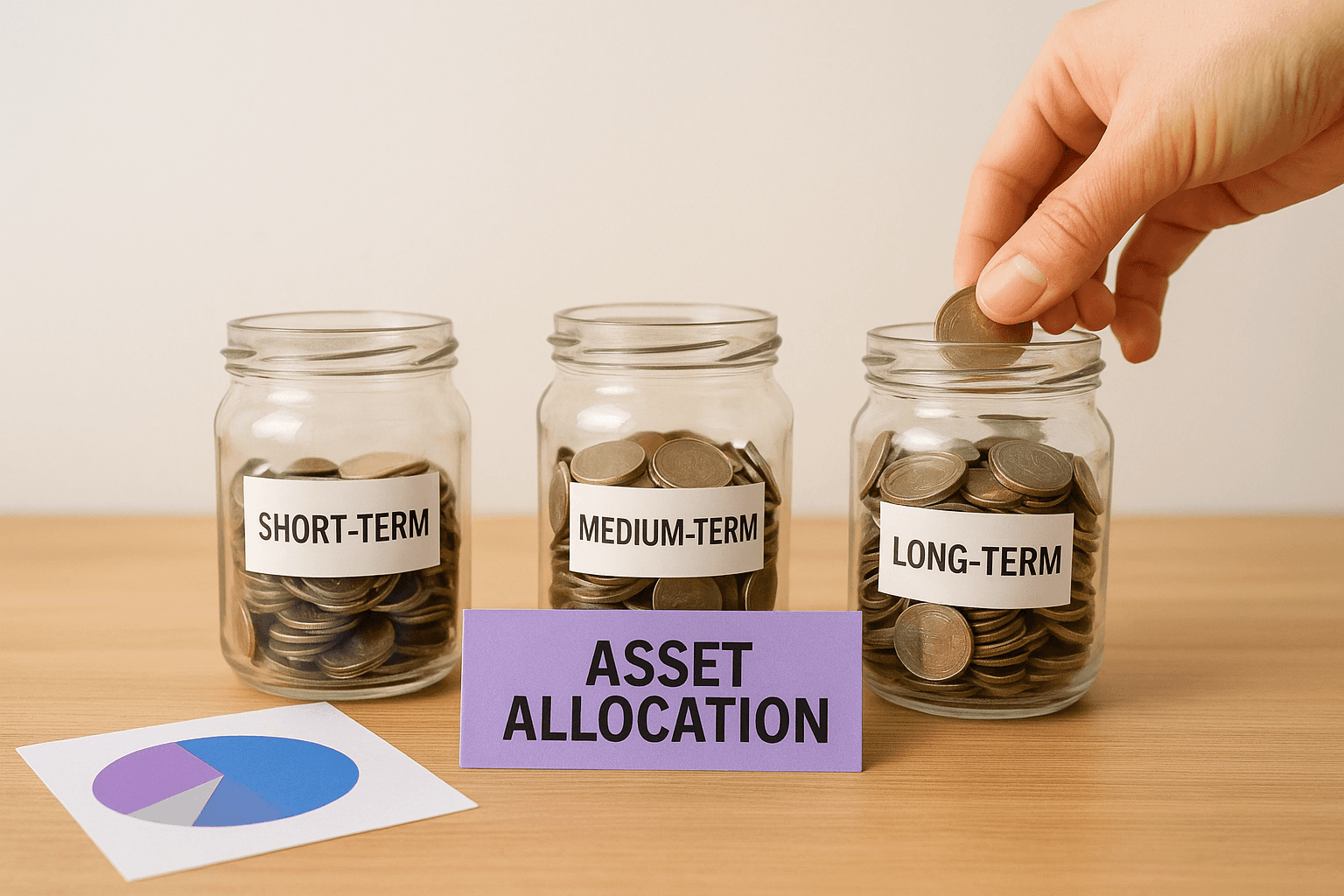

7. Use asset allocation for each goal

Different goals need different investment mixes. Your asset allocation determines how much goes into equity, debt, and other instruments based on when you need the money and how much risk that timeline allows. The same rupee invested for retirement twenty years away should sit in completely different instruments than money needed for a home down payment in three years. Smart wealth growth strategies customize allocation for each specific goal instead of treating all your money the same way.

Match risk levels to goal timelines

Goals arriving within three years cannot afford equity volatility that might leave you short when you need funds. Park these amounts in debt instruments that preserve capital even if returns stay modest. Goals five years or further away can absorb short-term market swings, so you load these with equity exposure that historically delivers superior long-term growth. Your timeline determines acceptable risk, not your personality or market optimism.

Sample mixes for short medium and long term

Short-term goals under three years work best with 80 to 100% debt allocation through liquid funds or short-duration debt funds. Medium-term goals spanning three to seven years suit balanced mixes of 50 to 60% equity and the rest in debt, capturing growth while managing volatility. Long-term goals beyond seven years benefit from 70 to 80% equity exposure that maximizes compounding over extended periods.

"The right asset allocation turns market volatility from a threat into an advantage."

How to choose equity debt and gold weights

Start with your goal timeline to set the equity-debt foundation, then add 5 to 10% gold allocation for diversification and inflation protection. Younger investors with longer horizons can push equity weightings higher, while those approaching goal deadlines should tilt conservative regardless of current market conditions.

When to shift allocation as goals get closer

Review and rebalance your allocation annually, gradually reducing equity exposure as goal dates approach. Begin shifting from aggressive to balanced allocations when you reach five years out, then move toward conservative allocations at the three-year mark to protect accumulated wealth from last-minute market crashes.

8. Choose low cost equity mutual funds

Equity mutual funds pool money from investors like you to buy diversified stock portfolios managed by professionals. These funds eliminate the need to pick individual stocks while providing instant diversification across sectors and companies. Your wealth growth strategies gain tremendous efficiency when you choose funds that charge less and deliver consistent returns rather than chasing past performance or brand names.

Why most salaried investors should use funds

Direct stock investing demands constant research, market monitoring, and nerves of steel during corrections. Most salaried professionals lack the time and expertise to analyze balance sheets or track quarterly results. Equity mutual funds handle this complexity through professional management while spreading risk across multiple holdings, so single company failures cannot devastate your portfolio.

Index funds versus active funds in India

Index funds simply replicate benchmark indices like Nifty 50 or Sensex, delivering market returns at rock-bottom costs. Active funds employ managers who try beating these benchmarks through stock selection. Data shows that over 70% of active funds fail to outperform their benchmark over ten years, making low-cost index funds the smarter default choice for most investors.

How expense ratios eat into long term wealth

Every rupee paid as expense ratio reduces your final corpus. A fund charging 2% annually versus one charging 0.5% costs you lakhs over twenty years through compounding drag. Calculate this impact yourself: a ₹10 lakh investment growing at 12% becomes ₹96.5 lakhs at 2% expense ratio but ₹1.15 crore at 0.5% expense ratio over twenty years.

"Lower costs guarantee higher returns when everything else stays equal."

Shortlist funds using data not hype

Evaluate funds using five-year rolling returns, not one-year spikes that often reverse. Check if the fund consistently ranks in the top quartile across market cycles. Verify expense ratios, portfolio turnover, and fund manager tenure before investing, ignoring celebrity endorsements or recent awards that mean nothing for future performance.

9. Add debt and fixed income for stability

Equity delivers growth, but debt keeps you standing when markets crash. Your portfolio needs stable instruments that generate predictable returns while protecting capital during volatility. Debt and fixed income investments balance your wealth growth strategies by reducing overall portfolio swings and ensuring you have money available when specific goals arrive, regardless of what equity markets do at that moment.

Role of debt in a balanced portfolio

Debt instruments act as ballast in your investment ship, preventing extreme ups and downs that force emotional decisions. When equity crashes 20%, your debt holdings remain stable or even gain value, limiting total portfolio damage. This stability lets you stay invested through corrections instead of panic-selling at losses. Debt also generates regular income through interest payments that you can reinvest or use for short-term needs.

Options like debt funds FDs and bonds

Debt mutual funds invest in government securities, corporate bonds, and money market instruments, offering better tax efficiency than fixed deposits for holdings beyond three years. Fixed deposits from banks and post offices provide guaranteed returns with deposit insurance up to ₹5 lakhs per bank. Government bonds through RBI Retail Direct offer safety and liquidity. Choose based on your tax bracket, liquidity needs, and risk tolerance.

How interest rate cycles affect returns

Rising interest rates hurt existing bond values while boosting returns on new investments. Falling rates do the opposite, lifting bond prices while reducing future income. Short-duration debt funds minimize interest rate risk for money needed within one to three years. Long-duration funds suit falling rate environments when you can lock in higher yields for extended periods.

"Debt protects wealth you've already built while equity grows wealth you're still building."

Avoiding credit risk and chasing yield

Higher yields always signal higher risk, usually through lower-rated corporate bonds that might default. Stick with high-quality papers rated AA or above, accepting lower returns in exchange for capital safety. Avoid debt funds holding excessive corporate bonds from single sectors or lower-rated issuers promising extra returns that evaporate when defaults strike.

10. Use tax efficient Indian investments

Taxes drain your returns silently every year unless you structure investments to minimize this leakage. Smart wealth growth strategies treat tax planning as an ongoing process that amplifies compounding rather than a March scramble to find deductions. You keep more of what you earn when you choose instruments that offer legitimate tax benefits while building wealth instead of parking money in low-return schemes just for certificates.

Plan taxes across the year not in March

Most salaried Indians wake up to tax planning in February, then rush into whatever products agents push hardest. This panic buying forces suboptimal choices that lock money into unsuitable instruments for years. Start planning when the financial year begins by listing your expected income, existing deductions, and remaining gaps. You can spread investments across monthly SIPs in ELSS or increase VPF contributions gradually rather than dumping lakhs in March.

Key sections for salaried taxpayers

Section 80C offers ₹1.5 lakh deduction through EPF, PPF, life insurance premiums, ELSS, and principal repayment on home loans. Section 80D covers health insurance premiums up to ₹25,000 for self and ₹50,000 including parents. Section 80CCD(1B) provides an additional ₹50,000 deduction exclusively for NPS contributions beyond the 80C limit.

Popular tax saving tools and how they differ

ELSS delivers potential equity returns with just three-year lock-in, making it the most flexible 80C option. PPF offers safety with 15-year maturity and tax-free interest. NPS provides extra deduction but restricts access until retirement. Life insurance premiums qualify but only term plans make financial sense, while traditional plans mix poor returns with insurance.

"Tax efficiency turns good investments into great ones by protecting your gains from unnecessary erosion."

Avoid common tax planning mistakes

Never buy insurance purely for tax deduction when term plans cost less and provide better protection. Avoid real estate investments justified only by Section 80C benefits when rental yields and appreciation matter more. Don't ignore the new tax regime that might suit you better if you have minimal deductions, saving paperwork while delivering similar take-home pay.

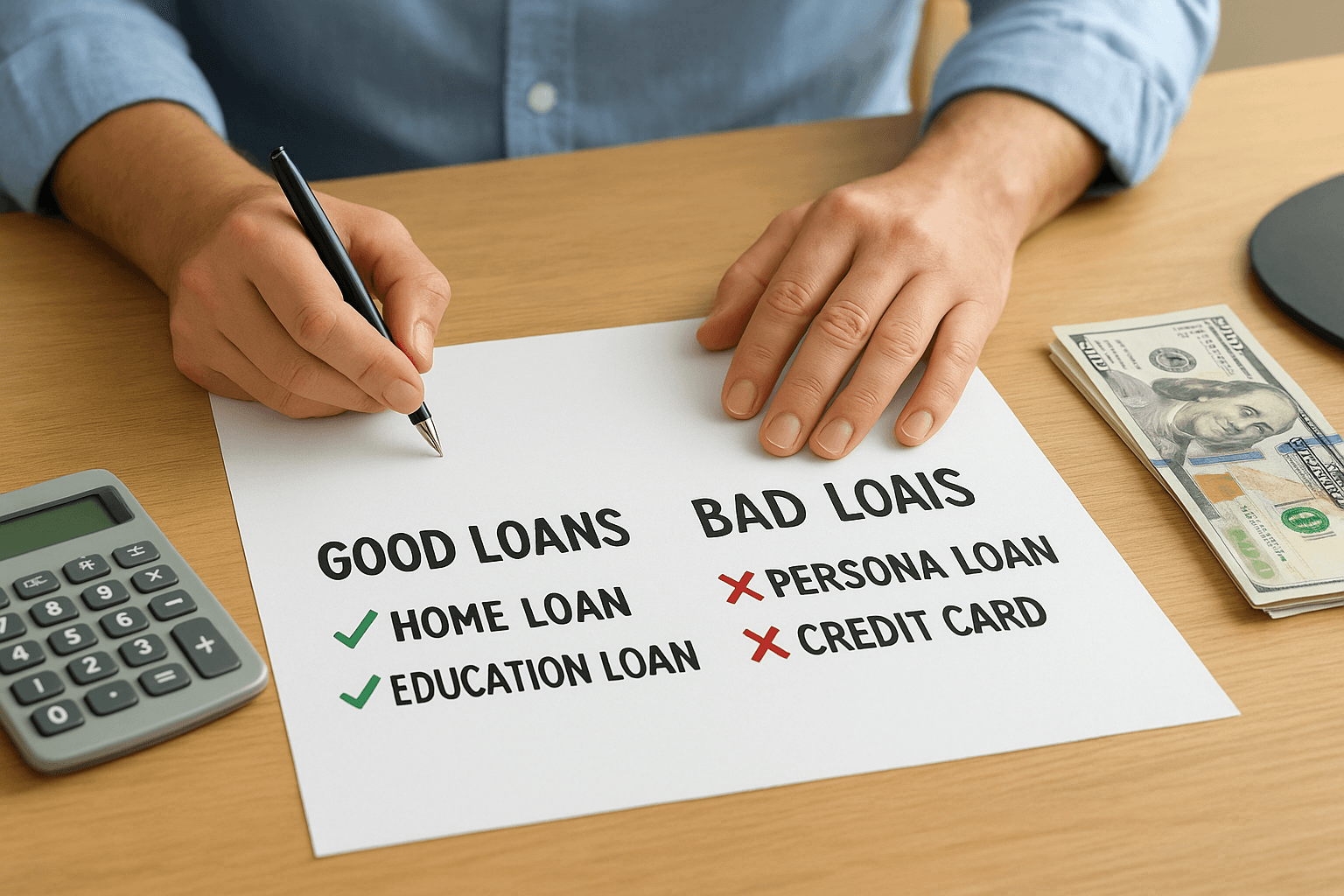

11. Avoid bad debt and loan traps

Debt accelerates wealth destruction faster than most investments can build it. Every rupee you pay in interest reduces what you can invest, and high-interest loans create cycles where you work for lenders instead of yourself. Smart wealth growth strategies require you to eliminate bad debt completely while using good debt strategically when it adds genuine value to your financial position.

Differentiate good loans from bad loans

Good loans finance appreciating assets at reasonable rates. Your home loan at 8 to 9% builds equity while providing shelter, and education loans boost earning capacity through higher future salaries. Bad loans fund depreciating assets or lifestyle expenses like personal loans for vacations or gadget EMIs costing 14 to 24% annually that destroy wealth.

How credit card debt kills wealth growth

Credit cards charging 36 to 42% annual interest destroy wealth faster than any investment creates it. A ₹50,000 balance takes years to clear while costing lakhs through minimum payment traps. You must clear credit card debt completely before investing elsewhere because no investment reliably beats these crushing rates.

"Eliminating high-interest debt delivers guaranteed returns no market investment can match."

Smart rules for home and car loans

Limit home loan EMIs to 35 to 40% of monthly income, leaving room for other goals. Choose the shortest tenure you can afford because longer loans multiply total interest paid dramatically. Avoid car loans by saving and buying outright, or keep EMIs under 15% of income if you must borrow.

Steps to get out of a debt spiral

List all debts with interest rates and balances, then attack the highest-rate debt first while paying minimums on others. Stop creating new debt by cutting cards or switching to debit-only spending immediately. Redirect bonuses entirely toward debt elimination until you break free completely.

12. Review and rebalance every year

Your portfolio shifts naturally over time as different investments grow at different rates. What started as a balanced mix tilts toward whatever performed best recently, often creating unintended risk concentrations that expose you to losses you never planned for. Annual reviews catch these drifts before they threaten your goals, making them essential maintenance for all wealth growth strategies rather than optional tasks you skip when busy.

Why portfolios drift away from your plan

Markets move investments in different directions throughout the year. Your equity allocation might balloon from 60% to 75% after a strong bull run, leaving you overexposed to a correction you cannot afford near goal deadlines. Debt portions shrink proportionally even though your original plan required that stability. These shifts happen silently while you focus on work and life, making scheduled reviews the only defense against unintended portfolio changes.

Simple annual review checklist

Check if your current asset allocation matches your target percentages within 5% tolerance. Verify each goal's progress toward its timeline and required corpus. Review fund performance against benchmark indices over three to five years, not just recent months. Confirm your insurance coverage still adequately protects your family as income and responsibilities grow.

"Annual reviews transform reactive panic into proactive control over your financial future."

How to rebalance without over trading

Sell portions of overweight assets and buy underweight ones to restore your target allocation. Use new investments to rebalance instead of selling whenever possible, directing fresh money toward lagging allocations rather than what performed best. Limit rebalancing to once or twice yearly because frequent trading generates taxes and transaction costs that erode returns.

When you should seek expert help

Complex situations involving inheritance, major life changes, or six-figure portfolios often benefit from professional guidance. If annual reviews leave you confused or paralyzed about decisions, a SEBI-registered advisor provides clarity and removes emotional bias from your wealth management.

13. Grow income with skills and side gigs

Every rupee you invest matters, but the amount you can invest matters more. Wealth growth strategies hit natural limits when your salary caps how much you contribute monthly. Raising your income through skill development and additional revenue streams removes this ceiling, letting you accelerate every goal on your timeline while maintaining your current lifestyle instead of making sacrifice the only path forward.

Why raising income speeds up wealth growth

Doubling your investment amount creates exponentially faster results than optimizing returns by a few percentage points. Adding ₹5,000 monthly to your SIPs compounds into lakhs more over twenty years compared to squeezing an extra 1% annual return from your current investments. Higher income also cushions against market downturns because you can continue investing when others pause, buying assets at discounted prices that amplify long-term gains.

Invest in skills that boost career prospects

Target certifications and training that directly translate into salary increments or promotions within your industry. Technical skills like data analysis, project management, or specialized software command premium compensation across sectors. Your employer often subsidizes relevant courses, making this the lowest-cost way to boost earning capacity while strengthening job security during economic uncertainty.

"Income growth multiplies the power of every other wealth building technique you use."

Build ethical side income streams

Freelancing, consulting, or teaching based on your existing expertise generates additional monthly cash flow without burning you out. Avoid pyramid schemes or high-risk ventures that jeopardize your primary income. Start small with weekend projects that test demand before scaling, keeping side work sustainable alongside your main career.

Use extra income to fast track your goals

Direct every rupee from raises and side income toward investment increases rather than lifestyle inflation. Treat bonuses as goal acceleration fuel by making lump sum investments or clearing debt. This discipline transforms temporary income spikes into permanent wealth gains that compound long after the extra work ends.

Next steps for your wealth plan

You now have 13 wealth growth strategies that work specifically for salaried Indians facing real constraints on time and resources. These steps transform scattered efforts into a coherent system that protects what you earn while growing it consistently year after year. Your success depends on starting immediately rather than waiting for the perfect moment or market conditions, because compounding needs time more than it needs large starting amounts or perfect timing.

Begin with whichever strategy addresses your biggest financial gap right now. If you lack emergency funds, build that buffer first. If insurance coverage is missing, fix that protection immediately. Get conflict-free advice from Invsify to personalize these strategies for your exact situation, income level, and specific goals. Your wealth plan becomes real the moment you take the first step today, not when you understand everything perfectly or feel completely ready.