Wealth Management Risk Assessment: Tools, Templates, Steps

Shlok Sobti

Wealth Management Risk Assessment: Tools, Templates, Steps

Most investors jump into mutual funds or stocks without understanding how much risk they can actually handle. When markets drop 20%, panic sets in. You sell at a loss, then watch prices recover while sitting in cash. This cycle repeats because you never took the time to assess your risk profile properly. Your investments should match your financial situation, goals, and ability to handle volatility.

A wealth management risk assessment gives you clarity. It measures your risk capacity based on your income, expenses, and timeline. It also captures your risk tolerance through structured questions about how you'd react to market swings. The result is a documented profile that guides your asset allocation decisions and keeps you aligned with your actual capacity to take on investment risk.

This guide walks you through the complete risk assessment process. You'll learn how to clarify your financial boundaries, define your risk levels using proven questionnaires, and map your profile to specific investment allocations. We'll also share templates and tools that Indian advisors use, plus the regulatory requirements you need to know as a SEBI compliant investor.

What is a wealth management risk assessment

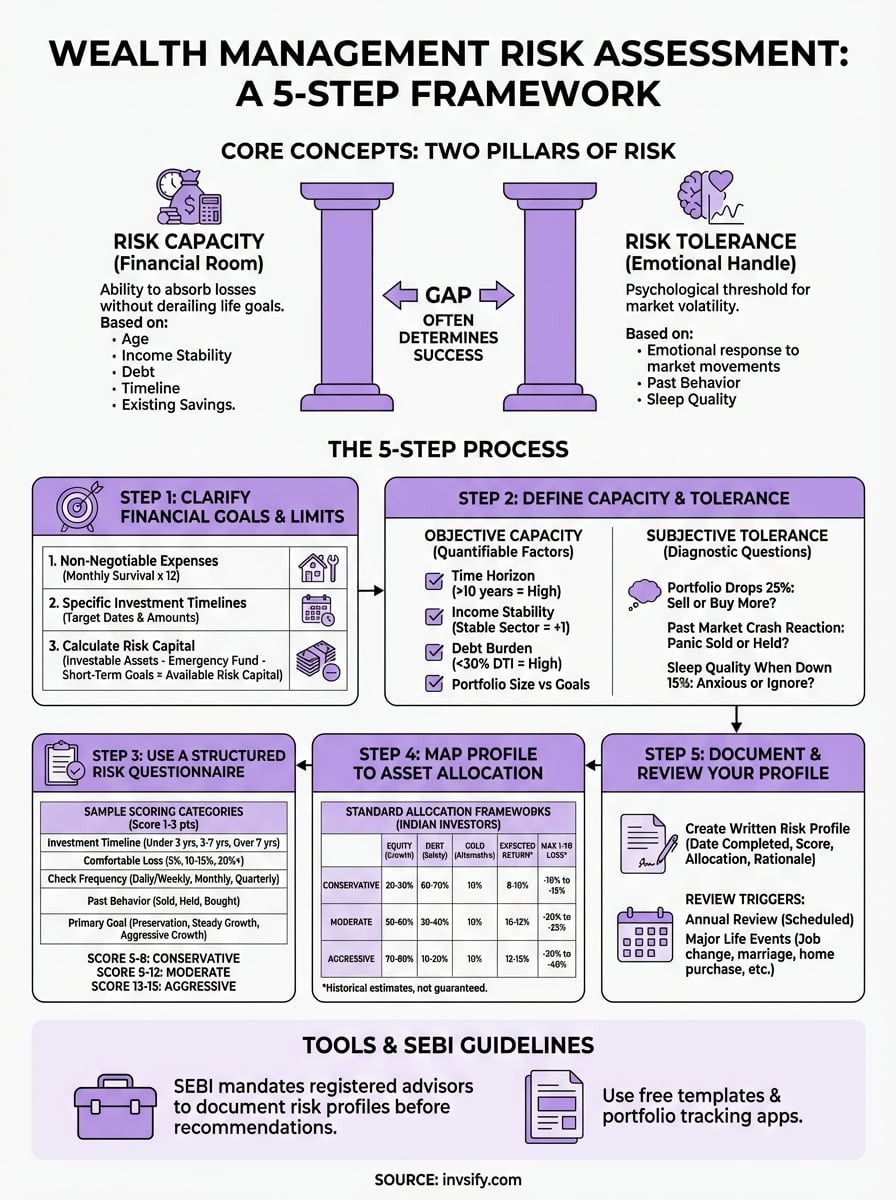

A wealth management risk assessment is a structured process that measures how much investment risk you can afford to take and how much volatility you can emotionally handle. It combines objective financial data with subjective behavioral responses to create a risk profile. This profile then guides your portfolio construction, ensuring your investments match both your financial capacity and psychological comfort level.

The two pillars of risk assessment

Your risk capacity represents the financial room you have to absorb losses without derailing your life goals. This depends on your age, income stability, existing savings, debt levels, and investment timeline. A 28-year-old software engineer with zero debt and a 30-year horizon has higher capacity than a 55-year-old with school fees due in three years.

Risk tolerance captures your emotional response to market movements. Even if you can financially afford a 30% portfolio drop, you might panic and sell everything when it happens. Tolerance questionnaires reveal these behavioral patterns through scenario-based questions about past reactions and hypothetical market crashes.

The gap between what you can afford to lose and what you're willing to lose often determines your actual investment success.

Why formal assessment matters

Most investors skip this step and choose portfolios based on recent returns or friend recommendations. You might load up on small-cap funds during a bull run, only to discover you can't stomach the 40% correction that follows. SEBI regulations now require advisors to document risk profiling before recommending any investment products, protecting both you and the advisor.

Documenting your risk profile creates a reference point for future decisions. When markets crash and fear peaks, you can review your assessment and remember why you chose your allocation. This written record prevents emotional decisions that destroy long-term wealth. Financial advisors in India use standardized questionnaires that classify investors into conservative, moderate, or aggressive categories, each mapped to specific equity-debt ratios.

Step 1. Clarify your financial goals and limits

Before any wealth management risk assessment can begin, you need absolute clarity on where your money must go and when you'll need it. This step creates the financial boundaries that determine your actual capacity to take investment risk. You'll document three critical elements: your fixed obligations, your goal timelines, and the capital you can genuinely afford to put at risk.

List your non-negotiable expenses

Start by calculating your monthly survival number. This includes rent or EMI, utilities, groceries, insurance premiums, loan payments, and any recurring commitments you cannot defer. Add 20% as a buffer for unexpected household expenses. Multiply this figure by 12 to get your annual baseline requirement.

Your emergency fund must cover at least six months of these expenses before you invest anything beyond employer PF contributions. Keep this amount in a liquid fund or sweep-in fixed deposit, not in equity mutual funds. This cushion protects you from being forced to sell investments during a market crash when you face a job loss or medical emergency.

Any money earmarked for expenses within 36 months should never enter equity markets, regardless of your risk profile.

Set specific investment timelines

Break down your financial goals with exact target dates and amounts. Don't just write "retirement" or "child's education." Instead, define "₹2 crore corpus by March 2053" or "₹15 lakh for college admission by June 2032." Each goal needs three data points: the target amount, the deadline, and your current savings toward it.

Map each goal to an investment bucket based on time horizon. Goals under three years go into debt funds or fixed deposits. Goals between three and seven years can handle a 30-50% equity allocation. Goals beyond seven years can take higher equity exposure. This timeline-based bucketing prevents you from chasing returns with money you'll need soon.

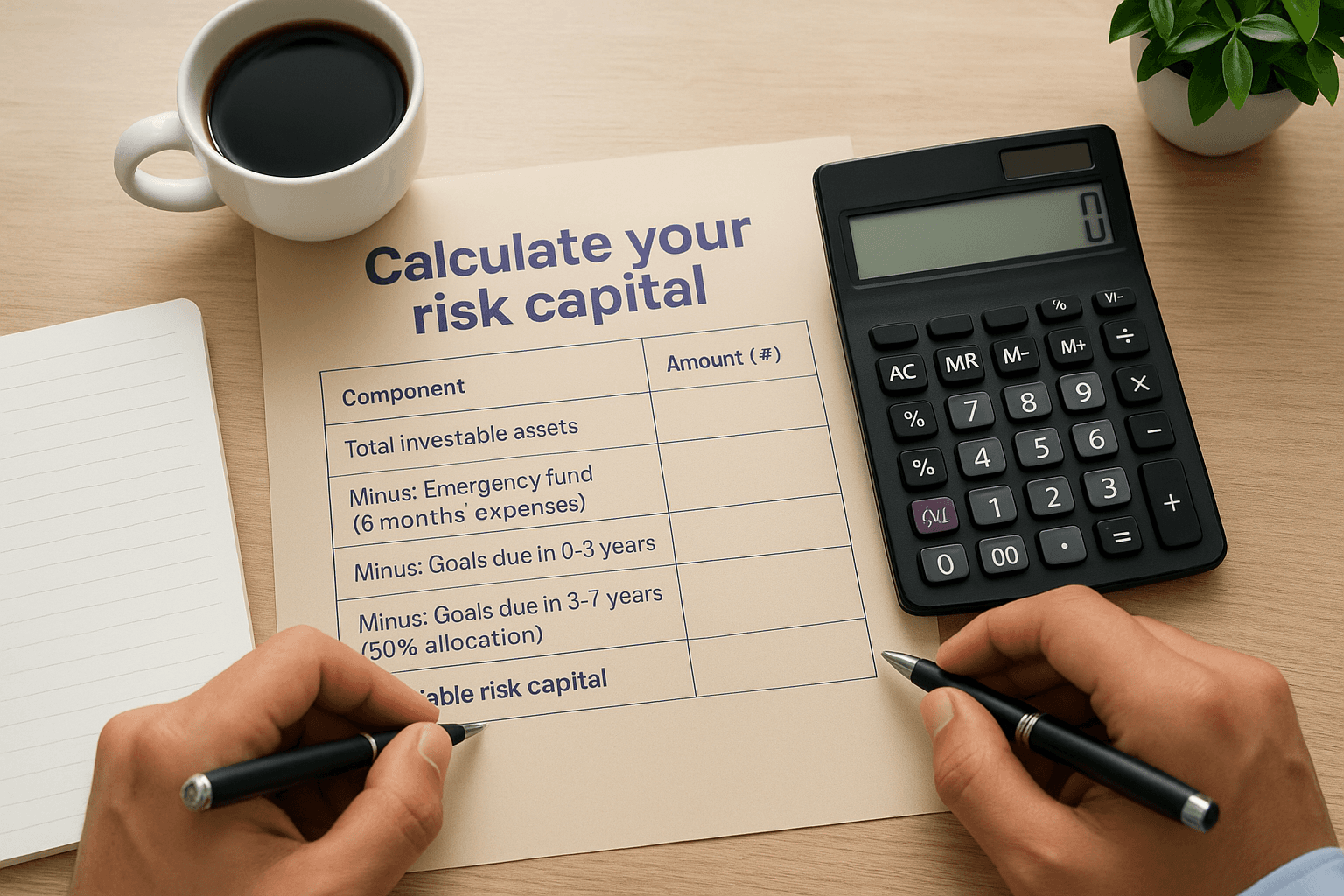

Calculate your risk capital

Subtract your emergency fund and short-term goal amounts from your total investable assets. What remains is your true risk capital. This is the only money that should enter growth-focused portfolios with significant equity exposure. Use this template to determine your risk capital:

Component | Amount (₹) |

|---|---|

Total investable assets | _______ |

Minus: Emergency fund (6 months expenses) | _______ |

Minus: Goals due in 0-3 years | _______ |

Minus: Goals due in 3-7 years (50% allocation) | _______ |

Available risk capital | _______ |

This calculation reveals your financial capacity independent of your emotional tolerance. You might feel comfortable with volatility, but if this number is small relative to your total assets, your actual risk capacity remains limited.

Step 2. Define your risk capacity and tolerance

Once you've established your financial boundaries, you need to measure two distinct components that form the foundation of your wealth management risk assessment. Risk capacity is the mathematical limit of how much loss your financial situation can absorb without compromising essential goals. Risk tolerance is the psychological threshold where volatility causes you to abandon your investment plan. These measurements work together to determine your actual risk profile.

Measure your objective risk capacity

Your risk capacity depends on five quantifiable factors that determine how much investment volatility your financial life can withstand. Calculate each factor separately, then combine them to understand your true capacity ceiling.

Time horizon: Count the years until you need to withdraw a significant portion of your portfolio. Subtract any amount needed within three years. If you have 15 years before retirement and need nothing before that, you have high time capacity. If you need funds in five years for a home down payment, your capacity drops significantly.

Income stability: Divide your annual passive income (rent, dividends, interest) by your annual expenses. Add one point if you work in a recession-proof sector like healthcare or government. Subtract one point if you're in cyclical industries like real estate or automotive. A stable government job with side rental income gives you higher capacity than commission-based sales work.

Debt burden: Calculate your debt-to-income ratio by dividing total monthly debt payments by gross monthly income. Ratios below 30% indicate higher capacity. If you're paying 50% of your income toward EMIs, you cannot afford portfolio volatility because a job loss or income drop leaves no buffer.

Portfolio size relative to goals matters more than absolute numbers. Someone with ₹50 lakh invested toward a ₹60 lakh retirement goal has low capacity because there's minimal room for losses. Another person with ₹50 lakh toward a ₹20 lakh goal has high capacity because they're already past their target.

Financial capacity exists independent of your feelings about money. It's pure mathematics based on your life situation.

Test your subjective risk tolerance

Risk tolerance reveals how you actually behave when markets drop, regardless of what your spreadsheet says you can afford. Answer these diagnostic questions honestly, writing down your immediate reaction before rationalizing:

Your portfolio drops 25% in three months during a market correction. You need no money from it for 10 years. What do you do? If you immediately think "sell everything," your tolerance is low. If you think "buy more," your tolerance is high. Your first instinct reveals your true tolerance more accurately than your considered response.

Consider your past investment behavior. Did you panic-sell during March 2020 when the market crashed 40%? Did you hold steady through the 2016 demonetization volatility? Review your actual transaction history during volatile periods. Past behavior predicts future behavior more reliably than hypothetical scenarios.

Rate your sleep quality when your portfolio is down 15%. If you check your portfolio app daily and feel anxious about losses, you have lower tolerance than you think. If you can ignore market noise for months, you have higher tolerance. Physical stress responses like insomnia or constant portfolio checking signal that your allocation exceeds your psychological capacity.

Step 3. Use a structured risk questionnaire

Standardized questionnaires eliminate guesswork by forcing you to confront specific scenarios that reveal your true risk tolerance. These tools ask pointed questions about your reactions to portfolio losses, your investment experience, and your financial priorities. SEBI guidelines require registered investment advisors to use documented questionnaires before recommending products, which means you should apply the same rigor to your self-directed wealth management risk assessment. Complete the questionnaire when markets are calm, not during a crash when fear distorts your judgment.

Core questions every assessment needs

Your questionnaire must cover five distinct categories that together paint an accurate picture of your risk profile. Each category targets a different aspect of how you handle investment uncertainty.

Investment timeline questions establish when you'll need your money. Ask yourself: "When will I withdraw 25% or more of this portfolio?" Options range from "within 2 years" (low risk capacity) to "more than 15 years" (high capacity). Follow up with: "If my goal date were delayed by 3 years due to market conditions, would that create financial hardship?"

Loss tolerance scenarios force you to quantify acceptable drawdowns. Use this exact question: "Your portfolio drops 30% in value over six months. You need nothing from it for 10 years. What would you do?" The four answer choices reveal your tolerance: (A) Sell everything immediately, (B) Reduce equity exposure by half, (C) Hold steady and wait, (D) Invest additional money to buy low.

Financial experience matters because familiarity with volatility builds tolerance. Ask: "How many years have you actively invested in equity mutual funds or stocks?" and "Have you held investments through at least one market correction of 20% or more without selling?"

Your answers to loss scenarios reveal more about your actual behavior than any theoretical discussion about risk and return.

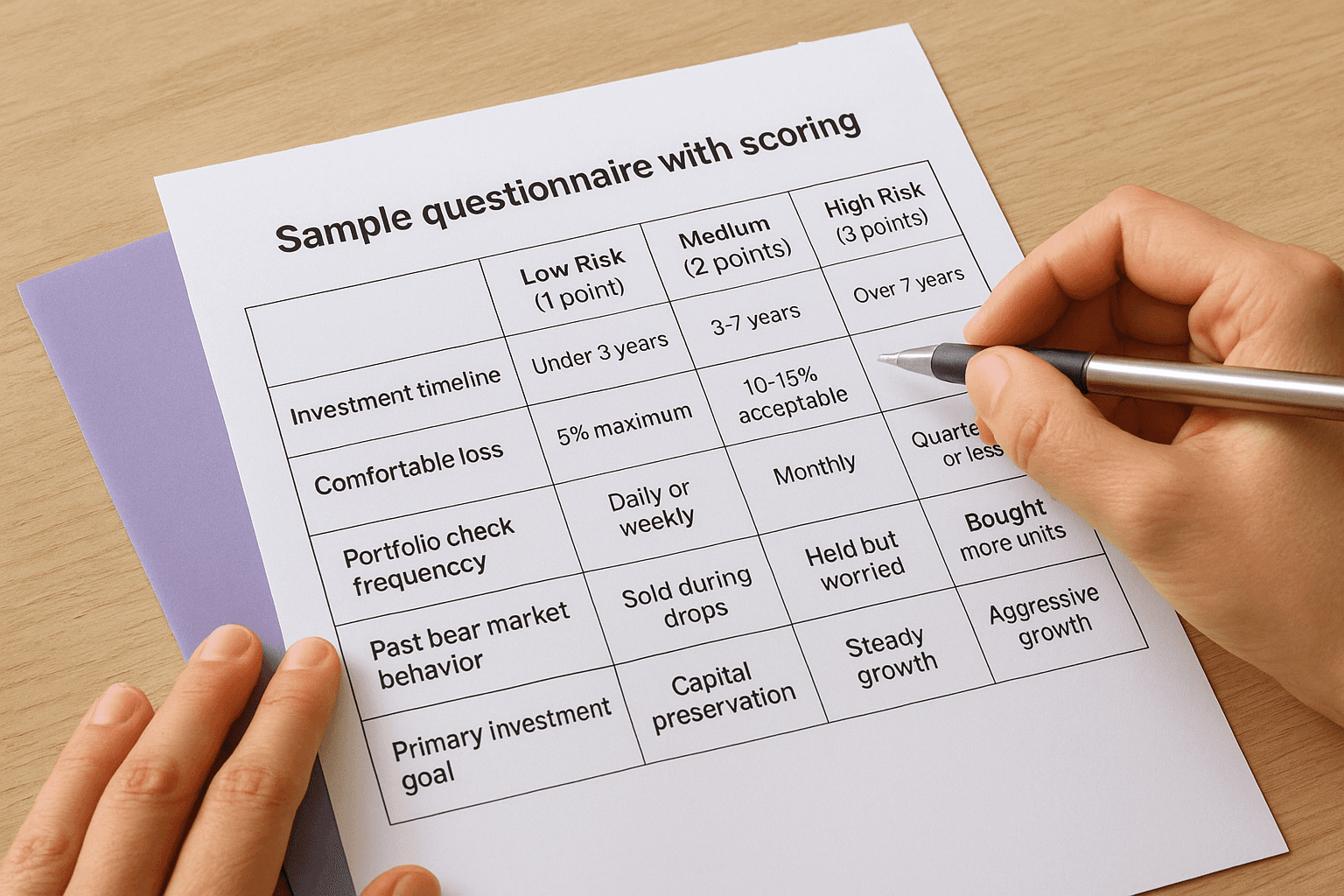

Sample questionnaire with scoring

Use this template to score your risk profile systematically. Answer each question, then add up your total points:

Question | Low Risk (1 point) | Medium Risk (2 points) | High Risk (3 points) |

|---|---|---|---|

Investment timeline | Under 3 years | 3-7 years | Over 7 years |

Comfortable loss | 5% maximum | 10-15% acceptable | 20%+ acceptable |

Portfolio check frequency | Daily or weekly | Monthly | Quarterly or less |

Past bear market behavior | Sold during drops | Held but worried | Bought more units |

Primary investment goal | Capital preservation | Steady growth | Aggressive growth |

Score 5-8 points: Conservative profile. Stick to debt-heavy allocations with maximum 30% equity exposure. Your capacity or tolerance cannot handle significant volatility.

Score 9-12 points: Moderate profile. Balance your portfolio with 40-60% equity allocation depending on your specific timeline and goals.

Score 13-15 points: Aggressive profile. You can handle 70-80% equity exposure based on both capacity and tolerance factors.

Document your completed questionnaire with the date. Revisit it annually or after major life changes like marriage, home purchase, or job transitions. Your risk profile evolves as your income stability, timeline, and experience level change over time.

Step 4. Map your profile to asset allocation

Your risk profile score means nothing until you translate it into an actual investment portfolio. This step converts your conservative, moderate, or aggressive classification into specific percentages of equity, debt, and other assets. The allocation you choose determines your expected returns, maximum drawdowns, and portfolio volatility over the next decade. You need a clear framework that matches Indian market conditions and regulatory guidelines, not generic global templates that ignore local factors like EPF contributions or tax-free debt options.

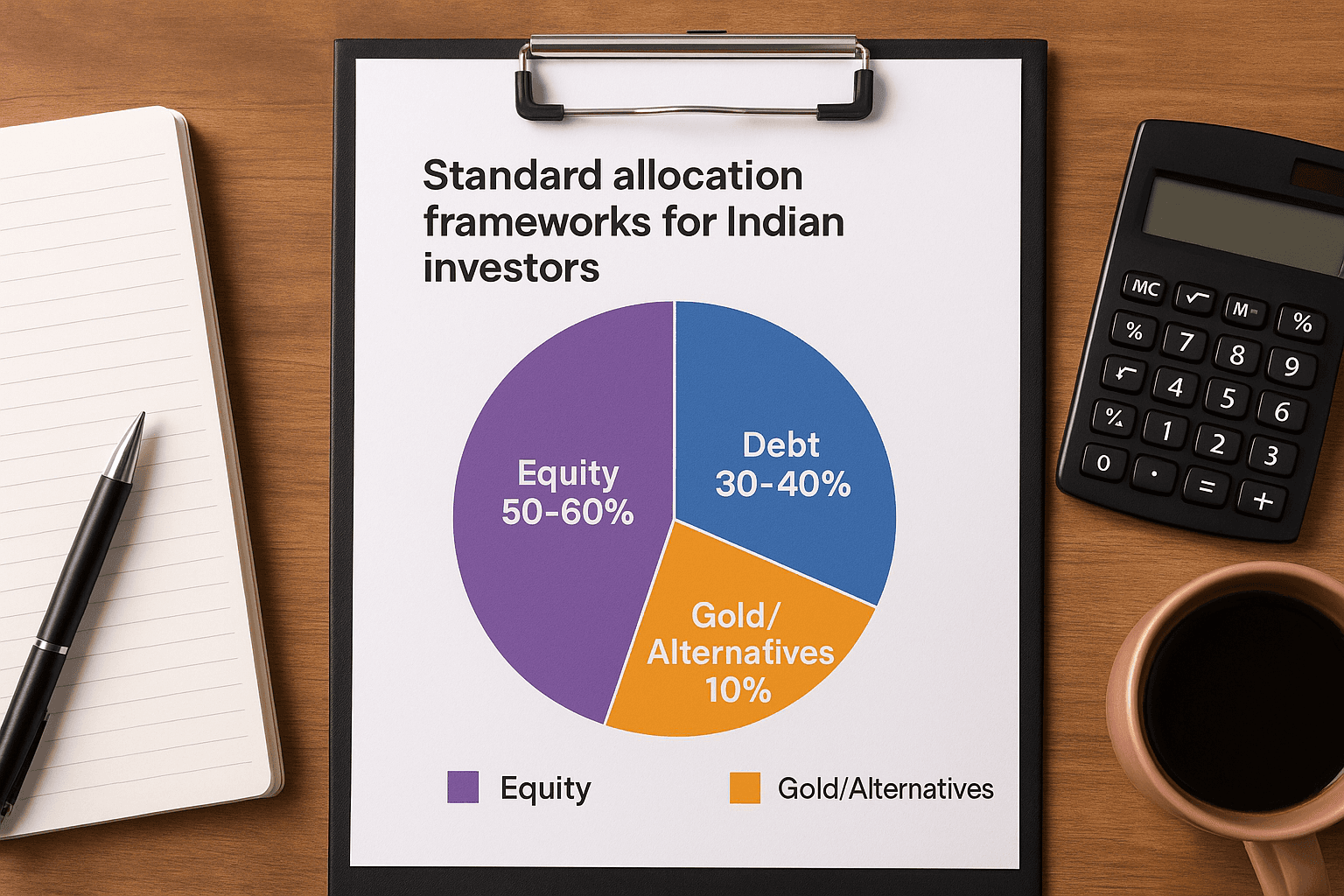

Standard allocation frameworks for Indian investors

Use these baseline allocations as your starting point, then adjust based on your specific goals and constraints. Each profile maps to a different equity-debt split that balances growth potential against downside protection. These ratios assume you've already separated your emergency fund and short-term goal money as covered in Step 1.

Risk Profile | Equity Allocation | Debt Allocation | Gold/Alternatives | Expected Annual Return* | Maximum 1-Year Loss* |

|---|---|---|---|---|---|

Conservative | 20-30% | 60-70% | 10% | 8-10% | -10% to -15% |

Moderate | 50-60% | 30-40% | 10% | 10-12% | -20% to -25% |

Aggressive | 70-80% | 10-20% | 10% | 12-15% | -30% to -40% |

*Historical estimates based on Indian market performance, not guaranteed returns

Conservative investors prioritize capital safety over growth. Your allocation keeps equity exposure minimal, using large-cap index funds or flexi-cap funds for the 20-30% equity portion. The 60-70% debt allocation goes into gilt funds, banking PSU funds, or corporate bond funds based on your tax bracket. This profile works when you're within 5 years of a major goal or cannot afford portfolio losses exceeding 15%.

Moderate profiles balance both objectives by splitting allocations roughly equally between equity and debt. Your 50-60% equity exposure allows participation in market growth while the 30-40% debt cushion reduces volatility during corrections. This allocation suits investors with 7-15 year timelines who completed the questionnaire with mid-range scores.

Aggressive investors maximize long-term growth by accepting significant short-term volatility. Your 70-80% equity allocation can drop 35% in a single year, but historical data shows this approach delivers superior returns over 10+ year periods. Keep the 10-20% debt allocation as a rebalancing source, not as a safety buffer.

Your allocation percentages create the actual risk you experience, not your risk score on a questionnaire.

Adjust for multiple goals with different timelines

Most investors juggle several goals simultaneously, each with its own deadline and importance. Create separate mental buckets rather than maintaining one unified portfolio. Your retirement corpus 20 years away can handle aggressive allocation, while your home down payment due in 4 years needs conservative treatment.

Calculate the present value of each goal, then assign an allocation based on its specific timeline. If you need ₹15 lakh in 4 years for your child's higher education, that ₹15 lakh gets a conservative 30-70 equity-debt split regardless of your overall aggressive profile. Your ₹50 lakh retirement portfolio with 25 years remaining takes the full 80% equity exposure your risk profile allows.

Select specific instruments for each allocation

Break down your allocation percentages into actual mutual fund categories and investment products available to Indian investors. Your equity allocation spreads across market capitalizations and investment styles to prevent concentration risk in any single segment.

For a moderate 60% equity allocation on a ₹10 lakh portfolio:

Large-cap index fund: ₹2.5 lakh (25%)

Flexi-cap active fund: ₹2 lakh (20%)

Mid-cap fund: ₹1 lakh (10%)

Small-cap fund: ₹0.5 lakh (5%)

Debt allocation of 30% (₹3 lakh) divides between:

Liquid fund for emergency access: ₹1 lakh (10%)

Short-duration fund: ₹1 lakh (10%)

Corporate bond fund: ₹1 lakh (10%)

Gold allocation of 10% (₹1 lakh) goes into gold ETFs or sovereign gold bonds for better tax efficiency than physical gold. This granular breakdown transforms your wealth management risk assessment into an executable investment plan with specific fund selections and target amounts for each category.

Step 5. Document and review your risk profile

Your completed wealth management risk assessment becomes useful only when you create a permanent written record that guides future decisions. Write down your risk score, selected allocation percentages, and the reasoning behind each choice in a document you can reference during market volatility. This written profile prevents emotional reactions from overriding your carefully considered risk assessment when fear peaks during corrections. Store this document with your investment policy statement or financial plan, not buried in email attachments you'll never find again.

Create a written risk profile document

Use this template to formalize your risk assessment results. Fill in each section with your specific data, then save it as a PDF with the completion date in the filename.

Set review triggers and timelines

Review your risk profile annually even if nothing significant changes in your life. Market experience affects your tolerance, and gradual income growth or debt reduction increases your capacity. Schedule this review for the same month each year, preferably during a quarter when markets are stable rather than during extreme bull runs or crashes.

Trigger immediate reviews when major life events occur. Job changes, marriage, home purchases, child births, or inheritance all shift your financial capacity and require allocation adjustments. Don't wait for your annual review if you suddenly need to redirect funds toward a new goal or if your income stability changes dramatically.

Tools, templates, and Indian rules to know

SEBI mandates specific documentation standards for wealth management risk assessment that apply to registered investment advisors, but you should follow the same framework even when managing your own portfolio. Understanding these regulatory requirements protects you from unsuitable product recommendations and ensures your risk profiling meets professional standards. The right tools and templates transform your assessment from rough guesswork into a repeatable process you can update as your financial situation evolves.

SEBI risk profiling requirements for advisors

Registered Investment Advisors (RIAs) must complete a written risk profile for every client before recommending any investment product. SEBI's 2013 Investment Adviser Regulations specify that advisors document your financial situation, investment objectives, and risk tolerance through standardized questionnaires. This creates an audit trail proving the advisor matched recommendations to your actual capacity and tolerance levels rather than pushing high-commission products.

Your risk profile must be reviewed and updated whenever significant changes occur in your income, expenses, financial goals, or investment timeline. SEBI requires advisors to maintain these records for at least five years, which means your documented assessment becomes legal evidence if disputes arise about suitability. Even if you self-manage your investments without an advisor, applying this same documentation standard protects you from your own future second-guessing during market crashes.

Following SEBI's framework ensures your wealth management risk assessment meets the same professional standards that regulate the financial services industry.

Free risk assessment template

Download and complete this structured template to formalize your risk profile. Save your completed assessment as a dated PDF so you can compare how your profile evolves over multiple years.

Portfolio tracking and rebalancing tools

Use portfolio management apps like Kuvera, ET Money, or Paytm Money to track your actual allocation against your target percentages. These platforms show your current equity-debt split automatically by aggregating holdings across multiple AMCs. Set up quarterly alerts to check if your allocation has drifted more than 5% from your target due to market movements.

Consolidate your holdings under a single CAMS or KFintech login to simplify tracking across fund houses. Both platforms provide free consolidated account statements (CAS) that list all your mutual fund investments in one document. Your CAS becomes the source data for calculating whether rebalancing is needed to restore your target allocation percentages.

Tax optimization by risk profile

Conservative profiles using debt-heavy allocations face different tax treatment than aggressive equity-focused portfolios. Debt mutual fund gains held over three years attract 20% tax with indexation benefits, while equity funds enjoy complete tax exemption on long-term gains up to ₹1.25 lakh per year. Your risk profile directly determines your annual tax liability on investment returns.

Structure your debt allocation between taxable and tax-free instruments based on your income bracket. If you fall in the 30% tax slab, PPF and EPF contributions within Section 80C limits make more sense than taxable debt funds for your conservative allocation. Tax-saving calculations must factor into your wealth management risk assessment because post-tax returns determine your actual wealth accumulation rate.

Key takeaways and next step

Your wealth management risk assessment gives you a concrete framework for making investment decisions that match your actual financial capacity and emotional tolerance. Start with your financial boundaries by calculating emergency funds and goal timelines, then complete a structured questionnaire to score your risk profile. Map that score to specific equity-debt allocations, write down your targets, and review annually or when life circumstances change significantly.

Most investors skip documentation and rely on memory or gut feel when markets crash, which leads to panic selling and destroyed returns. Your written risk profile becomes your behavioral anchor during volatility, reminding you why you chose your allocation when fear tempts you to abandon your plan.

Take action today by completing the risk assessment template provided in this guide. If you need AI-powered guidance that incorporates your risk profile into personalized investment recommendations, start your risk assessment on Invsify where you'll get conflict-free advice backed by SEBI registration and transparent pricing without hidden distributor commissions.