What Are Direct Mutual Funds? Meaning, Benefits, Vs Regular

Shlok Sobti

What Are Direct Mutual Funds? Meaning, Benefits, Vs Regular

If you've ever invested through a bank or distributor, you've likely paid more than you realized. That extra cost? It's the commission built into regular mutual fund plans. Understanding what are direct mutual funds could save you lakhs over your investment lifetime, and it starts with knowing where your money actually goes.

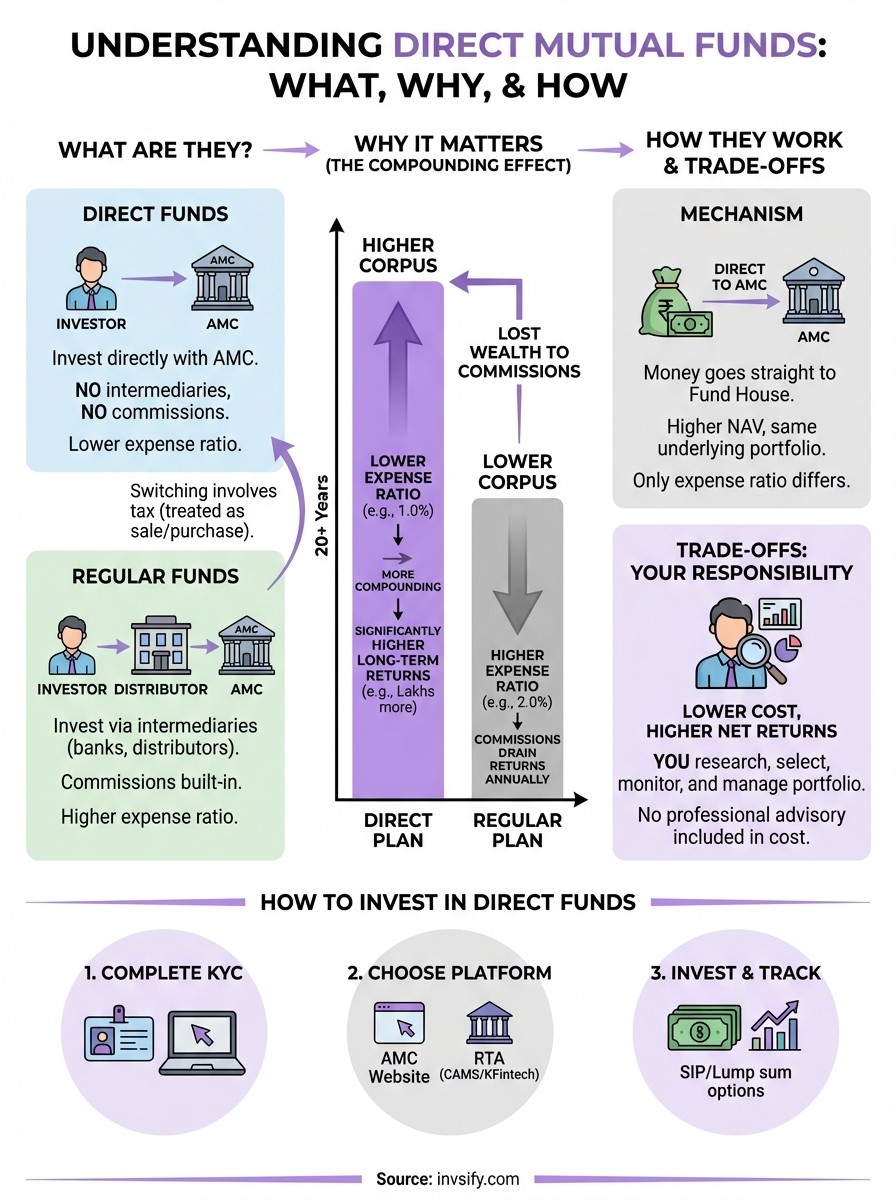

Direct mutual funds let you invest directly with the fund house, cutting out intermediaries entirely. No middlemen means no commissions, which translates to a lower expense ratio. Over 10, 20, or 30 years, this difference compounds into significantly higher returns. For Indian salaried professionals building long-term wealth, this isn't a minor detail, it's a major advantage.

Here's the thing: knowing the difference between direct and regular funds is just the starting point. At Invsify, we help investors make smart, conflict-free investment decisions using AI-powered insights and SEBI-registered advisory. You get the cost benefits of direct funds without navigating the complexity alone.

This article covers everything you need: the meaning of direct mutual funds, how they compare to regular funds in terms of expense ratios and returns, and practical ways to invest in them.

Why direct vs regular mutual funds matters

You're not just choosing between two labels when you pick direct or regular mutual funds. You're deciding how much of your money stays invested and how much gets diverted to intermediaries. This choice affects your final corpus more than most investors realize, especially over 15 to 30 years when compounding amplifies even small differences.

Regular mutual funds include a distributor commission inside the expense ratio. Fund houses pay distributors from your investment, typically between 0.5% to 1% annually. Direct mutual funds eliminate this commission entirely because you bypass the middleman. The difference looks small on paper, but when compounded over decades, it transforms into lakhs of rupees that could have been yours.

The commission structure you don't see

When you invest through a bank or distributor, they earn a trail commission from the fund house for as long as you stay invested. This commission gets deducted from your returns every single year, not just once. The fund house recovers this cost by charging a higher expense ratio on regular plans compared to direct plans.

The expense ratio difference typically ranges from 0.5% to 1.5% depending on the fund type. Equity funds usually have a gap of 0.7% to 1%, while debt funds see differences of 0.4% to 0.6%. These percentages might sound trivial, but they compound against you year after year. Understanding what are direct mutual funds means recognizing this hidden cost that regular plans carry.

Regular plans don't disclose commissions separately on your statement. You only see a higher expense ratio, which makes the true cost invisible to most investors.

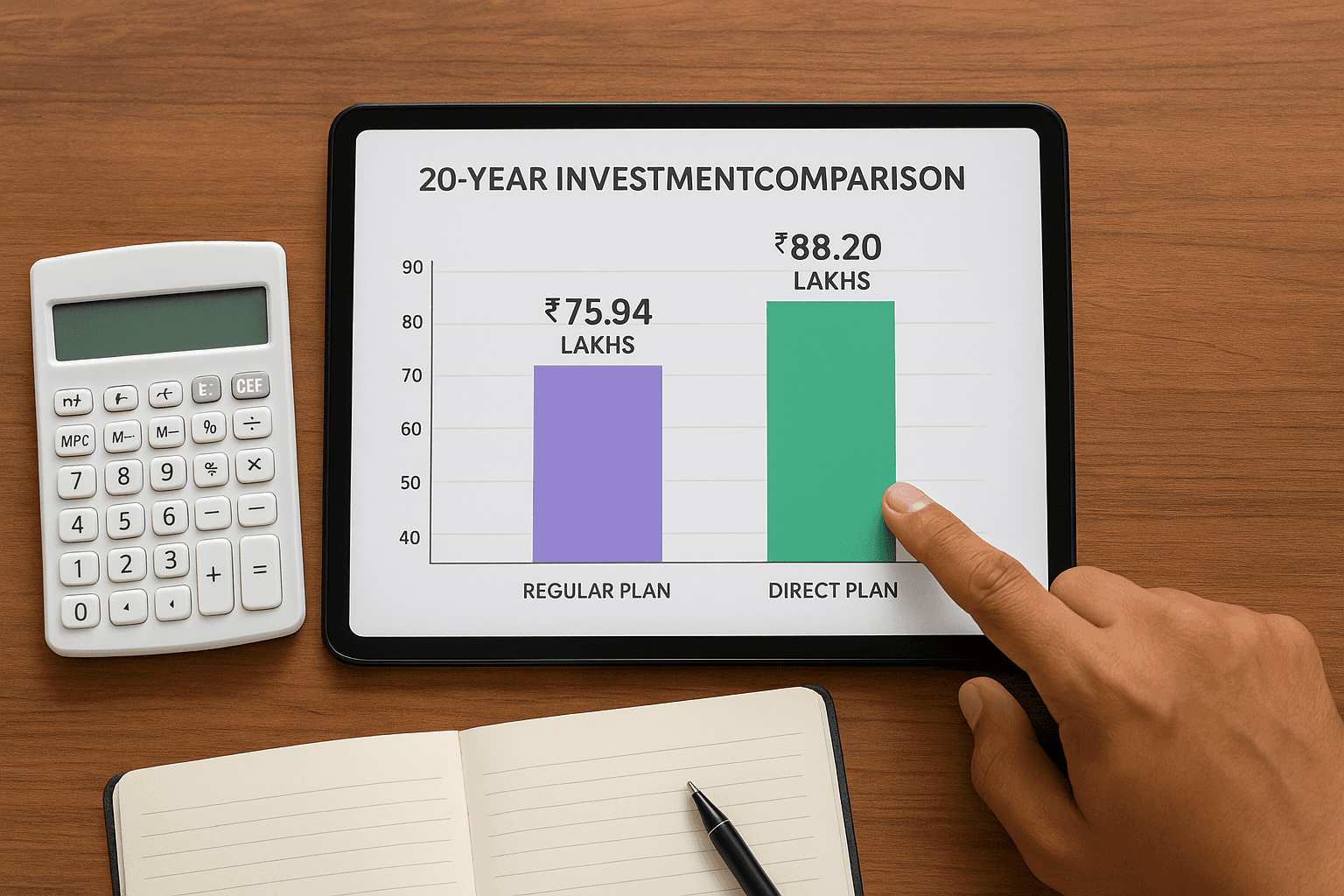

Real numbers: 20-year investment comparison

Imagine you invest ₹10,000 monthly in an equity fund for 20 years with an average return of 12% before expenses. A regular plan with a 2% expense ratio (10% net return) grows your corpus to approximately ₹75.94 lakhs. A direct plan with a 1% expense ratio (11% net return) reaches ₹88.20 lakhs. That's a difference of ₹12.26 lakhs, money that went to commissions instead of your retirement or goals.

The gap widens further with longer time horizons. Over 30 years, the same monthly investment at similar rates creates a difference exceeding ₹50 lakhs between direct and regular plans. Your distributor earns more than you save if you stick with regular plans for long-term goals.

Who should care most about this difference

Salaried professionals building retirement corpus face the largest impact. The longer your investment horizon, the more the commission cost compounds. If you're 30 years old planning for retirement at 60, that 0.8% annual difference becomes the cost of an entire house in many Indian cities.

DIY investors who research funds independently pay unnecessarily when they invest through regular plans. You're doing the work but still paying for advice you didn't need. Younger investors starting SIPs in their 20s or 30s should prioritize direct plans because their 30 to 40-year investment timeline magnifies even minor expense differences into substantial wealth loss.

How direct mutual funds work in India

Direct mutual funds operate through a straightforward mechanism that removes the traditional distributor layer from the investment process. You invest directly with the Asset Management Company (AMC) that manages the fund, either through their website, mobile app, or designated platforms. The AMC processes your investment, allots units, and manages your portfolio without sharing any portion of the expense ratio with distributors.

SEBI regulations mandate that every mutual fund scheme offer both direct and regular plans as separate options. The underlying portfolio remains identical in both plans, meaning the fund manager invests your money in the same stocks or bonds regardless of which plan you choose. The only difference lies in the expense ratio charged, which affects your net returns over time.

The investment flow without intermediaries

When you invest in a direct plan, your money travels straight from your bank account to the AMC. The AMC credits units to your folio based on the applicable Net Asset Value (NAV) for that day. You receive the same units, same fund management, and same investment strategy as regular plan investors, but you pay a lower expense ratio because no commission gets deducted for distributors.

Your investment gets recorded directly in your name with the AMC maintaining your folio records. SEBI's Know Your Customer (KYC) requirements apply equally to both direct and regular plans. Once you complete KYC with any SEBI-registered intermediary, you can invest in direct plans across all fund houses without repeating the process.

AMC registration and direct plan access

Every major fund house in India provides online platforms where you can register and invest in direct plans. You create an account on the AMC's website or app, complete your KYC verification if not done earlier, and link your bank account. Some AMCs offer instant registration while others may take one to two working days for verification.

Multiple channels exist for direct plan investments beyond individual AMC platforms. Registrar and Transfer Agents (RTAs) like CAMS and KFintech allow you to invest in direct plans across multiple fund houses through single platforms. The National Securities Depository Limited (NSDL) also provides direct plan access through its e-CAS facility. Understanding what are direct mutual funds includes knowing these access points that maintain the cost advantage while simplifying your multi-fund portfolio management.

Direct plans don't require you to visit branch offices or submit physical forms. The entire process happens digitally, making it faster and more convenient than traditional investment methods.

Direct vs regular mutual funds: key differences

The distinction between direct and regular mutual funds boils down to three measurable factors that directly affect your wealth accumulation. Expense ratios differ by 0.5% to 1.5%, NAVs reflect this cost difference daily, and your transaction process changes based on where you invest. These differences compound over time, turning small percentage gaps into substantial wealth differences that either stay in your portfolio or get paid out as commissions.

Expense ratio impact on your returns

Direct plans charge lower expense ratios because fund houses don't pay distributor commissions. A typical equity direct plan charges 1.0% to 1.5% while regular plans charge 1.7% to 2.5%. Debt funds show similar patterns with direct plans at 0.3% to 0.8% and regular plans at 0.7% to 1.5%. This percentage difference applies to your entire investment value every year, not just your initial capital.

Your net returns drop by exactly the expense ratio difference when you choose regular over direct plans. An equity fund generating 12% returns gives you approximately 10.5% in a regular plan (assuming 1.5% expense ratio) but 11% in a direct plan (assuming 1% expense ratio). Over 20 years on a ₹10 lakh investment, that 0.5% difference translates to roughly ₹3.5 lakhs less in your final corpus.

The expense ratio gets deducted daily from the fund's assets, so you never see it as a separate charge on your statement. It shows up only as a slightly lower NAV each day.

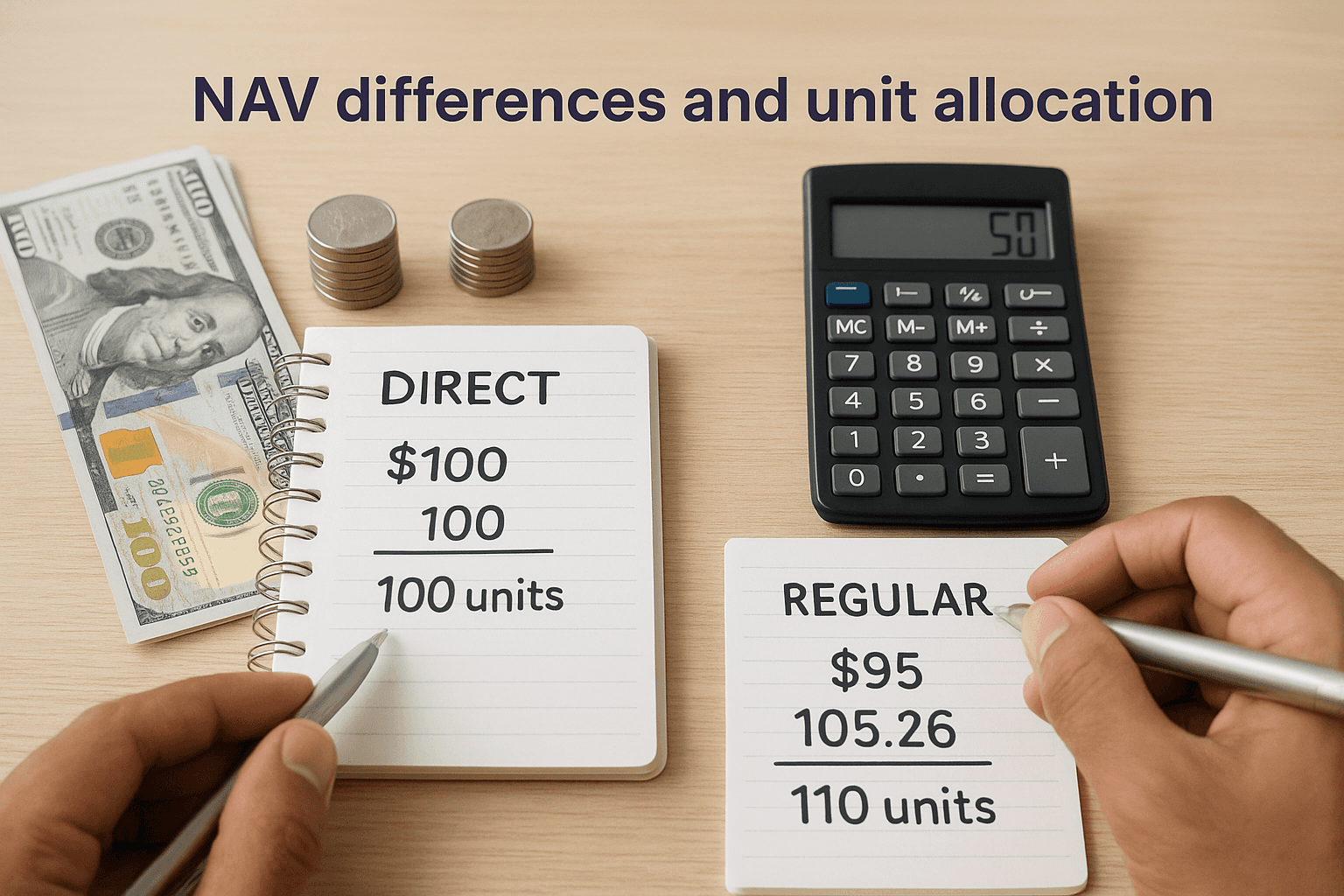

NAV differences and unit allocation

Direct plans show higher NAVs than regular plans for the same fund because they accumulate lower daily expense deductions over time. If a regular plan NAV stands at ₹50, the direct plan might be ₹52 or ₹53 depending on how long the fund has existed and the expense ratio gap. You receive fewer units when investing in direct plans because each unit costs more, but those units grow at a faster rate due to lower ongoing costs.

Unit allocation happens at the same NAV cutoff times for both plan types. If you invest ₹10,000 in a fund with a direct NAV of ₹100, you get 100 units. The same investment in a regular plan with NAV ₹95 gives you 105.26 units. Despite getting fewer units initially in direct plans, your final value exceeds regular plans because growth compounds at a higher net rate.

Transaction process and documentation

You complete direct plan investments through AMC platforms, RTAs, or designated investment portals without intermediary involvement. Regular plans require you to invest through distributors, brokers, or banks who process your transactions and maintain ongoing service relationships. Both plans issue identical account statements showing your holdings, transactions, and current value.

Understanding what are direct mutual funds means recognizing that your documentation remains standardized regardless of plan type. SEBI mandates identical disclosure requirements for both plans, so you receive the same portfolio updates, scheme information documents, and annual reports whether you invest directly or through distributors.

Benefits and trade-offs of direct mutual funds

Direct mutual funds deliver measurable financial advantages alongside practical challenges that you must handle independently. The primary benefit centers on cost reduction that compounds into substantial wealth differences over decades. However, understanding what are direct mutual funds also means accepting that you shoulder complete responsibility for fund selection, portfolio management, and investment decisions without professional guidance from distributors.

Cost savings and compounding advantages

Lower expense ratios translate directly into higher net returns that compound over your investment timeline. You save 0.5% to 1.5% annually compared to regular plans, which might seem minimal initially but grows exponentially over 20 or 30 years. This cost advantage applies every single year regardless of market conditions, creating a permanent boost to your wealth accumulation rate.

Higher NAV growth in direct plans means your portfolio value increases faster than identical regular plan holdings. The transparency also improves because you see exactly where your money goes without hidden commissions reducing your returns. You maintain full control over your investment choices and can switch strategies or rebalance portfolios without considering any distributor relationship or bias.

Direct plans force you to become an informed investor, which builds financial literacy that benefits all your future money decisions beyond just mutual funds.

Responsibilities you take on yourself

You must research funds independently, comparing performance metrics, portfolio composition, and risk factors without professional advisory support. Fund selection becomes your task, requiring you to understand categories like large-cap, mid-cap, debt funds, and hybrid options. Regular monitoring of your portfolio, rebalancing when necessary, and tax-loss harvesting all fall under your responsibility rather than a distributor handling these tasks.

The learning curve can feel steep if you're new to investing or lack time to study fund performance and market trends. You won't receive personalized recommendations based on your risk profile, financial goals, or life stage unless you seek independent advice separately. Documentation and transaction tracking require your active involvement since no relationship manager reminds you about SIP dates or reviews your portfolio quarterly.

When direct plans make most sense

Direct plans suit investors who already understand mutual fund basics and feel comfortable making independent decisions. If you invest through systematic research or follow clear investment strategies like index funds or diversified portfolios, direct plans maximize your returns without sacrificing quality. Younger investors with 20+ year horizons benefit most because the cost savings compound into the largest absolute differences over extended periods.

How to invest in direct mutual funds step by step

Investing in direct mutual funds requires you to handle the process independently, but the actual steps remain straightforward once you understand the sequence. You complete the entire journey digitally without visiting branch offices or filling physical forms. The three-stage process involves verifying your identity, selecting your investment platform, and executing your first transaction within minutes once setup completes.

Step 1: Complete your KYC verification

Your first action involves completing the Know Your Customer process through any SEBI-registered intermediary. You submit your PAN card, Aadhaar card, bank account details, and a recent photograph either through an AMC website, RTA platform, or mutual fund investment portal. Most platforms offer in-person verification (IPV) through video calls that take 5 to 10 minutes, eliminating the need for physical document submission.

Once verified, your KYC status becomes permanent across all mutual fund investments in India. You never repeat this process regardless of how many fund houses or schemes you invest in later. Check your KYC status at any time through the KRA (KYC Registration Agency) websites before starting your investment journey to avoid delays.

Step 2: Choose your investment platform

Select between individual AMC websites for single-fund-house investing or RTA platforms like CAMS and KFintech for multi-fund-house portfolios. AMC platforms work best when you prefer specific fund houses like HDFC, ICICI Prudential, or SBI Mutual Fund. RTA platforms give you access to multiple fund houses through one login, simplifying portfolio management when you diversify across different AMCs.

Register on your chosen platform by providing basic details including name, email, mobile number, and bank account information. Link your bank account through net banking verification or penny drop validation where the platform deposits a small amount to confirm account ownership. Understanding what are direct mutual funds means knowing these platforms maintain your transaction history, generate consolidated statements, and provide portfolio tracking tools.

Platform selection matters less than staying invested, so pick whichever interface feels most comfortable and stick with it for consistency.

Step 3: Select funds and execute transactions

Browse available direct plan options within your chosen fund category based on your investment goals and risk appetite. You enter the investment amount, select lump sum or SIP, and choose the payment method linking to your registered bank account. Most platforms process transactions within 24 hours, with unit allocation happening at the NAV applicable based on the cutoff time you met.

Set up systematic investment plans directly through the platform by selecting monthly dates, amounts, and duration. Your bank account gets debited automatically on chosen dates without requiring manual intervention each month.

FAQs: identification, switching, and taxes

Three questions dominate investor conversations once they understand what are direct mutual funds mean for their returns. You need clear answers on spotting direct plans in your existing holdings, the mechanics of moving from regular to direct plans, and the tax treatment that applies when you redeem units. These practical concerns determine whether you actually capture the cost advantage that direct plans offer.

How do you identify direct mutual funds in your portfolio?

Your account statement displays the plan type explicitly next to each fund name. Look for the word "Direct" in the scheme name on your consolidated account statement or individual fund statements. Regular plans typically show just the scheme name without any suffix, though some platforms add "Regular" for clarity.

The folio number itself doesn't indicate plan type, but you can verify through the RTA websites by entering your PAN. Your statement also shows different NAVs for the same fund if you hold both plan types, with direct plans consistently showing higher values. Check your investment confirmation emails when you purchase units, as these documents clearly mention whether you invested in a direct or regular plan at the transaction level.

Can you switch from regular to direct plans without tax?

Switching requires you to redeem your regular plan units and purchase direct plan units as a separate transaction. SEBI regulations treat this as a sale followed by a fresh purchase, which means capital gains tax applies based on your holding period. You cannot convert existing regular units into direct units within the same folio.

You trigger short-term or long-term capital gains depending on whether you held equity funds for less than one year or debt funds for less than three years. This tax cost often reduces the benefit of switching for investments you made recently. The decision to switch makes financial sense only when your remaining investment horizon exceeds 5 to 7 years, allowing the lower expense ratio advantage to offset the immediate tax hit.

Switching from regular to direct plans works best for fresh investments rather than existing holdings where tax costs eliminate near-term benefits.

What tax rules apply to direct mutual fund redemptions?

Direct and regular plans follow identical tax treatment under Income Tax Act provisions. Equity fund gains held over one year qualify as long-term and attract 12.5% tax beyond ₹1.25 lakh annual exemption. Debt fund gains now get taxed at your income tax slab rate regardless of holding period after April 2023 changes.

Your plan type doesn't affect taxation at all, only the asset class and holding period matter for determining applicable rates. You report gains in your ITR filing the same way whether units came from direct or regular plans.

Key takeaways and next step

Understanding what are direct mutual funds comes down to one financial reality: you keep more of your returns when you eliminate distributor commissions. The 0.5% to 1.5% expense ratio difference compounds into lakhs of rupees over your investment lifetime, money that either stays in your portfolio or gets paid out to intermediaries. Direct plans don't change the underlying investments, they just remove the cost layer that regular plans carry permanently.

Your next move depends on where you stand today. Fresh investors should start with direct plans immediately through AMC platforms or RTAs. Existing regular plan holders need to calculate whether switching makes sense based on remaining time horizons and tax implications. The process itself takes minutes once you complete KYC verification.

You don't have to navigate this alone. Sign up with Invsify to get AI-powered portfolio insights and SEBI-registered advisory that helps you maximize direct plan benefits while avoiding common pitfalls. Smart investing means keeping costs low and returns optimized, exactly what direct mutual funds deliver when paired with conflict-free guidance.