What Is Asset Allocation? Types, Examples, And How It Works

Shlok Sobti

What Is Asset Allocation? Types, Examples, And How It Works

Your investment portfolio might hold excellent stocks, but that alone doesn't guarantee success. The real question is whether your money is distributed wisely across different investment types. This is where understanding what is asset allocation becomes essential for building long-term wealth.

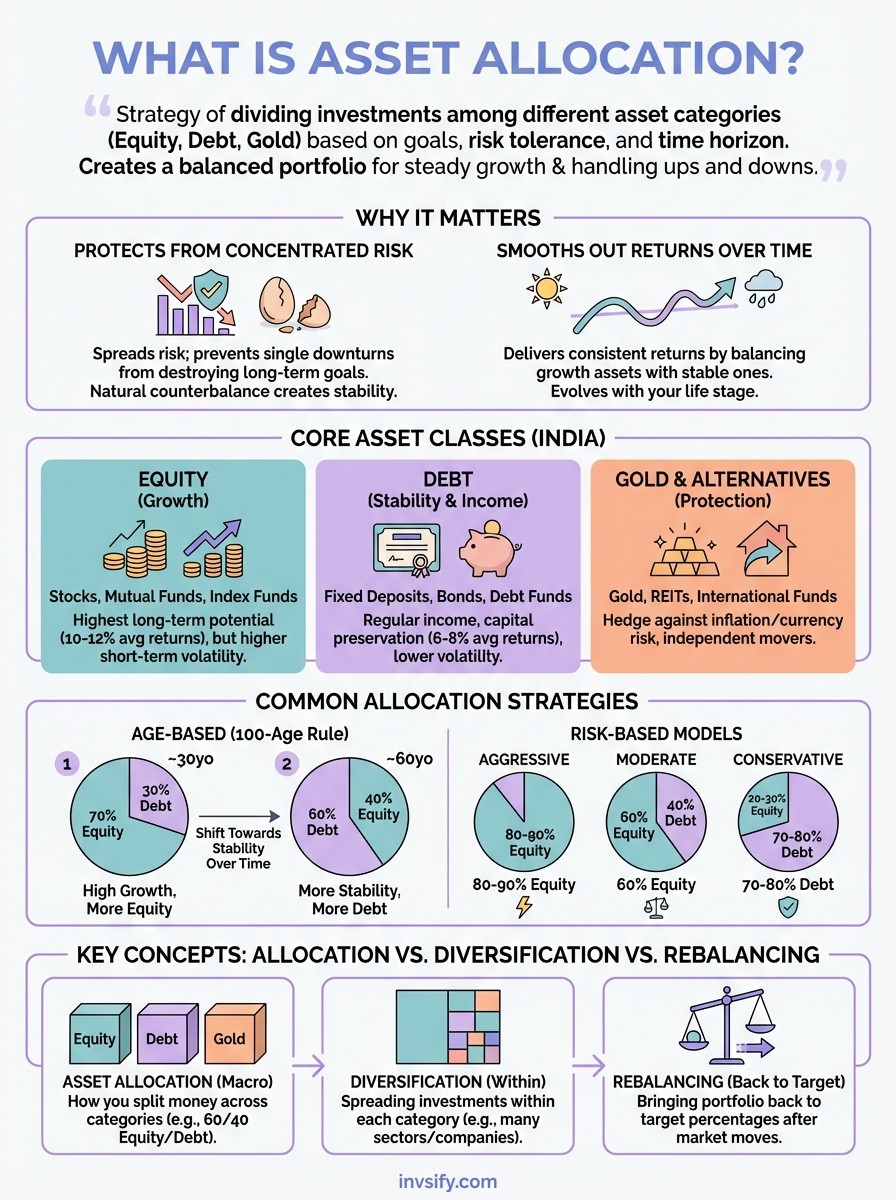

Asset allocation is the strategy of dividing your investments among different asset categories, like equity, debt, and gold, based on your goals, risk tolerance, and time horizon. It's not about picking individual winners; it's about creating a balanced portfolio that can handle market ups and downs while still growing your wealth steadily.

At Invsify, our AI-powered advisory helps you determine the right asset mix tailored to your unique financial situation. In this guide, we'll break down asset allocation, explore the major asset classes, walk through practical examples, and clarify how it differs from diversification. By the end, you'll have a clear framework for making smarter investment decisions.

Why asset allocation matters

Your returns depend less on individual stock picks and more on how you distribute your capital across different asset types. Research shows that asset allocation explains over 90% of portfolio performance variation over time, making it the single most important investment decision you'll make. Understanding what is asset allocation helps you avoid the mistake of putting all your money in one basket.

It protects you from concentrated risk

When you concentrate your investments in a single asset class, you expose yourself to unnecessary volatility and potential losses. If the stock market crashes and your entire portfolio sits in equity, you could see substantial value erosion that takes years to recover. Asset allocation spreads your risk across multiple categories, so poor performance in one area doesn't sink your entire wealth.

Asset allocation acts as your financial safety net, ensuring that no single market downturn can destroy your long-term goals.

Different asset classes rarely move in the same direction at the same time. Bonds typically rise when stocks fall, and gold often performs well during inflation or market uncertainty. This natural counterbalance within your portfolio creates stability without sacrificing growth potential.

It smooths out your returns over time

Markets move in cycles, and timing these perfectly is impossible. A well-allocated portfolio delivers more consistent returns by balancing growth assets with stable ones. You won't experience the extreme highs of an all-equity portfolio, but you'll also avoid the crushing lows that derail financial plans.

Your asset allocation also evolves with your life stage. Younger investors can tolerate more equity exposure for higher growth, while those nearing retirement need greater stability through debt and safer assets. This dynamic approach ensures your portfolio always matches your current risk capacity and financial timeline.

Asset classes you can allocate across in India

Understanding what is asset allocation requires knowing the building blocks available to you. Indian investors have access to multiple asset classes, each serving different purposes in your portfolio. Your allocation choice depends on your goals, risk appetite, and the unique characteristics of each category.

Core growth assets

Equity investments include stocks, equity mutual funds, and index funds that offer the highest growth potential over long periods. You can invest directly in shares through exchanges or choose managed funds that pool money across multiple companies. Equity historically delivers 10-12% average annual returns but comes with significant short-term volatility that requires patience.

Equity forms the growth engine of your portfolio, but only when you give it sufficient time to overcome market fluctuations.

Stability and income assets

Debt instruments encompass fixed deposits, bonds, and debt mutual funds that provide regular income and capital preservation. These assets generate 6-8% returns with much lower volatility than equity, making them essential for near-term goals and portfolio stability. Government securities, corporate bonds, and bank deposits all fall into this category.

Protection and alternative options

Gold serves as an inflation hedge and currency protection tool that often moves independently of stocks and bonds. Real estate investment trusts (REITs) and international exposure through mutual funds add further diversification beyond traditional Indian assets. These alternatives help you build a truly balanced portfolio resistant to local market shocks.

Common asset allocation strategies and models

Investors follow proven frameworks rather than guessing how to distribute their money. These models provide starting points you can customize based on your specific situation. Understanding what is asset allocation strategies means knowing which approach matches your financial profile best.

Age-based allocation models

The traditional 100-minus-age rule suggests subtracting your age from 100 to determine your equity percentage. A 30-year-old would hold 70% in equity and 30% in debt, while a 60-year-old maintains 40% equity and 60% debt. This approach gradually reduces risk as you approach retirement when you need capital preservation over growth.

Your allocation should naturally shift toward stability as your investment timeline shortens and income-generating years decline.

Risk-based approaches

Aggressive portfolios allocate 80-90% to equity for investors comfortable with volatility and holding periods exceeding ten years. Moderate allocations typically split 60% equity and 40% debt, balancing growth with some stability for medium-term goals. Conservative strategies favor 70-80% debt instruments with minimal equity exposure, suitable for near-term needs or risk-averse investors nearing retirement.

Each model serves different investor profiles, and you can adjust percentages based on your income stability, financial obligations, and comfort with market fluctuations. The right strategy aligns with both your goals and your ability to stay invested during downturns.

How to build an asset allocation step by step

Building your ideal asset mix doesn't require complex calculations or expensive advisors. You can create a solid allocation by following a systematic process that matches your personal situation. Once you understand what is asset allocation and why it matters, implementing it becomes straightforward with the right framework.

Assess your financial timeline and risk tolerance

Start by identifying when you need your money and how much volatility you can stomach. Goals within five years need conservative allocations with more debt, while retirement funds 20 years away can handle higher equity exposure. Your risk tolerance depends on both your emotional comfort with losses and your financial capacity to recover from downturns.

Your allocation succeeds only when you can stay committed during market drops without panic selling.

Calculate your target percentages

Use your age and timeline to determine initial splits between equity, debt, and alternatives. A 35-year-old saving for retirement might target 65% equity, 30% debt, and 5% gold. Someone five years from retirement should shift toward 40% equity and 60% debt for capital preservation. Adjust these numbers based on your income stability and existing financial cushion.

Select specific investment vehicles

Choose mutual funds, index funds, or direct stocks that fit each asset class category. Equity mutual funds or index funds offer diversified stock exposure without individual stock risk. Debt mutual funds or fixed deposits fulfill your stability requirement, while sovereign gold bonds or gold ETFs provide alternative asset exposure efficiently.

Asset allocation vs diversification and rebalancing

Many investors confuse these three concepts, but each plays a distinct role in portfolio management. Understanding what is asset allocation versus diversification and rebalancing helps you implement all three effectively. Asset allocation determines how you split money across asset classes like equity, debt, and gold. Diversification spreads investments within each asset class, while rebalancing maintains your target allocation over time.

What makes them different from each other

Asset allocation answers the macro question of which asset types you should own and in what proportions. If you decide on 60% equity and 40% debt, that's your allocation. Diversification operates within those categories, spreading your 60% equity across multiple sectors, companies, and market capitalizations to reduce concentrated risk.

Allocation protects you from entire asset class collapses, while diversification shields you from individual investment failures.

Rebalancing brings your portfolio back to target percentages after market movements push them off course. Strong equity performance might shift your 60/40 split to 70/30, increasing your risk beyond comfort levels. Periodic rebalancing sells winners and buys underperformers, maintaining your intended risk profile.

How they work together in your portfolio

These strategies form a complete risk management framework when used together. Your allocation creates the foundation, diversification strengthens each component, and rebalancing keeps everything aligned. Without allocation, diversification lacks direction. Without rebalancing, your carefully planned allocation drifts with market movements and exposes you to unintended risks.

Final takeaways

Understanding what is asset allocation gives you the foundation for building wealth that survives market cycles. Your portfolio's success depends more on how you distribute capital across asset classes than on picking individual winners. The right mix balances growth potential with downside protection based on your timeline, risk tolerance, and financial goals.

Start by defining your investment horizon and comfort with volatility. Choose percentages across equity, debt, and alternatives that match your profile. Remember that diversification within each category and regular rebalancing complete your risk management framework. Your allocation should evolve as you age and your goals change.

Invsify's AI-powered advisory removes the guesswork from asset allocation by analyzing your unique financial situation and recommending optimal splits tailored to your needs. Get your personalized allocation strategy and start building a portfolio designed for long-term success with transparent, conflict-free guidance.