What Is Digital Investing? Meaning, Benefits, And Examples

Shlok Sobti

What Is Digital Investing? Meaning, Benefits, And Examples

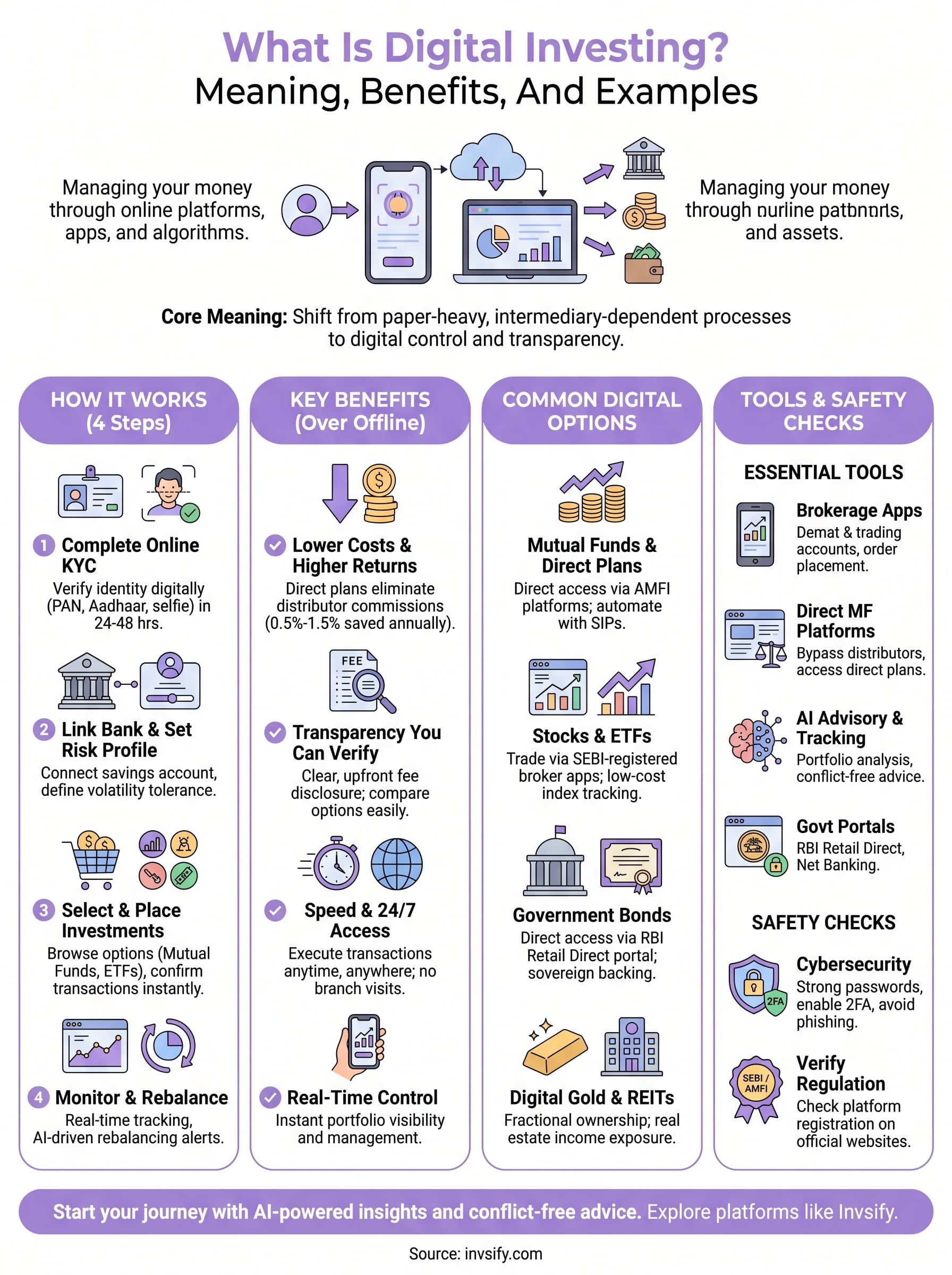

A decade ago, most Indians managed their investments through a local distributor or bank relationship manager. You'd sit across a desk, sign a stack of forms, and hope the advice you received wasn't shaped by the commissions earned on selling you a particular product. That's changed. What is digital investing, exactly? It's the shift from those paper-heavy, intermediary-dependent processes to managing your money through online platforms, apps, and algorithms, giving you more control, transparency, and access than ever before.

This shift matters because it directly addresses problems that Indian investors have dealt with for years: hidden fees eating into returns, limited access to quality advice, and the inability to track portfolios in real time. Digital investing removes many of these friction points by putting powerful tools directly in your hands, whether that's AI-driven portfolio analysis, automated rebalancing, or instant access to direct mutual funds.

At Invsify, we built our SEBI Registered Investment Advisory platform around this exact idea, using AI-powered insights and conflict-free advice to help salaried professionals grow and protect their wealth without the baggage of traditional distribution models. This article breaks down what digital investing means, walks through its real benefits backed by how the industry actually works, and gives you concrete examples of platforms and asset types you can explore. Whether you're just getting started or rethinking how you manage your portfolio, this guide covers what you need to know.

What digital investing means in plain English

When people ask what is digital investing, the simplest answer is this: it's using internet-connected tools, apps, and platforms to buy, sell, manage, and monitor financial assets without visiting a branch, signing physical documents, or relying on a human intermediary for every step. The process replaces paper with dashboards and algorithms that work around the clock, giving you visibility and control that traditional methods never offered.

The core idea: technology replaces paper-heavy processes

Traditional investing in India meant calling your bank's relationship manager, filling out forms at an AMC office, or handing money to a distributor who would invest it on your behalf. The problem wasn't just the inconvenience. Hidden commissions and limited transparency meant you often didn't know how much you were paying or whether the advice you received was truly in your interest. Digital investing removes those layers. Platforms execute your transactions directly, show you exactly what fees apply, and let you track every rupee in real time.

The shift from offline to digital investing isn't just about convenience. It changes who controls the information and who ultimately benefits from your money.

This change matters especially for salaried Indian professionals who don't have hours to spend visiting offices or chasing paperwork. A few taps on your phone can complete a KYC process, set up a SIP, or rebalance your portfolio based on updated market data. The technology handles the administrative work so you can focus on the decisions that actually affect your financial future.

What counts as digital investing (and what doesn't)

Digital investing covers a wide range of activities and asset types. Buying mutual funds through a direct plan on an online platform counts. Purchasing stocks through a mobile trading app counts. Investing in government bonds through the RBI Retail Direct portal counts. Even robo-advisors that automatically allocate your money based on your risk profile fall under this category. What ties all of these together is the use of online infrastructure to initiate, execute, and manage investments without physical paperwork as the primary requirement.

What doesn't count: if your advisor sends you a form over a messaging app and you print it, sign it, and courier it back, that's not digital investing, even if part of the communication happened online. The defining feature is whether the actual transaction and record-keeping happen through a regulated electronic system, end to end.

The role of regulation and trust in digital platforms

One concern you might have is whether digital platforms are safe and properly overseen. In India, SEBI (the Securities and Exchange Board of India) regulates investment advisors, brokers, and mutual fund platforms. A platform that carries SEBI registration operates under defined rules about how it handles your money, discloses conflicts of interest, and maintains your account data. This oversight is no different from what applies to traditional advisors, and in many respects digital platforms face stricter disclosure requirements because their operations are more visible and auditable.

Trusting a digital platform comes down to checking two things: whether it holds the appropriate SEBI or AMFI registration, and whether it clearly explains how it earns money. A conflict-free advisory model charges you a flat fee rather than earning commissions from the products it recommends. That structure matters because it aligns the platform's incentives directly with your financial outcomes, not with pushing specific products onto your portfolio.

How digital investing works step by step

Understanding what is digital investing becomes much clearer once you see the actual process laid out. The steps are more straightforward than most people expect, and modern platforms handle the administrative load so you spend less time on paperwork and more time on decisions that actually shape your financial future.

Step 1: Complete your KYC online

Before you invest a single rupee, you need to verify your identity through KYC (Know Your Customer). On digital platforms, this happens entirely online. You upload your PAN card, proof of address, and a live selfie through the platform's app or website. Most platforms complete verification within 24 to 48 hours, and you never need to visit an office or courier physical documents anywhere.

Step 2: Link your bank account and set a risk profile

Once your KYC clears, you connect your savings account to the platform for fund transfers. This step also involves completing a risk profiling questionnaire, which helps the platform understand how much volatility you can handle and what your investment horizon looks like. Your answers directly shape the asset allocation suggestions you receive going forward, so answering honestly here matters more than most people realize.

Getting your risk profile right from the start prevents you from allocating money to instruments that don't match your actual financial situation or time horizon.

Step 3: Select your investments and place transactions

With your account active, you can browse available investment options such as mutual funds, stocks, bonds, or ETFs, depending on what the platform supports. You pick the instrument, enter the amount, and confirm. The platform routes your order through the appropriate exchange or registrar, and you receive a digital confirmation almost immediately. For mutual funds, units get allocated at the applicable NAV for that day's cut-off time.

Step 4: Monitor performance and rebalance when needed

Digital investing doesn't stop at the purchase. Your portfolio dashboard updates in real time, showing you current values, returns, and asset allocation across all your holdings in one place. When your allocation drifts from your original targets, because some assets have grown faster than others, you can rebalance by trimming positions and adding to others. AI-powered platforms flag these rebalancing needs automatically, which reduces the chance of missing an important adjustment during a busy work week. This ongoing visibility is one of the biggest practical differences between digital and offline investing.

Why people choose digital investing over offline methods

Once you understand what is digital investing, the reasons people move away from traditional offline methods become clear. Offline investing carries structural disadvantages that quietly reduce your returns and limit your control, and most investors only realize this after years of paying costs they didn't fully understand. Digital platforms fix several of these problems at once, which explains why more Indian salaried professionals are making the switch every year.

Lower costs that show up directly in your returns

Traditional distributors earn commissions, often between 0.5% and 1.5% of your invested amount annually, by recommending regular mutual fund plans instead of direct plans. Over 20 years, that difference compounds into a significant gap in your final corpus. Direct plans available on digital platforms carry no distributor commission, which means more of your money stays invested and compounds on your behalf. On a portfolio of ₹50 lakh, even a 1% annual fee difference adds up to several lakh rupees by retirement.

The fee gap between regular and direct mutual fund plans is not a minor detail. Over a long investment horizon, it can amount to a larger sum than most investors expect.

Transparency you can verify yourself

Offline advisors rarely show you a full breakdown of what you're paying, and many investors go years without knowing their portfolio includes products generating commissions for the distributor. Digital platforms present fee structures clearly on screen, show you exactly which plan you're buying, and let you compare options before you commit. You don't need to ask twice or wait for a statement that may arrive weeks later.

SEBI mandates that registered investment advisors disclose all fees and potential conflicts of interest. Digital advisory platforms that operate under SEBI RIA registration follow these rules and typically make their disclosures easy to find, not buried in a document you'd never read.

Speed and access without geography limiting you

Traditional offline investing ties your access to business hours, branch locations, and the availability of a specific person. If you work in a city without a strong advisory presence, your options narrow considerably. Digital platforms operate around the clock, from any location with internet access, and execute transactions within minutes rather than days.

For salaried professionals managing demanding work schedules, this flexibility is not a luxury. It means you can review your portfolio during a lunch break, increase your SIP amount before the next installment date, or respond quickly when market conditions shift without waiting for a callback that may never come on time.

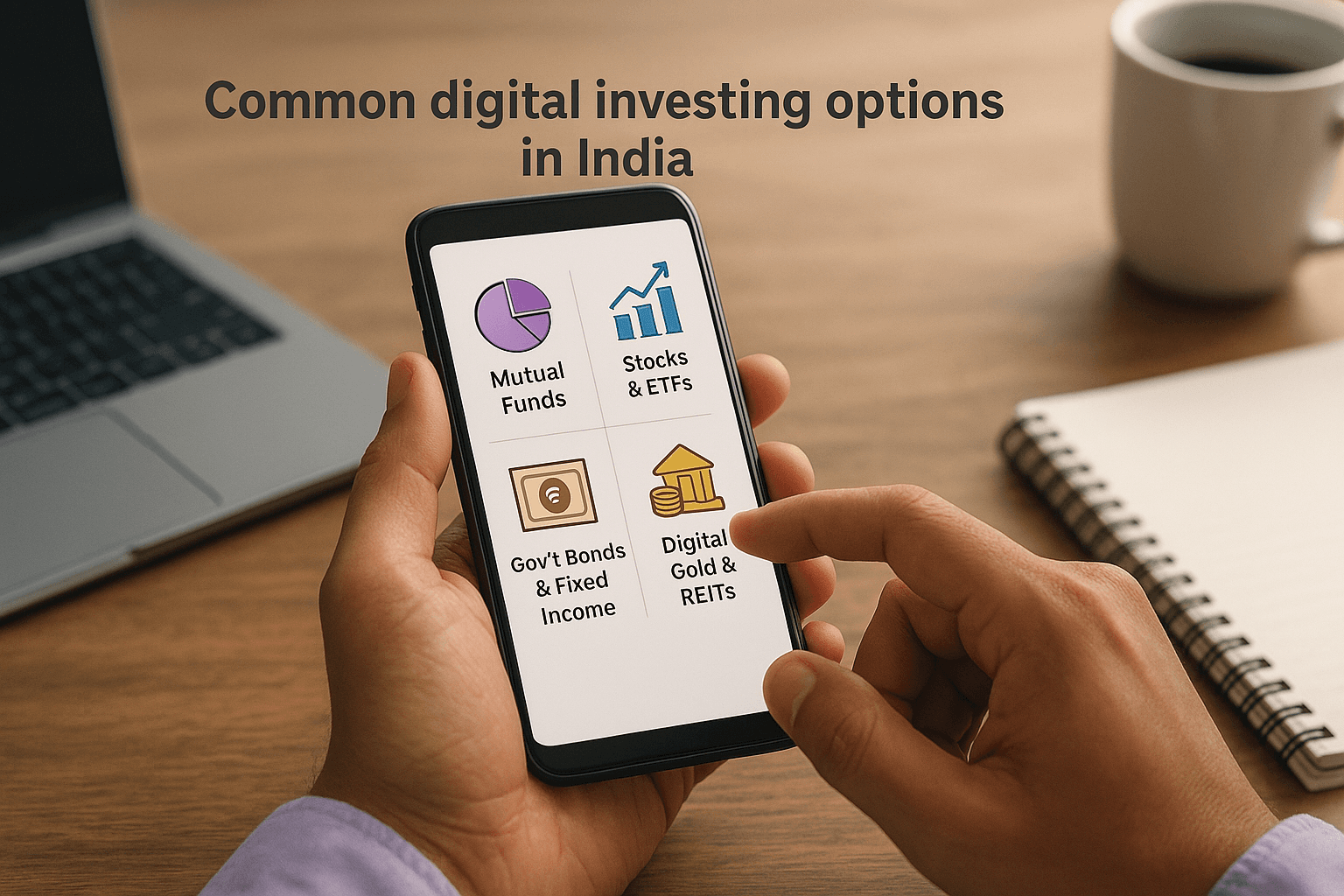

Common digital investing options in India

One of the most practical ways to understand what is digital investing is to look at the actual instruments available to you right now. Indian investors have a wider range of assets accessible through digital channels than at any earlier point, and knowing your options helps you build a portfolio that matches your actual financial goals rather than whatever a distributor happens to push your way.

Mutual funds and direct plans

Mutual funds are the most widely used digital investment option for salaried Indians, and direct plans are the key reason digital access matters here. By investing through a direct plan, you eliminate the distributor layer entirely, which means more of your money compounds over time instead of going toward commissions. SIPs let you automate monthly contributions starting from as little as ₹500, and AMFI-registered platforms give you access to funds across equity, debt, hybrid, and index categories.

Switching from a regular plan to a direct plan on your existing mutual fund investments is one of the simplest, highest-impact decisions you can make as an investor.

Stocks and ETFs

Direct equity investing through a SEBI-registered broker lets you buy shares in individual companies through your demat account, with transactions settling electronically. For investors who prefer a lower-maintenance approach, ETFs (Exchange Traded Funds) track an index like the Nifty 50 and trade on the exchange like stocks, giving you broad market exposure at low cost without requiring you to research individual companies in depth. Both options are fully accessible through mobile trading apps.

Here is a quick comparison of the two:

Option | Control | Effort Required | Cost |

|---|---|---|---|

Direct stocks | High | High | Brokerage per trade |

ETFs | Low | Low | Low expense ratio |

Government bonds and fixed-income instruments

The RBI Retail Direct portal gives you direct access to government securities, including Treasury Bills and dated Government Bonds, without going through a broker or bank. These instruments carry sovereign credit backing, which means your principal faces minimal default risk compared to corporate bonds or equity. For salaried investors building a stable, predictable portion of their portfolio, this option delivers transparency on pricing that offline fixed-income investing rarely offers.

Digital gold and REITs

Digital gold lets you buy fractional amounts of gold starting from a single rupee, without storing physical metal or worrying about purity. REITs (Real Estate Investment Trusts) give you exposure to commercial real estate rental income through a listed, tradeable instrument. Both are accessible through standard brokerage apps at lower entry points than their offline equivalents, making them practical additions to a diversified portfolio.

Tools and platforms you will use to invest online

Understanding what is digital investing also means knowing which tools actually handle your money and which ones help you make smarter decisions about it. The landscape in India includes SEBI-regulated brokers, direct mutual fund platforms, government portals, and AI-powered advisory services, and each serves a distinct purpose in a well-organized portfolio. Choosing the right combination matters more than using every tool available.

Brokerage apps for stocks and ETFs

SEBI-registered brokers provide your demat and trading account, which you need to buy and sell stocks, ETFs, and bonds on the NSE or BSE. Most major brokers now offer mobile apps that handle order placement, portfolio tracking, and tax reporting from a single dashboard. When selecting a broker, pay attention to the brokerage fee structure and whether the platform gives you access to IPOs, ETFs, and government securities in addition to regular equities. A lower per-trade cost compounds meaningfully over years of active investing.

The broker you pick shapes your access to instruments, your fee burden, and how clearly you can see your total investment picture in one place.

Mutual fund platforms and direct plan access

Direct mutual fund platforms let you bypass distributors entirely, so every rupee you invest goes into a direct plan rather than a regular one. These platforms connect directly to AMFI-registered fund houses, show you the full fund universe with sorting by category and performance, and let you set up SIPs or lump-sum investments within minutes. Look for platforms that provide clear comparisons between direct and regular expense ratios so you can see exactly how much you save by choosing direct.

AI-powered advisory and portfolio tracking tools

Beyond execution, AI-driven advisory platforms analyze your full portfolio and flag gaps, concentration risks, or rebalancing needs that you might miss when reviewing holdings manually. These tools pull data from your demat account, mutual fund folio, and other assets to build a unified view of your wealth across all instruments. Platforms like Invsify go further by combining AI recommendations with SEBI RIA-backed conflict-free advice, so the guidance you receive comes without the bias of commission-based incentives.

Government portals worth bookmarking

The RBI Retail Direct portal gives you direct access to government bonds and Treasury Bills without a broker. For tax-saving fixed deposits and PPF contributions, most public sector banks now offer fully digital account management through their net banking portals. These options require no third-party platform and carry sovereign or government-backed credibility that makes them reliable anchors in a diversified digital portfolio.

Risks, fees, and safety checks you should not skip

Any honest answer to what is digital investing has to include the risks alongside the benefits. Digital platforms give you speed and access, but that same accessibility means your account is always exposed to potential threats if you don't take basic precautions. Understanding where the risks sit, and what to check before you invest, protects your portfolio from problems that most people only learn about after something goes wrong.

Cybersecurity and account safety

Your trading and mutual fund accounts hold direct access to your money, which makes them targets for phishing, SIM-swap fraud, and unauthorized logins. Use a strong, unique password for each financial platform and always enable two-factor authentication, preferably through an authenticator app rather than SMS. Never click links in unsolicited messages claiming to be from your broker or fund platform, even if the sender looks legitimate.

One compromised account can undo years of disciplined investing, and recovering funds lost to fraud is difficult and slow through most platforms.

Check your registered mobile number and email address on each platform regularly. If either changes without your knowledge, report it immediately to the platform's support team and to SEBI's SCORES portal, which handles investor complaints against registered entities.

Fees that reduce your actual returns

Most digital platforms charge clearly, but you still need to read the fee schedule before you commit. Brokerage apps typically charge a flat fee or a percentage per trade. Mutual fund direct plans carry an expense ratio that gets deducted from the fund's NAV daily, so it doesn't show as a separate charge but still affects your returns. Advisory platforms that charge a flat annual fee are usually more transparent than those earning behind-the-scenes trail commissions.

Avoid platforms that earn from product recommendations without disclosing how. Conflict-free advisory, backed by a SEBI RIA registration, gives you the clearest fee structure because the platform earns from you directly, not from the funds it suggests.

Regulatory checks before you commit money

Before putting money into any digital platform, verify its registration on the SEBI or AMFI website using the official search tools available there. A SEBI-registered investment advisor carries a registration number you can look up independently. Mutual fund platforms must hold AMFI registration, and brokers must carry a valid SEBI broker license linked to a recognized exchange like NSE or BSE. These checks take under five minutes and confirm that the platform operates under enforceable rules, not just marketing promises.

How to start digital investing as an Indian salaried earner

Now that you understand what is digital investing and where the risks sit, the practical question is how to actually begin. Most salaried professionals in India hold the common misconception that starting requires a large lump sum or financial expertise. You need neither. The real requirements are a verified identity, a bank account, and a clear sense of what you want your money to do over the next five to ten years.

Get your documents and accounts in order

Your PAN card is the single most important document for any investment account in India. Beyond that, you need a proof of address, a bank account for fund transfers, and a mobile number linked to your Aadhaar for eKYC. Most platforms complete identity verification entirely online, and the process takes under 30 minutes from start to finish.

Before you open a brokerage or mutual fund account, gather the following:

PAN card

Aadhaar card (for eKYC)

Bank account details with IFSC code

A passport-size photograph in digital format

Your income details for risk profiling

Pick a starting point that matches your goal

Starting with direct mutual funds through a SEBI-registered platform is the most practical entry point for a salaried investor in India. You get broad market exposure, low entry amounts through SIPs, and a well-regulated structure without needing to analyze individual stocks before you build enough knowledge to do so with confidence.

Your first investment doesn't need to be your best investment. Starting with a small, consistent SIP teaches you how markets behave far better than reading about them ever will.

Your risk profile answers are the foundation for every allocation decision that follows, so complete the profiling questionnaire carefully and revisit it whenever your income or financial responsibilities change significantly.

Set a monthly amount and automate it

Choose a SIP amount you can sustain every month without disrupting your household budget, even during months with unexpected expenses. Starting at ₹1,000 a month and increasing it annually by 10% creates a disciplined investing habit that compounds meaningfully over time.

Automating your SIP removes the decision from your monthly routine, which means you don't skip contributions during volatile markets or busy work periods. This consistency matters more than timing the market perfectly, and digital platforms make automation straightforward once your bank mandate is active.

Conclusion

Understanding what is digital investing goes beyond knowing the definition. It means recognizing that you now have access to tools, platforms, and fee structures that give you a genuine advantage over the commission-heavy, paperwork-driven methods that shaped Indian investing for decades. Direct plans, AI-powered portfolio tracking, government bond portals, and conflict-free advisory have all become accessible from your phone, with SEBI oversight ensuring the same regulatory standards that apply offline.

The shift to digital investing rewards the investors who act on this knowledge rather than just reading about it. Your portfolio's long-term growth depends far less on picking the perfect stock and far more on eliminating unnecessary fees, staying consistent through market cycles, and getting advice that works for your interests rather than a distributor's. If you want to start with a platform built around exactly that approach, explore Invsify's AI-powered advisory and get your personalized Wealth Wellness Score.