Expense Ratio in Mutual Funds: What It Is, Formula & Impact

Shlok Sobti

Expense Ratio in Mutual Funds: What It Is, Formula & Impact

Expense ratio is the annual fee you pay for owning a mutual fund. Think of it as the cost of fund management expressed as a percentage of your investment. When you invest Rs. 1 lakh in a fund with a 1% expense ratio, you pay Rs. 1,000 per year for the fund house to manage your money. This covers everything from portfolio management to administrative costs. The fee gets deducted daily from your investment before the Net Asset Value (NAV) is declared, so you never see it as a separate charge. But here's what is expense ratio in mutual funds really about: it directly eats into your returns, and even a small difference can cost you lakhs over time.

This guide breaks down expense ratios in practical terms. You'll learn how the fee is calculated, when it's charged, and what counts as a good ratio for Indian mutual funds. We'll show you how different expense ratios impact your wealth over 10, 20, and 30 years with real numbers. You'll also discover which factors drive costs up or down and how to use this metric when choosing between funds. By the end, you'll know exactly how much you're paying and whether it's worth it.

Why expense ratio matters in mutual funds

You lose money to expense ratios every single day you hold a mutual fund. The fee gets deducted from your investment value before the NAV is announced, which means your returns shrink automatically. Most investors ignore this cost because it happens silently in the background. But over decades of investing, expense ratios can destroy 20-30% of your total wealth. When you're choosing between two large-cap funds with similar portfolios, the one with a lower expense ratio will almost always make you richer in the long run. This is exactly what is expense ratio in mutual funds boils down to: a hidden tax on your financial future.

The compounding impact on your wealth

Your expense ratio compounds negatively over time. When you pay 1% annually, you're not just losing Rs. 1,000 on a Rs. 1 lakh investment this year. You're also losing all the future returns that Rs. 1,000 would have generated. Over 20 years at 12% returns, that Rs. 1,000 would have grown to Rs. 9,646. Multiply this effect across every year of your investment, and the real cost becomes massive. A fund with 2% expense ratio versus 0.5% can cost you Rs. 8-10 lakhs extra on a Rs. 10 lakh investment held for 30 years.

The difference between a 0.5% and 1.5% expense ratio can cut your final corpus by 15-20% over 25 years.

How small differences add up over time

Consider two funds with identical 12% gross returns. Fund A charges 0.5% expense ratio, giving you 11.5% net returns. Fund B charges 1.5%, leaving you with 10.5%. On a Rs. 10 lakh investment over 30 years, Fund A grows to Rs. 2.49 crores while Fund B reaches only Rs. 1.96 crores. That's a Rs. 53 lakh difference from just 1% higher fees. Your fund house gets rich while you lose half your retirement corpus. This gap widens further when you compare actively managed funds (1.5-2.5% expense ratio) against index funds (0.1-0.5%). The expense ratio determines whether your money works for you or for the fund manager.

How to understand and calculate expense ratio

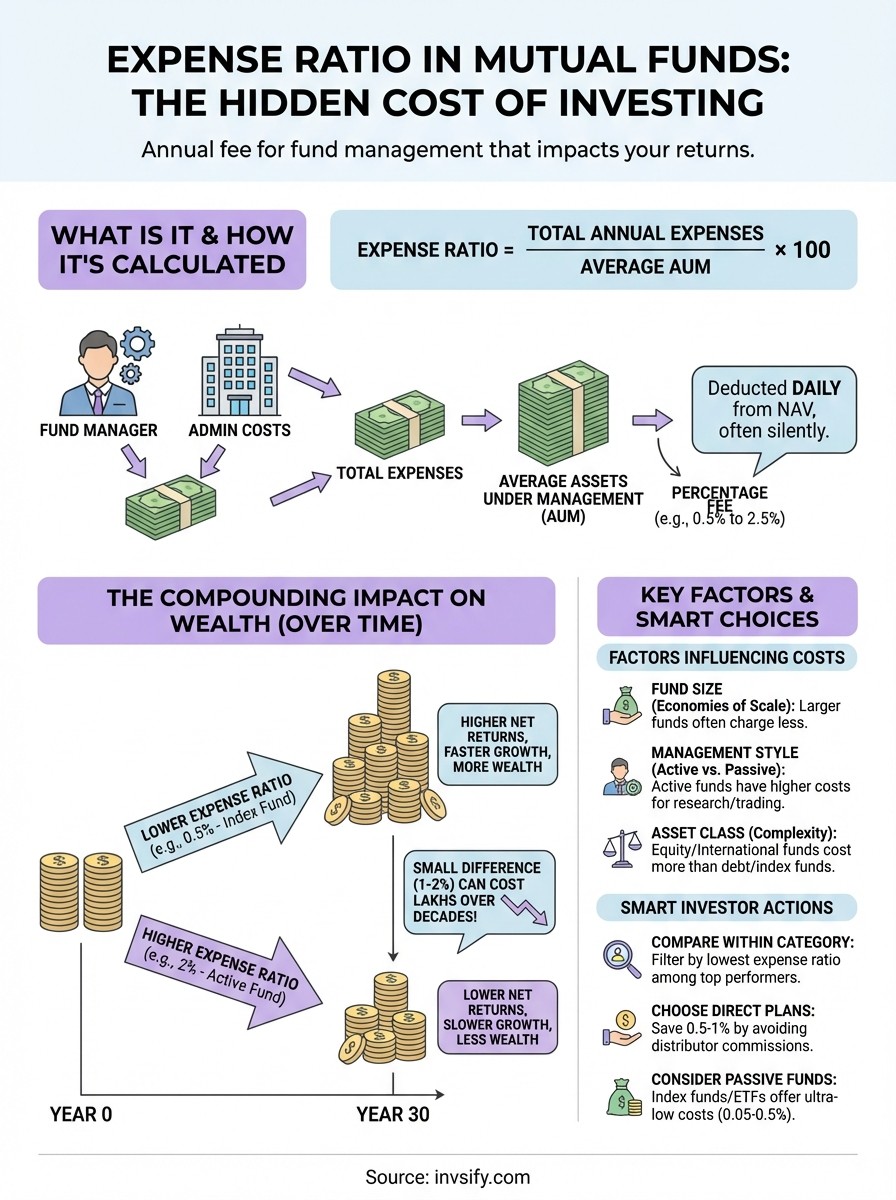

You calculate the expense ratio by dividing the total annual expenses of a mutual fund by its average assets under management (AUM). The formula is straightforward: Expense Ratio = (Total Annual Expenses / Average AUM) × 100. This percentage tells you exactly how much you pay each year for every rupee invested. Understanding what is expense ratio in mutual funds starts with this simple math, but the devil lives in the details. Your fund house bundles multiple costs into this single number, and knowing what goes inside helps you evaluate whether the fee is justified.

The basic expense ratio formula

The calculation works like this: if a fund has Rs. 500 crores in AUM and spends Rs. 10 crores annually on operations, the expense ratio equals (10 / 500) × 100 = 2%. This means you pay Rs. 2 for every Rs. 100 invested per year. Fund houses deduct this amount daily from the NAV before announcing it, so a fund with Rs. 50 NAV actually earns slightly more but reports less after expenses. You never write a separate check for this fee. The deduction happens automatically throughout the year, which is why most investors remain blind to the true cost of fund ownership.

Expense ratios hide in plain sight by reducing your NAV daily, making them harder to spot than direct fees.

Breaking down total expense ratio (TER) components

Your expense ratio covers several distinct costs that fund houses incur. Management fees form the largest chunk, paying portfolio managers and research analysts who pick stocks or bonds for your fund. Distribution and marketing costs go toward commissions paid to distributors, advertising campaigns, and investor education materials. Administrative expenses include legal fees, audit costs, custodian charges, and technology infrastructure that tracks your investments. Fund houses also pay registrar fees for maintaining investor records and processing transactions. Regular plans carry higher expense ratios than direct plans because they include distributor commissions of 0.5-1%, which direct investors avoid entirely.

Real calculation examples from Indian mutual funds

Consider HDFC Top 100 Fund with Rs. 25,000 crore AUM spending Rs. 500 crores annually. The expense ratio equals (500 / 25,000) × 100 = 2%. If you invest Rs. 1 lakh, you pay Rs. 2,000 per year in fees. Now compare this to an index fund like UTI Nifty Index Fund with Rs. 5,000 crore AUM and Rs. 25 crores in expenses. The expense ratio drops to (25 / 5,000) × 100 = 0.5%, costing you only Rs. 500 annually on the same Rs. 1 lakh investment. Your Rs. 1,500 savings might seem small today, but compounded over 20 years at 12% returns, that difference grows to Rs. 48,231. Check your fund's factsheet on the AMC website or AMFI portal to find its current expense ratio listed clearly at the top.

When expense ratio is charged in India

Your mutual fund charges the expense ratio every single day without asking for your permission or sending you a bill. The fund house deducts this fee before announcing the NAV each evening, which means you never see the gross returns your investments actually generate. Understanding what is expense ratio in mutual funds includes knowing exactly when this cost hits your portfolio. The daily deduction model differs completely from one-time charges like entry or exit loads, making it easier to miss but more damaging over time. SEBI regulates the maximum limits fund houses can charge, but within those caps, the deduction happens automatically throughout your investment journey.

Daily deduction from your NAV

Your expense ratio gets deducted 365 days a year as long as you hold the fund. If your fund charges 1% annually, the AMC actually deducts approximately 0.00274% daily (1% divided by 365 days). When your fund earns Rs. 100 in a day, the expense ratio of say Rs. 2.74 gets removed before the NAV increases. You see only the net change in your statement, never the gross earnings minus expenses separately. This daily deduction compounds negatively against you because the fee applies to your entire corpus, not just profits. Your fund could lose money on a particular day, and you'd still pay the expense ratio on the full investment value.

The expense ratio charges you even on days when your fund loses money, making it a guaranteed cost regardless of performance.

How timing differs from other mutual fund charges

Entry loads and exit loads work completely differently from expense ratios in India. SEBI banned entry loads in 2009, so you pay nothing when you buy mutual fund units today. Exit loads apply only when you redeem your investment before a specified period, typically 1% if you withdraw within the first year. These are one-time charges that you can calculate and avoid by holding funds longer. Expense ratios charge you continuously throughout ownership, whether you buy, hold, or do nothing. Transaction charges of Rs. 100-150 apply only on investments above Rs. 10,000 and occur just once per purchase. Your expense ratio runs silently in the background every single day, making it the most persistent cost of mutual fund investing.

What is a good expense ratio for Indian funds

A good expense ratio depends entirely on which type of fund you're buying and whether you choose direct or regular plans. SEBI sets maximum limits, but fund houses often charge less than these caps. Understanding what is expense ratio in mutual funds in the Indian context means comparing your fund against category averages, not absolute numbers. An actively managed equity fund at 1.5% might be reasonable, while the same ratio for an index fund would be highway robbery. Your goal should be finding the lowest expense ratio within each category while maintaining quality fund management.

Fund category benchmarks that matter

Equity funds in India typically charge 0.5% to 2.25% depending on their AUM and investment strategy. Large-cap equity funds averaging 1.5-1.8% are acceptable if they consistently beat their benchmark. Mid-cap and small-cap funds can justify slightly higher ratios of 1.8-2.25% because they require more research and active management. Index funds and ETFs should never exceed 0.5%, with the best ones charging just 0.05-0.20%. Debt funds charging above 1.5% are overpriced unless they're highly specialized strategies. International funds typically run 1.5-2% due to additional compliance costs. Any fund charging the SEBI maximum should raise red flags unless it delivers consistently superior returns that more than compensate for the higher fee.

Index funds charging above 0.5% are essentially taxing you for doing almost no active work.

Direct plans versus regular plans

Regular plans in India charge 0.5-1% more than direct plans of the exact same fund because they include distributor commissions. Your regular plan expense ratio of 2% becomes 1% in the direct plan, doubling your effective returns over time. This difference exists purely to pay intermediaries, adding zero value to your investment performance. Direct plans have become the obvious choice for educated investors who can research funds themselves or use fee-based advisors. A debt fund regular plan at 1.5% versus direct at 0.8% means you're paying nearly twice as much for someone to fill out a form on your behalf. Switch to direct plans immediately if you're currently in regular plans, especially for long-term holdings where the cost difference compounds brutally against you.

Factors that influence expense ratios

Several forces push expense ratios up or down, and none of them have anything to do with how much your fund actually earns. The type of fund you choose, its size, and the investment strategy all determine what you pay annually. Understanding these drivers helps you decode what is expense ratio in mutual funds and why two seemingly similar funds charge vastly different amounts. Your fund house faces real costs to operate, but many charge far more than necessary simply because investors don't compare. Knowing which factors create legitimate higher costs versus pure profit-taking puts you in control.

Fund size and economies of scale

Larger funds spread their fixed costs across more investors, which naturally lowers the expense ratio for everyone. A fund managing Rs. 10,000 crores can hire the same research team and pay the same audit fees as a Rs. 1,000 crore fund, but the per-investor cost drops to one-tenth. This economy of scale explains why massive funds often charge less than smaller competitors even when using identical strategies. SEBI recognizes this dynamic by setting lower maximum expense ratio limits as AUM crosses specific thresholds. Fund houses with Rs. 500 crores in equity AUM can charge up to 2.25%, but this drops to 1.6% beyond Rs. 2,000 crores. Your smaller niche funds naturally cost more to operate per rupee invested, though some fund houses pocket the difference as profit rather than passing savings to investors.

Active versus passive management

Active funds hire expensive research teams and trade frequently to beat the market, which justifies higher expense ratios of 1.5-2.5%. Your fund manager spends money on Bloomberg terminals, company visits, analyst reports, and continuous portfolio rebalancing. Passive funds like index funds and ETFs simply replicate an index, requiring minimal human intervention and almost no trading costs. This fundamental difference explains why your Nifty 50 index fund charges 0.1-0.5% while an actively managed large-cap fund demands 1.5-2%. The strategy itself creates the cost structure, not the fund house's generosity.

Active management's research intensity drives costs 3-10 times higher than passive strategies, regardless of whether it actually delivers better returns.

Asset class complexity

Equity funds cost more to manage than debt funds because stock selection demands deeper analysis and more frequent rebalancing. International funds add currency hedging costs, foreign transaction fees, and compliance with multiple regulators. Your gold ETF needs physical gold storage and insurance, driving costs higher than a simple domestic equity index fund. Sectoral and thematic funds require specialized expertise that commands premium fees. Multi-asset funds juggling stocks, bonds, and commodities need more complex risk management systems. Each layer of complexity adds legitimate operational costs, though fund houses still have wide latitude in how much they actually charge within SEBI limits.

How to use expense ratio to choose mutual funds

You make better investment decisions when you treat the expense ratio as a primary filter, not an afterthought. Start by narrowing your fund choices to specific categories that match your goals, then rank them by expense ratio from lowest to highest. Understanding what is expense ratio in mutual funds transforms into actionable strategy when you systematically eliminate overpriced options before evaluating anything else. Your first screening question should always be: "Am I paying more than the category average, and if so, what extra value am I getting?" This approach forces fund houses to justify their fees with superior performance or unique strategies you can't find cheaper elsewhere.

Compare funds within the same category first

You waste time comparing expense ratios across different fund types because each category has its own cost structure and norms. An actively managed small-cap fund at 2% might be reasonable while a large-cap fund at the same price would be absurd. Pull up three to five top-performing funds in your target category using the AMFI website or your fund platform's screener. List their expense ratios side by side along with their 3-year and 5-year returns. Any fund charging more than 0.25-0.5% above the category average needs to deliver consistently better returns to justify the premium. Eliminate funds in the top quartile of expense ratios unless they also rank in the top quartile of performance after accounting for risk.

Balance expense ratio with performance history

Your cheapest fund isn't always your best choice if it consistently underperforms by more than the fee difference. Calculate the net impact by subtracting each fund's expense ratio from its annualized returns over 5 years. A fund returning 14% with a 2% expense ratio gives you 12% net, while a fund returning 13.5% with a 1% expense ratio delivers 12.5% net. The second fund wins despite lower gross returns because of superior cost efficiency. Watch out for funds with stellar recent performance but high expense ratios, since past returns often mean-revert while fees stay permanent. Your ideal fund combines below-average expenses with above-average risk-adjusted returns measured by Sharpe or Sortino ratios.

Past performance pays you once, but low expense ratios save you money every single year you hold the fund.

Check for hidden costs beyond TER

Your total expense ratio doesn't capture everything you actually pay. Look for transaction charges on purchases above Rs. 10,000, though these one-time Rs. 100-150 fees matter less than ongoing expenses. Check the exit load schedule because some funds charge 1-2% if you withdraw within specific periods. Review the portfolio turnover ratio listed in the factsheet because high turnover creates tax events and trading costs that reduce your returns beyond the stated expense ratio. International funds sometimes have underlying fund fees when they invest in foreign ETFs, adding another 0.3-0.8% in hidden costs. Add all these elements together to calculate your true annual cost of ownership before committing capital.

Prioritize direct plans and passive funds

You instantly cut your expense ratio by 0.5-1% simply by choosing direct plans over regular plans for any fund you select. Visit the AMC website directly or use platforms that offer direct plans without charging advisory fees. For core portfolio allocations representing 60-80% of your money, consider passive index funds or ETFs charging 0.1-0.5% instead of active funds at 1.5-2.5%. Your satellite positions in specialized or tactical strategies can justify higher fees, but your foundational holdings should maximize cost efficiency. Rebalance from regular to direct plans and active to passive funds during your annual portfolio review, prioritizing your largest holdings first where the savings compound most dramatically over time.

Key takeaways on expense ratio

You now understand what is expense ratio in mutual funds and why this single number deserves serious attention when building your portfolio. Your expense ratio determines how much of your money actually works for you versus enriching fund houses. Small differences of 0.5-1% compound into massive wealth gaps over decades, potentially costing you lakhs in retirement savings. Direct plans beat regular plans by default, while passive index funds destroy most actively managed funds after accounting for their lower fees.

Stop accepting high expense ratios as inevitable. Compare funds within categories, eliminate anything charging above average without superior performance, and switch to direct plans immediately if you're stuck in regular plans. Your fund choices today lock in costs that repeat annually for your entire investment journey. Smart investors minimize these guaranteed losses before chasing uncertain returns. Start building a low-cost, AI-optimized portfolio that keeps more money working for your financial goals instead of funding expensive fund management teams.