What Is Investment Decision Making? Steps, Factors, Examples

Shlok Sobti

What Is Investment Decision Making? Steps, Factors, Examples

Every rupee you put to work carries a choice behind it, where to invest, how much risk to take, and when to act. That chain of choices is exactly what investment decision making is about: the process of evaluating options and allocating your money toward assets that align with your financial goals. It sounds straightforward, but most investors, especially salaried professionals in India, either skip the process entirely or rely on unverified tips from social media and online forums, which can quietly erode wealth over time.

Good investment decisions aren't just about picking the right mutual fund or stock. They involve understanding your risk tolerance, analyzing expected returns, factoring in taxes, and reviewing how each choice fits your broader financial plan. Miss any of these steps, and you're essentially guessing with your hard-earned salary. The difference between a structured decision-making process and a haphazard one can amount to lakhs over a 10–20 year horizon.

This is the problem Invsify was built to solve. As a SEBI Registered Investment Advisor, Invsify combines AI-powered analysis with human expertise to help you make smarter, conflict-free investment decisions, no hidden commissions, no guesswork. In this guide, we'll break down the investment decision-making process step by step, cover the key factors that influence your choices, and walk through real examples so you can apply this framework to your own portfolio.

What investment decision making means in finance

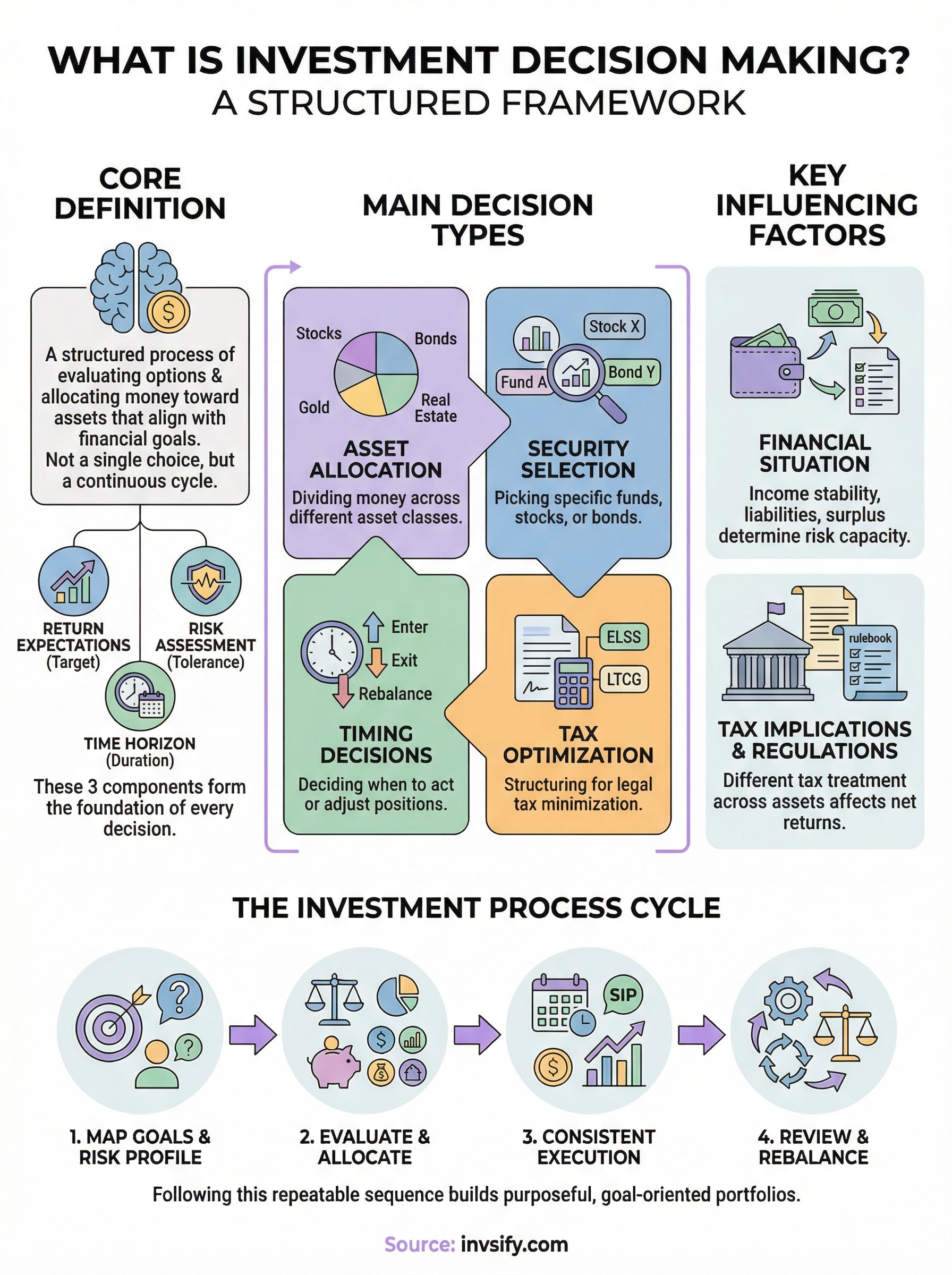

In finance, investment decision making refers to the structured process of evaluating where, when, and how much capital to allocate across different asset classes to meet specific financial goals. It's not a single moment of choice but a continuous cycle of analyzing options, assessing trade-offs, and adjusting your portfolio as your circumstances and market conditions shift. For a salaried professional in India, this process might involve deciding between PPF and ELSS for tax saving, or weighing the risk of direct equity against the relative stability of debt mutual funds.

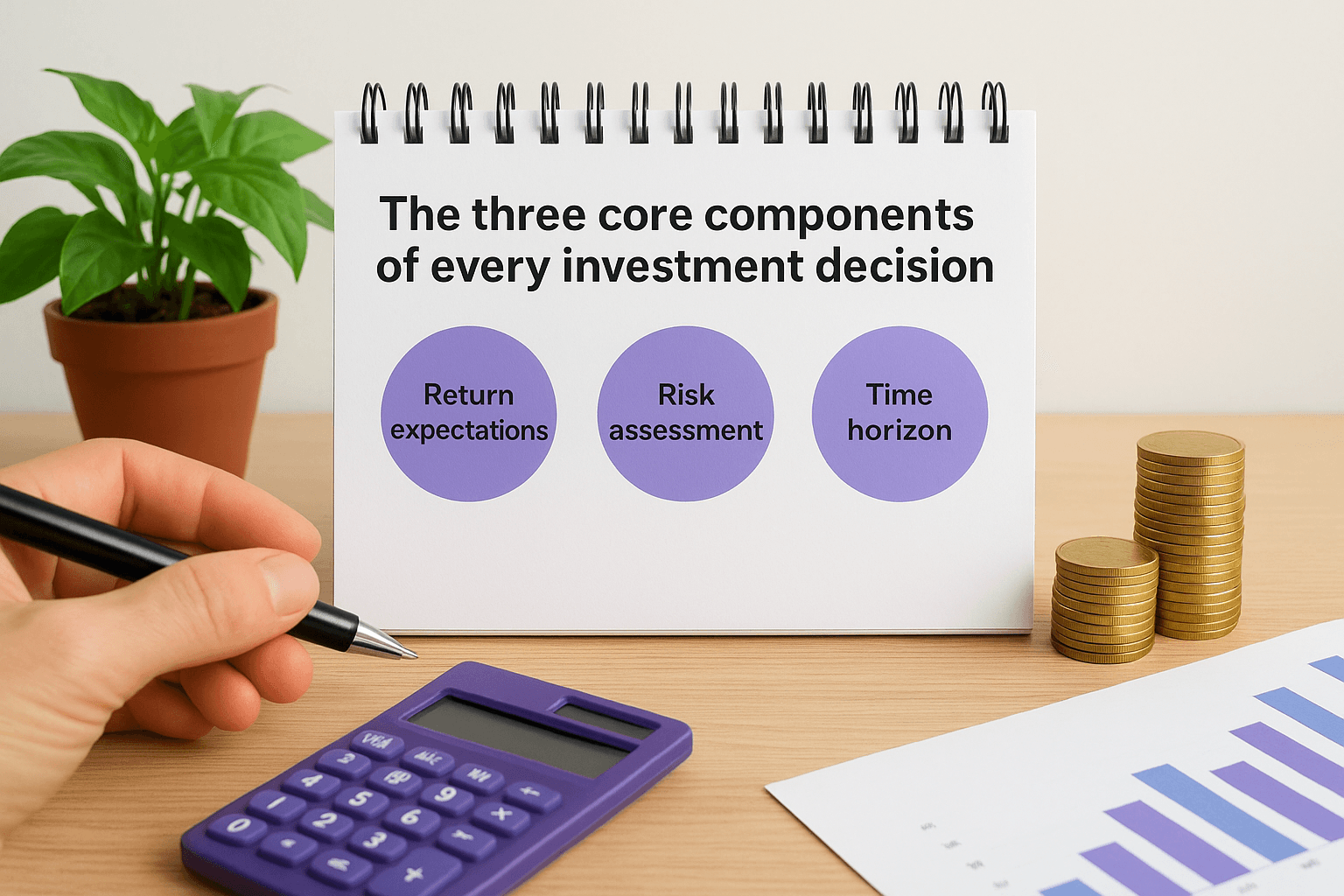

The three core components of every investment decision

Every investment decision you make rests on three core components: return expectations, risk assessment, and time horizon. Return expectations define what you're targeting, whether that's beating inflation, building a retirement corpus, or generating passive income alongside your salary. Risk assessment helps you understand how much volatility you can absorb without abandoning your plan when markets fall. Your time horizon ties the two together, because a 20-year investment runway allows you to take on more risk than a goal you need to fund within two years.

The quality of your investment decision is determined not by the market's short-term reaction, but by how well the choice aligned with your goals and risk profile before you made it.

Understanding these three components is what separates a deliberate investor from someone chasing tips. When you grasp what is investment decision making at its core, you stop reacting to market noise and start building a portfolio with a clear direction.

How risk and return interact in your choices

Risk and return move together in almost every financial instrument you'll encounter. Higher potential returns generally come with higher volatility, and lower-risk instruments tend to offer more modest growth. A fixed deposit in India offers near-guaranteed returns but rarely outpaces inflation meaningfully over a decade. Equity mutual funds, on the other hand, carry short-term price swings but have historically delivered significantly higher real returns over a 10-plus year period.

This relationship forces deliberate trade-offs based on your personal situation. A 28-year-old engineer with a stable income and no immediate large expenses can afford to tilt heavily toward equity-oriented instruments. Someone approaching retirement needs to prioritize capital preservation over aggressive growth. The right balance is never universal; it depends entirely on your financial reality at a given point in life.

The main types of investment decisions

Investment decisions generally fall into a few distinct categories, each requiring a different level of analysis:

Asset allocation decisions: Choosing how to divide your money between equity, debt, gold, and real estate

Security selection decisions: Picking specific funds, stocks, or bonds within each asset class

Timing decisions: Deciding when to enter, exit, or rebalance a position

Tax optimization decisions: Structuring investments to minimize your tax outgo legally, such as using ELSS or long-term capital gains planning

Each category involves its own set of variables, which is why treating investment decision making as one simple act often leads to costly mistakes.

Why investment decision making matters

Most people in India treat investing as a reactive habit: buy when markets look good, sell when panic sets in, and park the rest in a savings account. This approach costs you in ways that are hard to see in the short term but compound significantly over a decade. Understanding what is investment decision making, and actually applying it, changes how you build wealth from a guessing game into a repeatable, goal-oriented process tied to outcomes you actually care about.

The gap between India's average savings account return and a well-managed equity portfolio over 15 years can easily run into tens of lakhs for a salaried professional.

The real price of poor investment choices

When you skip a structured process, you don't just earn lower returns. You also expose yourself to unnecessary risk that isn't compensated by higher potential gains. Buying a thematic fund because a colleague mentioned it at lunch, or redeeming your SIPs during a market correction, are both decisions made without a framework. Over time, these choices accumulate into a portfolio that doesn't align with any specific goal, making it harder to plan for retirement, a home purchase, or your child's education.

Unplanned investments often overlap in risk exposure without adding real diversification

Reactive selling locks in losses that a longer time horizon would have recovered

Ignoring tax efficiency can erode 10 to 20 percent of your realized gains unnecessarily

Why consistency in decision making builds long-term wealth

Consistent, process-driven investing rewards you in two ways: it keeps your emotions out of the equation during volatile periods, and it ensures your portfolio evolves as your income and goals change. A salaried professional who reviews their asset allocation annually and rebalances when needed will almost always outperform someone who invests the same total amount without any structured review. The discipline behind each decision compounds just as powerfully as the returns themselves.

How the investment decision process works

Understanding what is investment decision making is only useful if you can apply it as a repeatable sequence. The process follows a clear structure, and skipping any stage increases the risk that your portfolio drifts away from what you actually need. Each step builds on the one before it, so the quality of your final allocation depends on how carefully you complete the earlier groundwork.

Map your goals and risk profile first

Before you evaluate a single instrument, you need a specific financial goal and an honest assessment of your risk tolerance. A goal gives every future decision a benchmark, whether you're building a retirement corpus by 60 or saving for a home down payment within five years. Your risk profile tells you how much short-term volatility you can absorb without reacting emotionally to a market dip. In India, SEBI-mandated risk profiling exists precisely to formalize this step before any money moves.

Define each goal with a timeline and a target amount

Complete a risk assessment before selecting any asset class

Link each investment to one specific goal so you can measure progress clearly

Skipping goal-setting is the single most common reason salaried investors end up with a portfolio full of unrelated products that serve no clear purpose.

Evaluate, allocate, and review on a schedule

Once your goals and risk profile are in place, you compare instruments across expected returns, liquidity, tax treatment, and time horizon alignment. For a salaried professional in India, this typically means choosing across ELSS, PPF, equity mutual funds, and debt funds based on what each goal actually requires. Asset allocation at this stage determines roughly 90% of your long-term portfolio outcome, so it deserves more deliberate attention than most people give it.

Your investment decisions don't stop at the point of purchase. Markets move, your income grows, and your goals shift, which means you need annual portfolio reviews to stay on course. Rebalancing brings your asset mix back to its intended allocation when market movements push it out of proportion, preventing unintended concentration in a single asset class over time.

Factors that influence investment decisions

No two investors face identical circumstances, which is why understanding what is investment decision making also means recognizing what shapes each choice. The factors that influence your investment decisions aren't random; they fall into predictable categories that you can evaluate systematically before committing capital. Beyond personal finances, broader forces like market conditions, interest rate cycles, and inflation trends all play a role in determining which asset classes are likely to serve your goals at any given point.

Your financial situation and income stability

Your current income, existing liabilities, and monthly surplus directly determine how much risk you can realistically absorb. A salaried professional with a stable monthly income and low EMI obligations can allocate more toward equity-heavy instruments than someone with variable income or significant loan repayments. This isn't just about how much you earn; it's about how secure and predictable that income is over the next few years.

Your investment capacity changes as your income and liabilities shift, which is why revisiting your financial position annually matters as much as reviewing your portfolio returns.

Monthly investable surplus after essential expenses

Existing debt obligations and their repayment timelines

Emergency fund adequacy, typically three to six months of expenses

Tax implications and regulatory framework

Tax treatment differs significantly across asset classes in India, and ignoring this factor quietly reduces your effective returns. ELSS funds offer deductions under Section 80C, long-term capital gains on equity are taxed at 12.5% above one lakh, and debt fund gains are now taxed at your applicable slab rate. Each of these rules creates a real difference in what you actually keep from your investments.

Structuring your investments with tax efficiency in mind can meaningfully improve your take-home returns without requiring you to take on additional risk. For example, placing short-term debt instruments inside a tax-advantaged wrapper or timing equity redemptions to qualify for long-term treatment are decisions that cost you nothing extra in risk but can save you a meaningful portion of your gains each year.

Examples of investment decisions in India

Seeing what is investment decision making in action makes the process far more concrete than any definition. Real investment decisions happen at specific crossroads: choosing between two tax-saving instruments, deciding how to handle a salary increment, or figuring out whether to stay invested during a sharp market fall. The examples below reflect situations that salaried professionals in India face regularly, and each one illustrates a different layer of the decision-making framework.

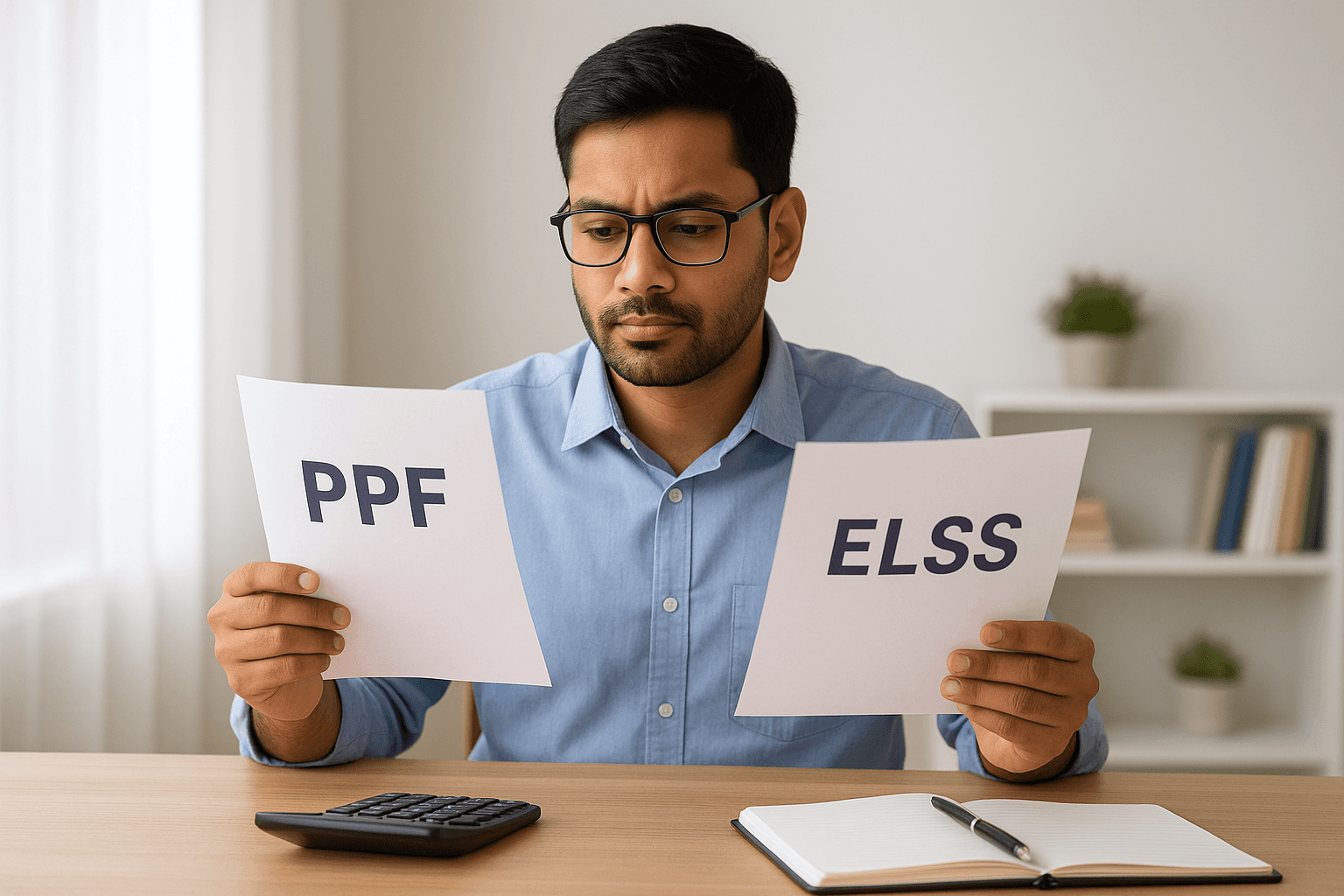

Choosing between PPF and ELSS for Section 80C

Both PPF and ELSS qualify for deductions under Section 80C, but they serve very different risk and liquidity profiles. PPF locks your money for 15 years with a government-backed return, currently around 7.1%, which is predictable but unlikely to significantly outpace inflation over a long period. ELSS funds carry equity market risk but have historically delivered much higher returns over a 10-plus year window, with a shorter three-year lock-in period.

A 30-year-old with a 25-year retirement horizon almost always benefits more from ELSS, while someone within five years of a major expense would lean toward PPF for its capital safety.

The right choice depends on your time horizon, your existing debt exposure, and your marginal tax bracket, not on which option a colleague prefers.

Managing a salary increment with structured allocation

When your salary increases, the additional surplus represents an active investment decision, even if you do nothing with it. Many salaried professionals leave salary increments sitting in a savings account for months, which means inflation quietly reduces its real value. A structured approach means increasing your SIP amount proportionally with each increment, so your investment contributions scale alongside your income without requiring you to revisit your entire portfolio.

Increase SIP contributions by at least 10% annually to match income growth

Redirect any performance bonuses toward goal-specific lump sum investments rather than lifestyle spending

Revisit your asset allocation after each significant income change to confirm it still reflects your risk profile

Key takeaways

What is investment decision making at its core: a structured process of evaluating your options, assessing risk, and allocating money toward goals that actually matter to you. The steps covered in this guide, from goal mapping and risk profiling to tax-efficient allocation and annual reviews, form a repeatable system that keeps your portfolio purposeful rather than reactive.

Every factor shapes the quality of your decisions: your income stability, time horizon, tax bracket, and broader market conditions all determine which instruments belong in your portfolio and in what proportion. Skipping any part of the framework creates gaps that quietly compound into missed returns or unintended risk over time.

The difference between an investor who builds wealth steadily and one who doesn't usually comes down to process discipline, not market timing or stock-picking ability. If you want to put this framework into practice with AI-powered, conflict-free advice, start your investment journey with Invsify today.