What Is Personal Finance? Basics, Pillars, Tips & Examples

Shlok Sobti

What Is Personal Finance? Basics, Pillars, Tips & Examples

What is personal finance? It's the process of managing your money to meet your needs today and reach your goals tomorrow. Think of it as everything you do with the rupees you earn—from splitting your salary between rent and savings, to choosing investments, clearing loans, or buying insurance. Personal finance isn't just for the wealthy or financial experts. It's for anyone who earns, spends, saves, or borrows money. Whether you're drawing ₹30,000 a month or ₹3 lakhs, these decisions shape your financial future.

This guide breaks down personal finance from the ground up. You'll learn why it matters for Indian professionals, how to take your first steps, and what the core pillars are. We'll cover practical topics like budgeting your monthly expenses, investing in instruments that work for Indian goals, managing credit scores and EMIs, and protecting yourself with the right insurance. By the end, you'll have real examples and simple plans you can use immediately—no jargon, no confusion, just clear action steps.

Why personal finance matters

Understanding what is personal finance gives you control over your money instead of letting money control you. Many Indians earn well but struggle at month-end because they never learned to manage cash flow, track expenses, or plan ahead. Without basic financial literacy, you face higher stress, more debt, and missed opportunities to build wealth. Personal finance equips you with the skills to make rupees work harder, reach milestones faster, and handle emergencies without panic.

Financial security in an uncertain world

Your job, health, and family circumstances can change overnight. Medical emergencies, job loss, or unexpected repairs can drain your savings within weeks if you haven't planned. Personal finance teaches you to build safety nets like emergency funds and insurance policies that cushion these shocks. When you manage money well, you sleep better knowing you can handle whatever life throws at you. This security extends beyond yourself; it protects your parents, spouse, and children from financial strain during tough times.

Financial security isn't about being rich. It's about being prepared when things go wrong.

Building wealth over time

Smart money management turns your salary into long-term wealth. Instead of spending every rupee you earn, personal finance shows you how to invest consistently in mutual funds, stocks, or retirement accounts. These investments grow through compounding, where your returns generate more returns year after year. Starting early makes a massive difference. Someone who invests ₹10,000 monthly from age 25 will build far more wealth than someone starting at 35, even if the second person invests more each month.

Avoiding costly mistakes

Poor financial decisions cost you real money. High-interest credit card debt, unnecessary insurance policies, and missed tax-saving opportunities drain thousands of rupees annually. Personal finance education helps you spot these traps before stepping into them. You learn to compare loan interest rates, negotiate better deals, and use tax-saving instruments under Section 80C. Every mistake you avoid today means more money in your pocket tomorrow.

How to get started with personal finance

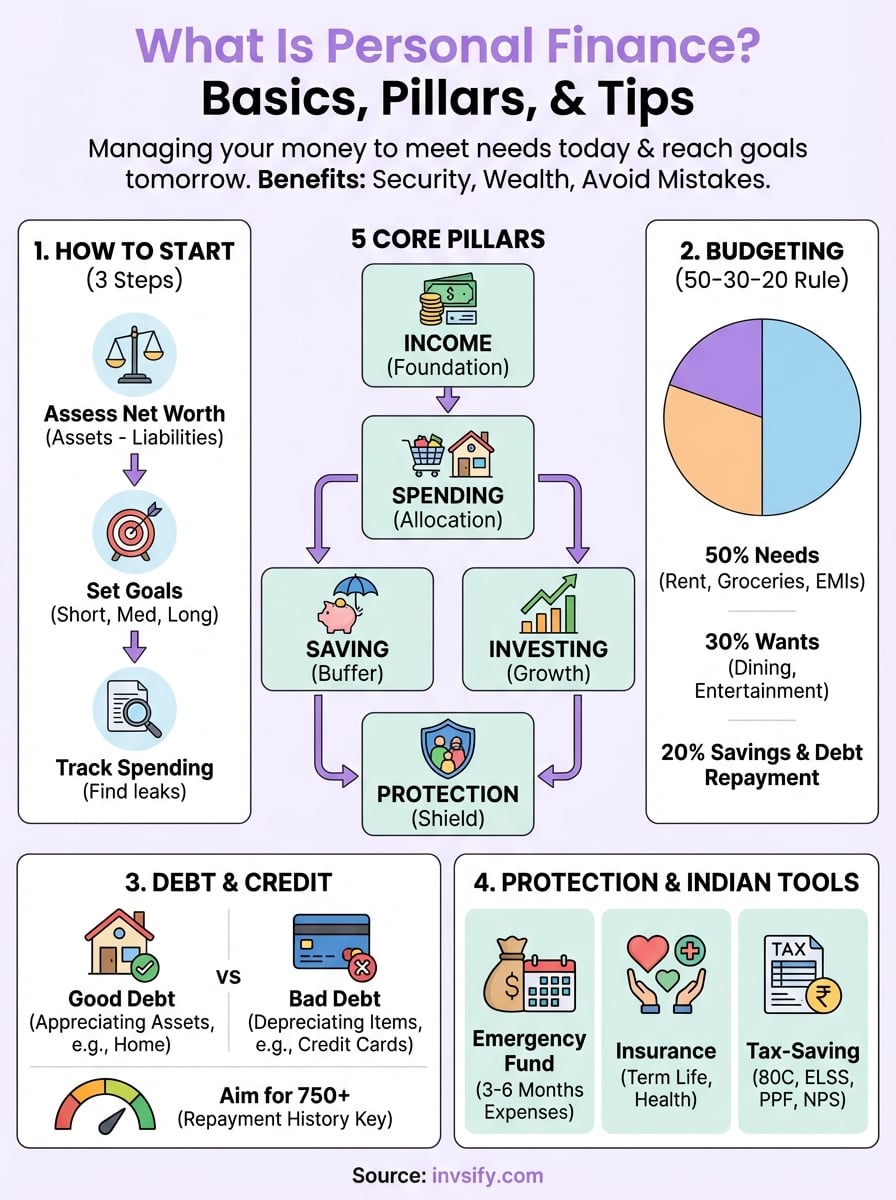

Getting started with what is personal finance feels overwhelming when you face countless decisions about where your money should go. You don't need fancy software or an MBA to begin. Start with three simple steps: understand your current situation, decide what you want to achieve, and track where your rupees actually go. These basics form the foundation every successful money manager builds on. Most Indians skip this groundwork and jump straight to investing or buying insurance, then wonder why their finances stay messy despite earning decent salaries.

Assess where you stand today

Take one hour to list everything you own and everything you owe. Write down your bank balances, fixed deposits, mutual fund investments, PF balance, and physical assets like jewelry or property. Then list your liabilities: credit card debt, personal loans, home loans, and any money borrowed from friends or family. Subtract total liabilities from total assets to get your net worth. This number tells you your exact financial position right now. Many people discover they're worse off than they thought, which becomes the wake-up call they needed to get serious about managing money.

Knowing your net worth is like checking your weight before starting a fitness plan. You can't improve what you don't measure.

Set clear financial goals

Your goals guide every financial decision you make. Split them into short-term needs (within one year) like saving for a wedding or vacation, medium-term targets (one to five years) like buying a car or funding higher education, and long-term objectives (beyond five years) like retirement or children's education. Write down the exact amount and deadline for each goal. Saying "I want to retire comfortably" means nothing. Saying "I need ₹3 crores by age 60 to retire" gives you a concrete target to plan around. Prioritize these goals based on urgency and importance, because you can't chase everything at once.

Track every rupee for one month

Download your bank statements and credit card bills for the past month. Categorize every expense into buckets: rent, groceries, transport, entertainment, dining out, subscriptions, and miscellaneous. Most Indians get shocked when they see how much they spend on food delivery, cab rides, or impulse purchases. This exercise reveals spending leaks you didn't know existed. Apps like Google Pay show transaction history that makes tracking easier. After one month of honest tracking, you'll know exactly where to cut back and where you can comfortably spend more.

Core pillars of personal finance

When you ask what is personal finance, you're really asking how to manage five connected areas that determine your financial health. These five core pillars work together like the foundation of a house: income, spending, saving, investing, and protection. Each pillar supports the others, and weakness in one area undermines your entire financial structure. You can earn a high salary but still struggle if you overspend. You can save diligently but fall behind if you never invest. Understanding how these pillars fit together helps you build a complete financial plan instead of random actions that don't add up to progress.

Income: Your financial foundation

Income forms the starting point for everything else in your money life. Your salary, bonuses, freelance earnings, rental income, or business profits determine how much you can allocate to other areas. Most Indians rely on one primary income source, which creates vulnerability if that source disappears. Smart financial planning means you actively work to increase your income through skill development, side hustles, or passive income streams like dividends from investments. Track your post-tax income accurately because that's the real money available for your use, not your gross salary before deductions.

Spending: Where your money goes

Spending eats up the largest portion of most people's income. Every rupee you spend on rent, groceries, utilities, transport, entertainment, and miscellaneous expenses reduces what's available for saving and investing. You control this pillar more than you think. Discretionary spending on dining out, subscriptions, and impulse purchases can be reduced without major lifestyle changes. Fixed expenses like rent and loan EMIs require longer-term planning to optimize. The key is ensuring your total spending stays below your income, creating a surplus you can direct toward building wealth.

Saving: Building your safety net

Savings represent the buffer between you and financial disaster. This pillar focuses on setting aside money for emergencies, short-term goals, and planned expenses. Your emergency fund should cover three to six months of essential expenses, stored in liquid instruments like savings accounts or liquid mutual funds. Beyond emergencies, you save for specific purchases or events within the next year or two. This money shouldn't be invested in volatile assets because you need guaranteed access when the time comes. Savings give you breathing room to handle life's surprises without derailing your long-term plans.

Investing: Growing wealth over time

Investing transforms your saved money into wealth that compounds over years and decades. Unlike savings that sit idle losing value to inflation, investments in mutual funds, stocks, bonds, PPF, or real estate generate returns that outpace rising prices. The time value of money means starting early matters more than investing large amounts later. Your investment choices depend on your goals, risk tolerance, and time horizon. Short-term goals need safer instruments like debt funds, while retirement decades away can handle equity's volatility for higher returns.

Investing isn't about getting rich quick. It's about getting rich slowly through consistent action.

Protection: Guarding against risks

Protection shields you and your family from financial shocks caused by death, disability, illness, or property loss. Term life insurance ensures your dependents survive financially if you die. Health insurance prevents medical bills from wiping out your savings. Disability insurance replaces lost income if you can't work. This pillar also includes estate planning, nominations, and wills that ensure your wealth transfers smoothly to heirs. Indians often neglect this pillar until crisis strikes, but adequate insurance costs less than you think and delivers peace of mind worth far more than the premiums.

Budgeting and controlling your spending

Budgeting forms the practical foundation of understanding what is personal finance because it connects your income to your goals through deliberate spending choices. A budget isn't about restricting yourself or living miserably. It's a plan that tells your money where to go instead of wondering where it went. Most Indians skip budgeting and rely on mental math, which leads to overspending in some categories while starving others. When you budget properly, you eliminate month-end stress, stop depending on credit cards to bridge gaps, and create consistent surplus for savings and investments.

Choose a budgeting method that fits

Different budgeting methods work for different personalities and circumstances. The 50-30-20 rule splits your post-tax income into 50% for needs (rent, groceries, utilities, EMIs), 30% for wants (dining out, entertainment, shopping), and 20% for savings and debt repayment. This simple framework helps beginners allocate without overthinking every rupee. The zero-based budget assigns every single rupee a job until your income minus expenses equals zero, giving you complete control but requiring more effort to maintain. The envelope system uses physical or digital envelopes for each spending category, and once an envelope empties, you stop spending in that area until next month.

Pick one method and stick with it for at least three months before switching. Consistency matters more than choosing the perfect system. Indian expenses like festival shopping, yearly insurance premiums, and family obligations need separate budget lines that you fund monthly instead of scrambling when these expenses hit.

Track and reduce unnecessary expenses

Your spending reveals patterns you don't notice until you examine the numbers. Review your bank statements and credit card bills monthly to spot subscriptions you forgot about, frequent food delivery charges, or impulse purchases that add up. Small leaks sink ships. Spending ₹200 daily on coffee means ₹6,000 monthly and ₹72,000 yearly that could have gone toward investments generating returns. Cut expenses by negotiating bills (internet, phone plans, insurance premiums), cooking more meals at home, using public transport or carpooling, and implementing a 24-hour rule before non-essential purchases.

Every rupee you don't waste on unnecessary expenses becomes a rupee that builds your wealth.

Focus on high-impact areas first. Reducing your rent by ₹5,000 through relocation saves more than cutting ₹500 from entertainment. Track your top five expense categories and target 10-15% reduction in at least two of them. This exercise doesn't require sacrifice. It requires awareness and intentional choices about what truly matters to you versus what you spend on from habit or social pressure.

Build the habit of living below your means

Living below your means creates the financial margin that separates those who build wealth from those who stay stuck. This habit means your spending stays consistently lower than your income, regardless of salary increases or windfalls. When you get a raise, resist lifestyle inflation. Instead, redirect 50-70% of the increase toward savings and investments while enjoying the rest. Many Indians fall into the trap of upgrading everything (bigger apartment, fancier car, expensive gadgets) whenever income rises, which keeps them living paycheck to paycheck at every salary level.

Practice delayed gratification by waiting three to six months before making major purchases, giving yourself time to evaluate if you truly need the item or just want it temporarily. Automate your savings by setting up standing instructions that transfer money to investment accounts on salary day, making you budget around what remains rather than saving what's left over. Living below your means isn't about deprivation. It's about choosing financial freedom over impressing others with consumption you can't truly afford.

Saving and investing for Indian goals

Understanding what is personal finance means recognizing that saving and investing strategies must align with Indian realities like tax structures, inflation rates, and specific financial products available to residents. Your approach differs fundamentally from Western models because India offers unique instruments like PPF, EPF, NPS, and tax-saving fixed deposits that work within our regulatory framework. The rupee's purchasing power erodes roughly 5-7% annually due to inflation, making it essential to invest rather than just save. Simply parking money in a regular savings account guarantees you'll lose wealth over time as inflation outpaces the 3-4% interest rate banks offer.

Build your emergency fund first

Your emergency fund acts as financial armor against unexpected expenses that would otherwise force you to break long-term investments or pile on debt. This fund should cover three to six months of essential expenses including rent, groceries, utilities, insurance premiums, and loan EMIs. Calculate this amount honestly. If your monthly essentials total ₹40,000, you need ₹1,20,000 to ₹2,40,000 sitting in easily accessible accounts. Park this money in a high-yield savings account earning 6-7% or a liquid mutual fund that allows instant redemption without exit loads.

Keep your emergency fund separate from accounts you use for daily spending. You need psychological barriers that prevent dipping into these reserves for non-emergencies like sale shopping or vacation impulses. Review and replenish this fund whenever you use it, and increase the amount as your lifestyle expenses grow or family responsibilities expand.

Use tax-saving instruments strategically

Section 80C of the Income Tax Act lets you reduce taxable income by up to ₹1.5 lakhs annually through specific investments and expenses. Popular 80C options include Equity Linked Savings Schemes (ELSS mutual funds with three-year lock-in), Public Provident Fund (PPF with 15-year maturity), National Savings Certificate (NSC), tax-saving fixed deposits, life insurance premiums, and home loan principal repayment. ELSS offers the shortest lock-in period among 80C instruments while providing equity market exposure for wealth creation potential that beats inflation significantly.

Tax savings aren't real savings if you choose inferior investments just for deductions. Pick instruments that build wealth while reducing taxes.

Additional deductions exist under Section 80D for health insurance premiums (up to ₹25,000 for self and family, ₹50,000 if you cover senior citizen parents) and Section 80CCD(1B) for extra ₹50,000 NPS contribution beyond the 80C limit. Strategic use of these sections can reduce your tax liability by ₹46,800 to ₹1,00,000 annually depending on your income bracket.

Plan for retirement decades ahead

Your retirement corpus needs to replace 70-80% of your final salary for 25-30 years after you stop working. Starting early dramatically reduces the monthly investment burden through compounding. Someone investing ₹10,000 monthly from age 25 to 60 at 12% returns accumulates roughly ₹6.4 crores, while starting at 35 requires ₹25,000 monthly to reach the same target. Employee Provident Fund (EPF) contributions happen automatically for salaried professionals, currently offering around 8.15% interest with favorable tax treatment.

National Pension System (NPS) provides equity exposure within a retirement account, allowing up to 75% allocation to stock markets with lower costs than mutual funds. The Tier-1 NPS account qualifies for tax deductions while building a retirement nest egg you can't withdraw until 60, which forces long-term discipline. Combine EPF, NPS, and equity mutual funds through Systematic Investment Plans (SIPs) to create a diversified retirement portfolio that balances safety and growth across multiple instruments suited to Indian investors.

Managing debt, loans, and credit scores

Debt represents borrowed money you must repay with interest, and managing it properly separates those who use leverage to build wealth from those who drown in financial obligations. Mastering what is personal finance requires understanding when debt helps you and when it hurts you. Your credit score acts as your financial reputation score that determines loan eligibility and interest rates you'll pay. Indians often misunderstand credit, treating all debt as evil or ignoring credit scores until loan rejection forces awareness. Smart debt management means borrowing strategically for assets that appreciate or generate income while avoiding expensive consumer debt that finances depreciating purchases.

Understand good debt versus bad debt

Good debt finances assets that increase your net worth or earning potential over time. Home loans let you buy property that typically appreciates while building equity through EMI principal payments. Education loans fund skills and degrees that boost your lifetime earning capacity. Business loans generate revenue that exceeds interest costs. These debts carry lower interest rates (7-10% for home loans, 10-15% for education loans) and often provide tax benefits under Section 24 for home loan interest or Section 80E for education loan interest.

Bad debt funds consumption and depreciating assets at high interest rates that erode wealth. Credit card debt charges 36-42% annually on unpaid balances, making it the most expensive money you'll ever borrow. Personal loans for vacations, weddings, or gadgets cost 11-18% interest without creating assets or income. Vehicle loans finance cars that lose 15-20% value immediately after purchase. Minimize bad debt aggressively and redirect those EMI amounts toward investments once you clear these obligations.

Build and protect your credit score

Your CIBIL score ranges from 300 to 900, with scores above 750 qualifying you for best interest rates and quick loan approvals. This three-digit number reflects your repayment history, credit utilization, credit mix, and credit age. Banks report your payment behavior monthly to credit bureaus, building your score over time through consistent on-time payments across all credit cards, loans, and EMIs. One missed payment drops your score significantly and stays on your report for three years.

Check your credit report annually through CIBIL, Experian, or Equifax to spot errors or fraudulent accounts that damage your score. Keep credit card utilization below 30% of your total limit. Avoid applying for multiple loans simultaneously because each application triggers a hard inquiry that temporarily reduces your score. Build credit history early by using credit cards responsibly, even if you don't need loans today, because future loan approvals depend on demonstrated repayment track record.

Your credit score is your financial passport. Guard it carefully because rebuilding takes years while destroying takes minutes.

Create a debt repayment strategy

List all your debts with outstanding balances, interest rates, and monthly EMIs to see your complete obligation. The avalanche method prioritizes paying extra toward the highest interest debt first while making minimum payments on others, mathematically saving the most money on interest. The snowball method attacks the smallest debt first for psychological wins that build momentum, though it costs slightly more in total interest. Pick the approach that matches your personality because consistency matters more than perfection in debt elimination strategies.

Protecting yourself with insurance and planning

Protection completes your understanding of what is personal finance by ensuring that wealth you build doesn't disappear when life throws emergencies at you. Insurance and planning act as defensive shields that protect your family's financial stability against death, disability, critical illness, or property damage. Indians typically under-insure themselves, either skipping coverage entirely or buying inadequate policies pushed by commission-hungry agents. You need enough protection to cover actual risks without paying for unnecessary add-ons that drain your budget without delivering proportional value.

Essential insurance for Indian professionals

Term life insurance provides your dependents with a lump sum if you die during the policy period, ensuring they maintain their lifestyle without your income. Calculate coverage as 10-15 times your annual income or enough to replace lost earnings until dependents become self-sufficient. A healthy 30-year-old non-smoker can secure ₹1 crore coverage for roughly ₹12,000-15,000 annually through online term plans, making it absurdly affordable compared to traditional endowment or money-back policies that mix insurance with poor-performing investments.

Health insurance protects your savings from catastrophic medical expenses that Indian hospital bills generate during serious illness or accidents. Your employer coverage typically stops when you leave the job or retire, so buy personal health insurance with ₹10-15 lakh coverage that stays with you throughout life. Start young when premiums cost less and pre-existing conditions haven't developed. Consider super top-up policies that provide additional coverage beyond base policy limits at lower cost than increasing your primary policy amount.

Insurance isn't about betting on bad things happening. It's about ensuring bad things don't destroy your family's financial future.

Disability insurance replaces lost income if accident or illness prevents you from working, though this coverage remains rare in India with limited standalone options. Critical illness riders or policies pay lump sums upon diagnosis of specified serious conditions like cancer, heart attack, or stroke, giving you financial breathing room during treatment and recovery when you can't earn regular income.

Estate planning and nominations

Estate planning ensures your wealth transfers smoothly to intended beneficiaries instead of getting stuck in legal battles or going to unintended recipients through default succession rules. Write a legally valid will specifying exactly who inherits which assets, appointing an executor to distribute your estate, and naming guardians for minor children. Update your will whenever major life changes occur like marriage, divorce, or children's birth.

Add nominations across all financial accounts including bank deposits, mutual funds, insurance policies, PF, and demat accounts so designated nominees receive assets without requiring succession certificates that take months to obtain. Remember that nominees act as custodians who must distribute assets per your will, not as automatic owners. Store original documents securely with family members knowing their location and grant trusted individuals power of attorney for financial decisions if you become incapacitated.

Real life examples and simple starter plans

Applying what is personal finance becomes clearer when you see how real people with different situations handle their money. These examples show you practical starting points based on typical Indian salaries and circumstances, giving you templates to adapt for your own situation rather than starting from scratch.

Starter plan for ₹50,000 monthly salary

Rajesh earns ₹50,000 monthly after tax and lives in a tier-2 city with moderate expenses. He allocates ₹25,000 (50%) to needs including ₹12,000 rent, ₹8,000 groceries, and ₹5,000 for utilities and transport. His wants consume ₹15,000 (30%) covering dining out, entertainment, and personal shopping. The remaining ₹10,000 (20%) splits between ₹5,000 monthly SIP in a diversified equity mutual fund for long-term growth and ₹5,000 building his emergency fund in a liquid fund until he reaches ₹1.5 lakhs.

He maintains one credit card with ₹1 lakh limit, keeps utilization under 30%, and pays the full statement balance every month to avoid interest charges while building his credit score. Rajesh bought ₹50 lakh term insurance for ₹10,000 annually and health insurance with ₹5 lakh coverage through his employer.

Starting small beats waiting until circumstances feel perfect. Consistency compounds faster than perfection.

Plan for ₹1 lakh monthly salary

Priya brings home ₹1 lakh monthly after tax in a metro city. Her needs take ₹50,000 including ₹25,000 rent, ₹15,000 for groceries and household expenses, and ₹10,000 for transport and utilities. Wants account for ₹30,000 on dining, subscriptions, travel, and shopping. She directs ₹20,000 toward wealth building through ₹10,000 equity SIP, ₹5,000 PPF contribution, and ₹5,000 toward clearing her personal loan faster.

Priya maintains ₹3 lakhs emergency fund in a combination of savings account and liquid mutual fund. She carries ₹1 crore term insurance and ₹10 lakh health insurance with ₹10 lakh super top-up for additional coverage at minimal cost.

Key takeaways

Understanding what is personal finance gives you control over every rupee you earn and spend. The five pillars (income, spending, saving, investing, and protection) work together to build your financial foundation. Start with the basics: track expenses for one month, build an emergency fund covering three to six months, and create a budget using the 50-30-20 rule. Invest consistently through SIPs rather than timing the market, clear high-interest debt aggressively, and protect your family with adequate insurance.

Your financial journey needs consistent action, not perfect knowledge. Small steps taken today compound into significant wealth over decades. AI-powered tools help you make smarter decisions without commission-driven bias. Get conflict-free, AI-driven financial advice that optimizes your wealth through transparent, SEBI-registered guidance.