SIP In Mutual Funds: What It Is, How It Works, How To Start

Shlok Sobti

SIP In Mutual Funds: What It Is, How It Works, How To Start

A Systematic Investment Plan (SIP) in mutual funds is a method that lets you invest a fixed amount of money at regular intervals (like monthly) into a mutual fund scheme. Think of it as a recurring deposit for investments. Instead of putting a large sum at once, you invest small amounts consistently. This approach removes the pressure of timing the market and helps you build wealth gradually through disciplined investing.

This guide breaks down everything you need to know about SIPs. You'll learn why they matter for your financial goals, how to start your first SIP, what happens to your money over time, and which type suits your needs. We'll also cover common mistakes that cost investors money and how to avoid them. By the end, you'll have a clear roadmap to begin your SIP journey with confidence.

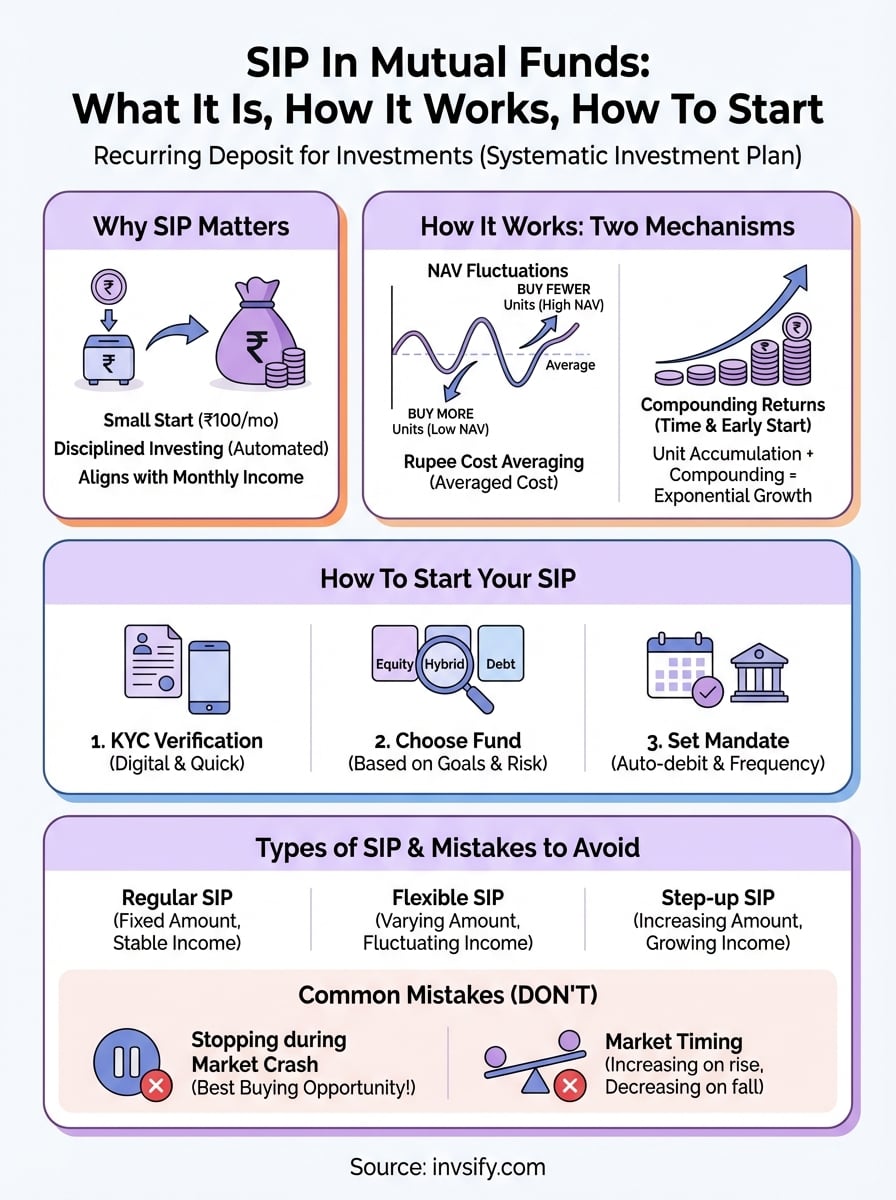

Why SIP in mutual funds matters for you

Understanding what is SIP in mutual funds becomes crucial when you realize that investing doesn't require a large lump sum upfront. You can start with as little as ₹100 per month and gradually build your portfolio. This makes SIPs particularly valuable for salaried professionals who receive monthly income and want to invest consistently without disrupting their cash flow. Traditional investment methods often demand significant capital, which keeps many people on the sidelines.

SIPs align with your monthly income

Your salary arrives every month, and so should your investments. SIPs automate the entire process by deducting a fixed amount from your bank account on a chosen date. You don't need to remember to invest or decide when markets look favorable. This systematic approach eliminates procrastination and ensures you invest before spending on non-essential items. The automation also removes emotional decision-making from your investment journey.

When you automate your investments, you pay yourself first before other expenses.

Market timing becomes irrelevant

Rupee cost averaging works in your favor with SIPs. When markets fall, your fixed investment amount buys more mutual fund units. When markets rise, you buy fewer units. Over time, this averages out your purchase cost and reduces the impact of market volatility on your portfolio. You don't need to predict market movements or wait for the "perfect" entry point.

How to start a SIP in mutual funds

Starting a SIP takes less than 15 minutes once you have the right information ready. You need three main components: completed KYC verification, a chosen mutual fund scheme, and a bank account with sufficient balance. The process has become entirely digital, which means you can begin investing from your phone without visiting any office or filling physical forms. Most platforms guide you through each step with clear instructions.

Complete your KYC verification

Your investment journey begins with Know Your Customer (KYC) compliance, which is a one-time process mandated by SEBI. You need to submit your PAN card, Aadhaar card, bank account details, and a recent photograph. Most investment platforms offer in-person verification (IPV) through video calls that take approximately 10 minutes. Once verified, your KYC status becomes valid across all mutual fund houses and investment platforms in India.

The verification process also includes risk profiling, where you answer questions about your financial goals, income stability, and investment timeline. This assessment helps you understand your risk tolerance and guides you toward suitable mutual fund categories.

Choose your mutual fund scheme

You face thousands of mutual fund schemes, but your selection depends on your financial goal and investment horizon. For long-term wealth creation (10+ years), equity mutual funds typically offer higher growth potential. For medium-term goals (3-5 years), hybrid or balanced funds provide stability with moderate growth. Short-term goals (1-3 years) work better with debt funds that focus on capital preservation.

Research the fund's historical performance, expense ratio, and fund manager track record before committing. When you understand what is SIP in mutual funds, you realize that consistent investing matters more than finding the "perfect" fund. A good large-cap or flexi-cap fund serves as an excellent starting point for beginners.

Set up the SIP mandate

After selecting your fund, you specify three critical details: investment amount, frequency (monthly/quarterly), and start date. Link your bank account through net banking authorization, which creates an auto-debit mandate. Your chosen amount gets deducted automatically on the specified date each month and invested in your selected mutual fund scheme.

Auto-debit ensures you never miss an investment cycle due to forgetfulness or procrastination.

Most platforms let you start with ₹500 per month, though some funds allow even lower amounts. You can always increase the SIP amount later as your income grows.

How SIP in mutual funds works over time

Your SIP investment grows through two powerful mechanisms: unit accumulation and compounding returns. Each month, your fixed investment amount purchases mutual fund units at the prevailing Net Asset Value (NAV). The NAV changes daily based on market performance, which means you buy more units when prices drop and fewer units when prices rise. This automatic buying pattern protects you from making emotional decisions during market fluctuations and builds your investment gradually regardless of market conditions.

Unit accumulation and NAV dynamics

When you understand what is SIP in mutual funds from a time perspective, you realize that your unit count grows continuously. Suppose you invest ₹5,000 monthly in a mutual fund. In January, the NAV is ₹50, so you receive 100 units. In February, the market corrects and NAV drops to ₹40, giving you 125 units for the same ₹5,000. In March, when NAV recovers to ₹55, you get approximately 91 units. Over three months, you own 316 units with an average cost of ₹47.47 per unit, which is lower than two of the three NAVs you encountered.

Your total investment value fluctuates based on the current NAV, but your unit count only increases with each SIP installment. This distinction matters because temporary market declines become buying opportunities rather than losses.

Compounding amplifies your returns

The real magic happens when your accumulated units generate returns, and those returns generate further returns. Compounding works exponentially, not linearly. A monthly SIP of ₹5,000 for 20 years at 12% annual return grows to approximately ₹50 lakhs. Your total investment is only ₹12 lakhs, but the remaining ₹38 lakhs comes purely from compounding.

The first few years show modest growth, but the final years of your SIP journey deliver exponential wealth creation.

Starting early matters more than investing large amounts. A 25-year-old investing ₹3,000 monthly until age 60 accumulates more wealth than a 35-year-old investing ₹6,000 monthly until age 60, assuming similar returns. Those 10 additional years of compounding make the critical difference in your final corpus.

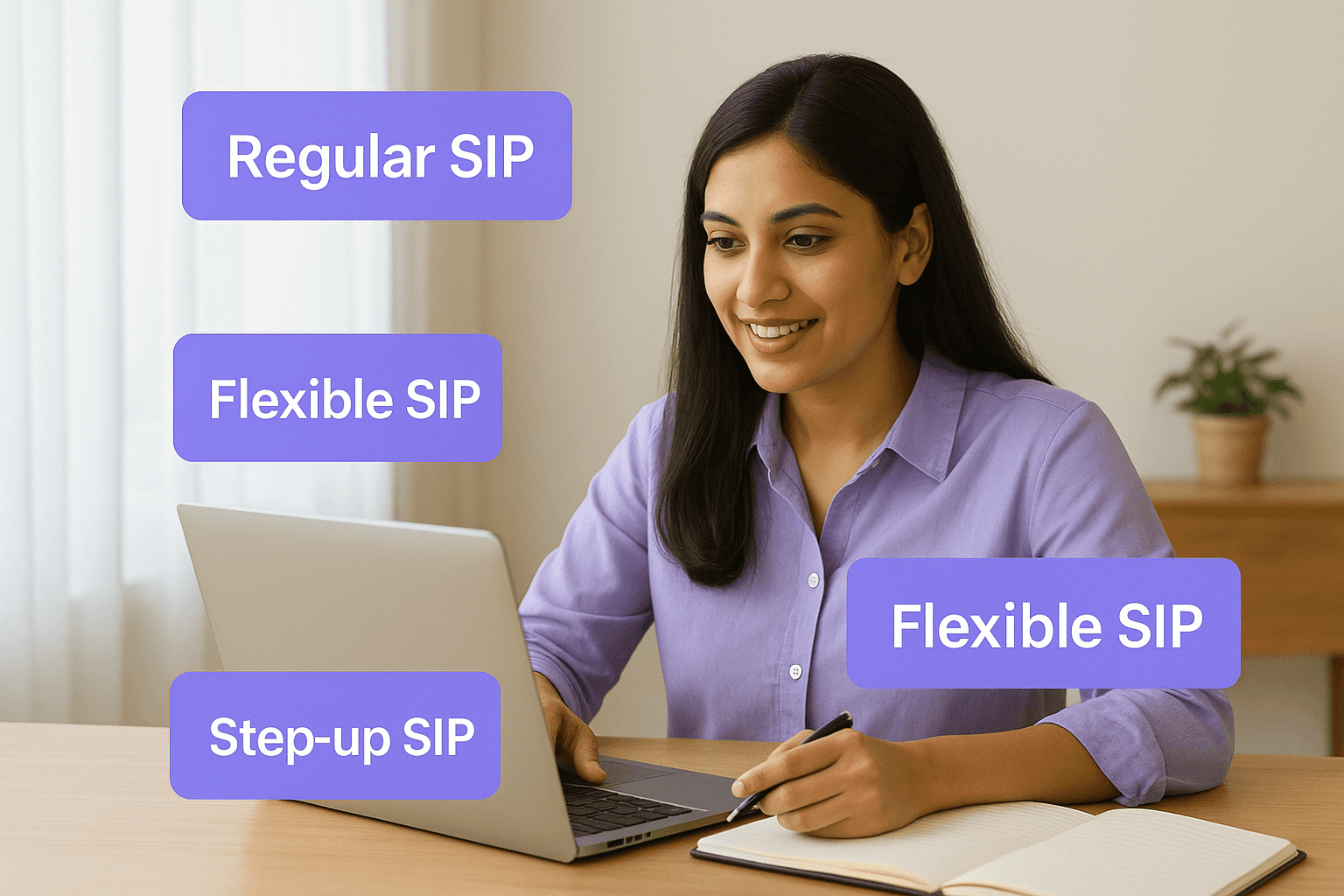

Types of SIP and which one to choose

Understanding what is SIP in mutual funds extends to knowing that different SIP structures serve different financial situations. Your choice depends on your income pattern, financial goals, and ability to increase contributions over time. Most investors start with regular SIPs, but alternative structures offer flexibility as your career progresses and income grows.

Regular SIP with fixed amounts

A regular SIP involves investing the same amount every month until your chosen end date. You decide upfront whether to invest for 5 years, 10 years, or any specific period. This structure works perfectly if you earn a stable monthly salary and want predictable investment planning. Your bank account gets debited automatically on the same date each month, and you receive the same number of units when NAV remains constant.

Flexible SIP for varying cash flow

Flexible SIPs let you adjust the investment amount each month based on your available funds. Freelancers, business owners, and commission-based professionals benefit most from this option because their income fluctuates. You set a minimum amount (like ₹1,000) but can increase it to ₹3,000 or ₹5,000 in months when you earn more. The flexibility prevents you from stopping your SIP during lean periods.

Step-up SIP for growing income

Step-up SIPs automatically increase your investment amount by a fixed percentage annually. If you start with ₹5,000 monthly and choose a 10% annual step-up, your SIP becomes ₹5,500 after one year and ₹6,050 after two years. This structure aligns with typical salary increments and helps you invest more as your income grows without manual intervention.

Increasing your SIP amount by even 5-10% annually significantly accelerates your wealth creation timeline.

Tips, risks and common SIP mistakes to avoid

Knowing what is SIP in mutual funds includes understanding where most investors go wrong and how to protect your portfolio from unnecessary losses. The mistakes you avoid matter as much as the strategies you follow. Your discipline during market downturns determines whether your SIP delivers the compounding magic or becomes another abandoned investment. Most SIP failures happen due to behavioral errors rather than poor fund selection or market performance.

Don't stop your SIP during market crashes

Stopping your SIP when markets fall represents the costliest mistake you can make. Your instinct tells you to pause investments when NAVs drop, but this is exactly when you accumulate the most units at discounted prices. Markets recovered from every historical crash, and investors who continued their SIPs during downturns earned the highest returns. Set up automatic debits and avoid checking your portfolio daily during volatile periods.

Market corrections create buying opportunities that boost your long-term returns significantly.

Avoid timing the market with SIP amounts

Some investors increase their SIP amount when markets rise and decrease it during falls, which defeats the entire purpose of rupee cost averaging. Your SIP amount should follow your income growth, not market movements. Stick to your predetermined investment plan regardless of whether the Sensex hits new highs or corrects sharply. Market timing works against SIP investors because you end up buying more expensive units and fewer cheap ones.

Review your portfolio but don't overtrade

Checking your SIP performance quarterly or half-yearly keeps you informed without triggering impulsive decisions. Avoid switching between funds every time you see better performers because past returns don't guarantee future performance. Give your selected funds at least three years before evaluating whether they meet your goals. Exit costs, taxation, and timing risks make frequent switches expensive. Focus on your asset allocation rather than chasing the highest returns across categories.

Key takeaways

Understanding what is sip in mutual funds gives you a powerful tool for disciplined wealth creation without requiring large capital upfront. You can start with ₹100 per month and benefit from rupee cost averaging, which automatically buys more units during market falls and fewer during rises. The combination of unit accumulation and compounding delivers exponential growth over long periods, especially when you start early and stay invested through market cycles. Your success depends more on consistency than timing, which is why automated monthly investments work better than trying to predict market movements.

Sign up with Invsify to access AI-powered investment recommendations that help you select the right mutual funds based on your financial goals and risk profile. The platform eliminates hidden distributor fees while providing 24/7 multilingual support, portfolio tracking, and personalized weekly insights. Starting your SIP journey today positions you to build substantial wealth through disciplined investing over the coming years.