What Is Tax Planning in India? Types, Objectives & Examples

Shlok Sobti

What Is Tax Planning in India? Types, Objectives & Examples

Every rupee you earn gets taxed, but not every rupee has to be. Understanding what is tax planning in India starts with a simple fact: the Income Tax Act offers dozens of legal provisions that let you reduce your tax liability while building wealth at the same time. Most salaried individuals either overlook these provisions entirely or scramble to use them during the last week of March.

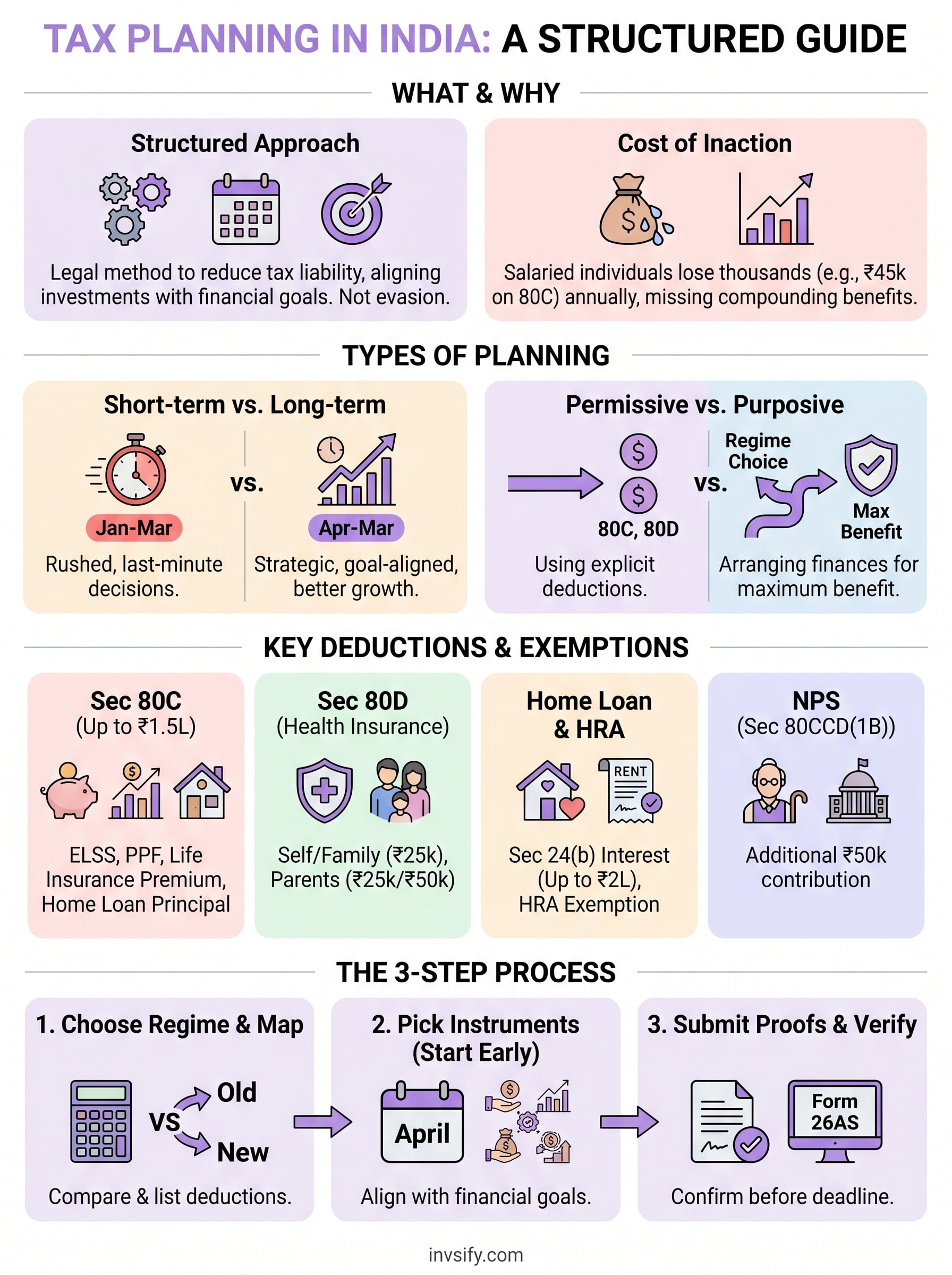

Tax planning isn't about evasion or shady workarounds. It's a structured approach to arranging your finances so you pay only what you legally owe, nothing more. When done right, it aligns your investments, expenses, and income streams with the deductions and exemptions already available under sections like 80C, 80D, HRA, and others. The result? More money stays in your pocket and works harder for your goals.

At Invsify, our AI-powered advisory platform helps salaried individuals across India make these decisions with clarity, no guesswork, no last-minute panic. As a SEBI Registered Investment Advisor, we combine data-backed recommendations with transparent, conflict-free advice so your tax-saving investments actually fit your financial plan.

This guide breaks down the definition, objectives, types, and real examples of tax planning in India. Whether you're a first-time taxpayer or someone looking to optimize an existing strategy, you'll walk away with a clear framework to approach tax season with confidence.

Why tax planning matters in India

India's income tax system places a significant burden on salaried employees, who have taxes deducted at source before they even receive their pay. Unlike business owners who can structure income across multiple heads, salaried individuals work with a fixed salary that leaves little room to maneuver unless they plan deliberately. That's exactly why understanding what is tax planning in India is not optional for anyone earning above the basic exemption limit. It's the difference between handing over a large chunk of your income and keeping it working toward your goals.

The direct cost of skipping tax planning

Most salaried professionals in India lose thousands of rupees every year simply by not using the deductions already available to them under the Income Tax Act. Section 80C alone allows a deduction of up to ₹1.5 lakh annually, which at the 30% tax bracket translates to a saving of ₹45,000 in a single financial year. That's money you could redirect into an emergency fund, a child's education, or your retirement corpus. When you skip tax planning, you're not just paying more tax today. You're also losing the compounding benefit of that extra capital over decades.

Unused tax deductions don't carry forward to the next financial year. Every year you skip planning is a permanent, unrecoverable loss of savings.

Beyond Section 80C, provisions like Section 80D for health insurance premiums, HRA exemption, LTA, and the standard deduction of ₹75,000 under the old tax regime are frequently left on the table. Many salaried individuals simply don't know these provisions exist, or they submit their investment declarations too late for their employer to account for them. The result is an inflated monthly TDS deduction and a refund chase that ties up your money for months.

How tax planning connects to your financial goals

Tax planning works best when it's treated as part of your overall financial plan, not as a standalone exercise you complete in a panic during January or February. The investments you make for tax benefits under Section 80C include options like PPF, ELSS mutual funds, and life insurance premiums, all of which serve long-term wealth goals well beyond just cutting your tax bill. When your tax-saving instruments align with your broader objectives, you get two benefits from a single financial decision.

The Indian government has also introduced the new tax regime as an alternative to the old regime with its deductions and exemptions, which adds another layer of decision-making for salaried taxpayers. Choosing the wrong regime for your income level and investment profile can mean paying more tax than you legally owe. For a person with a significant home loan, health insurance, and 80C investments, the old regime often wins. For someone with minimal deductions, the new regime might make more sense. This is not a decision to make based on a colleague's advice or a social media post. It requires a clear look at your actual numbers, which is where structured tax planning gives you a genuine financial advantage year after year.

Types of tax planning in India

Not every approach to tax planning looks the same. Depending on when you act and how you use the law's provisions, your strategy can fall into different categories. Understanding what is tax planning in India across these types helps you pick an approach that fits your financial situation and timeline rather than following a one-size-fits-all method.

Short-term vs. long-term tax planning

Short-term tax planning refers to the decisions you make toward the end of a financial year, typically between January and March, to reduce your taxable income before the year closes. This might involve a last-minute PPF contribution or paying your health insurance premium before March 31. While short-term planning beats doing nothing, it often leads to rushed choices that don't align with your broader financial goals.

Long-term tax planning runs through the entire year. You choose instruments like ELSS funds or NPS contributions at the start of the year and let those decisions compound over time. This approach gives you more control over cash flow, avoids year-end pressure, and usually produces better financial outcomes overall.

Long-term tax planning is not just about saving tax today. It's about building wealth systematically while keeping your annual tax liability low.

Permissive and purposive tax planning

Permissive tax planning means you use the specific deductions, exemptions, and reliefs that the Income Tax Act explicitly provides. Claiming deductions under Section 80C, 80D, or HRA falls into this category. The government designed these provisions to encourage behaviors like saving for retirement, buying health insurance, or purchasing a home, and you are simply using what the law already makes available to you.

Purposive tax planning takes a more structural view. Here, you arrange your income, investments, and financial decisions in a way that achieves the maximum tax benefit without crossing into evasion or avoidance. Choosing between the old and new tax regimes based on your actual deduction profile is a purposive decision. Both types are legal, both are legitimate, and used together they form a complete tax strategy that serves your financial interests across every year.

Key deductions and exemptions used for tax planning

Understanding what is tax planning in India means knowing which specific provisions you can actually use. The Income Tax Act contains over a dozen sections that allow you to legally reduce your taxable income, but in practice, a handful of deductions and exemptions do most of the heavy lifting for salaried individuals. Knowing these sections before the financial year begins gives you time to choose the right instruments deliberately, rather than grabbing whatever your bank promotes in the last week of March.

The deductions you claim must be backed by actual investments or verifiable expenses. Claiming them without documentation during an income tax assessment can result in disallowance and penalties.

Section 80C: Your largest single deduction

Section 80C offers a deduction of up to ₹1.5 lakh per financial year on a wide range of investments and expenses. This is the most commonly used provision and covers ELSS mutual funds, PPF contributions, 5-year tax-saving fixed deposits, life insurance premiums, and ULIP premiums. Your home loan principal repayment and children's tuition fees also qualify under this section. The key is selecting 80C instruments that match your risk tolerance and liquidity needs, not just whichever product your bank pushes hardest.

Investment | Lock-in Period | Risk Level |

|---|---|---|

ELSS Mutual Funds | 3 years | Market-linked |

PPF | 15 years | Low |

5-Year Tax-Saving FD | 5 years | Low |

Life Insurance Premium | Policy term | Low |

Health insurance, HRA, and home loan interest

Section 80D lets you claim a deduction of up to ₹25,000 per year on health insurance premiums for yourself and your immediate family. You get an additional ₹25,000 for your parents' coverage, or ₹50,000 if your parents are senior citizens. This single deduction rewards a decision, buying health cover, that protects your finances on two fronts simultaneously.

If your employer includes HRA in your salary structure, you can claim an HRA exemption based on actual rent paid, your basic salary, and your city of residence. Section 24(b) adds another layer by allowing a deduction of up to ₹2 lakh per year on home loan interest, which carries significant value during the early years of a large housing loan when interest payments are at their highest.

How to do tax planning step by step

Knowing what is tax planning in India is one thing; putting it into practice is another. Most salaried individuals delay the process until the last quarter, which limits their options and often leads to rushed investment decisions driven by urgency rather than strategy. A structured, year-round approach fixes that entirely.

Start your tax planning in April, not January. The earlier you act, the more time your tax-saving investments have to grow and the less pressure you face at year-end.

Step 1: Choose your regime and map your deductions

Your first decision is choosing between the old tax regime and the new tax regime. Calculate your gross income, list every deduction you can realistically claim, and compare your net taxable income under both options. The Income Tax Department's official e-filing portal provides a calculator to help you run this comparison before you commit.

Once you've selected your regime, map out every deduction category available to you:

Section 80C: Up to ₹1.5 lakh on ELSS, PPF, life insurance premiums, and home loan principal repayment

Section 80D: Up to ₹25,000 on health insurance for yourself and your family, with higher limits for parents or senior citizens

Section 24(b): Up to ₹2 lakh on home loan interest payments

Section 80CCD(1B): An additional ₹50,000 on NPS contributions, separate from the 80C limit

Step 2: Pick instruments that match your goals

Not every tax-saving instrument serves the same financial purpose. ELSS funds work well if you want equity exposure and can handle short-term market movements. PPF suits a conservative, long-term savings objective. NPS builds your retirement corpus while unlocking the additional ₹50,000 deduction under Section 80CCD(1B). Match each instrument to a specific financial goal so your tax plan and your broader financial plan move in the same direction.

Starting investments in April or May rather than waiting until December spreads your outflows evenly, reduces cash flow pressure toward year-end, and gives your market-linked investments more time to navigate volatility before the financial year closes.

Step 3: Submit proofs and verify your Form 26AS

Your employer collects investment declaration proofs between December and February to finalize your TDS calculation. Missing this window forces them to deduct tax at a higher rate, and you then need to claim a refund through your ITR filing, which delays access to your own money for months. After filing, cross-check your Form 26AS and Annual Information Statement to confirm every declared deduction is correctly reflected before the assessment year ends.

Examples and mistakes to avoid

Understanding what is tax planning in India becomes easier when you see it through real scenarios. A salaried professional earning ₹12 lakh annually under the old tax regime can reduce their taxable income significantly by combining Section 80C investments (₹1.5 lakh), health insurance under 80D (₹25,000), and an NPS contribution under 80CCD(1B) (₹50,000). That's ₹2.25 lakh in deductions before accounting for HRA or home loan interest, which can push someone from the 30% bracket down to the 20% bracket entirely.

A practical scenario

Consider Priya, a 32-year-old software engineer in Bengaluru earning ₹14 lakh per year. She pays ₹18,000 monthly in rent, carries a health insurance policy, and contributes to NPS through her employer. By claiming HRA exemption, 80D deduction, and the additional NPS deduction under 80CCD(1B), she reduces her net taxable income by over ₹3 lakh compared to a colleague in the same bracket who claims nothing. The old regime works in her favor because her total deductions exceed the flat benefit available under the new regime.

Her situation also illustrates one important point: the choice between regimes is not permanent. You can switch between the old and new tax regime every year as a salaried taxpayer, which means you should run the comparison fresh at the start of each financial year rather than assuming last year's decision still applies.

Common mistakes that cost you money

The most frequent mistake salaried individuals make is treating Section 80C as the only tax-saving tool available to them. They fill it up with a life insurance policy or a tax-saving FD and assume the job is done. In reality, Section 80D, 80CCD(1B), and HRA can add substantial deductions that never get claimed simply because no one pointed them in that direction.

Choosing investments purely for tax benefits without considering lock-in periods, returns, and your actual financial goals is not tax planning. It's just guessing.

Another mistake is waiting until January or February to start, which forces you into whichever instrument is easiest to buy quickly rather than the one that fits your plan. You also forfeit months of potential compounding on market-linked instruments like ELSS. Acting in April gives you twelve months of disciplined, goal-aligned investing instead of a rushed transaction that ticks a compliance box but adds little real value to your portfolio.

Bring it all together

Understanding what is tax planning in India comes down to one core idea: the law already gives you the tools to reduce your tax bill, and the only question is whether you use them deliberately or ignore them by default. Section 80C, 80D, NPS contributions, HRA exemptions, and home loan interest deductions can together save you lakhs every year, but only if you start early, choose the right regime, and match your tax-saving instruments to actual financial goals.

Tax planning is not a one-week exercise you run in March. It's a year-round discipline that compounds in your favor every time you make a well-informed decision. The salaried professionals who get this right don't just pay less tax; they build real, lasting wealth in the process. If you want structured, conflict-free guidance on putting this into practice, start your tax planning journey with Invsify today.