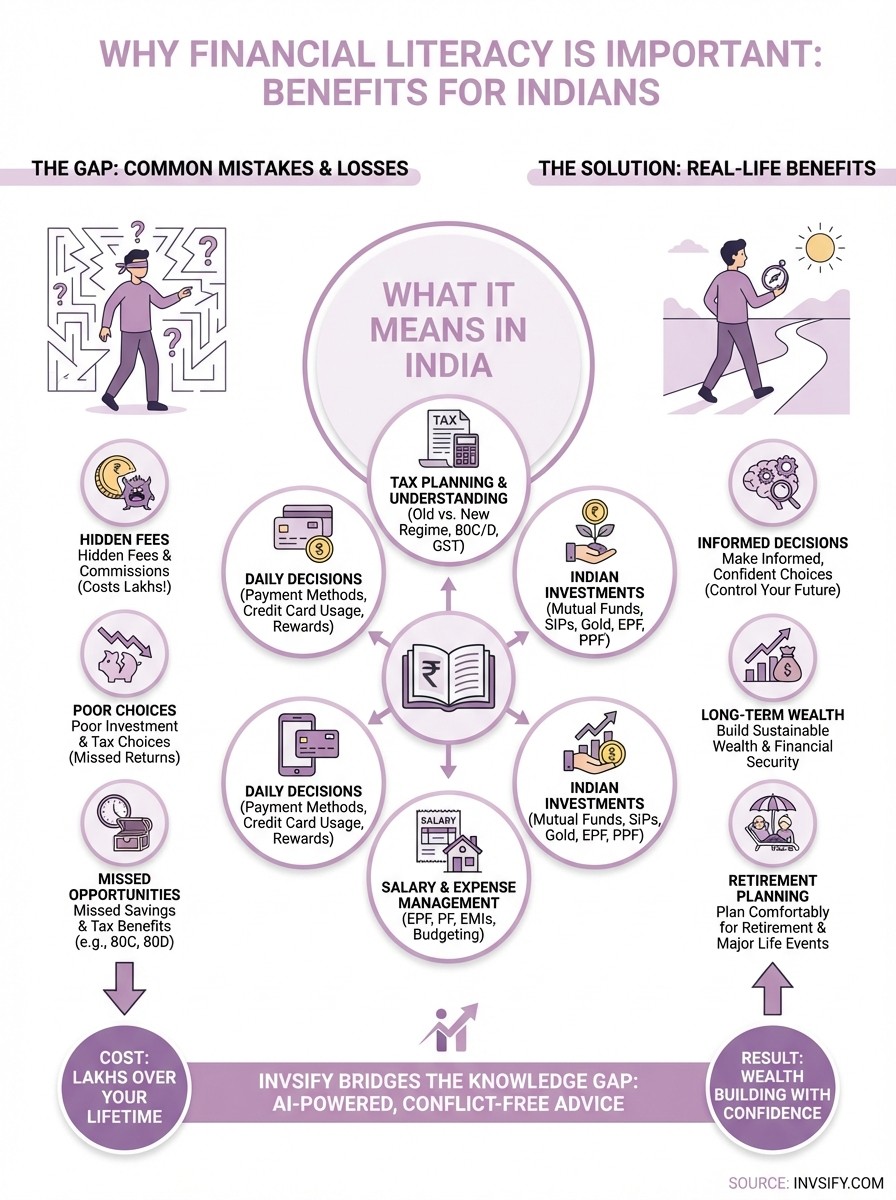

Why Financial Literacy Is Important: Benefits For Indians

Shlok Sobti

Why Financial Literacy Is Important: Benefits For Indians

Most Indians learn about money the hard way, through mistakes, missed opportunities, or advice from well-meaning relatives who may not have the full picture. Schools rarely teach it, and by the time you're earning a salary, you're expected to figure out taxes, investments, and retirement planning on your own. Understanding why financial literacy is important isn't just academic; it directly affects how much wealth you build, how well you protect it, and whether you'll have financial security when you need it most.

Financial literacy gives you the ability to make informed decisions about your money, from choosing the right mutual funds to understanding the real cost of a loan. Without it, you're essentially navigating a complex system blindfolded, often relying on distributors or online forums that may not have your best interests at heart. The gap between what you know and what you need to know can cost you lakhs over your lifetime in hidden fees, poor investment choices, and missed tax-saving opportunities.

This is exactly why Invsify exists, to bridge that knowledge gap with AI-powered, conflict-free financial advice that puts your interests first. In this article, we'll break down the specific benefits of financial literacy for Indians, covering everything from daily money management to long-term wealth creation, so you can take control of your financial future with confidence.

What financial literacy means in India

Financial literacy in India means understanding how to manage your money effectively within the specific context of the Indian financial system. This includes knowing how to save, invest, borrow, and plan for your future while navigating unique challenges like joint family finances, gold investments, and complex tax structures. Unlike generic definitions, financial literacy for Indians requires you to grasp the interplay between traditional savings methods (like fixed deposits and LIC policies) and modern investment vehicles (like mutual funds and SIPs), all while maximizing tax benefits under sections like 80C and 80D.

You need to understand concepts that directly affect your take-home salary, from EPF contributions to professional tax, and how these fit into your overall wealth-building strategy. The Reserve Bank of India's regulations, SEBI guidelines for investments, and GST implications on various financial products all form part of what you need to know. This knowledge base extends beyond simple budgeting to include understanding the true cost of EMIs, the impact of inflation on your savings, and how to evaluate insurance products that aren't just disguised investment schemes.

The basic skills that count

Your financial literacy foundation starts with budgeting within an Indian salary structure, where you account for everything from dearness allowance to HRA exemptions. You should be able to calculate your actual tax liability, understand the difference between old and new tax regimes, and know when each makes sense for your situation. Reading your salary slip correctly is just the beginning; you also need to grasp how your PF accumulates, what gratuity means, and how to optimize your CTC structure.

Beyond monthly management, you need to understand investment basics specific to India. This means knowing the difference between equity and debt mutual funds, understanding NAV, recognizing what an exit load is, and being able to evaluate fund performance beyond just returns. You should understand how SIPs work, why rupee cost averaging matters in volatile markets, and how to rebalance your portfolio as your goals change.

Financial literacy isn't about becoming an expert; it's about knowing enough to ask the right questions and spot the wrong advice.

How it differs from Western concepts

Indian financial literacy requires you to navigate unique cultural factors that don't exist in Western markets. Joint family finances mean you're often managing money for multiple generations, with expectations around supporting parents and funding weddings or education for siblings. Gold purchases aren't just jewelry; they're often considered investments, and you need to understand how they fit (or don't fit) into a balanced portfolio compared to sovereign gold bonds or gold ETFs.

Your retirement planning can't simply follow a 401(k) model because NPS, EPF, and PPF operate differently from Western equivalents. The lack of comprehensive social security means you need to plan more aggressively for healthcare costs in retirement, understanding critical illness insurance and senior citizen health policies. Tax-saving investments in India are often intertwined with long-term wealth creation in ways that require you to balance immediate deductions with actual returns, making why financial literacy is important even more critical for Indian investors compared to their Western counterparts.

Why financial literacy matters for Indians

Your financial security depends on decisions you make today, from choosing between tax regimes to selecting the right health insurance for your aging parents. Financial literacy directly determines whether you'll retire comfortably or struggle in your later years, whether you'll pay unnecessary commissions or keep more of your returns, and whether you'll fall for mis-sold products or invest in instruments that actually align with your goals. The Indian financial system operates with complexities that don't exist in many other markets, making why financial literacy is important a question of survival rather than just success.

Every year, millions of Indians lose lakhs to investment schemes that promise unrealistic returns, insurance policies that barely cover inflation, or credit card debt that compounds at 36% annually. Without basic financial knowledge, you're vulnerable to everyone from pushy distributors earning hidden commissions to relatives suggesting "can't miss" opportunities that actually carry substantial risk. Your salary might be growing, but if you don't understand how to optimize taxes, choose the right investment mix, or plan for contingencies, you're essentially working harder to give away more money in fees and lost opportunities.

The cost of financial ignorance

Financial illiteracy costs you real money every single month, from unnecessary bank charges you don't spot to suboptimal investment choices that underperform by 3-4% annually. When you don't understand expense ratios, you might stick with regular mutual fund plans that cost you an extra 1% every year, which compounds to lakhs over a 20-year investment horizon. Credit card interest alone can consume 15-20% of your monthly income if you only pay minimum dues, creating a debt trap that financial literacy would help you avoid entirely.

The difference between understanding and not understanding compound interest can mean the difference between ₹50 lakhs and ₹1 crore at retirement.

What financial literacy includes in real life

Financial literacy shows up in everyday decisions that seem small but compound into significant financial outcomes over time. You use it when you're comparing credit card reward programs, evaluating whether to prepay a home loan, or deciding if that festival sale purchase makes sense on EMI. It's not theoretical knowledge sitting in a textbook; it's the practical skill that helps you navigate salary negotiations, understand your Form 16, and calculate whether switching from the old tax regime to the new one actually saves you money or costs you more.

Real financial literacy means you can read a mutual fund fact sheet and understand what the portfolio turnover ratio means for your taxes, or look at an insurance policy document and spot that it's actually a ULIP with high charges disguised as a pure insurance product. You apply it when your bank offers you a pre-approved personal loan, and you can quickly calculate the actual interest cost versus using your emergency fund or negotiating a salary advance.

Daily money decisions

Your financial literacy determines how you handle routine transactions that most people don't think twice about. When you choose between paying via credit card, UPI, or debit card, you're making a decision that affects your cashback, reward points, and transaction security. You apply this knowledge when splitting restaurant bills, understanding that payment apps charging convenience fees might cost more than the rewards you earn.

Budget allocation requires you to balance multiple priorities simultaneously, from monthly groceries and rent to SIP investments and insurance premiums. You need to know when to use your credit card float strategically versus when you're just delaying inevitable payments and risking interest charges.

Financial literacy turns autopilot spending into conscious choices that align with your actual priorities and long-term goals.

Planning for major life events

Understanding why financial literacy is important becomes crystal clear when you face big financial decisions like buying property, funding your child's education, or planning your parents' medical care. You need to evaluate home loan options beyond just EMI amounts, considering processing fees, prepayment charges, and the total interest outgo over 20 years. Wedding planning requires you to balance tradition with financial reality, knowing when gold purchases make sense versus when they're just emotional spending that could be better allocated to investments.

How to build financial literacy step by step

Building financial literacy doesn't require you to enroll in an MBA program or spend hours reading textbooks. You start where you are, with your current income and expenses, and gradually expand your knowledge as you encounter new financial situations. The process works best when you combine learning with action, applying concepts immediately rather than waiting until you've mastered theory. Your first step involves getting clear on your present financial position, then systematically adding skills as you need them for specific goals or decisions.

Start with your current financial situation

Your financial education begins with tracking every rupee you earn and spend for at least one month. Download your bank statements, credit card bills, and UPI transaction history to see where your money actually goes, not where you think it goes. This exercise reveals spending patterns you weren't aware of, like ₹3,000 monthly on food delivery or ₹5,000 on subscriptions you barely use.

Calculate your net worth by listing all assets (savings accounts, investments, EPF balance) and subtracting all liabilities (credit card debt, loans, EMIs). Understanding this baseline helps you measure progress and identify immediate problems like negative cash flow or excessive debt.

Learn through practical application

You build real competence by applying concepts to your own money rather than consuming endless content. When you need to choose between tax regimes, research that specific decision, calculate both scenarios with your actual numbers, and make the choice. Each financial decision becomes a learning opportunity that sticks because it affects your wallet directly.

Financial literacy grows fastest when you're solving your own money problems rather than studying hypothetical scenarios.

Start asking specific questions about your financial products: What's the expense ratio on your mutual funds? What's your effective interest rate on that personal loan? Why did your tax refund differ from what you expected? Understanding why financial literacy is important becomes obvious when you realize each answer either saves you money or helps you earn more returns.

Common money mistakes and how to avoid them

Most Indians repeat the same financial errors because they see relatives and friends making them, assuming these patterns represent normal behavior. You avoid entire account statements, skip reading insurance policy documents, and invest based on tips from colleagues rather than your own analysis. These mistakes compound over years, costing you lakhs in lost returns, unnecessary fees, and missed opportunities that you can't recover simply by earning more later.

Understanding why financial literacy is important becomes obvious when you see how preventable most money mistakes actually are. You don't need advanced knowledge to avoid them; you just need to recognize the patterns and apply basic principles consistently.

Chasing returns without understanding risk

You see your neighbor bragging about 40% returns from some scheme and immediately want in, without asking about the underlying assets, lock-in periods, or what happens if markets fall. This approach leads you into high-risk investments that don't match your actual risk tolerance, causing you to panic-sell during corrections and lock in losses. Avoid this by evaluating every investment against your specific goals and time horizon, not against someone else's apparent success.

Your focus should stay on asset allocation that matches your risk profile rather than chasing the highest advertised returns. Diversification protects you better than concentration in any single hot investment, regardless of recent performance.

Keeping emergency funds in the wrong place

You either have no emergency fund at all, or you lock it in fixed deposits that penalize early withdrawal or in equity mutual funds that fluctuate when you need stability. This forces you to take expensive personal loans during emergencies, paying 12-18% interest because your money isn't accessible. Fix this by maintaining 6 months of expenses in liquid funds or savings accounts that you can access within 24 hours without penalties.

Your emergency fund exists to prevent emergencies from becoming financial disasters, which means accessibility matters more than returns.

Your next step

You now understand why financial literacy is important and how it directly affects your wealth-building potential and financial security. The knowledge alone won't change your situation; you need to apply it to your actual money decisions, starting today. Begin with one area where you're currently uncertain, whether that's optimizing your tax strategy, rebalancing your portfolio, or finally understanding what you're actually paying in mutual fund fees.

Financial literacy isn't a destination you reach; it's a continuous process of learning, applying, and refining your approach as your income grows and your goals evolve. The difference between reading about concepts and acting on them determines whether you'll build substantial wealth or just stay financially stable. Start with Invsify's AI-powered financial advisor to get personalized insights on your current investments, identify hidden fees you're paying, and receive conflict-free recommendations that put your interests first rather than someone's commission targets.