Zerodha Varsity Personal Finance: Complete Module Guide

Shlok Sobti

Zerodha Varsity Personal Finance: Complete Module Guide

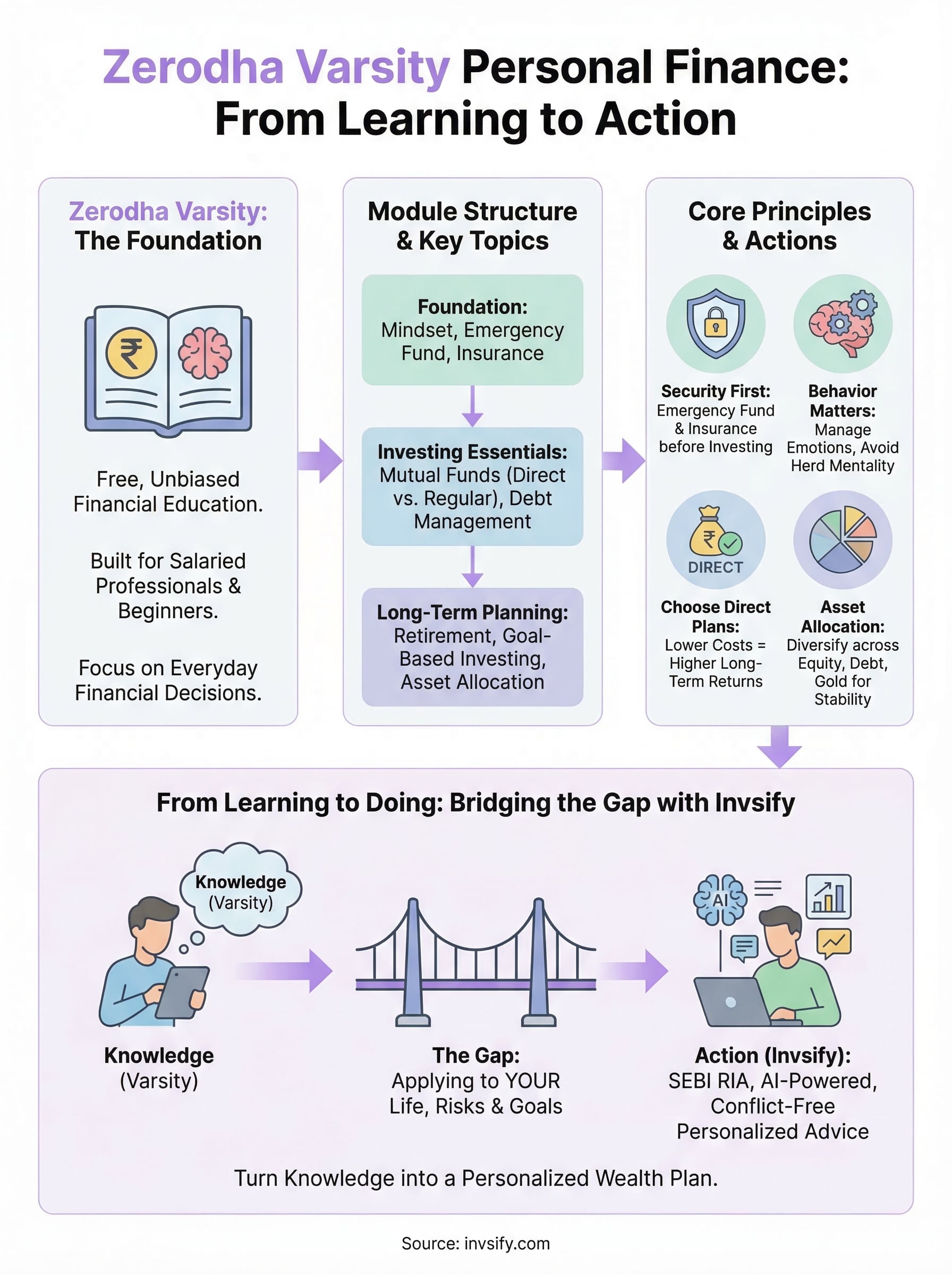

Zerodha Varsity has quietly become one of the most popular free financial education platforms in India, and its personal finance module is where a lot of people start their money journey. If you searched for zerodha varsity personal finance, you're probably looking for a clear breakdown of what the module covers, from mutual funds and insurance to retirement planning and goal-based investing, and whether it's worth your time.

Short answer: yes, it absolutely is. The module does a solid job of explaining foundational concepts that every salaried individual in India should understand. But here's the thing, knowing the theory is only half the battle. The real challenge starts when you try to apply those lessons to your own portfolio, your own risk profile, and your own financial goals. That gap between learning and doing is exactly where most people get stuck.

That's also where a platform like Invsify fits in. As a SEBI Registered Investment Advisor, Invsify uses AI-powered advisory tools to turn the kind of knowledge you'll pick up from Varsity into actionable, personalized recommendations, without the hidden commissions that traditional distributors charge. Think of this guide as your complete walkthrough of the Varsity personal finance module, and think of Invsify as what comes next: putting that knowledge to work.

Let's break down everything the module covers, chapter by chapter.

What Zerodha Varsity personal finance is

Zerodha Varsity is a free financial education platform built by Zerodha, India's largest discount stockbroker by active client base. It was created to give retail investors access to structured, well-written learning material across a wide range of topics, including stock market fundamentals, options trading, technical analysis, and personal finance. The personal finance module sits at the heart of what makes Varsity genuinely useful for salaried individuals in India who want to get their financial life in order before diving into more complex investment strategies.

The platform behind the module

Zerodha originally built Varsity to educate its own users, but the platform quickly grew into something far larger. Today, millions of people across India use Varsity to learn about investing, including people who have never opened a Zerodha account and have no intention of doing so. The platform is completely free and accessible both through its website and a dedicated mobile app. Chapters are written in plain language, supported by real-world examples, illustrations, and downloadable PDFs for those who prefer reading offline.

Varsity works because the content is genuinely educational, with no product being pushed at you. That kind of unbiased writing is rare in the Indian financial media space.

What makes the personal finance module stand out from the rest of the Varsity catalog is its focus on everyday financial decisions, not market speculation. Most people who come to Varsity for the first time are not looking to become full-time traders. They are salaried professionals who want to understand where their money should go, how to protect what they earn, and how to build wealth steadily over time. This module was written specifically for them.

What the personal finance module specifically covers

When you open the zerodha varsity personal finance module, you find content organized around the key pillars of a sound financial life. These include understanding your relationship with money, building an adequate emergency fund, selecting the right insurance products, investing in mutual funds, managing debt responsibly, and planning for long-term goals such as retirement and your children's education. The module covers both the "what" and the "why" behind each concept, which is important because understanding the reasoning behind a financial decision makes you far less likely to abandon it when markets get rough.

The module is not designed to help you pick the next hot stock or time the market. It is built to help you construct a solid financial foundation, the kind that lets you invest with clarity and manage uncertainty without panic. Each chapter starts from the assumption that you have no prior knowledge, so you can follow along whether you are in your first job or your tenth year of working.

Topic Area | What You Learn |

|---|---|

Money mindset | How your behavior and biases shape your financial outcomes |

Emergency fund | How much to set aside and where to park it |

Insurance | Term life, health coverage, and products to avoid |

Mutual funds | Fund types, how to select them, and how to invest |

Debt management | Distinguishing useful debt from harmful debt |

Retirement planning | Estimating your corpus and starting early |

Goal-based investing | Matching investments to specific life goals |

This table gives you a quick overview of the breadth covered, but each area goes well beyond a surface-level summary. The chapters on mutual funds alone run through fund categories, expense ratios, direct vs. regular plans, and how to think about returns in the context of inflation. By the time you finish the module, you have a clear and practical picture of what responsible personal finance looks like in the Indian context, and you know exactly what your next steps should be.

Who the module helps and what you learn

The zerodha varsity personal finance module was written with a specific type of person in mind: someone who earns a steady income, wants to invest wisely, but has never been given a clear and honest roadmap for doing so. If that sounds like you, this module will feel like it was written specifically for your situation.

The people this module was built for

Most personal finance content in India falls into two camps: overly simplified tips that barely scratch the surface, or technical jargon that assumes you already have a finance degree. The Varsity module sits in the space between those two extremes. It targets salaried professionals in their 20s and 30s who are earning reasonably well but still feel uncertain about whether they are saving enough, investing in the right places, or adequately protected against financial setbacks.

You do not need any prior investing experience to benefit from this module. It is equally useful if you are a fresher just starting your first job, someone who has been investing through random tips from Reddit or WhatsApp groups, or a mid-career professional who realizes their finances are scattered and needs to build structure. The module also works well for people who have been investing in traditional instruments like FDs and PPF but want to understand whether mutual funds and goal-based investing might serve them better.

The module's real strength is that it treats you as a capable adult who can handle real information, not someone who needs to be protected from complexity.

What you actually walk away knowing

By the time you finish the module, you will have a working understanding of several areas that most salaried Indians never get formally taught. You will know how to calculate your emergency fund requirement based on your actual monthly expenses, how to evaluate term insurance coverage amounts, and why a direct mutual fund plan consistently outperforms a regular plan over a long investment horizon. These are not abstract concepts; the module ties each one to numbers and real scenarios so you can immediately apply the logic to your own situation.

More importantly, you will understand how to prioritize financial decisions in the right sequence. Most people make the mistake of jumping straight into investing without securing their income, managing high-interest debt, or covering themselves with adequate insurance. The module teaches you the correct order of operations for building a sound financial life. Once you finish, you will have the clarity to make confident decisions rather than defaulting to whatever your colleague or relative recommends.

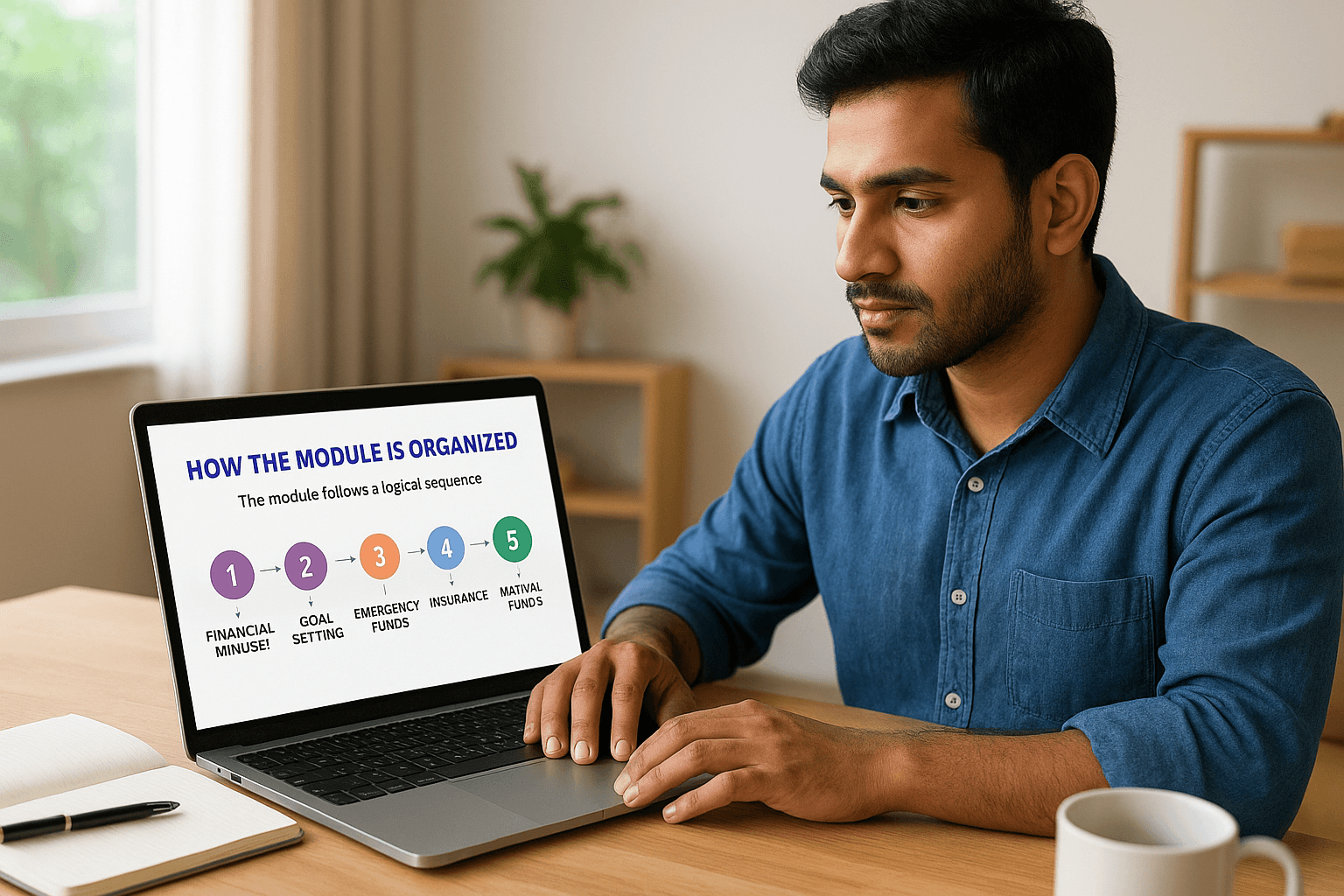

How the module is organized

The zerodha varsity personal finance module follows a logical sequence that mirrors how you should actually build your financial life, starting with your relationship with money and ending with long-term wealth building. This is not a collection of random articles loosely grouped under one label. Each chapter leads into the next, and reading them in order gives you a clear progression rather than disconnected facts. You can jump around if you want, but you'll get the most out of it by starting at the beginning and working forward.

The chapter sequence and what it builds toward

The module opens with chapters on financial mindset and goal-setting, which sets the foundation before anything else. From there, it moves into emergency funds and insurance, which are the two most commonly skipped steps in a typical Indian investor's financial journey. Only after those fundamentals are covered does the module shift into mutual fund investing, asset allocation, and long-term planning.

This sequence matters because skipping to the investing chapters without covering insurance and emergency funds is one of the most common and costly mistakes salaried investors make.

The deliberate order prevents you from making the classic mistake of optimizing for returns before securing your baseline. By the time you reach the chapters on mutual funds and portfolio construction, you already understand why those decisions need to sit on a stable financial foundation.

How each chapter is structured

Each chapter in the module is self-contained but connected to the ones around it. You will typically find an explanation of the concept, followed by worked examples using Indian-specific numbers and scenarios. The chapters avoid abstract theory and instead anchor everything to situations that a salaried professional in India will actually recognize, such as deciding between term plans and endowment policies or figuring out how much SIP contribution is enough for a specific goal.

Most chapters also include key takeaways at the end, which help you confirm that you understood the main points before moving on. The writing is consistent throughout, meaning you won't hit a chapter that suddenly reads like a legal document after a string of plain-language explanations.

Offline access and learning tools

Varsity provides a downloadable PDF version of the personal finance module, which means you can save it to your phone and read through chapters without an internet connection. The mobile app mirrors the web content closely and lets you track your progress through the module. Both formats are free, and neither requires you to have a Zerodha trading account to access them. You simply open the platform, navigate to the personal finance module, and start reading.

Core ideas the module teaches

The zerodha varsity personal finance module is built around a handful of core principles that connect every chapter together. These are not just interesting concepts; they are the mental frameworks you will return to again and again every time you make a financial decision. Understanding these ideas early will help you read the rest of the module with much greater clarity.

Financial security comes before wealth building

Most people approach personal finance by asking "where should I invest?" That is actually the wrong starting point. The module is clear that building financial security has to come before you put a single rupee into a mutual fund or equity investment. Your emergency fund and insurance coverage are not optional extras; they are the structural base that everything else rests on. Without them, any investment you make is vulnerable to being liquidated at the worst possible time, during a job loss, a medical emergency, or some other unexpected event.

Investing without insurance and an emergency fund is like building on unstable ground, and the module makes this point clearly and repeatedly.

A practical example the module uses is the impact of a single uninsured medical expense on an otherwise healthy equity portfolio. If you pull money out of the market during a downturn to cover a hospital bill you were not prepared for, you lose both on the withdrawal and on the recovery you miss. This is exactly why the module insists on sequencing your financial decisions in the correct order before you think about chasing returns.

Your behavior shapes your results as much as your strategy does

The module dedicates real attention to financial behavior and money psychology, which most investing guides skip entirely. The core idea here is that even a perfect investment strategy fails if you panic-sell during a market correction, overextend yourself chasing higher returns, or delay starting because you are waiting for the right moment. Your emotional response to uncertainty is one of the biggest variables in your financial outcome, and the module treats it accordingly.

Two behavioral patterns the module highlights are loss aversion (where you feel the pain of losing money more intensely than the satisfaction of gaining the same amount) and herd behavior (where you invest based on what everyone around you seems to be doing). Recognizing these patterns in your own decision-making gives you a meaningful edge. The module does not ask you to become emotionless about money. Rather, it asks you to build systems and habits that reduce the influence of short-term emotion on decisions that play out over decades.

Mutual fund basics covered in the module

The mutual fund chapters in the zerodha varsity personal finance module are among the most practically useful sections in the entire platform. Rather than drowning you in regulatory definitions, these chapters focus on giving you enough working knowledge to make confident fund selection decisions and understand exactly what you are buying when you invest.

How the module explains fund categories

The module breaks mutual funds down into categories based on what they invest in and the risk profile they carry. You learn the difference between equity funds, debt funds, and hybrid funds, and the module explains why each category serves a different purpose in your portfolio. Equity funds are positioned as long-term wealth builders, debt funds as stability providers, and hybrid funds as middle-ground options that blend both characteristics. The explanations stay grounded in scenarios that an Indian salaried investor will recognize, so you are never left trying to translate abstract concepts into real-world decisions.

The module also walks you through sub-categories within equity funds, such as large-cap, mid-cap, small-cap, and flexi-cap funds. Instead of telling you which one is best, it explains the risk and return characteristics of each so you can judge for yourself which category fits your time horizon and tolerance for short-term volatility.

Direct plans vs regular plans and why it matters

This is one of the most important topics the module covers, and it handles it well. The core distinction is simple: regular plans include a distributor commission built into the expense ratio, while direct plans do not. That difference in expense ratio compounds significantly over time because you are paying a higher fee on a growing corpus year after year.

Switching from a regular plan to a direct plan on the same fund can add up to several lakhs of rupees over a 20-year investment horizon, purely by eliminating the distributor markup.

The module supports this point with clear numerical examples that show how a seemingly small difference in annual expense ratio grows into a meaningful gap over a long investment period. Once you see those numbers, the case for direct plans becomes impossible to ignore.

SIPs, NAV, and expense ratios explained clearly

The module explains SIPs (Systematic Investment Plans) not just as a convenient way to invest but as a behavioral tool that removes the temptation to time the market. By investing a fixed amount at regular intervals, you automatically buy more units when prices are lower and fewer when prices are higher, which works in your favor over a long period.

You also get a clear explanation of NAV (Net Asset Value) and how it works, along with a practical breakdown of how expense ratios reduce your real returns and why you should compare them before selecting a fund.

Building a long-term portfolio with asset allocation

The zerodha varsity personal finance module dedicates meaningful space to asset allocation because it is one of the decisions that influences your long-term returns more than almost anything else. Asset allocation simply means deciding how much of your money goes into different types of investments, such as equity, debt, and gold, rather than putting everything into a single asset class and hoping for the best.

What asset allocation actually means

Asset allocation is not about picking individual stocks or funds. It is about dividing your investable money across asset classes in a way that matches your risk tolerance, time horizon, and financial goals. The module explains that each asset class behaves differently under different market conditions. When equity markets fall sharply, debt instruments often hold their value or even appreciate, which is why holding both together reduces the volatility of your overall portfolio without necessarily sacrificing long-term returns.

A portfolio that only holds equity might grow faster in a bull run, but it can also drop 40% in a downturn, which most investors are not emotionally or financially prepared to handle.

The module uses simple numerical examples to show how a 60% equity and 40% debt allocation behaves differently from a 100% equity allocation over a 10-year period. The all-equity portfolio produces higher peak returns but also deeper losses during downturns. The blended allocation smooths out the ride while still generating meaningful growth over time.

How to adjust allocation as your timeline changes

Your asset allocation should not stay fixed for your entire investing life. The module teaches that equity carries higher short-term risk but rewards you handsomely if you hold it long enough, typically 7 years or more. This means a 25-year-old with a 30-year investment horizon can afford to hold a higher proportion of equity than a 55-year-old who will need that money in 5 years for retirement.

The practical approach the module recommends involves gradually shifting your allocation toward safer, income-generating assets as you get closer to needing the money. This process, sometimes called a glide path, removes the risk of a market correction wiping out a large portion of your corpus just before you need to use it.

Life Stage | Suggested Equity Allocation | Reasoning |

|---|---|---|

20s to early 30s | 70% to 80% | Long horizon absorbs short-term losses |

Mid 30s to 40s | 60% to 70% | Balancing growth with emerging responsibilities |

50s and beyond | 40% to 50% | Protecting corpus as retirement approaches |

Understanding this principle gives you a clear framework for reviewing and rebalancing your portfolio at regular intervals rather than reacting to market noise.

Personal finance review: goals, debt, and insurance

The zerodha varsity personal finance module treats goal-setting, debt management, and insurance as a connected trio rather than separate topics you deal with in isolation. Understanding how these three areas interact gives you a much clearer picture of where your money is actually going and where it should go instead. Most salaried investors skip at least one of these areas early on, and that gap tends to show up later as financial stress.

Setting and tracking your financial goals

The module pushes back hard against vague intentions like "save more" or "invest for the future." Instead, it teaches you to define specific, time-bound goals tied to real numbers. Buying a home in 8 years, funding your child's college education in 15 years, or retiring at 58 are all goals you can actually plan for because each one has a target amount and a deadline. Vague goals cannot be planned for, and the module makes this distinction early so you do not waste years investing without direction.

Once you assign a number and a timeline to each goal, you can reverse-engineer exactly how much you need to invest each month to reach it.

Managing debt before it manages you

Not all debt is harmful, but high-interest consumer debt, such as credit card balances and personal loans, can quietly destroy the returns you are working hard to build through investments. The module draws a clear line between productive debt like a home loan, which builds an asset and carries a relatively low interest rate, and destructive debt that costs you 24% or more per year in interest. Carrying the second type while simultaneously investing in equity funds that return 12% annually means you are losing money in net terms, even while your portfolio grows.

The module recommends paying off high-interest debt before increasing your investment contributions. This is not obvious advice to most people, but the math supports it clearly.

Insurance: what to buy and what to skip

The module is direct about insurance: term life insurance and health insurance are the two products every earning adult needs. Term insurance gives your family a large, affordable cover that replaces your income if you die unexpectedly, while health insurance protects your savings from being wiped out by a single medical event. Both products are straightforward and relatively inexpensive when you buy them young.

The module is equally direct about what to avoid. Endowment plans, ULIPs, and money-back policies combine insurance with investment in a way that delivers poor returns on both fronts. The module explains why separating your insurance and investment decisions almost always produces better outcomes than bundling them into a single product.

How to use the lessons in real life

Reading the zerodha varsity personal finance module is a good start, but the real value comes when you connect what you read to your actual financial situation. Most people finish a few chapters, feel informed, and then go back to doing exactly what they were doing before. That gap between understanding and action is where most personal finance journeys stall. The way to close that gap is to treat each chapter as a direct prompt for a specific action, not as general information you might use someday.

Start with a financial snapshot

Before you apply anything from the module, you need a clear picture of where you currently stand. Pull together your monthly income, all regular expenses, existing investments, outstanding loans, and current insurance coverage. Write these down in a simple spreadsheet or even on paper. You cannot set meaningful goals or identify what is missing until you see everything in one place.

Once you have that snapshot, run it against the module's framework. Check whether your emergency fund covers at least 6 months of expenses, whether your term insurance coverage is adequate relative to your income and liabilities, and whether you are carrying any high-interest debt that should be cleared before you add more investments. This exercise takes an hour at most, and it immediately shows you where your priorities should sit.

The snapshot is not about judgment; it is about getting accurate information so your next financial decision has a solid basis behind it.

Build one habit before adding another

The module covers a lot of ground, and it is tempting to try to fix everything at once. That approach rarely works. Instead, pick one concrete action from each section and complete it fully before moving on. If the insurance chapter showed you that your term cover is insufficient, sort that out first. Once it is done, move to the next item on your list.

This sequenced approach matches the logic the module itself uses. Each financial decision you make depends on the ones before it being in place, so rushing past the foundation to work on returns will cost you more than the delay of doing things in order.

Use the module as a reference, not just a course

After your first read-through, keep the module accessible for ongoing reference. When you are about to make a financial decision, whether it is choosing between two mutual funds or deciding how much to invest in an NPS account, go back to the relevant chapter and re-read it with your specific question in mind. The module was written to be practical and reusable, which means it gives you more value the second time through than it did the first.

FAQs about Varsity access, PDFs, and tools

If you are new to the zerodha varsity personal finance module, you probably have a few practical questions before you dive in. The answers are straightforward, and knowing them upfront will save you time and help you get the most out of the platform from your first session.

Is Zerodha Varsity free to use?

Yes, Varsity is completely free. There are no subscription fees, no paywalled chapters, and no premium tiers that lock away the useful content. Every module, including the full personal finance section, is accessible to anyone without paying a single rupee. Zerodha built the platform to educate retail investors, and that open-access model has not changed since the platform launched.

Can you download the personal finance module as a PDF?

You can. Varsity provides official PDF downloads for its modules directly through the platform. On the web version, you will find the download option within each module. These PDFs are well-formatted and include the same content, examples, and explanations you find online. Downloading the offline version is particularly useful if you want to read through chapters on a commute or refer back to specific sections without needing an internet connection.

The PDF versions are especially helpful for revisiting chapters on insurance or mutual fund selection when you are actively making a financial decision and want the reasoning in front of you.

Do you need a Zerodha account to access Varsity?

No, you do not need a Zerodha trading or demat account to access Varsity. The platform is completely independent of Zerodha's brokerage services. You can visit the Varsity website, read every chapter, download PDFs, and use the mobile app without creating any account at all. Some features like progress tracking may require a basic login, but the core content remains freely accessible regardless.

Does Varsity offer any tools or calculators?

Varsity itself focuses primarily on educational content rather than interactive tools. The platform does not include built-in calculators for SIP projections, insurance coverage, or retirement corpus estimation. What it does offer is the conceptual framework and the formulas you need to run those calculations yourself, which builds genuine understanding rather than just giving you a number to copy. For deeper, personalized number-crunching tied to your actual goals and risk profile, you will need to take those inputs to a dedicated financial planning tool or advisor. Reading Varsity gives you the knowledge to ask the right questions; applying that knowledge to your own situation is the step that follows.

Where to go from here

The zerodha varsity personal finance module gives you a strong foundation, from understanding your money mindset to selecting the right mutual funds and building a goal-based portfolio. Reading it carefully will sharpen your thinking around every major financial decision you face as a salaried professional in India. But the module stops at education. It does not know your income, your liabilities, your risk profile, or your specific goals, which means applying what you learned still requires work on your end.

That is exactly the gap Invsify fills. As a SEBI Registered Investment Advisor, Invsify combines AI-powered portfolio analysis with conflict-free advice, so the principles you picked up from Varsity translate into a personalized financial plan built around your actual numbers. No hidden commissions, no generic recommendations. If you are ready to move from learning to doing, start building your personalized wealth plan with Invsify today.